Download as PDF, PPTX

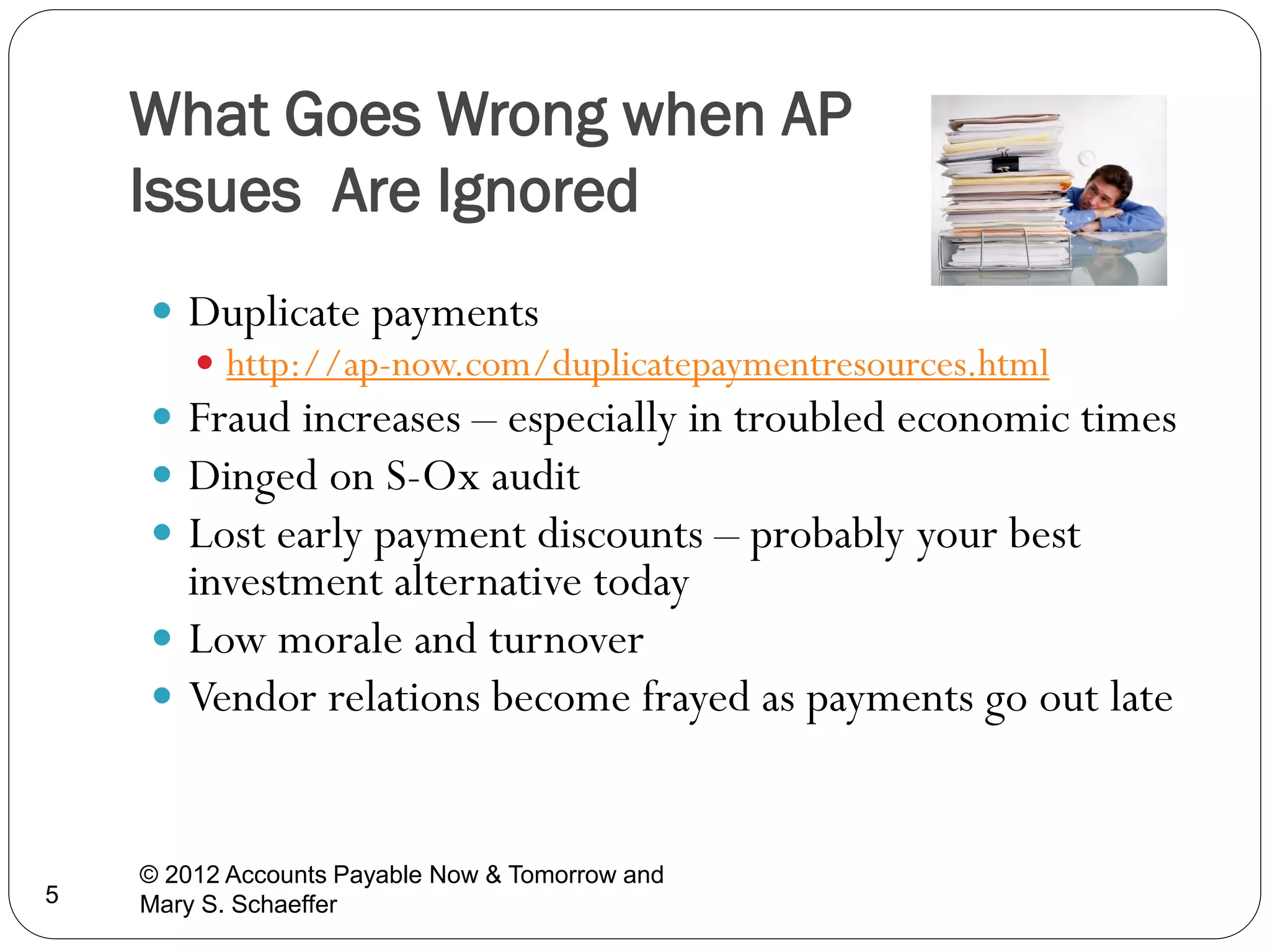

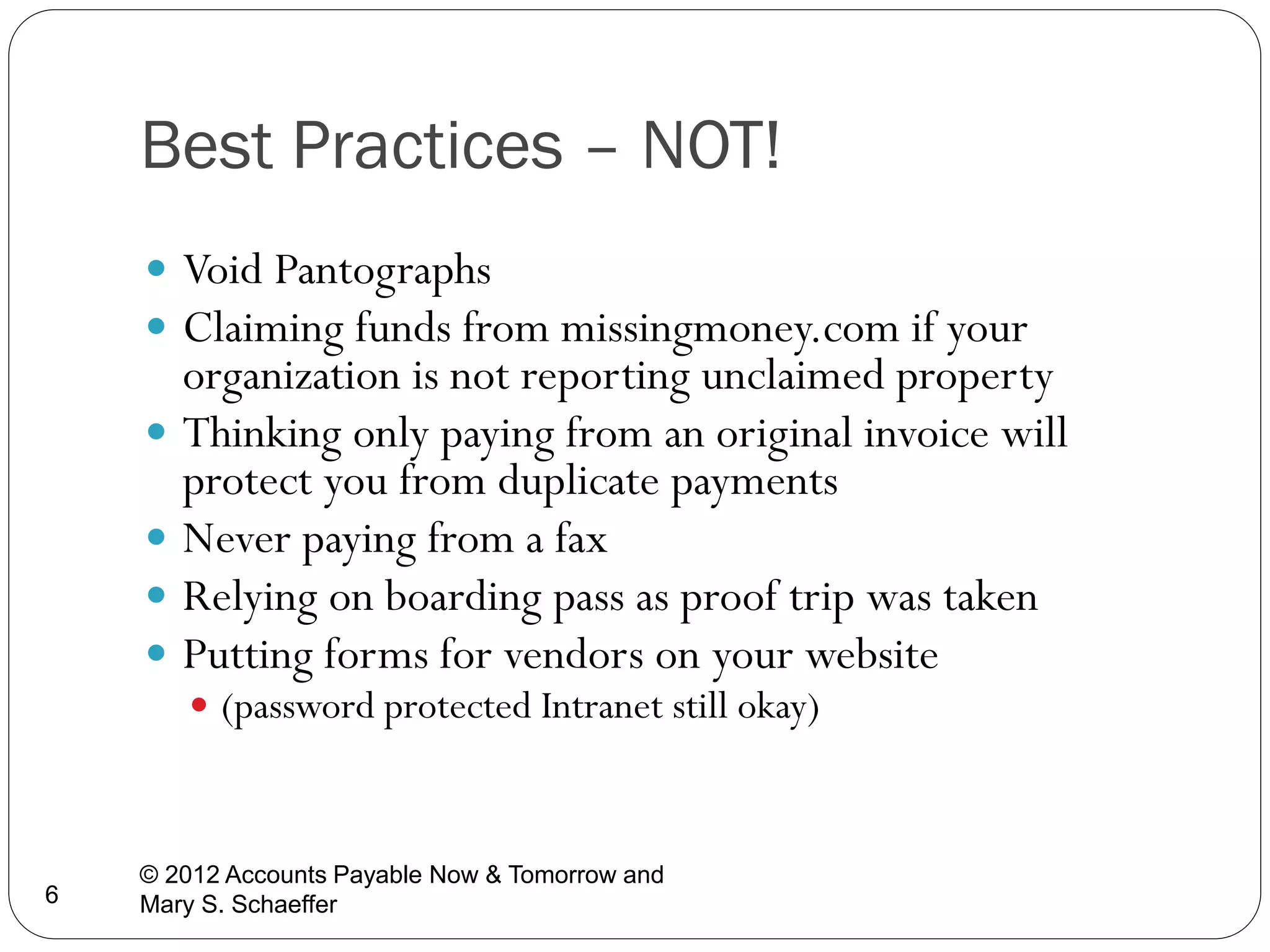

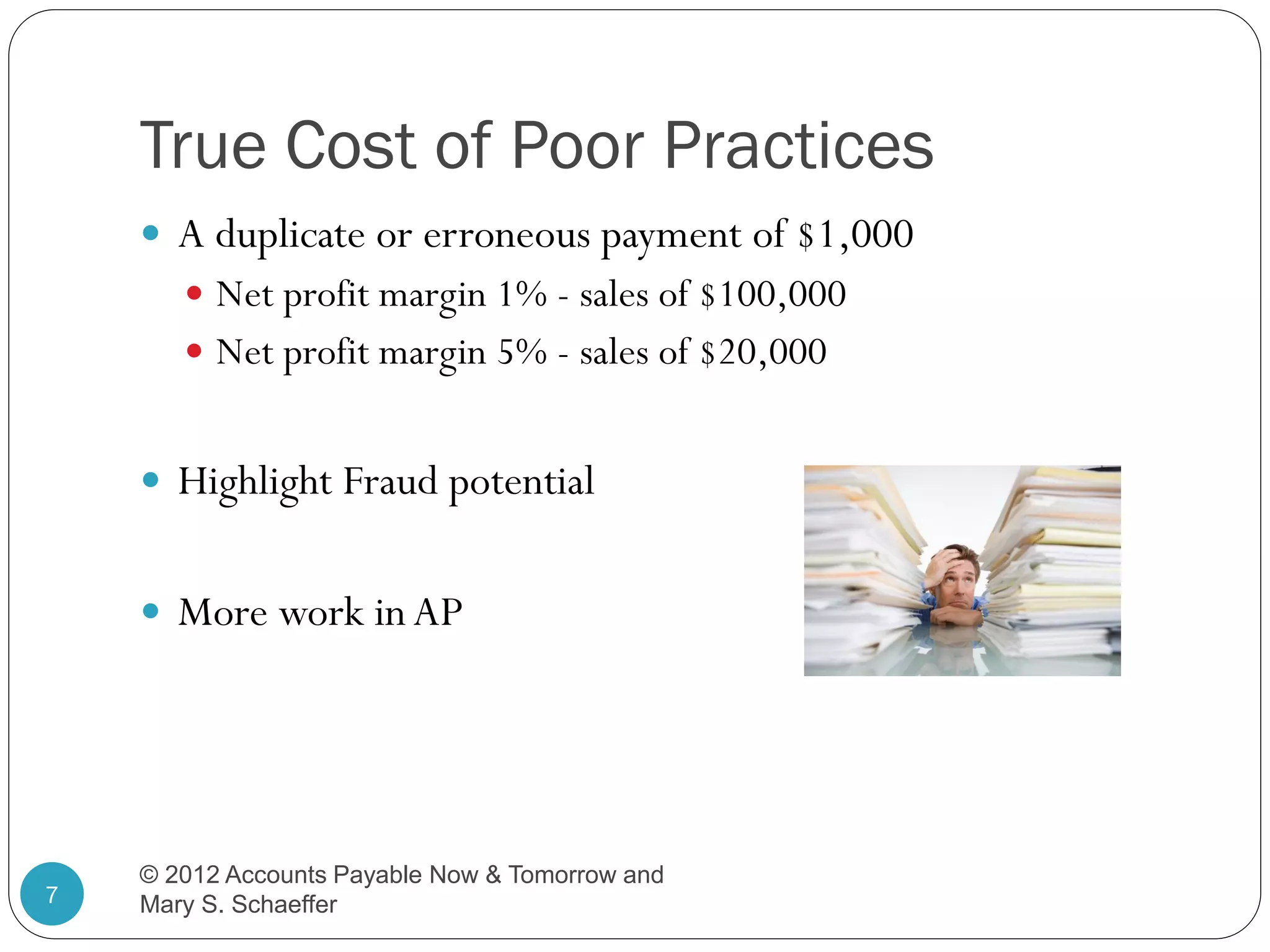

The document discusses implementing best practices for a more efficient accounts payable function. It outlines changing best practices due to technology advances and increased regulations. Implementing best practices across the entire procure-to-pay process from invoice handling to payments can help avoid issues like duplicate payments and fraud. Technology is playing a larger role in automating invoice processing. Future best practices will focus on continued automation, regulatory compliance, and fraud prevention.

![[Webinar] Implement Simple Best Practices with AP Now & Tomorrow](https://cdn.slidesharecdn.com/ss_thumbnails/anybillbestpracticeswithapnow-130208133900-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] AP Efficiency: It's All In The Controls](https://cdn.slidesharecdn.com/ss_thumbnails/anybillwebinarapefficiencyitsallinthecontrols-130208133954-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] Little Mistakes that Cause Big Problems in Accounts Payable](https://cdn.slidesharecdn.com/ss_thumbnails/11911webinarslideslittlemistakesthatcausebigprogblems-131120122620-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] Fraud in Accounts Payable](https://cdn.slidesharecdn.com/ss_thumbnails/fraudandothershenanigansinap-25wayscrooksstealyourorganizationsmoneyandhowyoucanstopthem-131120124610-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] Fraud and Other Shenanigans in Accounts Payable](https://cdn.slidesharecdn.com/ss_thumbnails/anybillfraud25presentation-130123154130-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] AP Improvements that Repay: Planning for the New Year](https://cdn.slidesharecdn.com/ss_thumbnails/anybillapimprovementsthatrepaynovember2013-131114130402-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] New Year, New AP](https://cdn.slidesharecdn.com/ss_thumbnails/ifoanybillwebinarnewyearnewapfinal-140113092111-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] Unveiling the Benefits of Accounts Payable with The Institute of Fi...](https://cdn.slidesharecdn.com/ss_thumbnails/instituteoffinancialoperations-anybillunveilingthebenefitsofap32212-131120131729-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] From Tactical to Strategic: A Shift in the Understanding of Account...](https://cdn.slidesharecdn.com/ss_thumbnails/fromtacticaltostrategic-ashiftintheunderstandingofaccountspayable-131120124048-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Article] The Accounts Payable Function: Are There Cracks in Your Foundation?](https://cdn.slidesharecdn.com/ss_thumbnails/anyapstrongfoundationarticle102413-131106094430-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] Stop Thinking About It and Automate Your AP Processes](https://cdn.slidesharecdn.com/ss_thumbnails/paystream-anybillstopthinkingaboutitandautomate2013101013final-131010145230-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] AP Function: Does Yours Have a Strong Foundation?](https://cdn.slidesharecdn.com/ss_thumbnails/anybillfoundationaugust-130813132613-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] Benefits of AP Automation: Why Companies of All Sizes Should Be Tak...](https://cdn.slidesharecdn.com/ss_thumbnails/tapnwebinarbenefitsofapautomation-130227084947-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Whitepaper] Prioritizing Payables](https://cdn.slidesharecdn.com/ss_thumbnails/prioritizingpayables000-130208140400-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Whitepaper] From Profit Recovery To Retention](https://cdn.slidesharecdn.com/ss_thumbnails/profitrecoverytoretention000-130208134624-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Whitepaper] Aberdeen Research Report: AP Invoice Management in a Networked E...](https://cdn.slidesharecdn.com/ss_thumbnails/invoicemgmtnetworked-finalreport-130208134623-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] Unveiling the Benefits of AP with the Institute of Financial Operat...](https://cdn.slidesharecdn.com/ss_thumbnails/instituteoffinancialoperations-anybillunveilingthebenefitsofap32212-130208134100-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Webinar] Invoice Processing in Accounts Payable: Start the Year Strong](https://cdn.slidesharecdn.com/ss_thumbnails/anybillinvoiceprocessinginaccountspayable-130128133129-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)