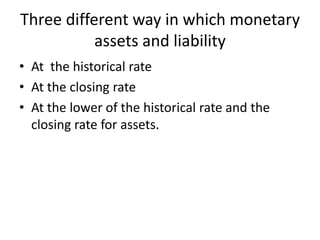

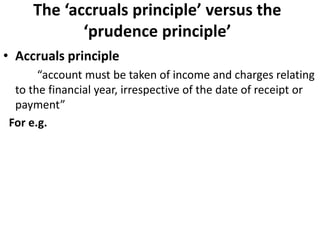

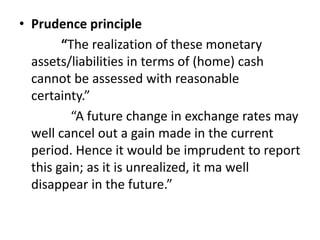

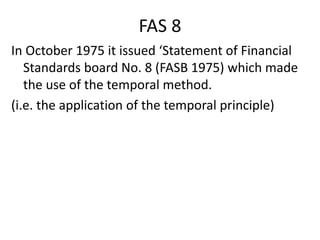

This document discusses foreign currency translation, which is the process of converting financial data expressed in one currency into another currency. It provides definitions and outlines the challenges of currency translation, specifically which exchange rate to use for assets/liabilities and how to account for gains/losses. The key methods discussed are the temporal method, which uses historical exchange rates, and the closing rate method, which uses the rate at the end of the reporting period. International accounting standards like IAS 21 provide guidance on foreign currency transactions and translation of financial statements.