CA Varun Sethi Ind AS 21 - The effects of changes in foreign exchange rates

•

2 likes•1,271 views

Presentation by CA Varun Sethi: Explains through flowboxes - IndAS 21/ IAS 21 - The effects of changes in foreign exchange rates - especially 1. Accounting for Foreign Currency transactions and 2. Accounting for ‘Exchange differences’ on Foreign Currency transactions 3. Foreign currency translations for consolidation procedures (translation of account balances into reporting / presentation currency)

Recommended

More Related Content

What's hot

What's hot (19)

Similar to CA Varun Sethi Ind AS 21 - The effects of changes in foreign exchange rates

Similar to CA Varun Sethi Ind AS 21 - The effects of changes in foreign exchange rates (20)

More from Varun Sethi

More from Varun Sethi (20)

Recently uploaded

Recently uploaded (20)

CA Varun Sethi Ind AS 21 - The effects of changes in foreign exchange rates

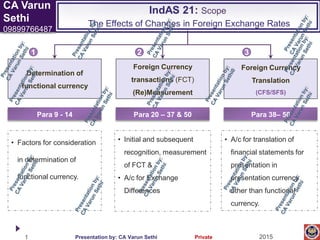

- 1. 20151 Presentation by: CA Varun Sethi Private • Factors for consideration in determination of functional currency. • Initial and subsequent recognition, measurement of FCT & • A/c for Exchange Differences IndAS 21: Scope The Effects of Changes in Foreign Exchange Rates CA Varun Sethi 09899766487 Determination of functional currency Foreign Currency Translation (CFS/SFS) 1 3 Foreign Currency transactions (FCT) (Re)Measurement 2 Para 9 - 14 Para 38– 50Para 20 – 37 & 50 • A/c for translation of financial statements for presentation in presentation currency other than functional currency.

- 2. 20152 Presentation by: CA Varun Sethi Private 1. In Functional currency 2. At Spot /Average Exchange Rate 3. As on transaction date IndAS 21: Para 20 - 26 Accounting for ‘Foreign Currency transactions’ CA Varun Sethi 09899766487 Initial Recognition Subsequent Recognition (Each reporting date) 1 2 Foreign currency Non-monetary items Historical Cost Foreign currency monetary items Fair value NMI Measured at 1. In Functional currency 2. At Closing Exchange Rate 1. In Functional currency 2. At transaction date exchange Rate 1. In Functional currency 2. At FV determination date exchange Rate

- 3. 20153 Presentation by: CA Varun Sethi Private ED Recognized initially in OCI ED Recognized in Income Statement in the period in which they arise IndAS 21: Para 27 - 31 Accounting for ‘Exchange differences’ on Foreign Currency transactions CA Varun Sethi 09899766487 Exchange differences (ED)* on MONETARY ITEMS Exchange differences (ED) on NON MONETARY ITEMS (NMI) 1 2 Hedging Instruments (HI) Gain or Loss on NMI recognized in OCI Other than HI Gain or Loss on NMI recognized in PL *EXCLUDING Exchange differences arising from translation of long-term foreign currency monetary items recognized in the financial statements as of First Time adoption of IndAS

- 4. 20154 Presentation by: CA Varun Sethi Private ED Recognized in Income Statement/ Profit and Loss. ED Recognized in OCI initially IndAS 21: Para 32 – 34, 48 - 49 The Effects of Changes in Foreign Exchange Rates CA Varun Sethi 09899766487 Exchange differences (ED) on MONETARY ITEMS forming part of a reporting entity’s ‘net investment in a foreign operation’ (for which settlement is neither planned nor likely to occur in the foreseeable future) SFS of Parent On *Partial/ Full Disposal* of foreign operation SFS of Foreign operation Before any Disposal of foreign operation • *Disposal = Resulting in loss of control • SFS = Separate Financial Statements • CFS = Consolidated Financial Statements CFS On Partial Disposal NOT resulting in loss of control of foreign operation Re-attribute the proportionate share to NCI Reclassify parent’s share of ED from OCI to profit or loss.