Download to read offline

![Gathering Requirements

Bank’s Objectives:

To provide sustainable flow of financial services to less privileged /

poor, including economic empowerment of women and micro-

entrepreneurs.

To arrange capacity building of underserved masses by improving

attitudes, skill, knowledge, social justice and ability to initiate and manage

economically viable projects.

To coordinate, arrange and supervise grants / funds from various persons or

bodies of persons for socio-economic well being of privileged / poor.

To provide loans, advances and other credit facilities for the development of

agriculture and micro market sector including production, marketing and

house-finance facilities.

To mobilize savings by accepting deposits [demand, savings and time

deposits].](https://image.slidesharecdn.com/amblfinallyfinal-120502134344-phpapp02/75/AMBL-7-2048.jpg)

![ Developing brand identity for AMBL [Apna Micro-finance Bank Limited]

including logo[s] for the entity

The identity should reflect AMBL’s “essence”

Easy to comprehend by the target market

Quick brand recall](https://image.slidesharecdn.com/amblfinallyfinal-120502134344-phpapp02/75/AMBL-8-2048.jpg)

![Study the competition

• Other micro-finance organizations

• NGO’s [local and foreign]

• Established “mainstream” banks](https://image.slidesharecdn.com/amblfinallyfinal-120502134344-phpapp02/75/AMBL-9-2048.jpg)

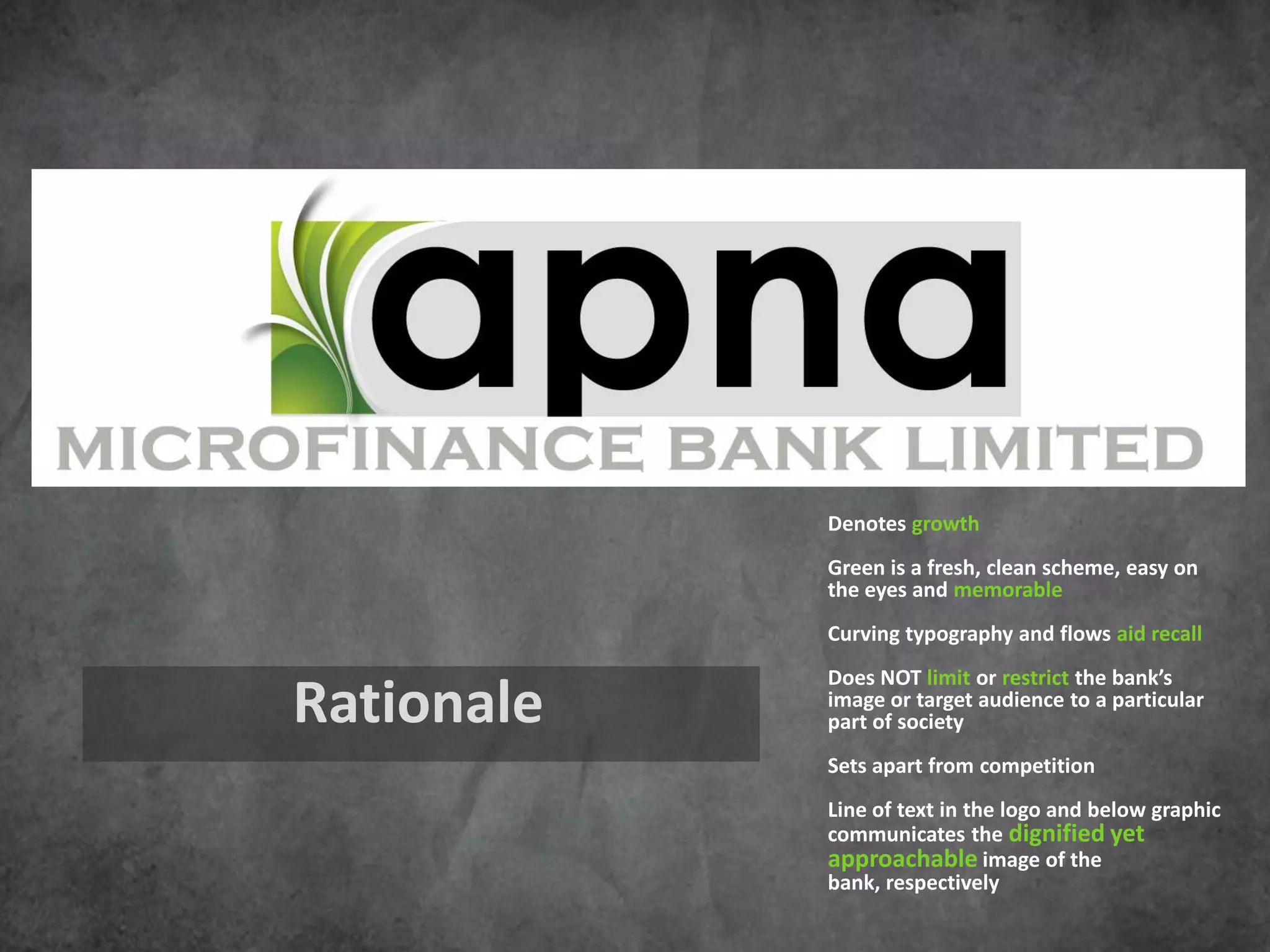

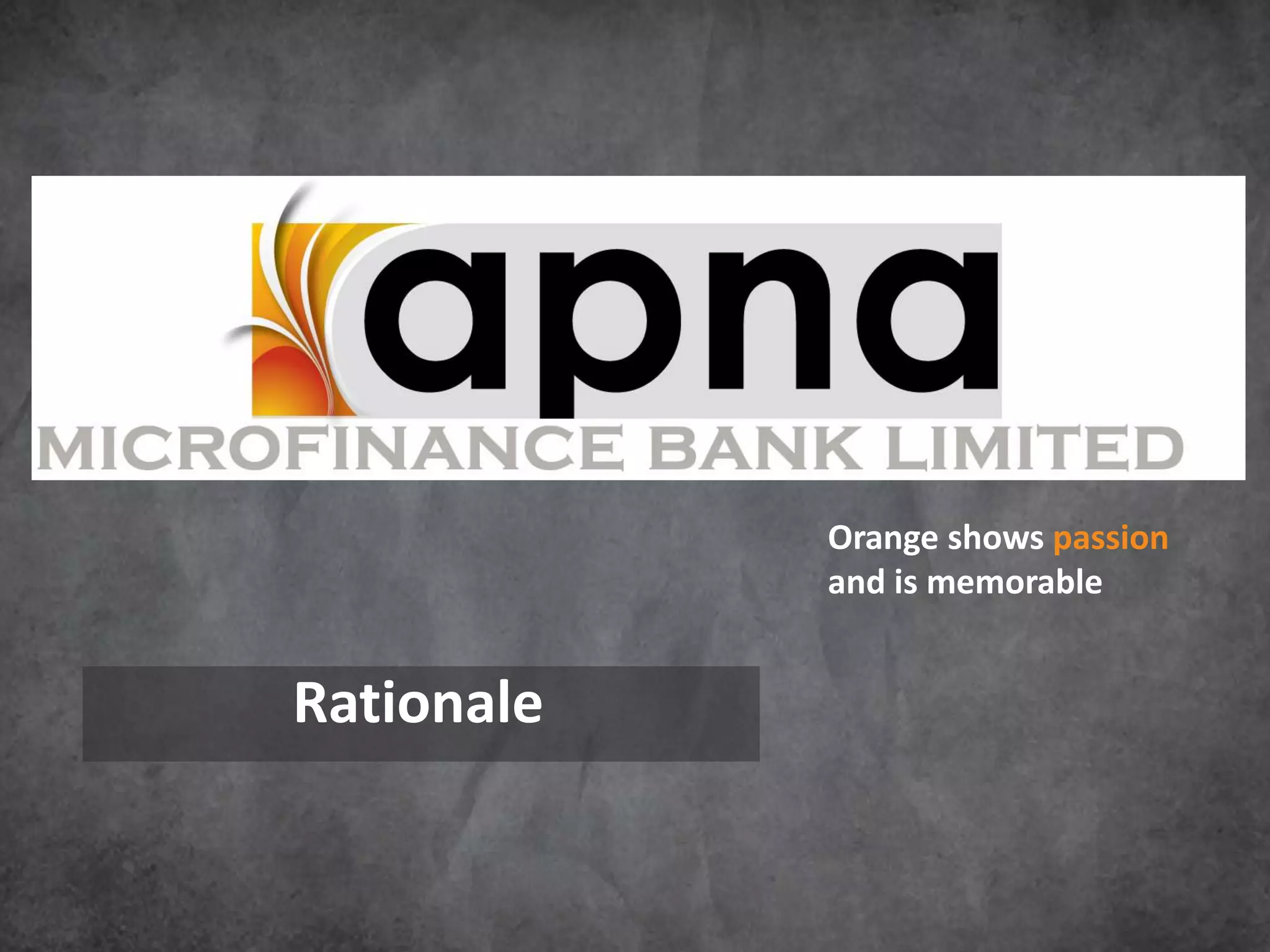

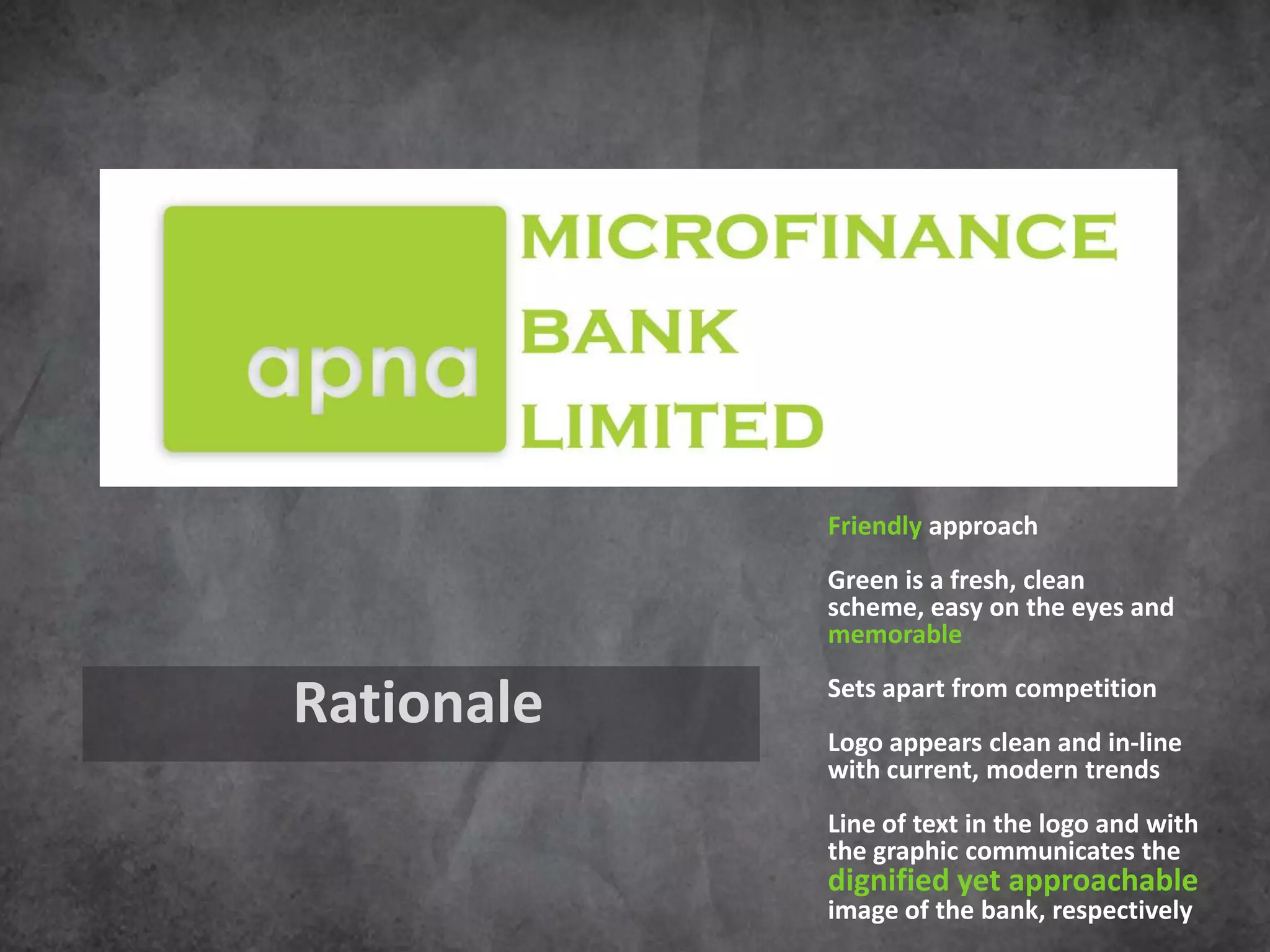

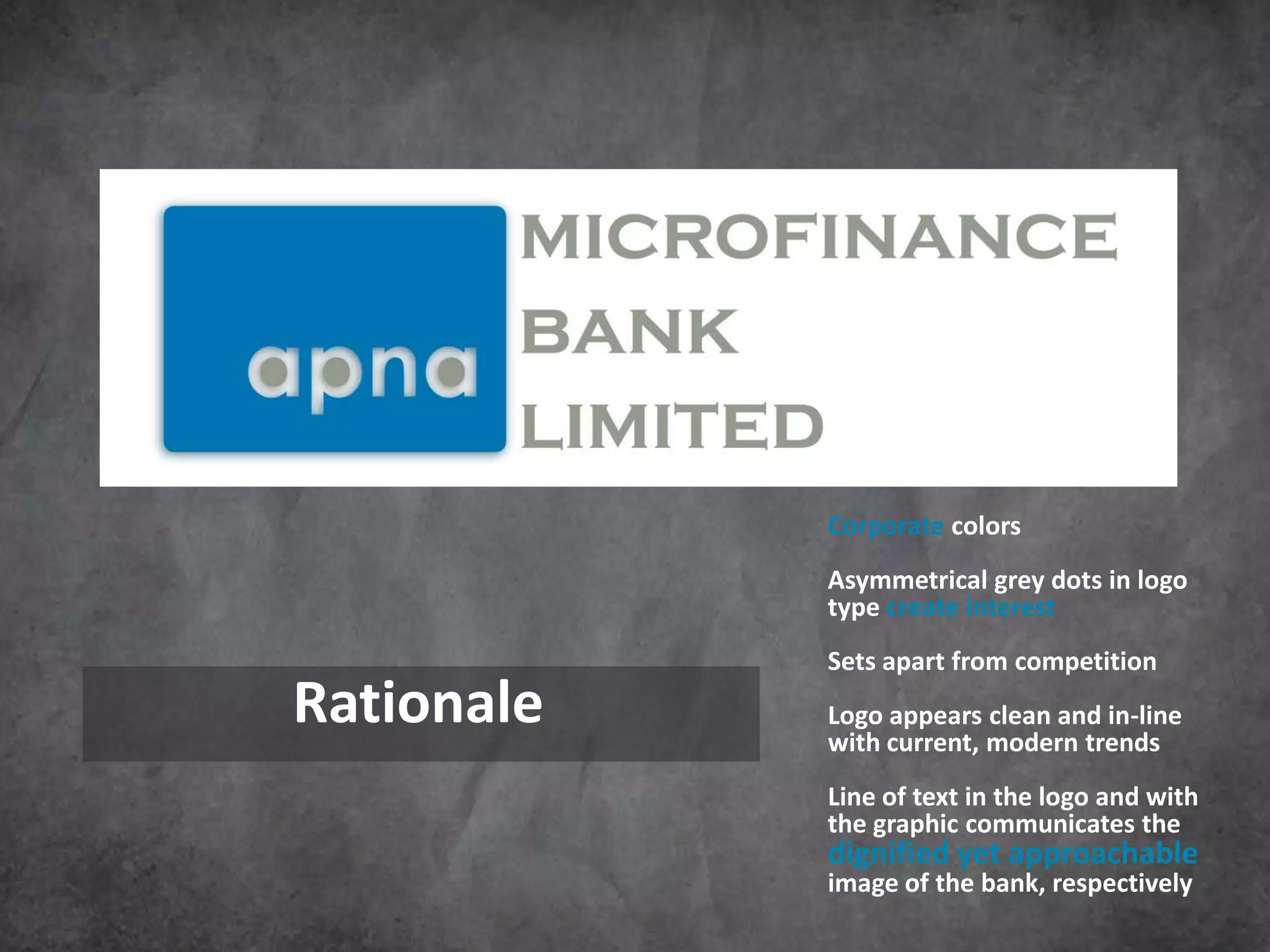

The document outlines the brand identity development process for Apna Microfinance Bank Limited (AMBL), including gathering requirements, studying competition, and developing an identity. It details AMBL's vision, mission, objectives, and philosophy of empowering customers and alleviating poverty. Requirements include providing microfinance and infrastructure in rural and urban areas. Competition includes other microfinance organizations and established banks. Several potential logos are presented that aim to depict growth, passion, and approachability while differentiating AMBL and appearing modern.