Downloaded 49 times

![Positivistic Perspectives in Accounting Research

Positivism still seems largely underpin the dominant mode of accounting research.

In this regard, economic is currently the undisputable source of theories & methods for the

mainstream accounting studies. Moreover, accounting journals view the scientific approach is

appropriate to the discovery, explanation and prediction of accounting phenomena.

This approach focuses on the existence of a priori fixed [hypothetical-deductive] relationships

within phenomena which are typically investigated through structured instrumentation (Landry

and Banville, 1992). Indeed, the aim of this approach should be to identify causal explanations and

fundamental laws that explain regularities in human social behavior.

Research using positivistic perspectives or theories see “reality” as a concrete structure and

“people” as adopters, respondents and information processors to achieve efficiency and goals of

the organisation (Morgan and Smircich, 1980).

Advocators of positivistic approach seek primarily to discover law-like regularities, believe that

accounting is objective, and that accounting hypotheses can be statistically tested with empirical

data sets to produce generalizable findings. Finally, there is a tendency in positive research to

discount contrary research findings as anomalous.

Accounting research from this perspectives, views accounting control systems, such as budgeting

as a means to achieving low cost, efficient operations.

By using this approach the researchers normally rely on an arm-length research method-

statistically categories, key variables and then attempts to retrieve meaning by ex post facto

interpretations of tests of significance (Tomkins and Groves, 1983).

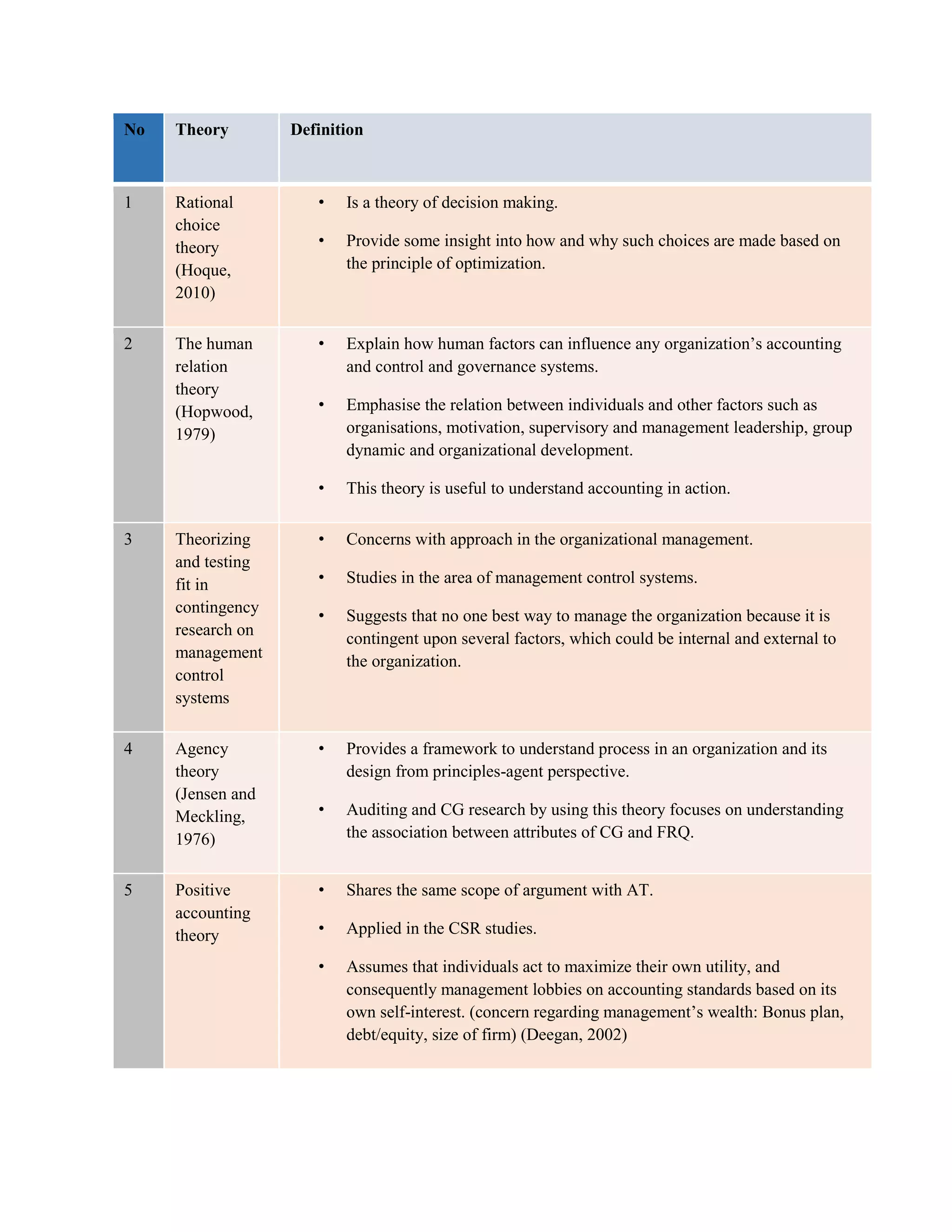

Common Theories in Positivistic Perspectives

Table 2 describes common theories utilized in positivism perspectives of social science researches.

Table 2 Common theories in positivistic perspective](https://image.slidesharecdn.com/differentapproachesinaccountingresearch-160113075805/75/Different-approaches-in-accounting-research-3-2048.jpg)

1) The document discusses different approaches to accounting research, including positivistic, naturalistic, and institutional/contextual perspectives. 2) Positivistic research views accounting objectively and aims to identify laws and relationships through statistical analysis. Common theories used include rational choice and agency theory. 3) Naturalistic research assumes multiple interpretations of reality and focuses on interpretation over explanation. Grounded theory is a common approach. 4) Institutional research examines accounting in its social/political context and considers organizational legitimacy important for survival. Legitimacy and institutional theories are discussed.