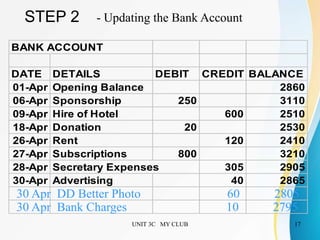

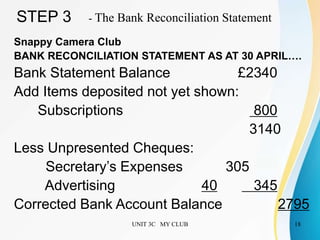

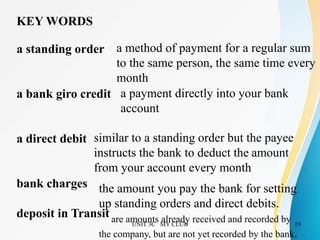

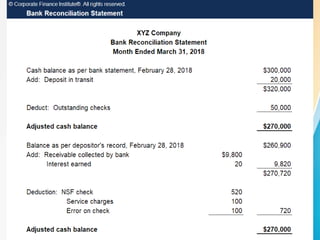

The document discusses bank reconciliation statements. It begins by outlining the content, performance, and learning competencies which include describing bank reconciliation statements, identifying common reconciling items, and analyzing their effects. It then provides motivation and introduces the key objectives of understanding the nature of bank reconciliation statements, identifying reconciling items, and analyzing their effects. The remainder of the document provides details on reconciling items, the reconciliation process involving comparing bank and accounting records, and examples of reconciling different balances.