Downloaded 509 times

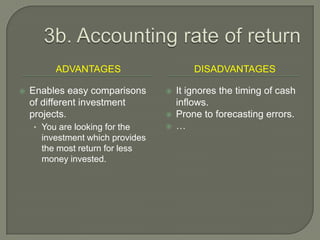

The document discusses investment appraisal methods, focusing on quantitative techniques like payback period and accounting rate of return. It explains the concepts of investments, how payback period calculates the time needed for an investment to recoup costs, and the use of accounting rate of return for comparing investment profitability. Advantages and disadvantages of these methods are also outlined, highlighting their practical applications and potential pitfalls.