2

PURPOSE OF BUDGETING(PECCCMAD)

A budget is a quantitative plan prepared for a specific time period. It is

normally expressed in financial terms and prepared for one year.

Budgeting serves a number of purposes:

Planning

Evaluation

Control

Communication

Co-ordination

Motivation

Authorization

Delegation

3.

3

BUDGETING AND PERFORMANCEMANAGEMENT

Budgeting contributes to performance management by

providing benchmarks against which to compare actual results

and develop corrective measures.

Budgets give managers pre-approval for execution of spending

plans and allow them to provide forward looking guidance to

investors and creditors.

Individuals react to the demands of budgeting and budgetary

control in different ways and their behaviour can damage the

budgeting process.

4.

4

APPROACHES TO BUDGETING

There are a number of budgetary systems:

Incremental budgeting

Zero-based budgeting

Rolling budgets

Activity-based budgeting

Top-down budgeting

Bottom-up budgeting

5.

5

FLEXIBLE BUDGETING

Fixedbudget - It is prepared before the beginning of a budget period for a

single level of activity.

Flexible budget – it is prepared for a number of levels of activity and

requires the analysis of costs between fixed and variable elements.

It is prepared at the end of the budget period. It provides a more meaningful

estimate of costs and revenues and is based on the actual level of output.

Budgetary control compares actual results against expected results to

determine the variance which may be favourable or adverse.

A cost is controllable if a manger is responsible for it being incurred or is

able to authorize the expenditure.

Managers should only be evaluated on costs over which they have control.

A notional cost is outside the control of a manager and should not be

included in performance appraised.

7

BEHAVIOURAL ASPECTS OFBUDGETING

Individuals react to the demands of budgeting and budgetary

control in different ways and their behavior can damage the

budgeting process.

Behavioural problems are often linked to management style and

include dysfunctional behaviour and budget slacks.

Budgetary targets will assist motivation and appraisal if they are

at the right level.

Expectations Budget- It is a budget set at current achievable

level.

Aspirations Budgets- It is a budget set at a level which exceeds

the level currently achieved

8.

8

BUDGETING AND PARTICIPATION

•There are basically two ways in which a budget

can be set: from the top down (imposed budget)

or from the bottom up (participatory budget).

9.

9

TOP-DOWN (IMPOSED) BUDGETING

It is a budget set without permitting the ultimate budget user the

opportunity to participate in the budgeting process.

Advantages of Top-Down (Imposed Style):

Involving managers in the setting of budgets is time consuming.

Managers may not have the skills or motivation to participate.

Senior managers have the better overall view of the company and

its resources.

Senior managers are also aware of the long-term strategy of the

company and can prepare budgets which are in line with that.

10.

10

TOP-DOWN (IMPOSED) BUDGETINGCONT.

Managers may build budgetary slack or bias into the

budget in order to make it easier for them to achieve

it.

Managers cannot use budgets to play games which

disadvantage other budget users/holders.

It enhances objectivity.

It discourages pseudo-participation.

11.

11

BOTTOM-UP (PARTICIPATIVE) BUDGETING

It is a budgeting system in which all budget

holders/users are given the opportunity to participate

in setting the budget.

Advantages of participative budgets:

The morale of management is boosted.

Managers are more likely to accept the plans

contained in the budget and strive to achieve them.

Lower level managers have detained knowledge of

their departments than senior managers.

12.

12

INCREMENTAL BUDGETS

Itstarts with the previous year’s budget or actual results and adds or

subtracts an incremental amount to cover inflation and other known

changes.

It is suitable for stable business, where costs are not expected to

change significantly.

Advantages of Incremental

Budgets

Disadvantages of

Incremental Budgets

Quickest and easiest method Builds in previous problems

and inefficiencies

Suitable if the company is

stable and historic figures

are acceptable since only the

increments needs to be

justified

Uneconomic activities may be

continued

managers may spend

unnecessarily in order to use

up their budget.

13.

13

ZERO-BASED BUDGETING (ZBB)

It is a method of budgeting that required each cost element to be specifically

justified, as though the activities to which the budget relates were being

undertaken for the first time.

Without approval, the budget allowance is zero.

It is suitable for allocating resources in areas where spending is discretionary,

and public sector organisations.

There are four distinct stages in the implementation of ZBB.

Managers should specify, for their responsibility centres, those activities that

can be individually evaluated.

Each of the individual activities is then described in a decision package.

Each decision package is evaluated and ranked usually using cost/benefit

analysis.

The resources are then allocated to the various packages

14.

14

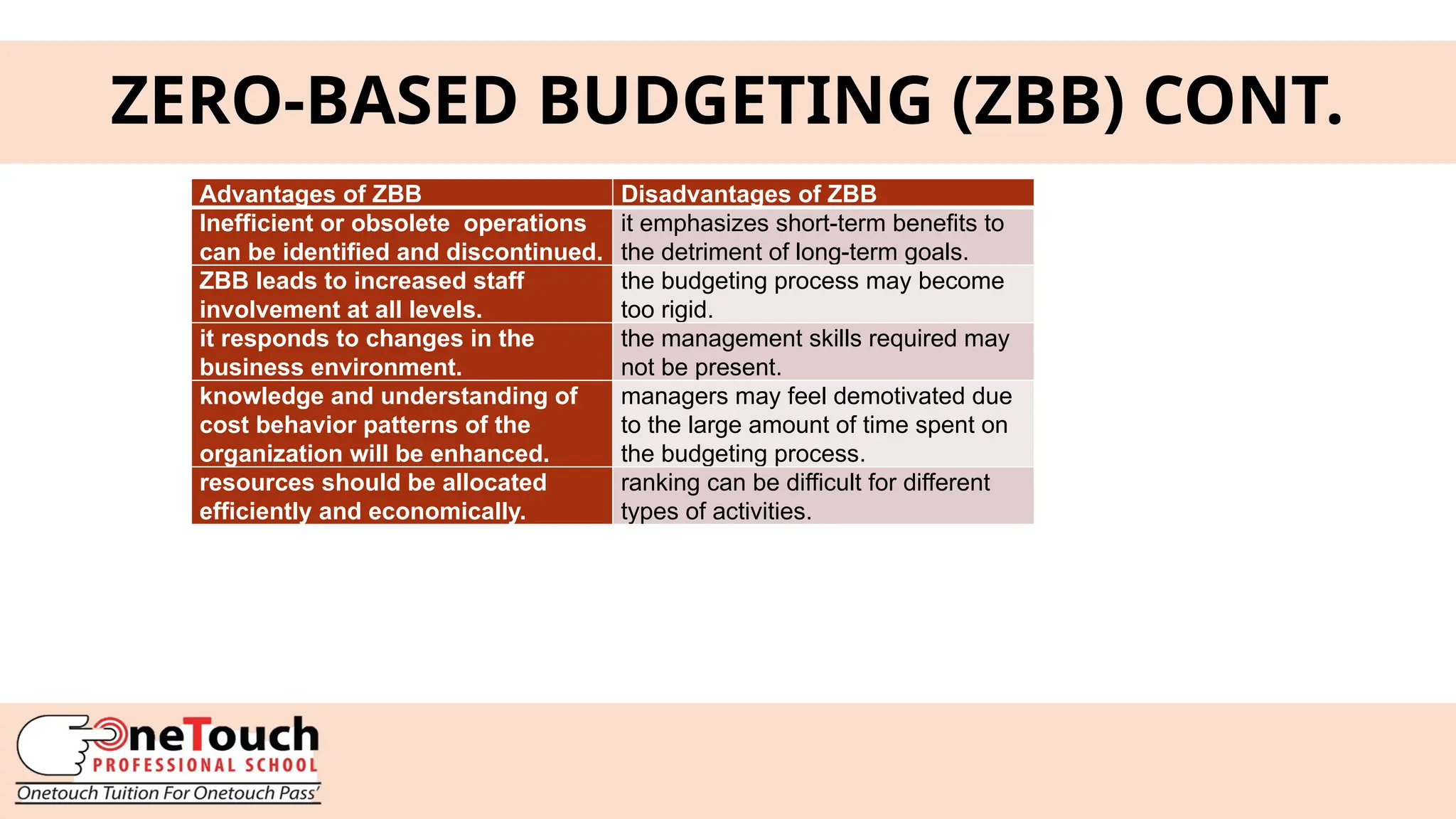

ZERO-BASED BUDGETING (ZBB)CONT.

Advantages of ZBB Disadvantages of ZBB

Inefficient or obsolete operations

can be identified and discontinued.

it emphasizes short-term benefits to

the detriment of long-term goals.

ZBB leads to increased staff

involvement at all levels.

the budgeting process may become

too rigid.

it responds to changes in the

business environment.

the management skills required may

not be present.

knowledge and understanding of

cost behavior patterns of the

organization will be enhanced.

managers may feel demotivated due

to the large amount of time spent on

the budgeting process.

resources should be allocated

efficiently and economically.

ranking can be difficult for different

types of activities.

15.

15

ROLLING BUDGET

Itis a budget (usually annual) kept continuously up to date by adding

another accounting period.

It is suitable if accurate forecasts cannot be made or for any areas of

business that needs tight control.

Advantages of Rolling Budget Disadvantages of Rolling Budget

Planning and control will be based on

a more accurate budget.

More costly and time consuming.

It reduces the element of uncertainty

in budgeting

May demotivate employees if they feel

they spend too much time budgeting.

There is always a budget that extends

into the future.

There is the danger that the budget may

become the last year’s budget “plus or

minus a bit”.

It forces management to reassess the

budget regularly.

An increase in budgeting work may lead

to less control of the actual results.

Issues with version control, as each

month the full year numbers will change

17

ACTIVITY BASED BUDGETING(ABB)

It is a method of budgeting based on an activity framework and

utilizing cost driver data in the budget-setting and variance feedback

processes.

It is the preparing of budgets, using overhead costs from activity-

based costing methodology.

Advantages of ABB Disadvantages of ABB

It draws attention to the costs of

‘overhead activities” which can be a

large proportion of total operating

costs.

A considerable amount of time and effort

might be needed to establish the key

activities and their cost drivers.

It recognized that if is activities which

drive costs.

It may be difficult to identify clear

individual responsibilities for activities.

It can provide useful information in

TQM environment.

It could be argued that in the short-term

many overhead costs are not

controllable and do not vary directly with

activity levels.

18.

18

BUDGET MANUAL

There shouldbe a budget manual or budget handbook to guide everyone involved

in the budgeting process. This should set out:

The key objectives of the budget.

Budget planning procedures and budget timetables.

The budget details that must be included in the functional budgets.

Responsibilities for preparing the functional budgets.

Details of the budget approval process. The budget must be approved by the

budget committee and then by the board of directors.

19.

19

THE MASTER BUDGET

The“master budget” is the final approved budget. It is usually presented in

the form of financial statements (a budgeted statement of profit or loss and a

budgeted statement of financial position).

It is the result of a large number of detailed plans, many of them prepared at

a departmental or functional level.

20.

20

FUNCTIONAL BUDGETS

A functionalbudget is a budget for a particular aspect of the entity’s operations. It

varies with the type of business and industry. In a manufacturing company,

functional budgets should include:

A sales budget.

A production budget

A budget for production resources and resource costs (such as a materials cost

budget and a labour cost budget).

A material purchasing budget

An expenditure budget for every overhead cost centre and general overhead

costs.

21.

21

PRINCIPAL BUDGET FACTOR

Thebudgeting process begins with the preparation of functional budgets,

which must be coordinated and consistent. The first functional budget that

should be prepared is the budget for the principal budget factor.

Normally, the principal budget factor (or key budget factor) is the expected

sales demand.

22.

22

PROFILED BUDGETS

Most budgetsare prepared to cover a 12-month period and broken down into

months.

Budgetary control involves comparing actual results to a budget and taking

corrective action where needed.

Thus, a budgetary control system will usually compare actual performance for

the month to the budget for the month and actual performance for the year to the

budget for the year.

A profile budget reflects the expected pattern of expenses and income across the

year. This is important, as some parts of a budget do not occur evenly each

month of the year.

23.

23

BEHAVIOURAL FACTORS

Unfortunately, inpractice human behaviour in the budgeting process often has a

negative effect. There are several possible reasons why behavioural factors can be

harmful:

Misunderstanding and worries about cost-cutting.

Opposition to unfair targets set by senior management.

Blame culture.

Sub-optimisation (dysfunctional behaviour).

Budget slack or budget bias,

24.

24

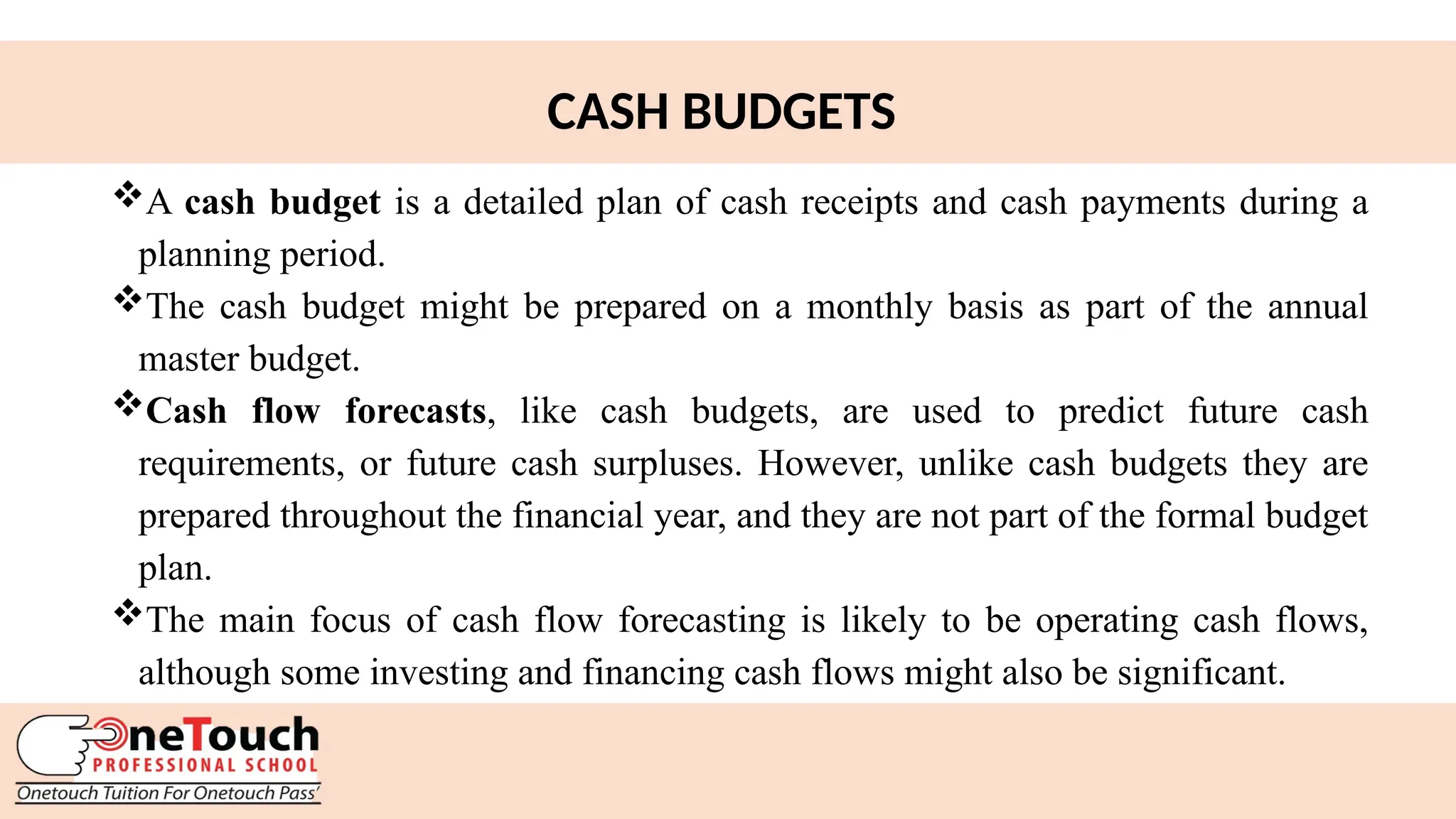

CASH BUDGETS

A cashbudget is a detailed plan of cash receipts and cash payments during a

planning period.

The cash budget might be prepared on a monthly basis as part of the annual

master budget.

Cash flow forecasts, like cash budgets, are used to predict future cash

requirements, or future cash surpluses. However, unlike cash budgets they are

prepared throughout the financial year, and they are not part of the formal budget

plan.

The main focus of cash flow forecasting is likely to be operating cash flows,

although some investing and financing cash flows might also be significant.

25.

25

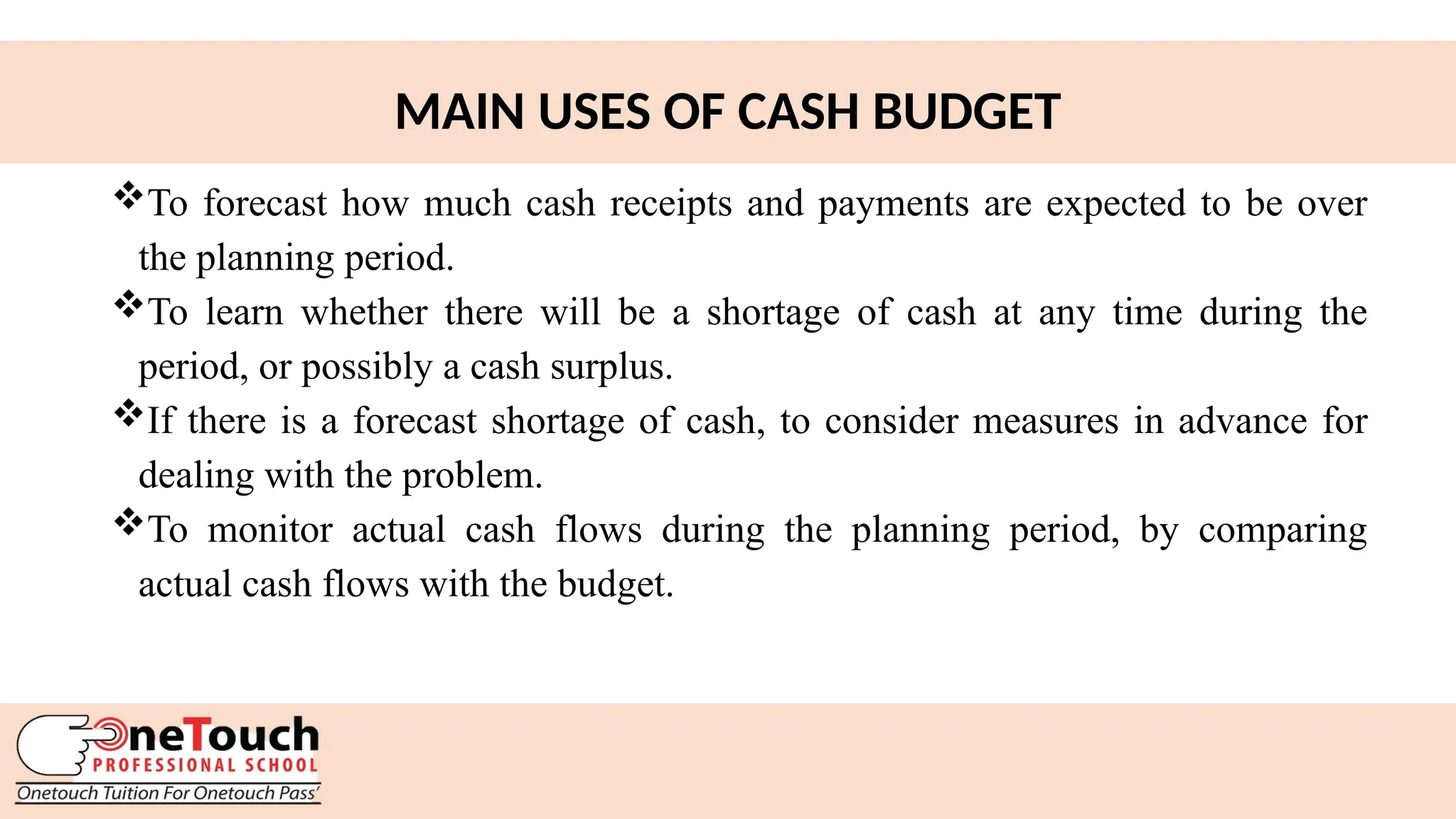

MAIN USES OFCASH BUDGET

To forecast how much cash receipts and payments are expected to be over

the planning period.

To learn whether there will be a shortage of cash at any time during the

period, or possibly a cash surplus.

If there is a forecast shortage of cash, to consider measures in advance for

dealing with the problem.

To monitor actual cash flows during the planning period, by comparing

actual cash flows with the budget.

26.

26

FORMAT OF ACASH BUDGET

Cash receipts: January

GH¢

February

GH¢

March

GH¢

Cash sales 500 600 500

Cash from credit sales 7200 6400 6400

Other cash receipts 400 200 200

Total cash receipts 8100 7200 7100

Cash payments:

Cash purchases 600 660 620

Payments for credit purchases 840 900 990

Rental payments - 3000 -

Wages and salaries 2300 2300 2300

Dividend payments - - 400

Other payments 300 7300 1300

Total cash payments (4040) (14160) (9210)

Net cash flow 4060 (6960) (2110)

Cash balance at the beginning 4500 8560 1600

Cash balance at the end 8560 1600 (510)

27.

27

FORMAT OF SALESBUDGET

Product Budgeted sales

quantity

Units

Budgeted sales

price

GH¢

Budgeted sales

revenue

GH¢

A 200 40 8,000

B 300 50 15,000

Total 23,000

28.

28

FORMAT OF PRODUCTIONBUDGET

Units

Sales budget in units xx

Add: Budget closing inventory of F.G xx

Less: Opening inventory of F.G xx

Production budget xx

29.

29

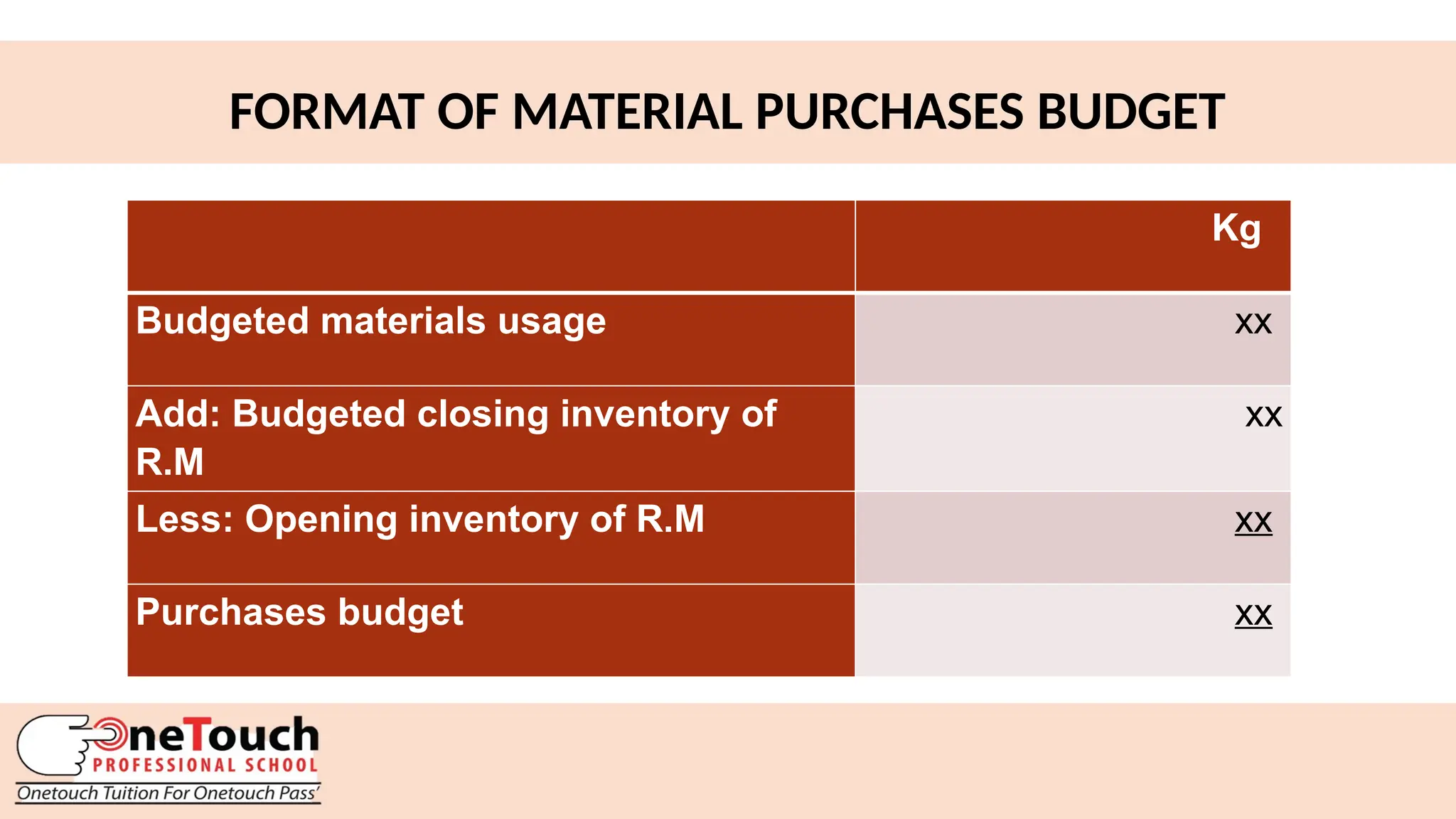

FORMAT OF MATERIALPURCHASES BUDGET

Kg

Budgeted materials usage xx

Add: Budgeted closing inventory of

R.M

xx

Less: Opening inventory of R.M xx

Purchases budget xx

30.

30

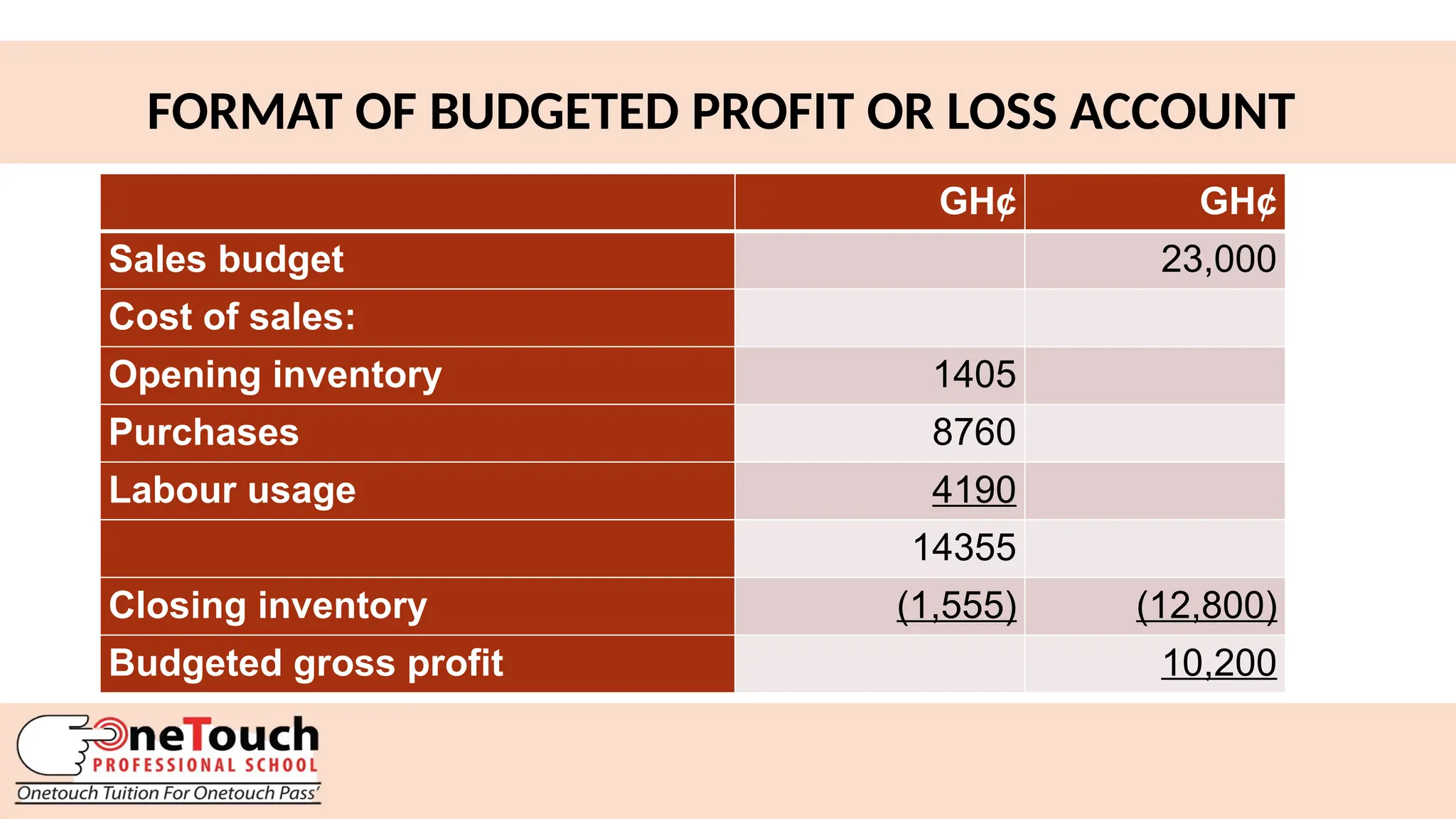

FORMAT OF BUDGETEDPROFIT OR LOSS ACCOUNT

GH¢ GH¢

Sales budget 23,000

Cost of sales:

Opening inventory 1405

Purchases 8760

Labour usage 4190

14355

Closing inventory (1,555) (12,800)

Budgeted gross profit 10,200

31.

31

MATERIALS USAGE BUDGETFORMAT

Total production quantity x materials required per unit.

You may need to gross up the material required per unit so pay attention to

the examiner.