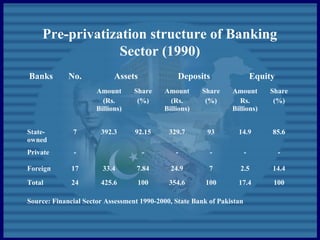

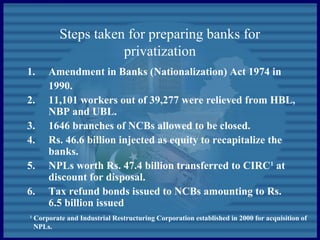

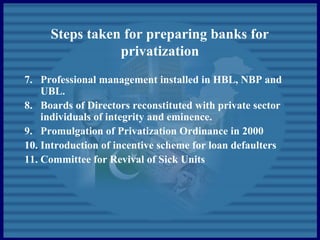

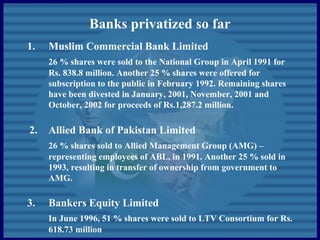

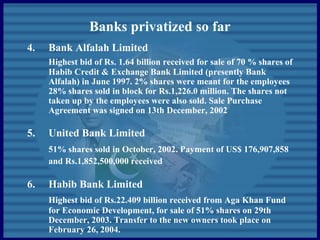

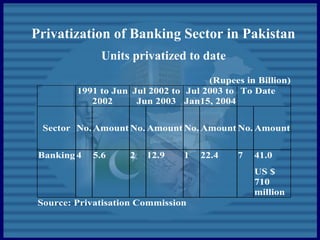

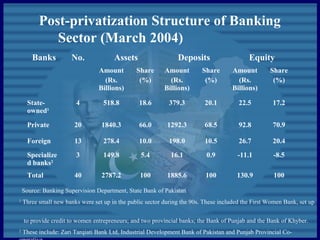

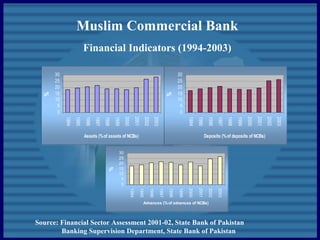

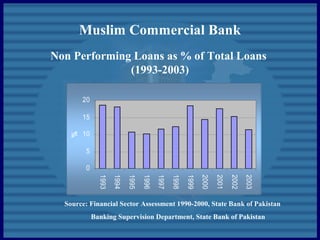

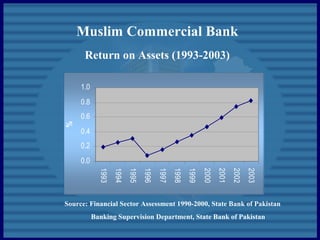

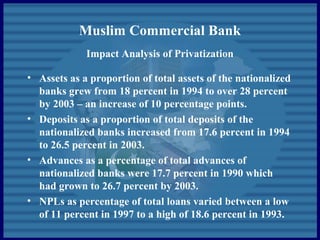

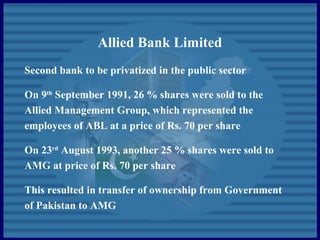

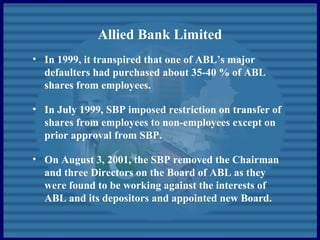

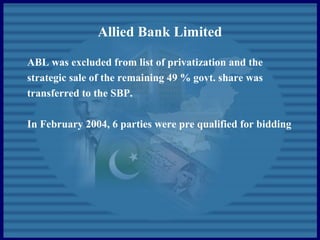

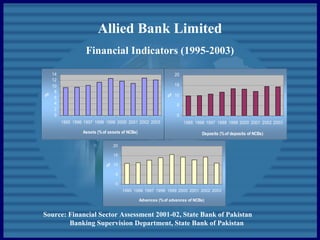

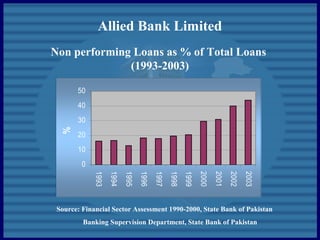

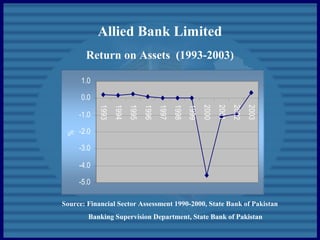

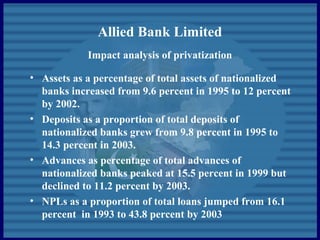

The document discusses policy considerations for bank privatization based on country experiences. It provides background on Pakistan's banking sector nationalization in the 1970s and rationale for privatization in the 1990s, including reducing fiscal deficit and increasing efficiency. Steps taken to prepare banks for privatization included restructuring, recapitalization and transferring non-performing loans. Several banks were privatized through competitive bidding and IPOs, generating over $710 million. Case studies of Muslim Commercial Bank and Allied Bank highlight their financial indicators and impact of privatization.

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)