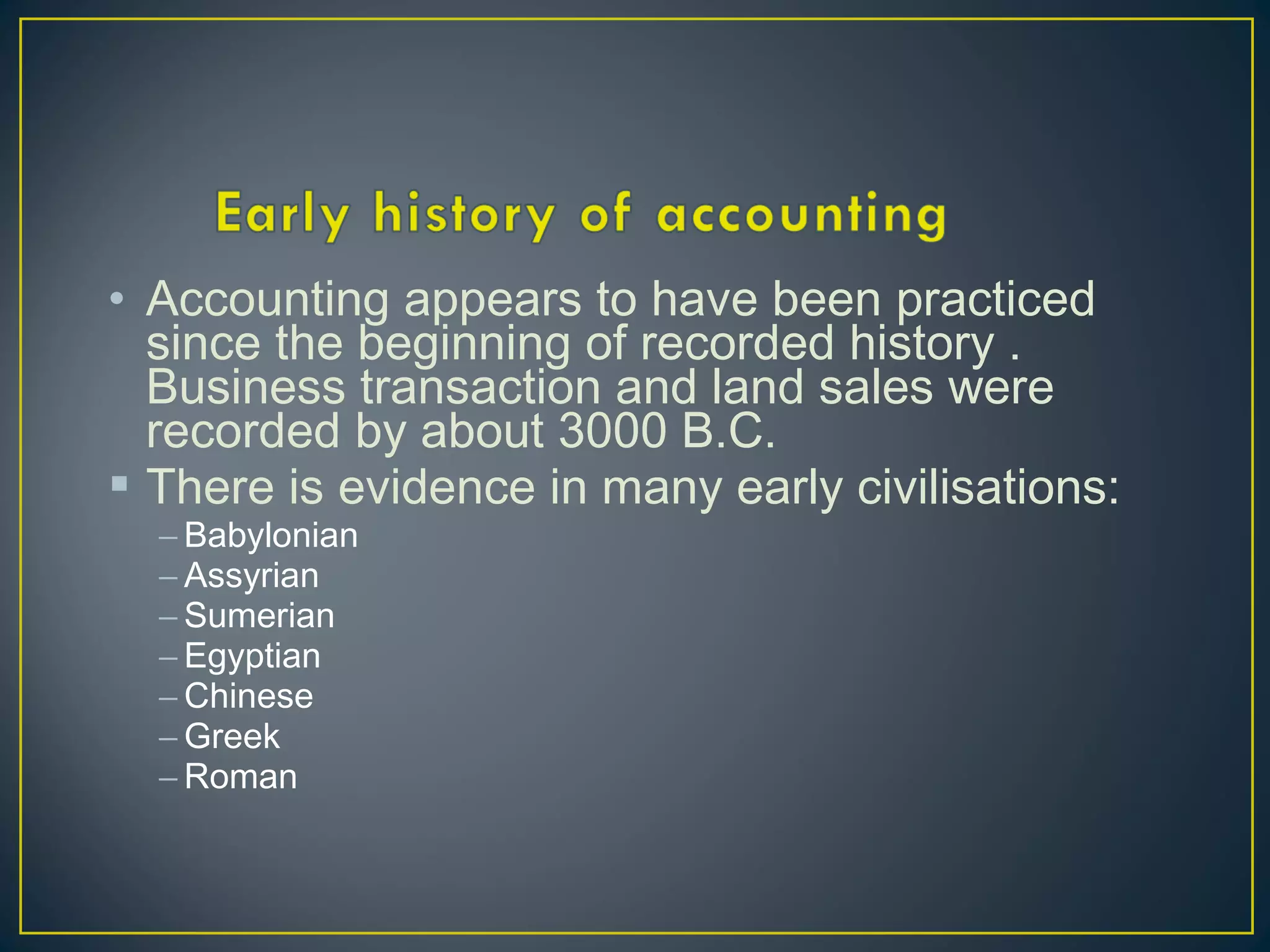

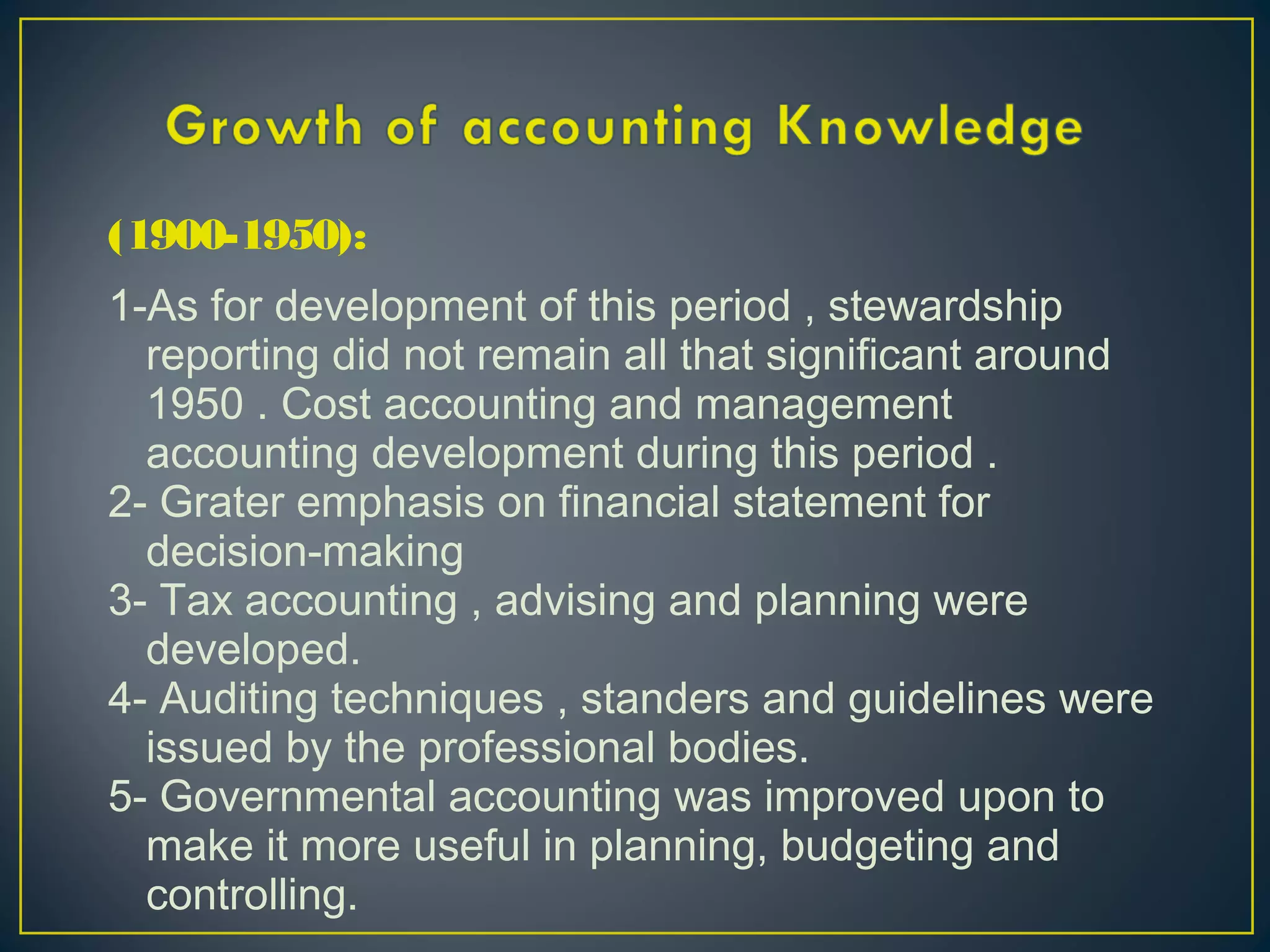

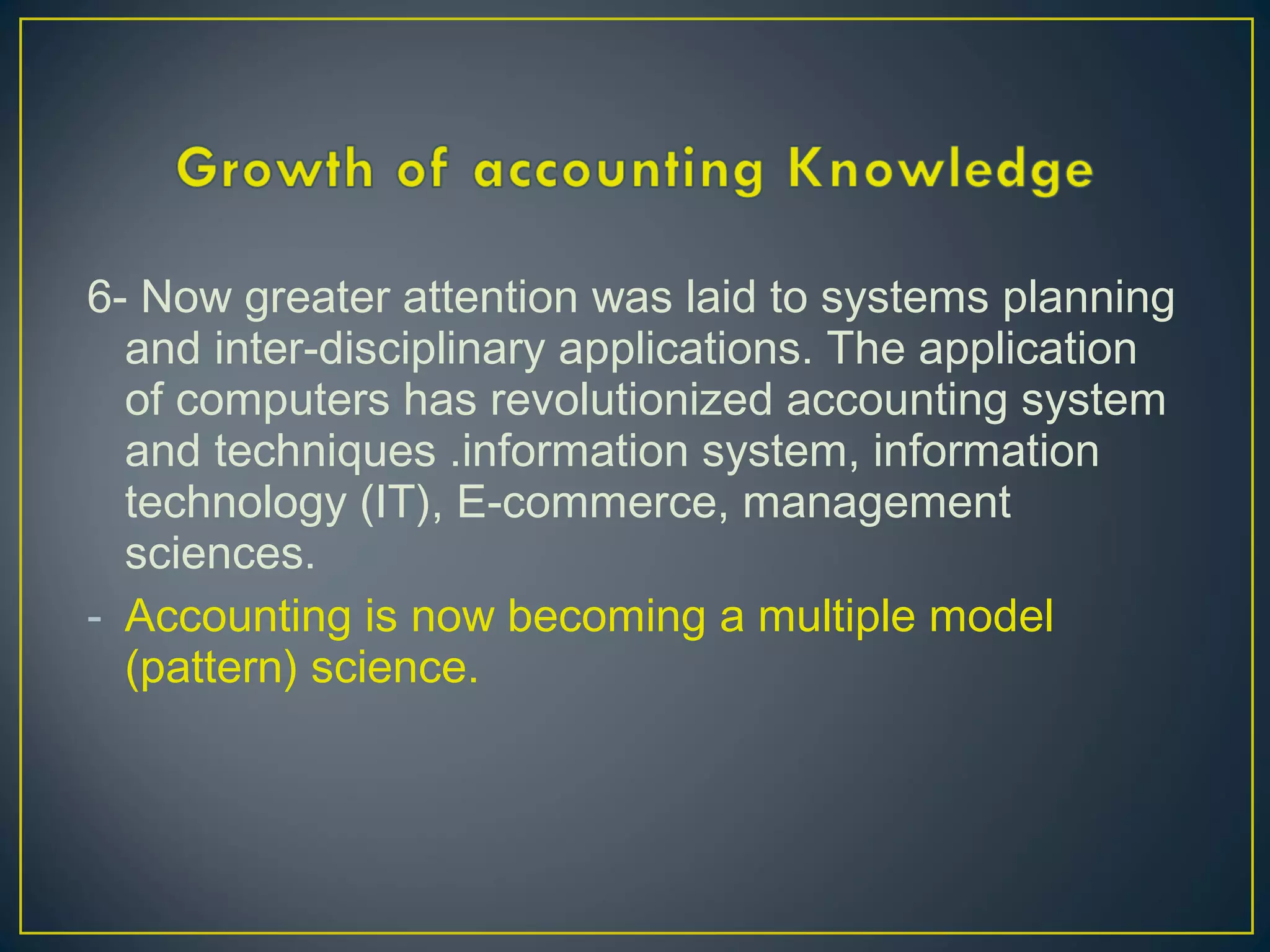

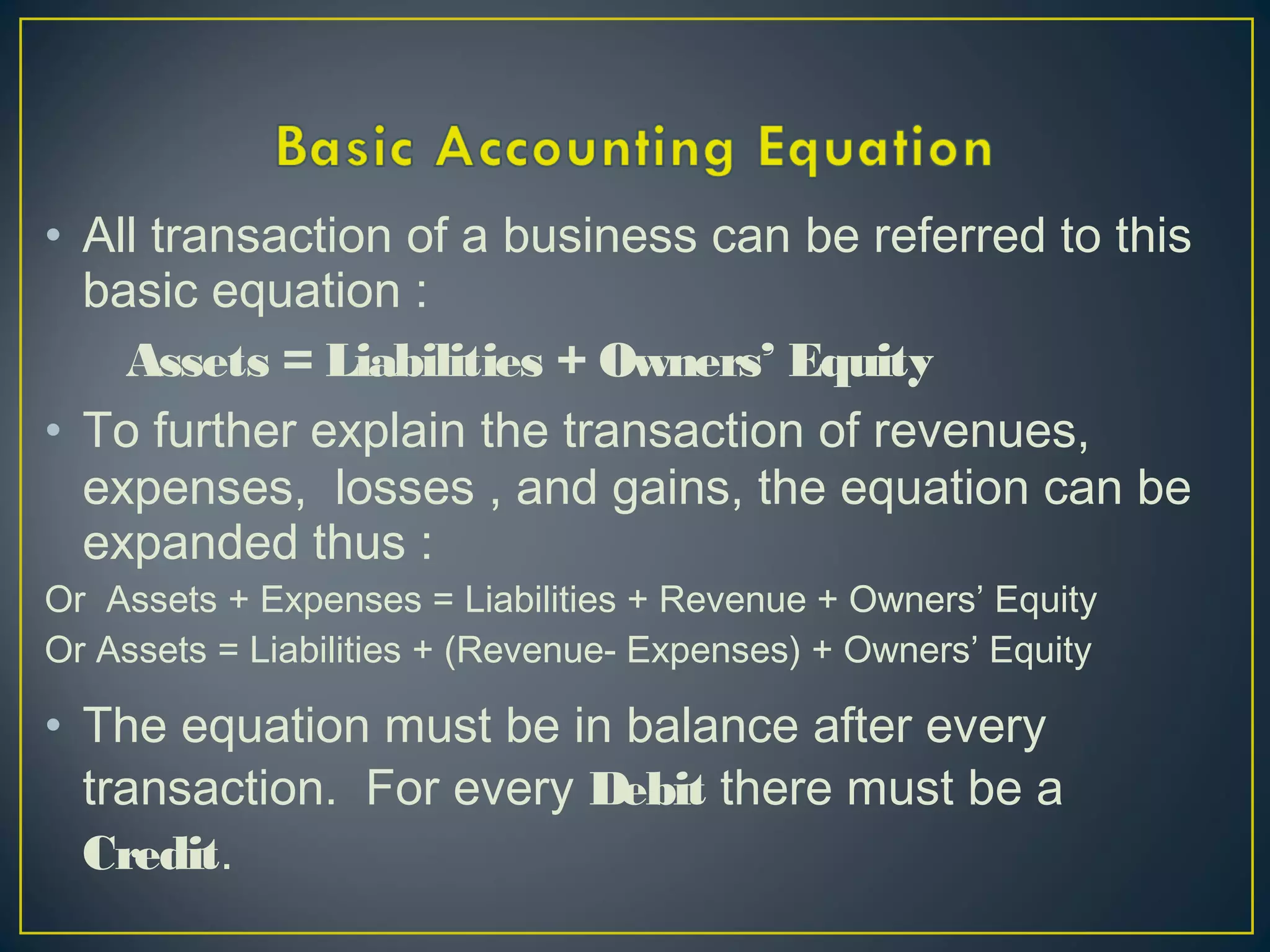

This document discusses the history and development of accounting knowledge over the past 200 years. It begins by describing early accounting practices in ancient civilizations. It then outlines key developments in different time periods, including the establishment of double-entry bookkeeping in Europe in the 15th century, stagnation from 1494-1775, an emphasis on the balance sheet from 1775-1850, and the development of accounting principles and assumptions from 1850-1900. The document also discusses the leadership of the United States and European countries in advancing accounting theory in the 20th century.