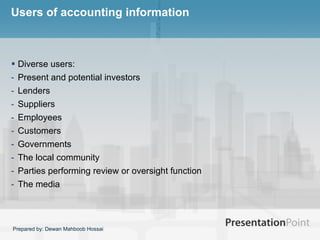

Chapter 2 of Craig Deegan's financial accounting theory discusses the diverse users of accounting information and their varying levels of understanding and knowledge. It highlights the importance of regulation in protecting the information rights of external users and the debate over whether accounting standards should be set privately or publicly. Furthermore, it emphasizes the role of professional judgment in accounting practices, acknowledging that while regulations exist, significant discretion remains in the treatment of financial transactions.