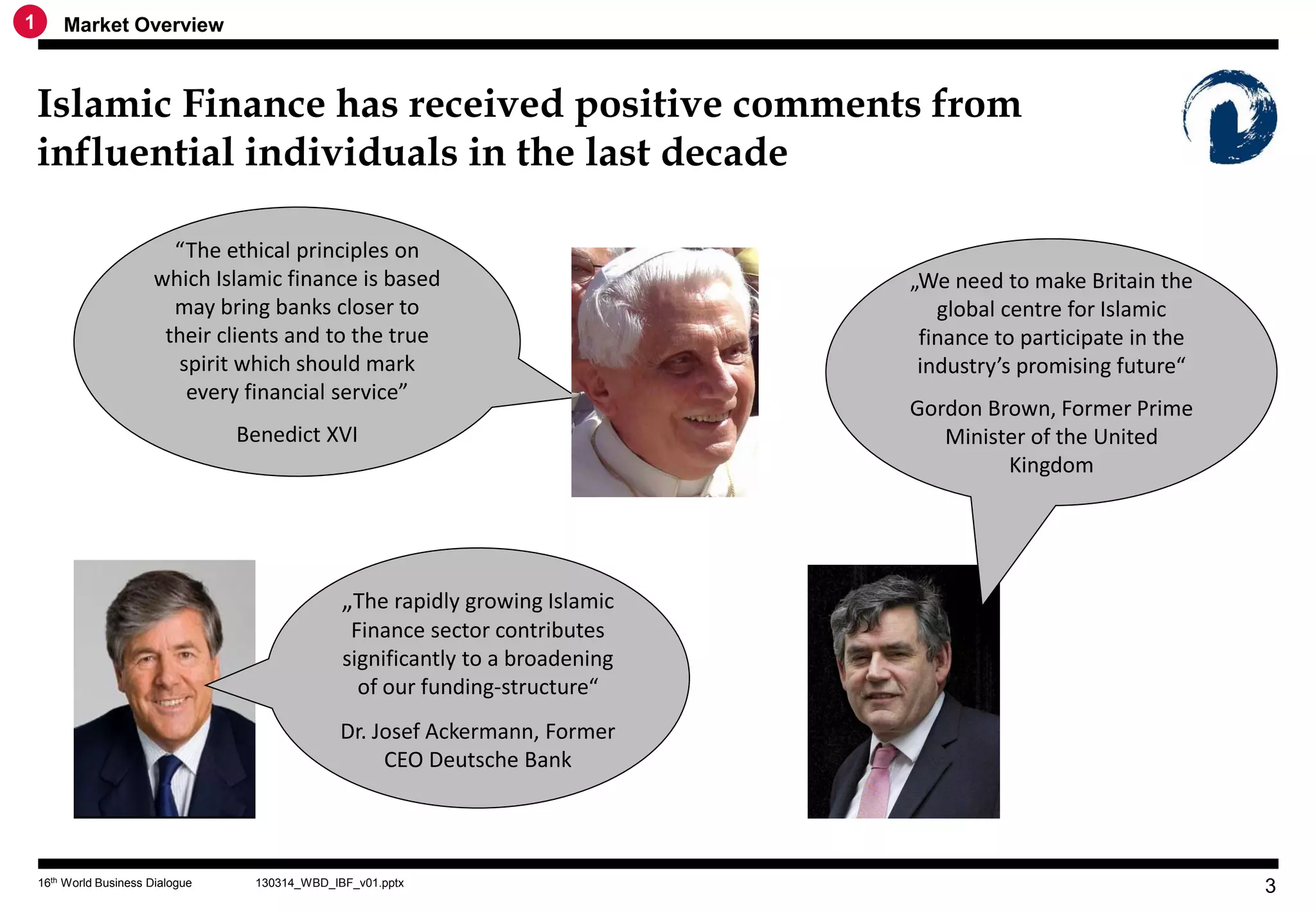

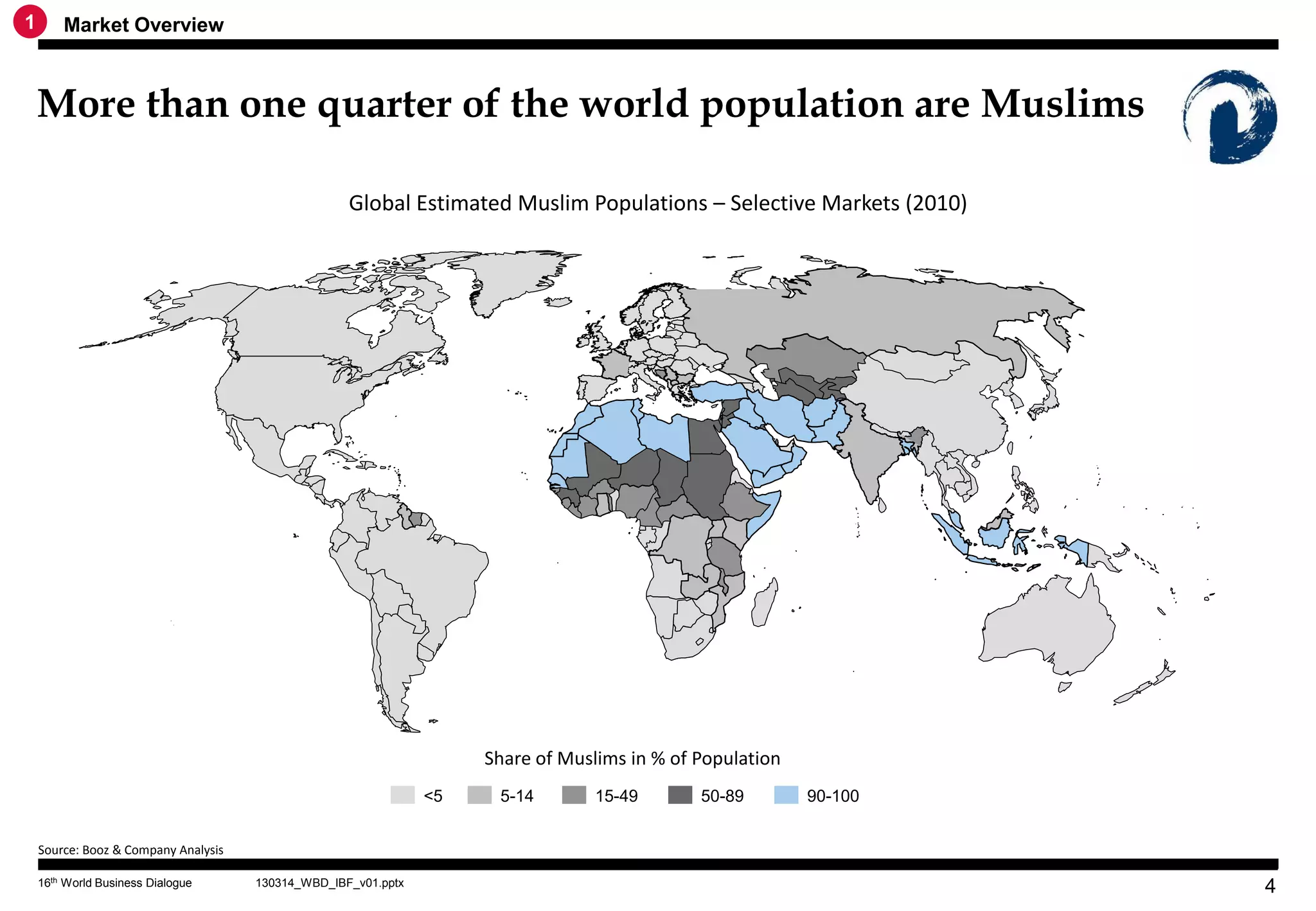

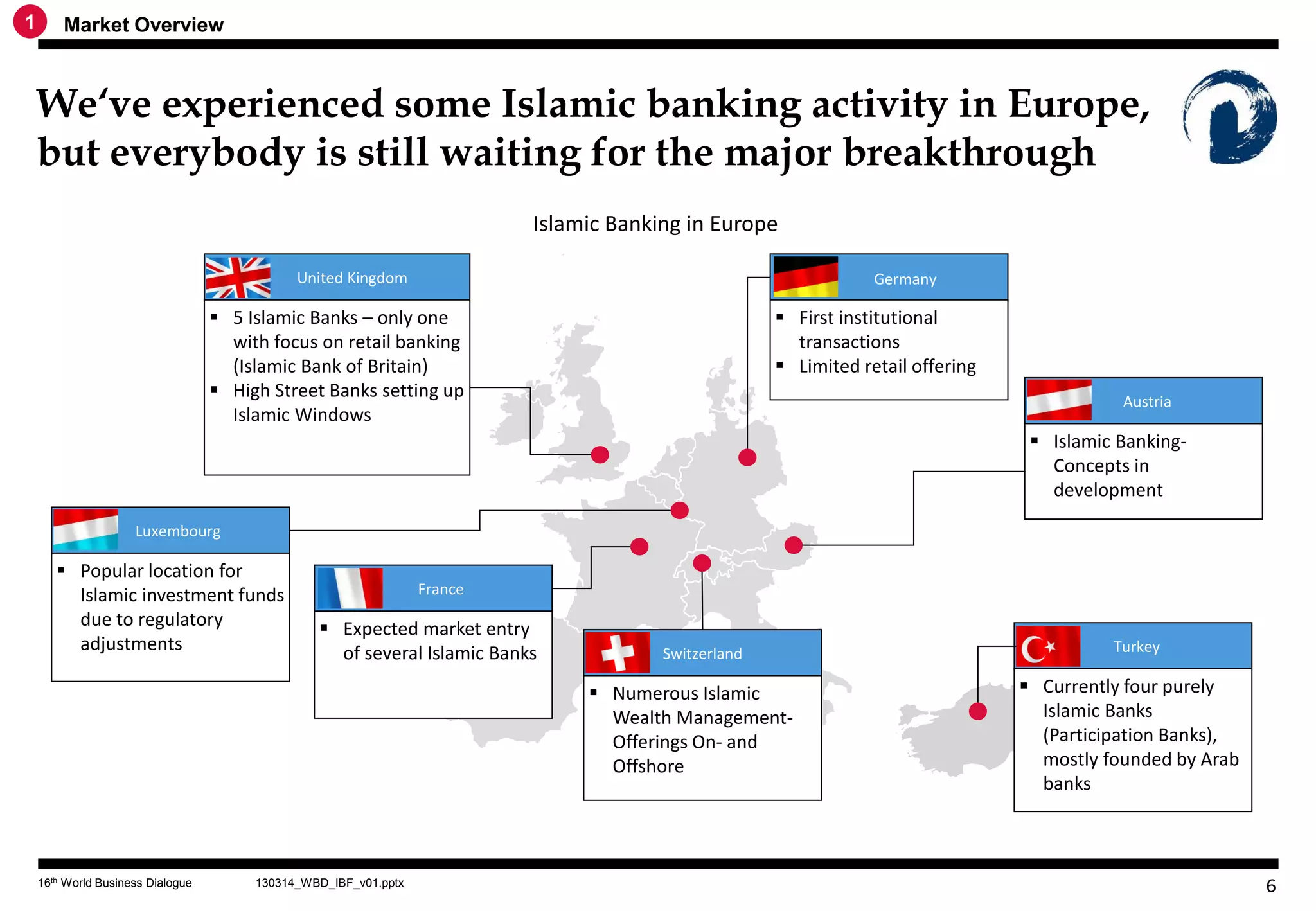

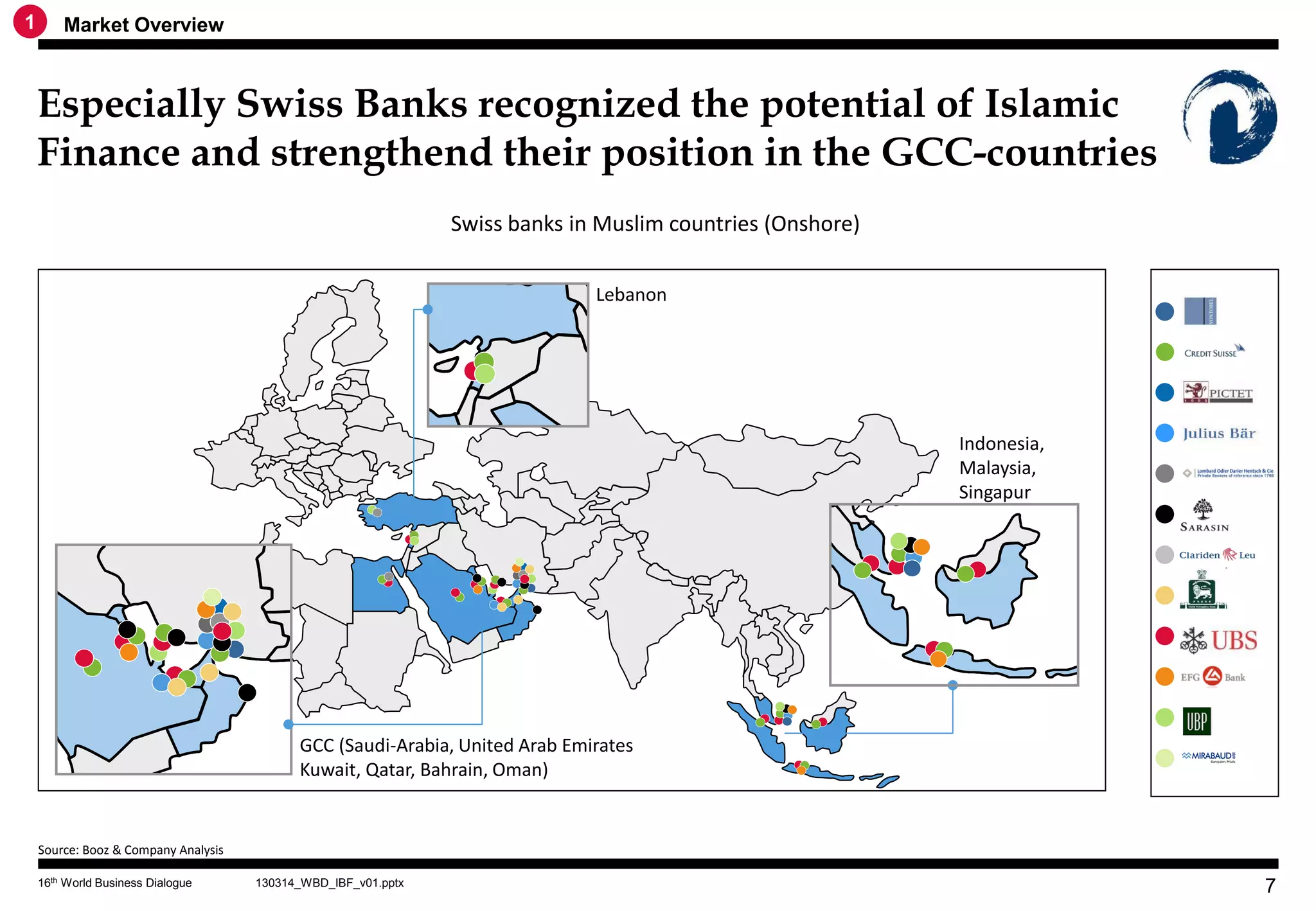

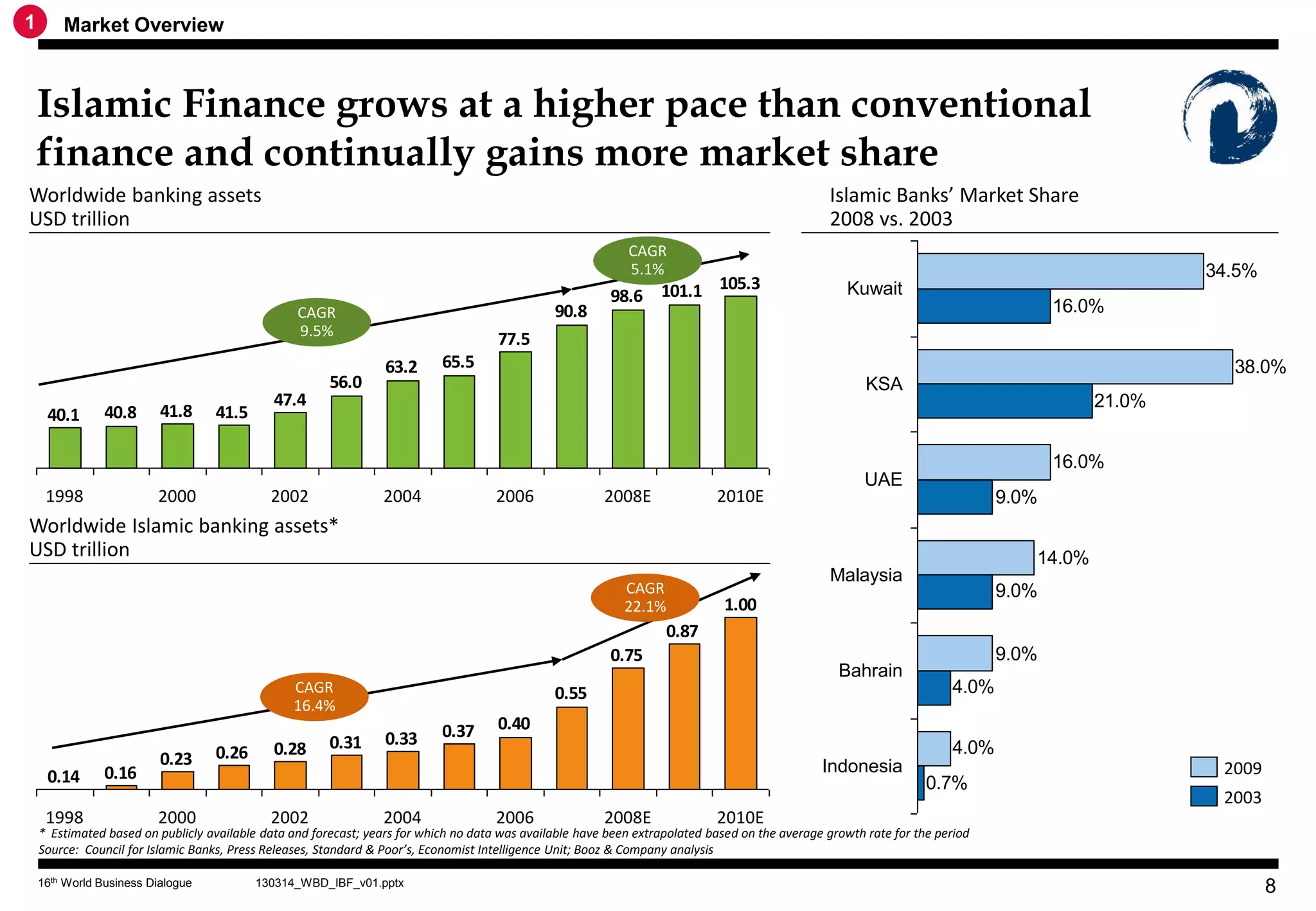

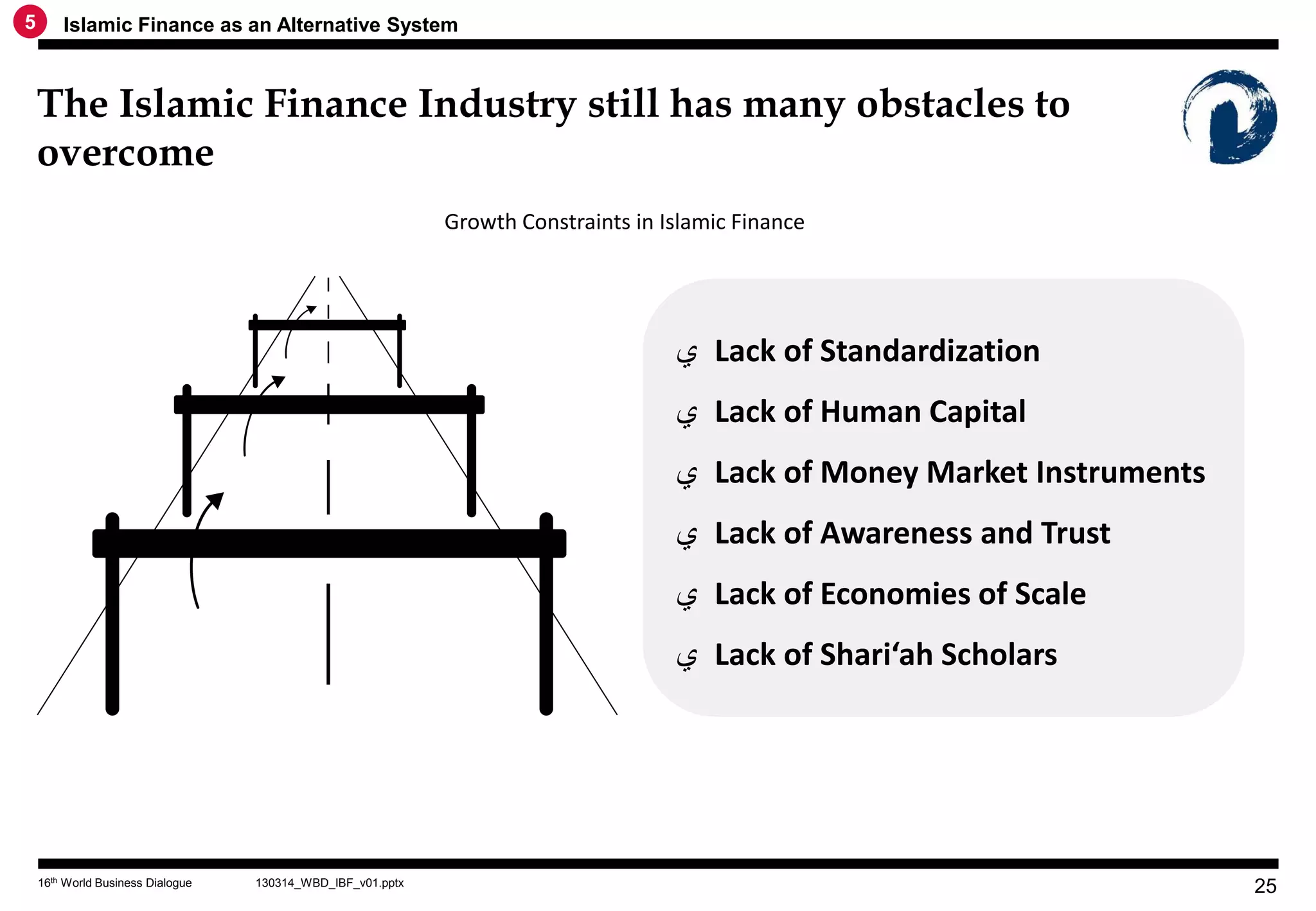

The document discusses the growth and principles of Islamic finance as an alternative banking model compared to conventional finance, emphasizing its ethical underpinnings and increased market presence. It highlights the expanding market, case studies, and key differences in operational structures, such as risk-sharing and prohibition of interest. Additionally, it addresses challenges the sector faces, such as standardization and limited access to Shari'ah scholars.

![3[1]](https://cdn.slidesharecdn.com/ss_thumbnails/31-130204001051-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)