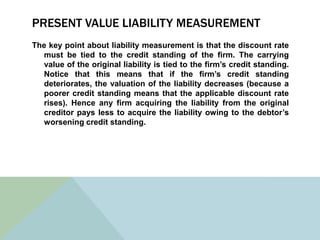

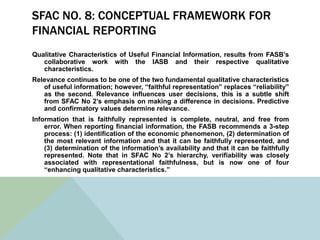

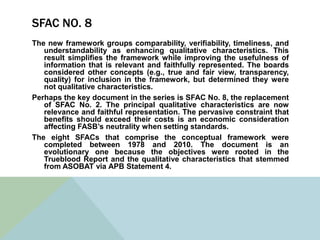

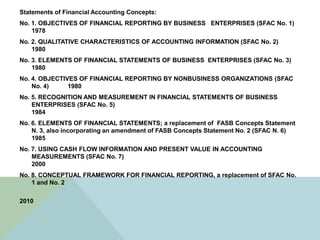

SFAC documents are issued by the FASB to provide broad accounting concepts and definitions that serve as a framework for establishing financial accounting standards. SFAC No. 1 discusses the objectives of financial reporting for business enterprises as providing useful information for economic decision making. SFAC No. 2 addresses the qualitative characteristics of accounting information such as relevance, reliability, and neutrality. SFAC No. 5 and 7 provide guidance on recognition criteria, measurement attributes, and using present value and cash flow information in financial statements.

![Relevance has two main aspects and one minor:

Predictive value, as in previous documents, refers to usefulness of inputs for

predictions, such as cash flows or earning power, rather than being an actual prediction

itself.

Feedback value concerns “confirming or correcting their [decision makers] earlier

expectations.” It thus refers to assessing where the firm presently stands and overlaps

with how well management has carried out its functions.

Timeliness is really a constraint on both of the other aspects of relevance. To be

relevant, information must be timely, which means that it must be “available to decision

makers before it loses its capacity to influence decisions.” There is a conflict between

timeliness and the other aspects of relevance because information can be more

complete and accurate if the time constraint is relaxed.](https://image.slidesharecdn.com/accountingtheory-130317190706-phpapp01/85/Accounting-theory-8-320.jpg)