The document summarizes two models:

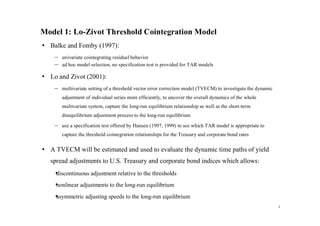

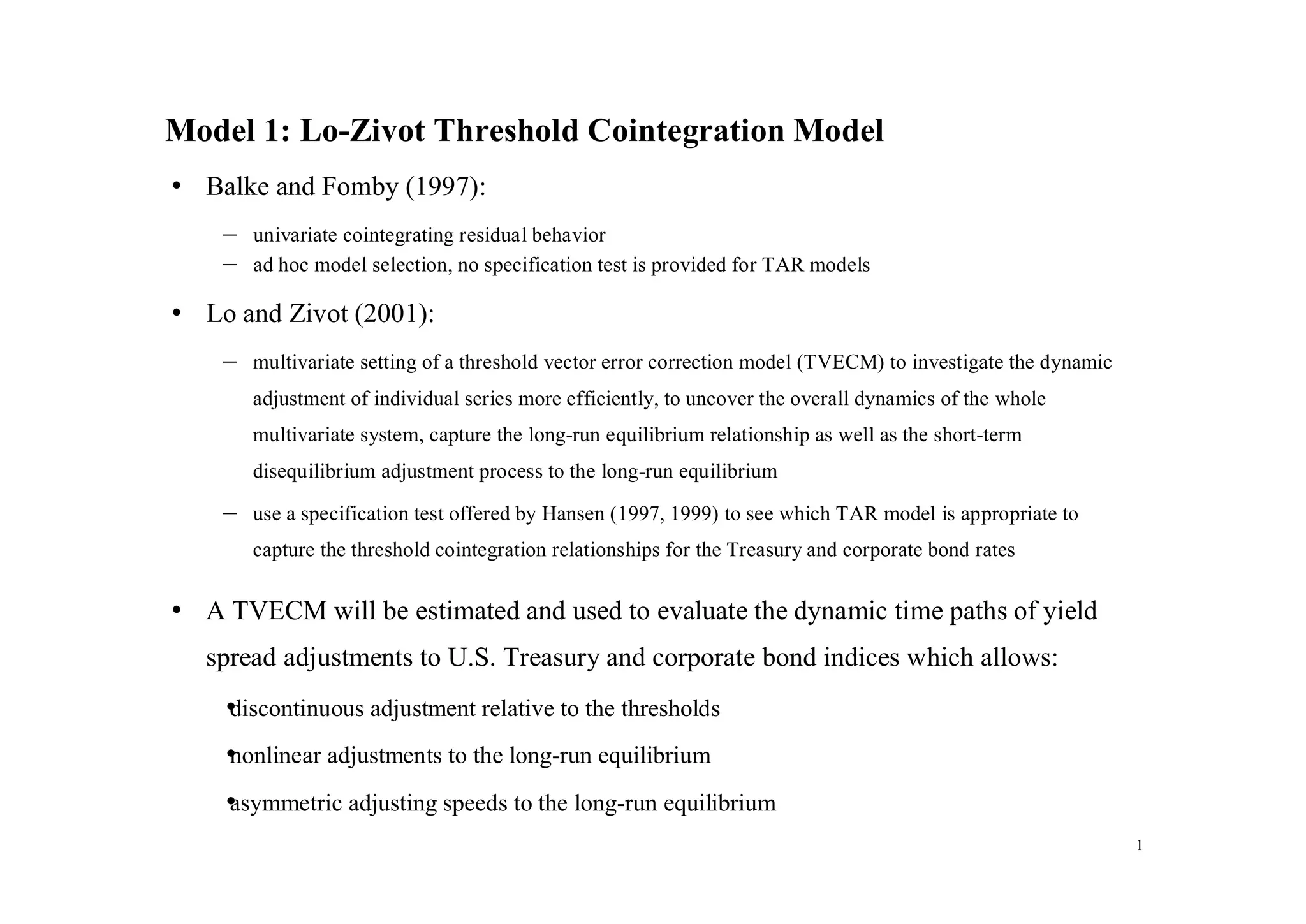

1. The Lo-Zivot Threshold Cointegration Model, which uses a threshold vector error correction model (TVECM) to analyze the dynamic adjustment of cointegrated time series variables to their long-run equilibrium. It allows for nonlinear and asymmetric adjustment speeds.

2. A bivariate vector error correction model (VECM) and band-threshold vector error correction model (BAND-TVECM) that extend the VECM to allow for nonlinear and discontinuous adjustments to long-run equilibrium across multiple regimes defined by thresholds on a variable. This captures asymmetric adjustment speeds and dynamic behavior.

The BAND-TVECM allows modeling of

![ γ 1( j) γ ( j) − β 2 γ 1( j)

where γ ( j)

β '= Π ( j)

( j) (1,− β 2 ) = 1( j)

= γ , and j = 1, 2, 3 (9)

γ 2

2 − β 2 γ 2( j)

• note that although the three regimes share a common cointegrating vector β ' = (1, − β 2 ) , the speeds of adjustment

γ ( j) ' = (γ 1( j) , γ 2( j) ) are regime specific. For example, we may observe that γ 1(1) ≠ γ 1( 3) or γ 2( 2 ) ≠ γ 2( 3)

• the simplest form for the TVECM occurs when k = 1 in equation (8) so that all lag difference terms drop out of the

equation, the cointegrating residual β ' X t follows a regime specific AR(1) process or threshold autoregressive (TAR)

process:

β ' X t = δ ( j) + ρ ( j) β ' X t −1 + η t( j) ,

with ρ ( j) = 1 + β ' γ ( j) = 1 + γ 1( j) − β 2 γ 2( j) , where δ ( j) = β ' A (0j) and η t( j) = β ' ε t( j)

Proof:

Set k = 1 in equation (8) to obtain:

∆X t = X t − X t −1 = [A (01) + γ (1)

β ' X t −1 ]I 1t (z t − d ≤ c (1) ) + [A (02 ) + γ ( 2) β ' X t −1 ]I 2 t (c (1) < z t − d ≤ c ( 2 ) )

+ [A (03) + γ ( 3 ) β ' X t −1 ]I 3 t (z t − d > c ( 2 ) ) + ε t .

Multiply both sides by β ' , then move β ' Xt-1 to the right-hand side, will obtain:

β ' X t = β ' X t −1 + [β ' A (01) + β ' γ (1) β ' X t −1 ]I 1t ( z t −d ≤ c (1) ) + [β ' A (02 ) + β ' γ ( 2 ) β ' X t −1 ]I 2 t (c (1) < z t −d ≤ c ( 2 ) )

+ [β ' A (03 ) + β ' γ (3 ) β ' X t −1 ]I 3 t ( z t −d > c ( 2 ) ) + β ' ε t .

5](https://image.slidesharecdn.com/2003amesmodels-13205413335934-phpapp02-111105201117-phpapp02/85/2003-Ames-Models-5-320.jpg)

![Split β ' X t −1 and ε t to each regime, then obtain:

β ' X t = [β ' A (01) + β ' X t −1 + β ' γ (1) β ' X t −1 + β ' ε t(1) ]I1t (z t − d ≤ c(1) )

+ [β ' A (02 ) + β ' X t −1 + β ' γ ( 2 ) β ' X t −1 + β ' ε t( 2 ) ]I 2 t (c(1) < z t − d ≤ c ( 2 ) )

+ [β ' A (03 ) + β ' X t −1 + β ' γ ( 3) β ' X t −1 + β ' ε t(3 ) ]I3 t ( z t − d > c ( 2 ) ).

Collect terms to get:

β ' X t = [β ' A (01) + (1 + β ' γ (1) ) β ' X t −1 + β ' ε t(1) ]I1t ( z t − d ≤ c (1) )

+ [β ' A (02 ) + (1 + β ' γ ( 2 ) ) β ' X t −1 + β ' ε t( 2 ) ]I 2 t (c (1) < z t − d ≤ c( 2 ) )

+ [β ' A (03 ) + (1 + β ' γ ( 3) ) β ' X t −1 + β ' ε t( 3) ]I3 t (z t − d > c( 2 ) )

= δ ( j) + ρ ( j ) β ' X t −1 + η t( j ) .

Q.E.D.

• β ' X t is stable within each regime if the stability condition ρ ( j) = 1 + γ 1( j) − β 2 γ 2( j) < 1 holds for each regime

• in equation (8), with k = 1, then we have:

∆X t = [A (01) + γ (1) β ' X t −1 ]I 1t (z t − d ≤ c (1) ) + [A (02 ) + γ ( 2)

β ' X t −1 ]I 2 t (c (1) < z t − d ≤ c ( 2) )

(10)

+ [A (03 ) + γ ( 3 ) β ' X t −1 ]I 3 t (z t − d > c ( 2 ) ) + ε t .

• it is easier to capture the long-run equilibrium relationship if we rewrite (10) in:

∆X t = γ (1) [β ' X t −1 − µ (1) ]I 1t ( z t − d ≤ c (1) ) + γ ( 2 ) [β ' X t −1 − µ ( 2) ]I 2 t (c (1) < z t − d ≤ c ( 2 ) )

(11)

+ γ ( 3) [β ' X t −1 − µ ( 3) ]I 3t (z t − d > c ( 2) ) + ε t .

explicitly we have:

6](https://image.slidesharecdn.com/2003amesmodels-13205413335934-phpapp02-111105201117-phpapp02/85/2003-Ames-Models-6-320.jpg)

![γ 1(1) [x 1t −1 − β 2 x 2 t −1 − µ (1) ] + ε 1(t1) , if z t − d ≤ c (1) ,

∆x 1t = γ 1( 2 ) [x 1t −1 − β 2 x 2 t −1 − µ ( 2 ) ] + ε 1(t2 ) , if c (1) < z t − d ≤ c ( 2 ) , and

γ ( 3 ) [x − β x − µ ( 3) ] + ε 1(t3 ) , if z t − d > c ( 2 ) ,

1 1t −1 2 2 t −1

γ 2(1) [x 1t −1 − β 2 x 2 t −1 − µ (1) ] + ε 2(1t ) , if z t − d ≤ c (1) ,

∆x 2 t = γ 2( 2 ) [x 1t −1 − β 2 x 2 t −1 − µ ( 2 ) ] + ε 2( 2 ) ,

t

if c (1) < z t − d ≤ c ( 2 ) ,

γ ( 3 ) [x − β x − µ ]+ ε 2 t ,

( 3) (3)

if z t − d > c ( 2 ) .

2 1t −1 2 2 t −1

• the magnitudes and signs of the γ’ will provide fruitful information regarding the equilibrium relationships

s

• equation (11) offers the regime-specific means µ ( j) , which is calculated as:

β ' A (0j) A (0j,1 − β 2 A (0j,)2

)

δ ( j)

µ ( j)

=− = − ( j) = , (12)

β ' γ ( j) γ 1 − β 2 γ 2( j) 1 − ρ ( j)

where A (0j) ' = (A (0j,1 , A (0j,)2 ) , and β ' = (1, − β 2 )

)

• it is also possible to eliminate the regime specific drift in Xt through the restriction:

A (0j) = −γ ( j) µ ( j) (13)

where µ ( j) is calculated by (12)

• note that we may rewrite equation (11) as follows with z t −1 = β ' X t −1 = x 1t −1 − β 2 x 2 t −1 :

7](https://image.slidesharecdn.com/2003amesmodels-13205413335934-phpapp02-111105201117-phpapp02/85/2003-Ames-Models-7-320.jpg)

![γ (1)

[z t −1

− µ (1 ) ] + ε t , if z t −d ≤ c (1) ,

∆X t = γ (2)

[z t −1 − µ (2) ] + ε t , if c (1) < z t − d ≤ c ( 2 ) , (14)

γ

( 3)

[z t −1

− µ ( 3) ] + ε t , if z t − d > c ( 2 ) .

• consider the case of d = 1, γ ( 2 ) = 0 and A (02 ) = 0 in equation (14), this is the Band-TVECM structure which is the most

popular form in threshold cointegrating applications:

γ (1) [z t −1 − µ (1) ] + ε t , if z t −1 ≤ c (1) ,

∆X t = ε t , if c (1) < z t −1 ≤ c ( 2 ) , (15)

γ ( 3 ) [z − µ ( 3 ) ] + ε , if z t −1 > c ( 2 ) .

t −1 t

• the stability conditions must hold for the outer regimes, i.e., ρ ( j) = 1 + γ 1( j) − β 2 γ 2( j) < 1, for j = 1 and 3

• one may interpret above model as:

1. if the cointegrating residual (the error-correction term) z t −1 = β ' X t −1 lies within the inner band [c (1) , c ( 2 ) ] , then Xt

behaves like a random walk process without the drift, i.e., ∆X t has no tendency reverting to any long-term

equilibrium

2. if z t −1 is less than c (1) , then z t reverts to the regime specific mean µ (1) with adjustment coefficient ρ (1) while ∆X t

adjusts with speed of adjustment vector γ (1)

8](https://image.slidesharecdn.com/2003amesmodels-13205413335934-phpapp02-111105201117-phpapp02/85/2003-Ames-Models-8-320.jpg)

![3. if z t −1 is greater than c ( 2 ) , then z t reverts to the regime specific mean µ ( 3) with adjustment coefficient ρ ( 3) and

∆X t adjusts with speed of adjustment vector γ ( 3 )

4. expect γ i( 3) ≤ 0, γ i(1) > 0, for i = 1, 2, because of the force of the error correcting toward the long-term equilibrium

• if the regime specific means of the cointegrating residual z t are equal to the nearby threshold values (it is called the

“continuous”model): µ (1) = c (1) , µ ( 3) = c ( 2 ) , then (15) may be written as:

γ (1) [z t −1 − c (1) ] + ε t , if z t −1 ≤ c (1) ,

∆X t = ε t , if c (1) < z t −1 ≤ c ( 2 ) , (16)

γ ( 3) [z − c ( 2 ) ] + ε , if z t −1 > c ( 2 ) .

t −1 t

• the “symmetric”threshold model arises when the threshold values are symmetric against the origin ( c ( 2 ) = −c(1) = c ):

γ (1) [z t −1 + c] + ε t , if z t −1 ≤ −c,

∆X t = ε t , if − c < z t −1 ≤ c, (17)

γ ( 3) [z − c] + ε , if z t −1 > c .

t −1 t

• if µ (1) = µ (3 ) = 0, then we have the EQ-TVECM:

γ (1) z t −1 + ε t , if z t −1 ≤ c (1) ,

∆X t = ε t , if c (1) < z t −1 ≤ c ( 2 ) , (18)

γ ( 3 ) z + ε , if z t −1 > c ( 2 ) .

t −1 t

9](https://image.slidesharecdn.com/2003amesmodels-13205413335934-phpapp02-111105201117-phpapp02/85/2003-Ames-Models-9-320.jpg)

![Two-Regime Threshold Cointegration Model

• xt is a p × 1 I(1) with one p × 1 cointegrating vector β, w t ( β ) = β ' x t denotes the I(0) error-correction term

• A linear vector error correction model (VECM) of order (L+1):

∆x t = A ' X t −1 ( β ) + u t , (1)

where X 't −1 ( β ) = [ 1, w t −1 ( β ), ∆x t −1 , ∆x t − 2 , ..., ∆x t − L ], with dimensions: Xt-1(β) is k × 1, k = p × L + 2, A is k ×

p

• The error term ut is a p × 1 Martingale difference sequence with finite variance-covariance matrix Σ = E(u t u 't ) of

dimension p × p

• The approach is to estimate the parameters (β, A, Σ) by maximum likelihood estimation given the assumption

that the error terms u t’ are i.i.d. Gaussian distributed

s

• Let γ be the threshold parameter, a two-regime threshold cointegration model:

A 1' X t −1 ( β ) + u t , if w t −1 ( β ) ≤ γ ,

∆x t = ' ,

A 2 X t −1 ( β ) + u t , if w t −1 ( β ) > γ ,

15](https://image.slidesharecdn.com/2003amesmodels-13205413335934-phpapp02-111105201117-phpapp02/85/2003-Ames-Models-15-320.jpg)

![Extensions to modify the basic threshold cointegration model:

(1) allow a non-zero drift term as the linear attractor, which can be expressed as:

∆µ t = I t ρ 1 ( µ t −1 − a 0 ) + (1 − I t ) ρ 2 ( µ t −1 − a 0 ) + ε t , (7)

where It is the Heaviside indicator function such that:

1, if µ t −1 ≥ a 0

It = (8)

0, if µ t −1 < a 0 .

(2) allow a drift and linear trend as attractor with the expression:

∆µ t = I t ρ 1 [ µ t −1 − a 0 − a 1 ( t − 1)] + (1 − I t ) ρ 2 [ µ t −1 − a 0 − a 1 ( t − 1)] + ε t , (9)

where It is the Heaviside indicator function such that:

1, if µ t −1 ≥ a 0 + a 1 ( t − 1)

It = (10)

0, if µ t −1 < a 0 + a 1 ( t − 1).

(3) involve higher-order terms of the error process to purge possible auto-correlation:

23](https://image.slidesharecdn.com/2003amesmodels-13205413335934-phpapp02-111105201117-phpapp02/85/2003-Ames-Models-23-320.jpg)

![[Vvedensky d.] group_theory,_problems_and_solution(book_fi.org)](https://cdn.slidesharecdn.com/ss_thumbnails/vvedenskyd-grouptheoryproblemsandsolutionbookfi-org-130405071812-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)