Downloaded 743 times

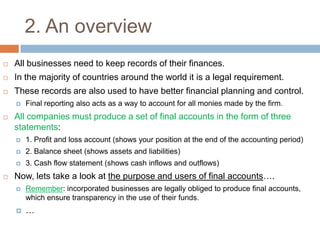

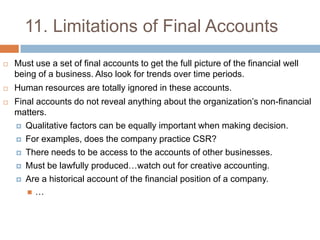

Final accounts are essential financial statements that businesses must produce, including profit and loss accounts, balance sheets, and cash flow statements, to keep track of their financial position and ensure transparency. The income statement shows profit or loss during a trading period, while the balance sheet outlines assets, liabilities, and equity at the end of the trading year. Despite their importance, limitations exist, such as the potential for creative accounting and failure to reflect non-financial factors, necessitating a comprehensive view when assessing a company's financial health.