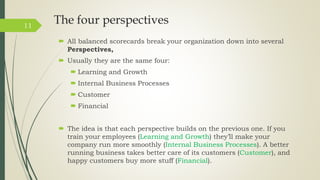

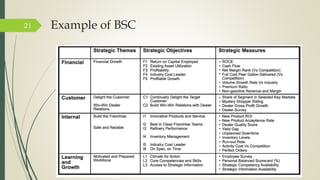

The document discusses the balanced scorecard (BSC) as a strategic planning and management tool. It describes the BSC as having four perspectives - learning and growth, internal business processes, customer, and financial. Strategy maps are used to visually link objectives and measures across the four perspectives to translate strategy into operational terms. The steps to develop balanced scorecards and strategy maps are outlined, including assessing the environment, selecting customer segments, defining value propositions, and identifying key internal processes. Examples of goals for each perspective are also provided.