This document discusses key accounting concepts including journals, ledgers, and trial balances. It provides the following information:

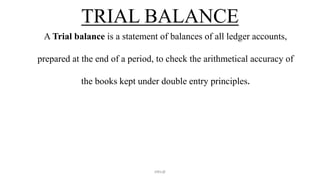

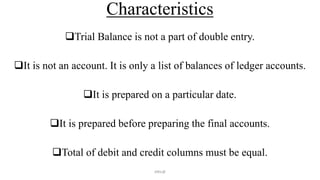

Journals are books used to record daily business transactions chronologically. Transactions are first recorded in journals before being posted to ledger accounts. Ledgers contain individual accounts for assets, liabilities, equity, income and expenses where journal entries are collected. A trial balance is a financial statement prepared at the end of an accounting period that lists the balances of all ledger accounts to check for errors in double-entry bookkeeping. It shows equal totals for total debits and total credits.