Download to read offline

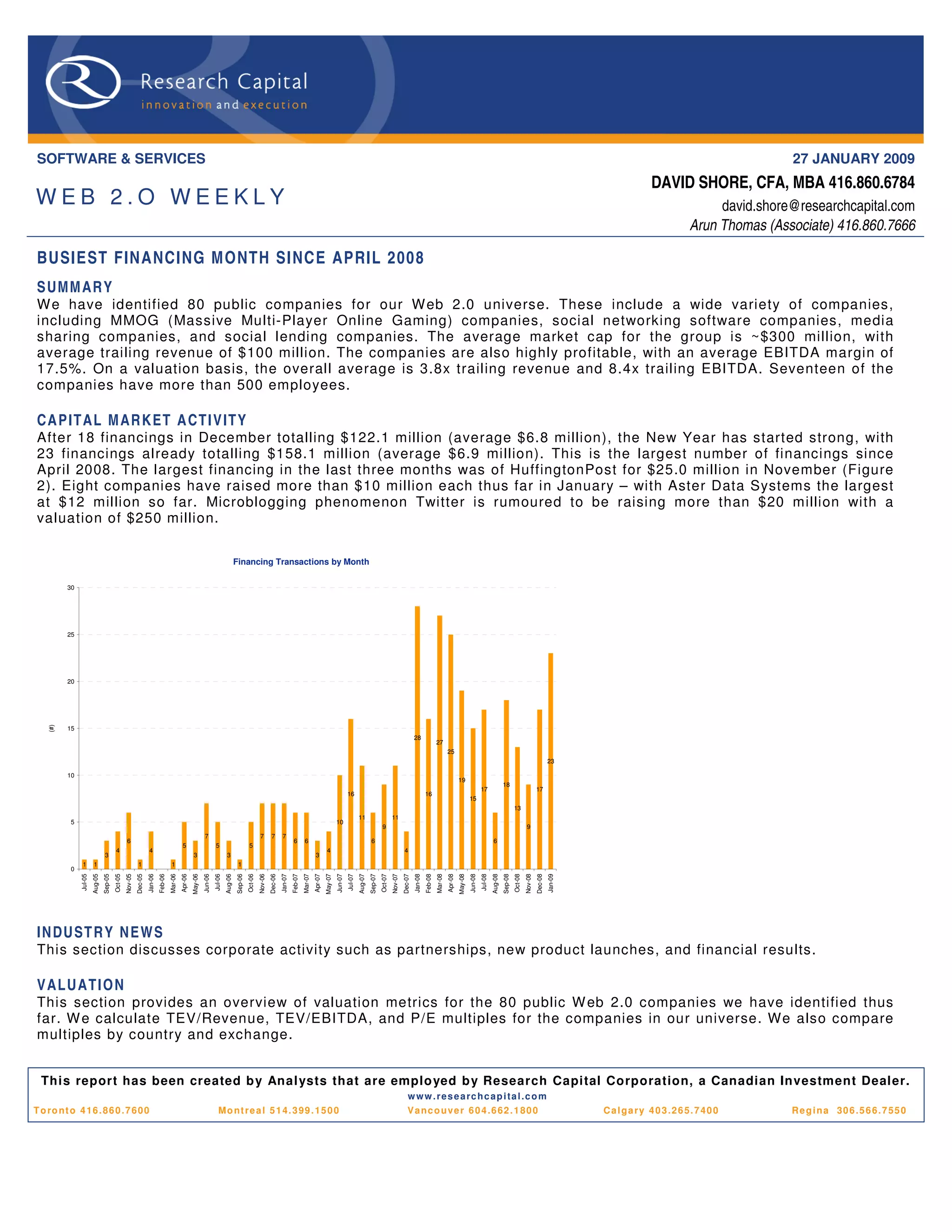

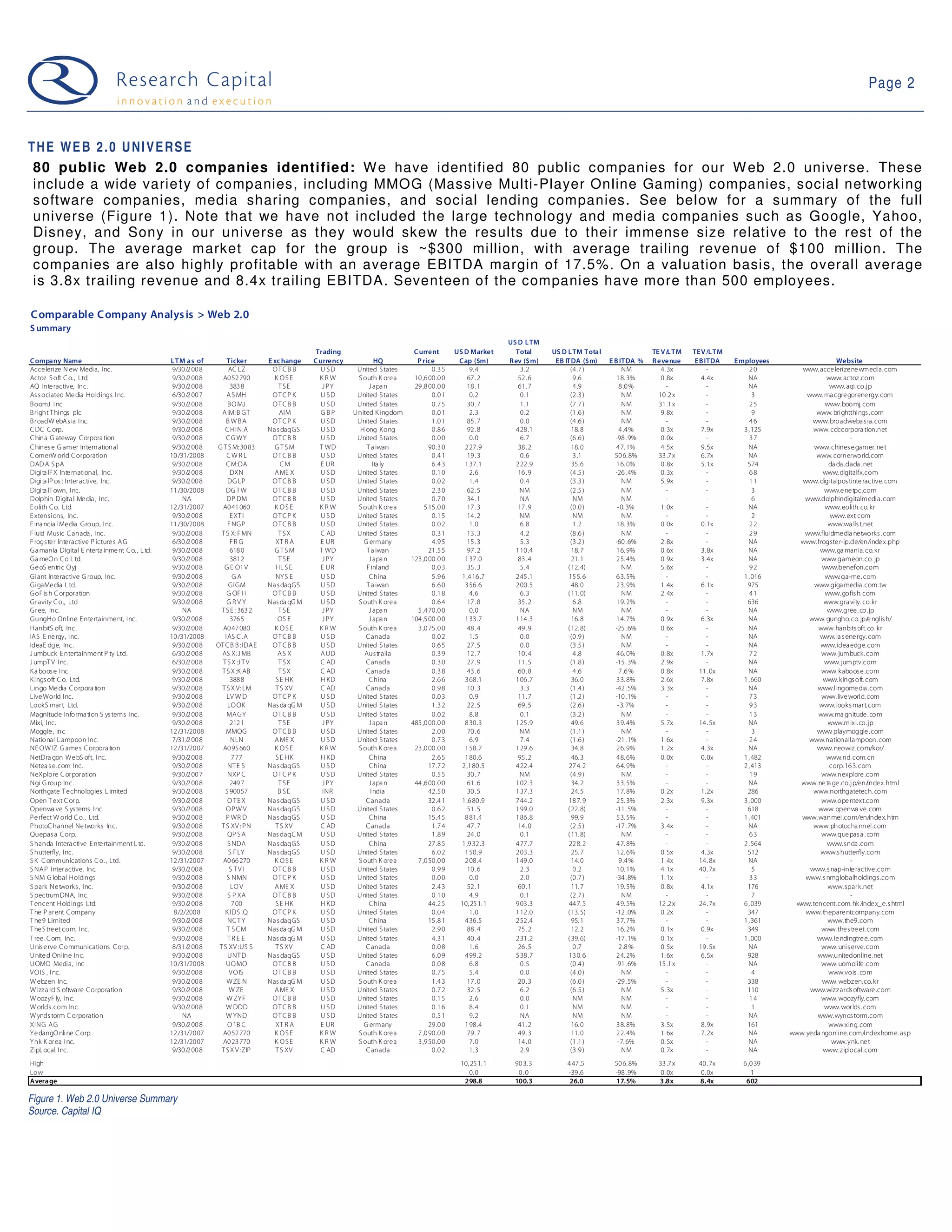

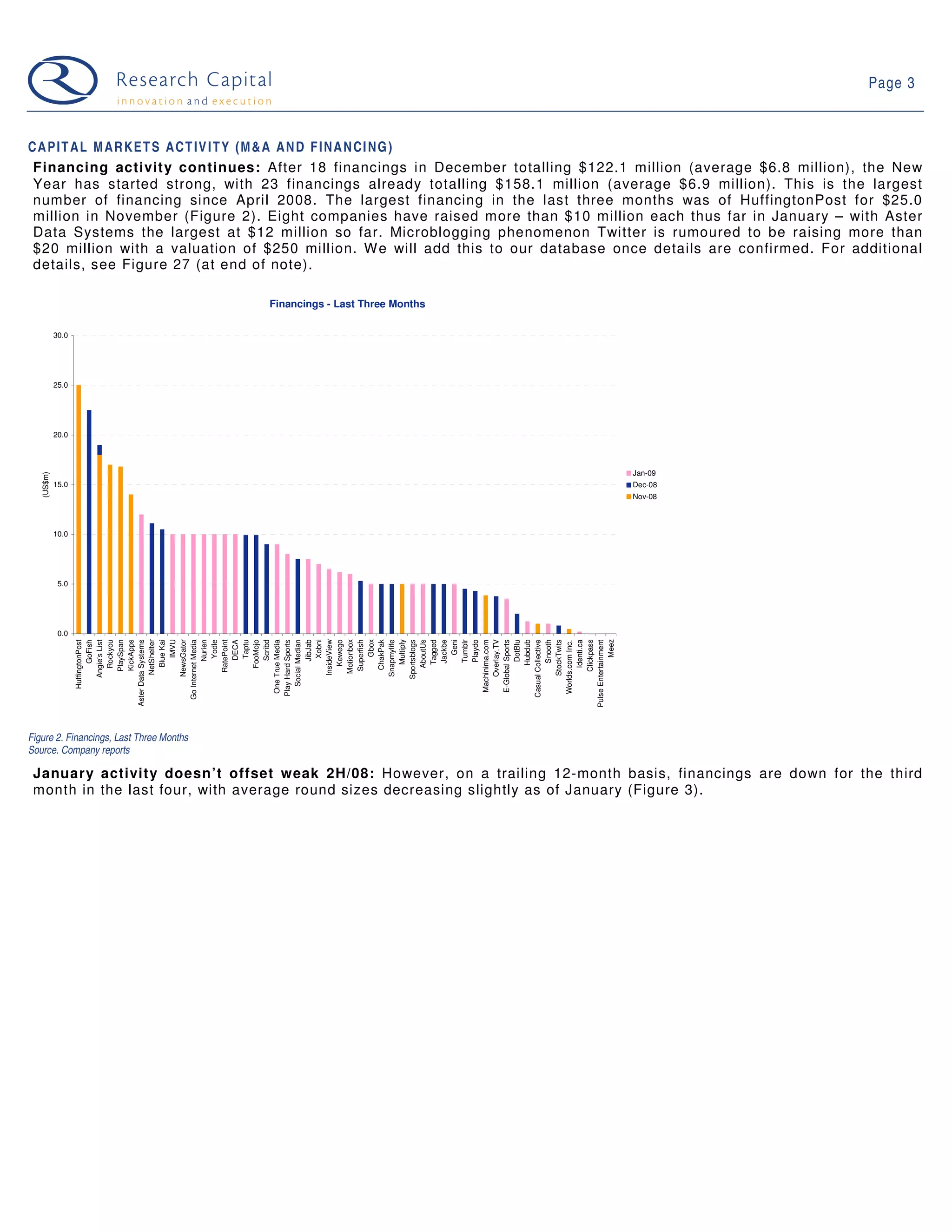

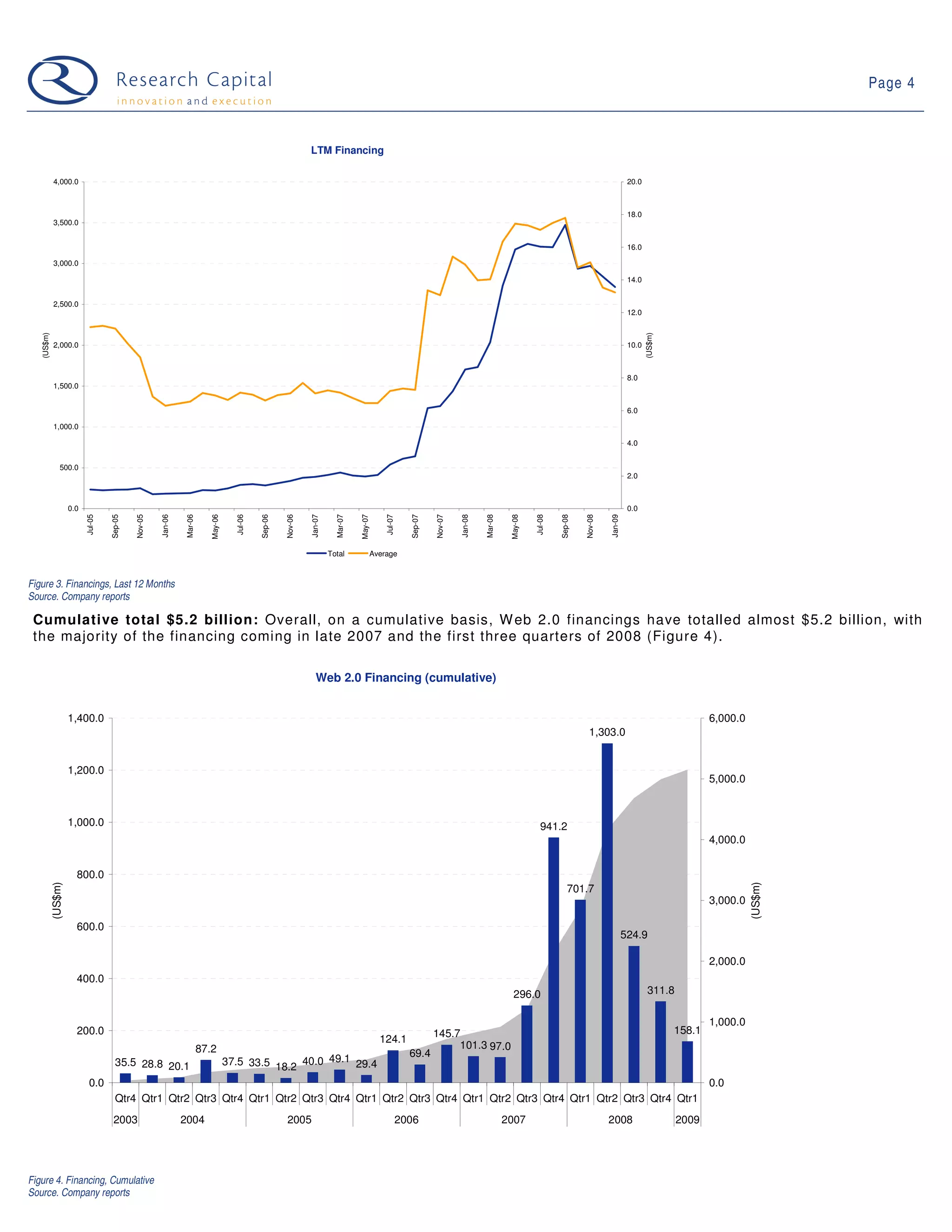

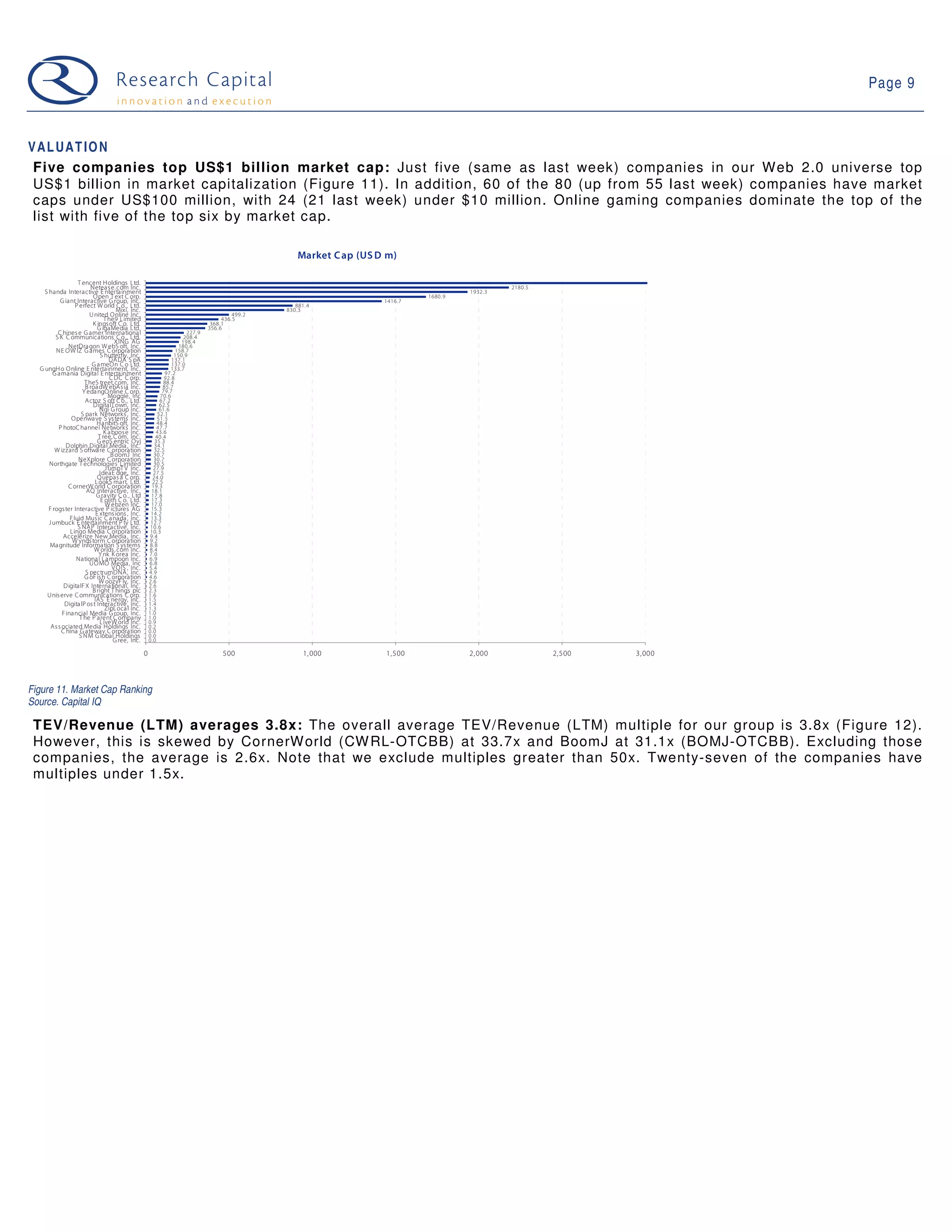

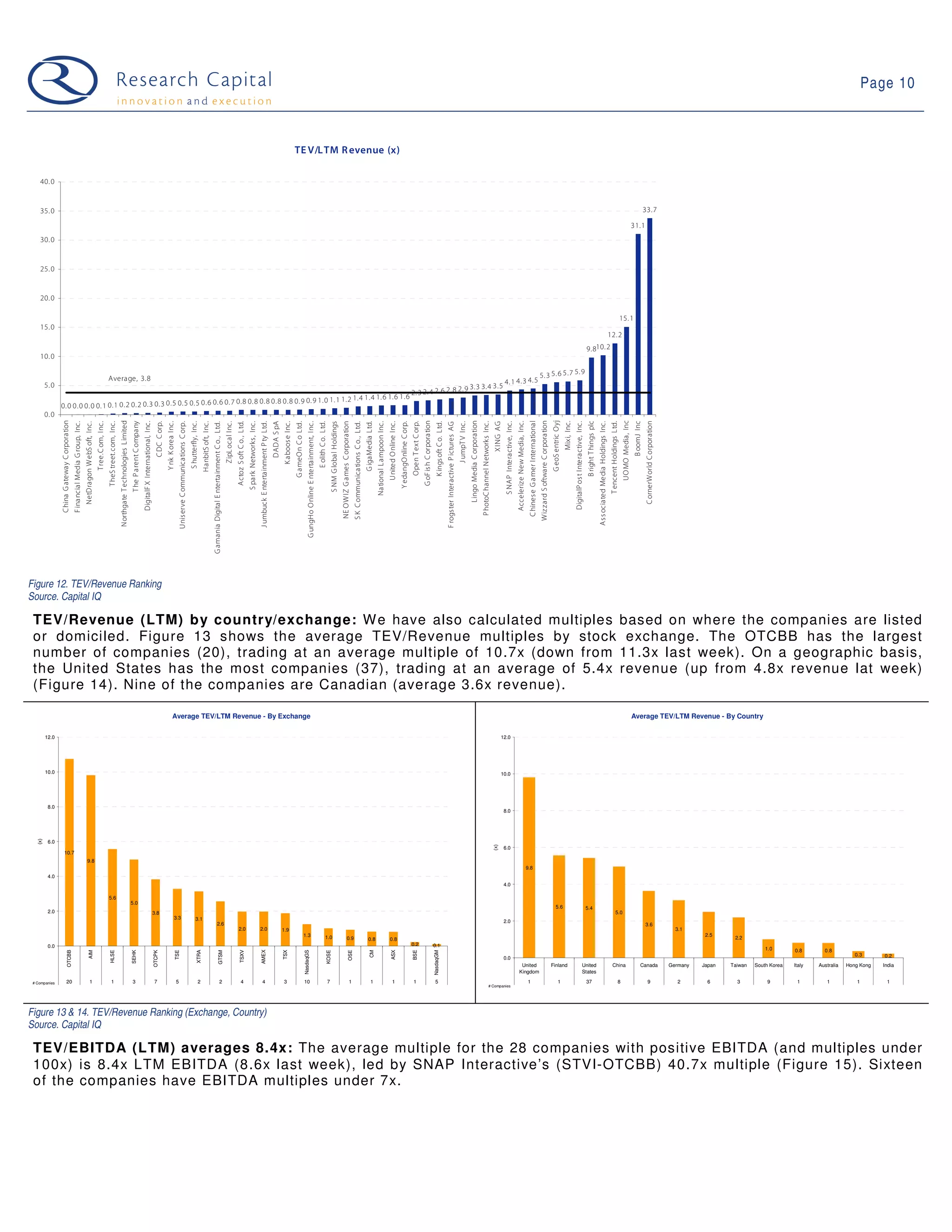

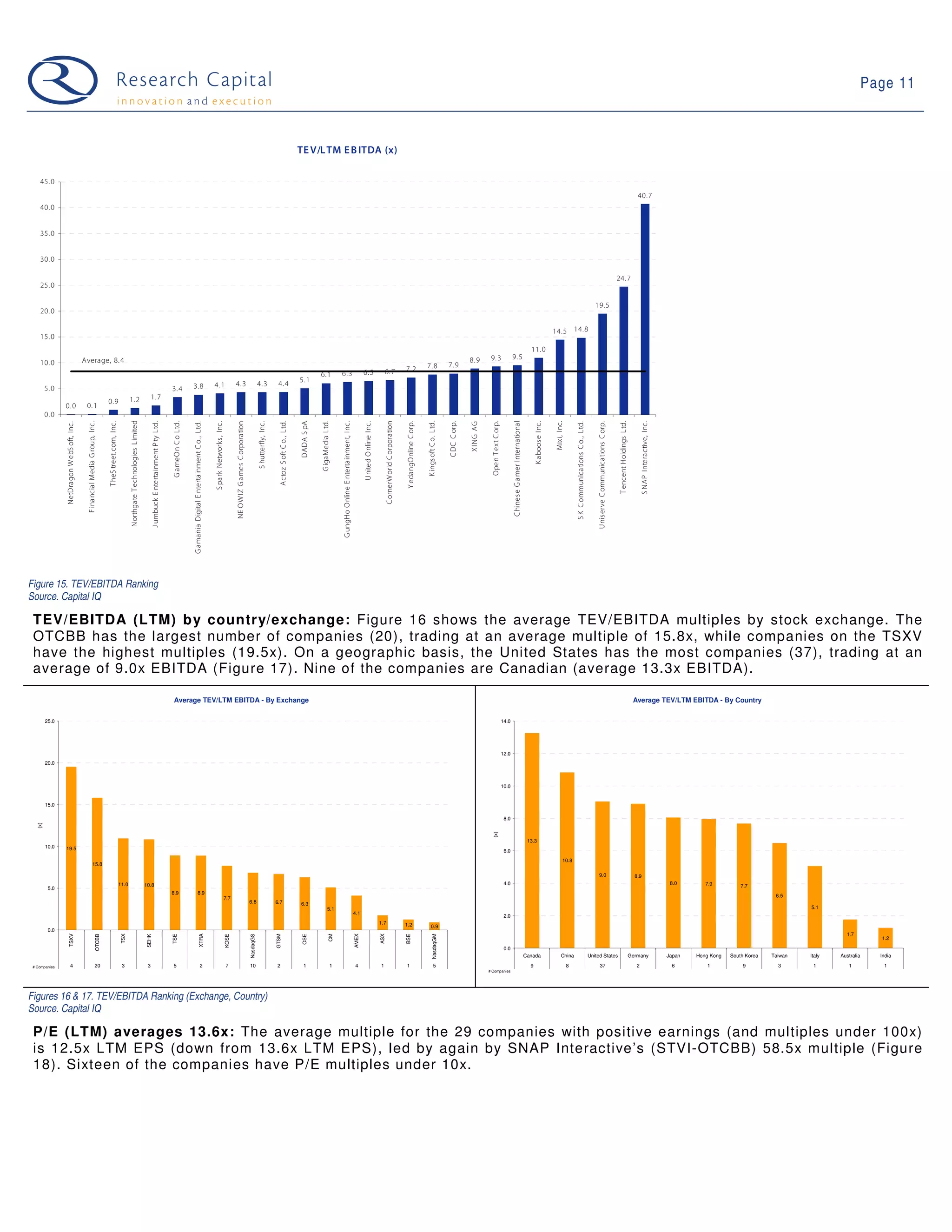

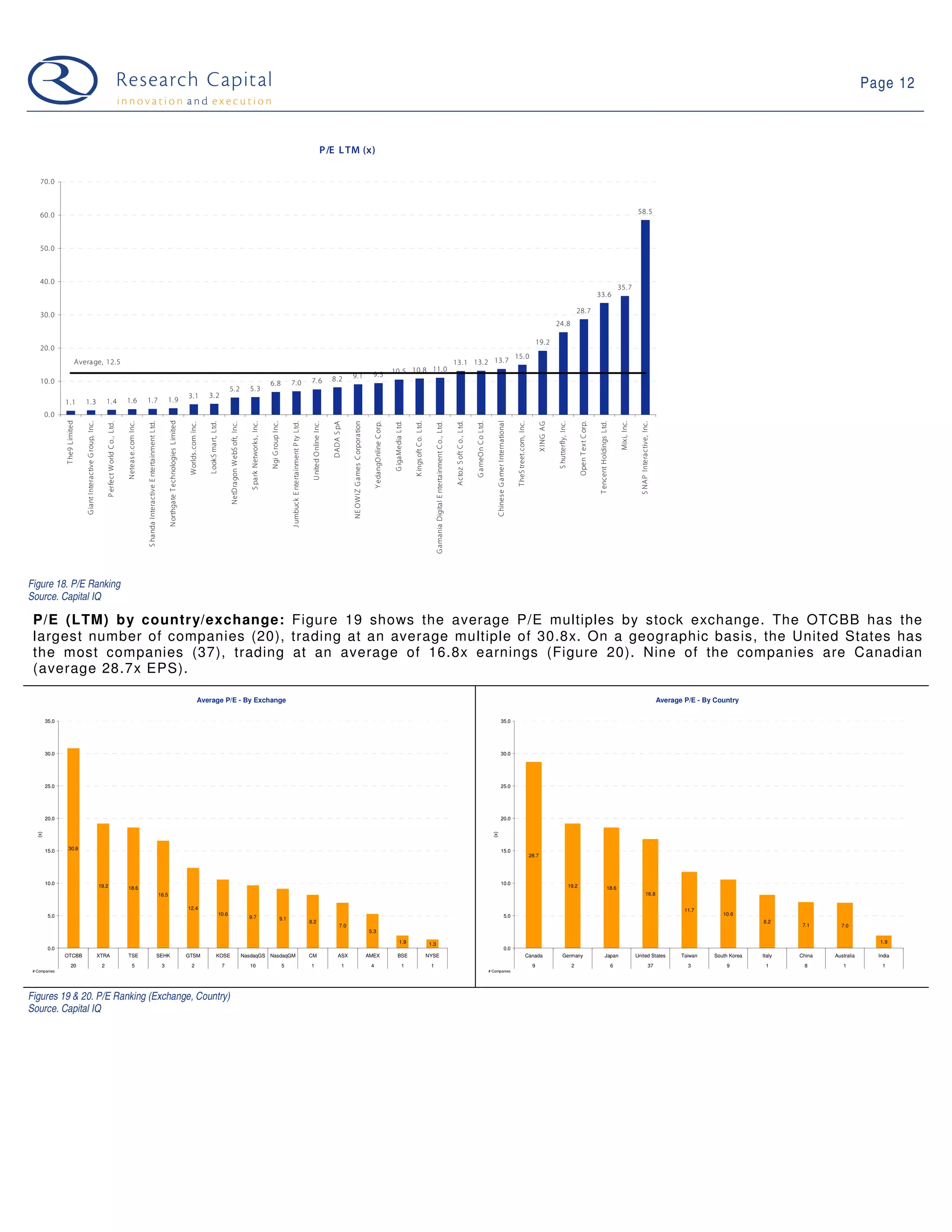

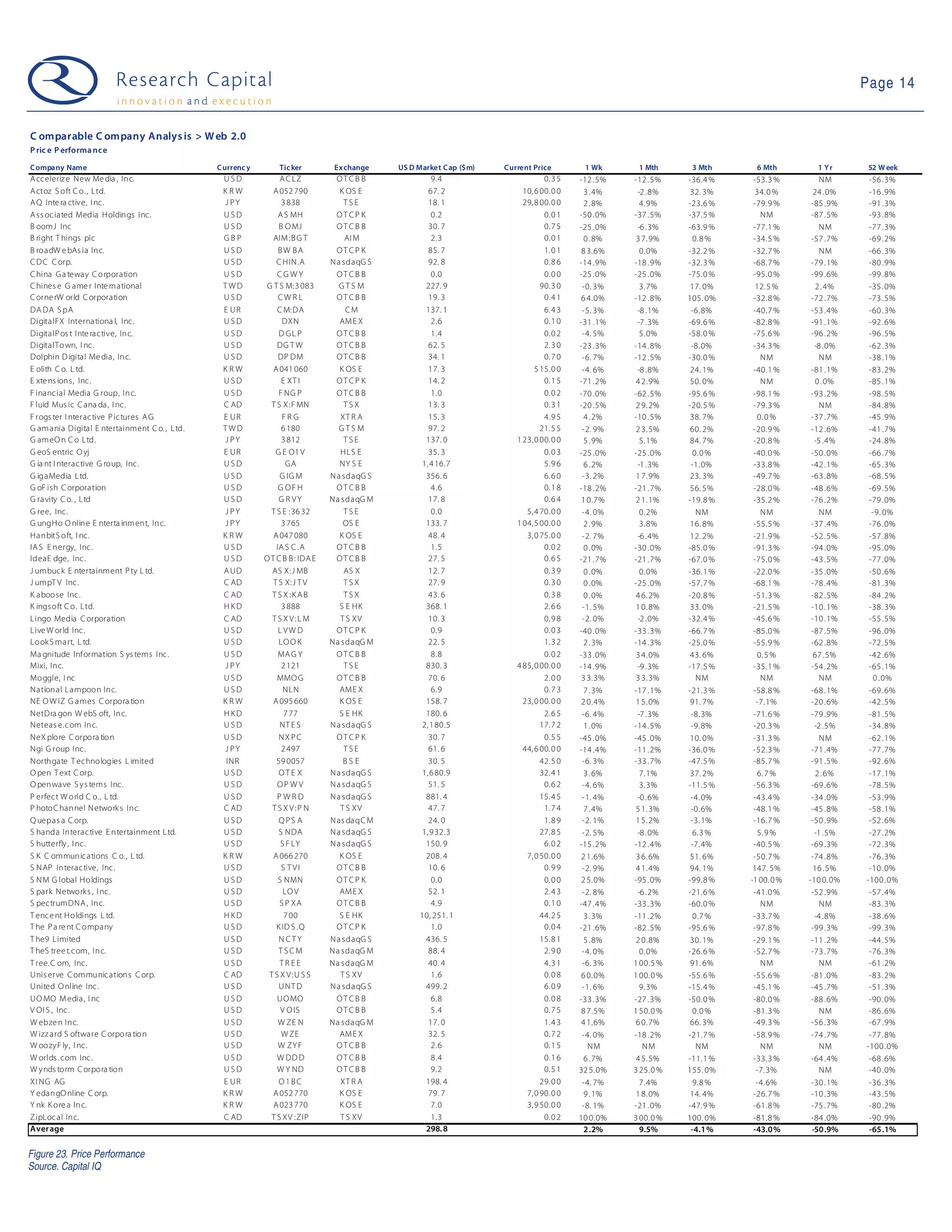

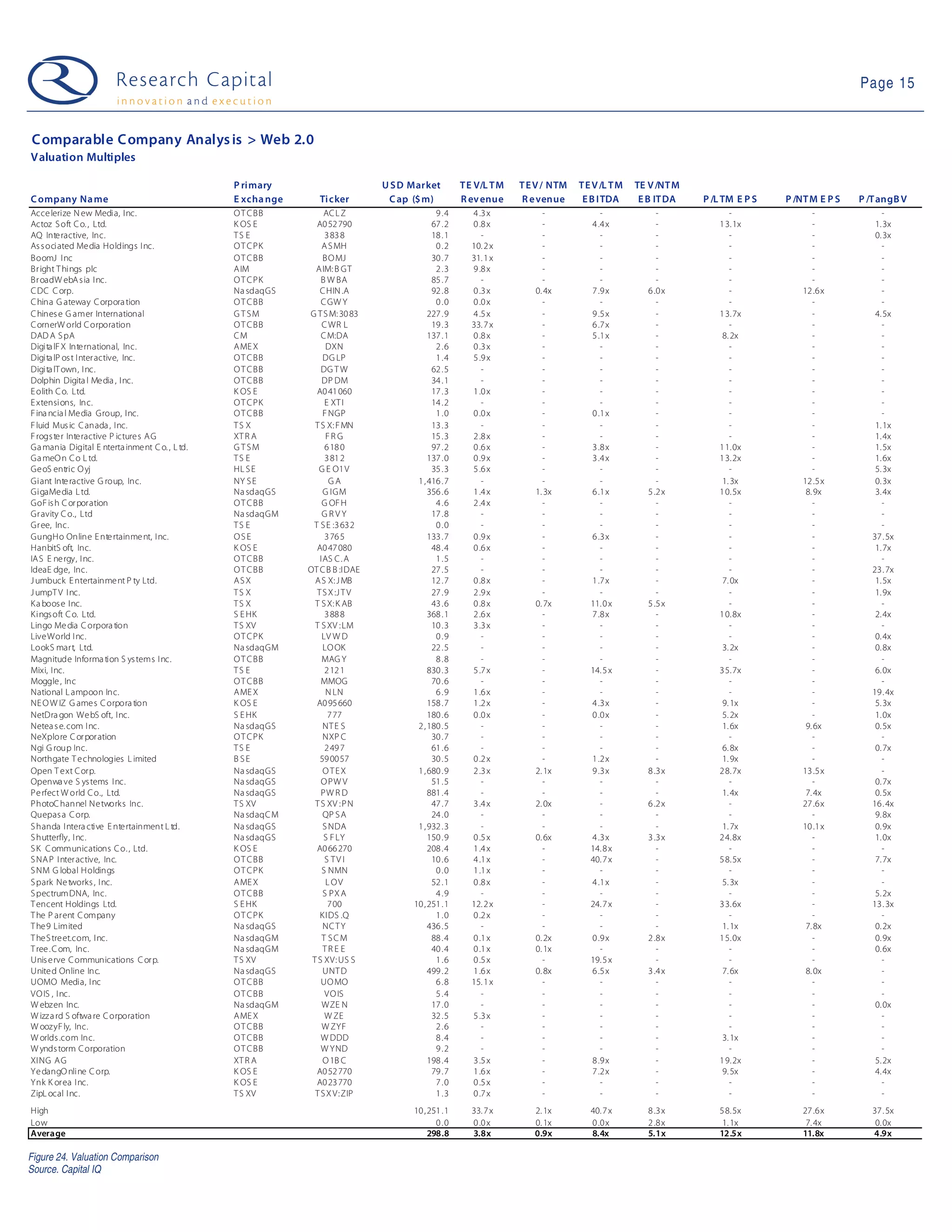

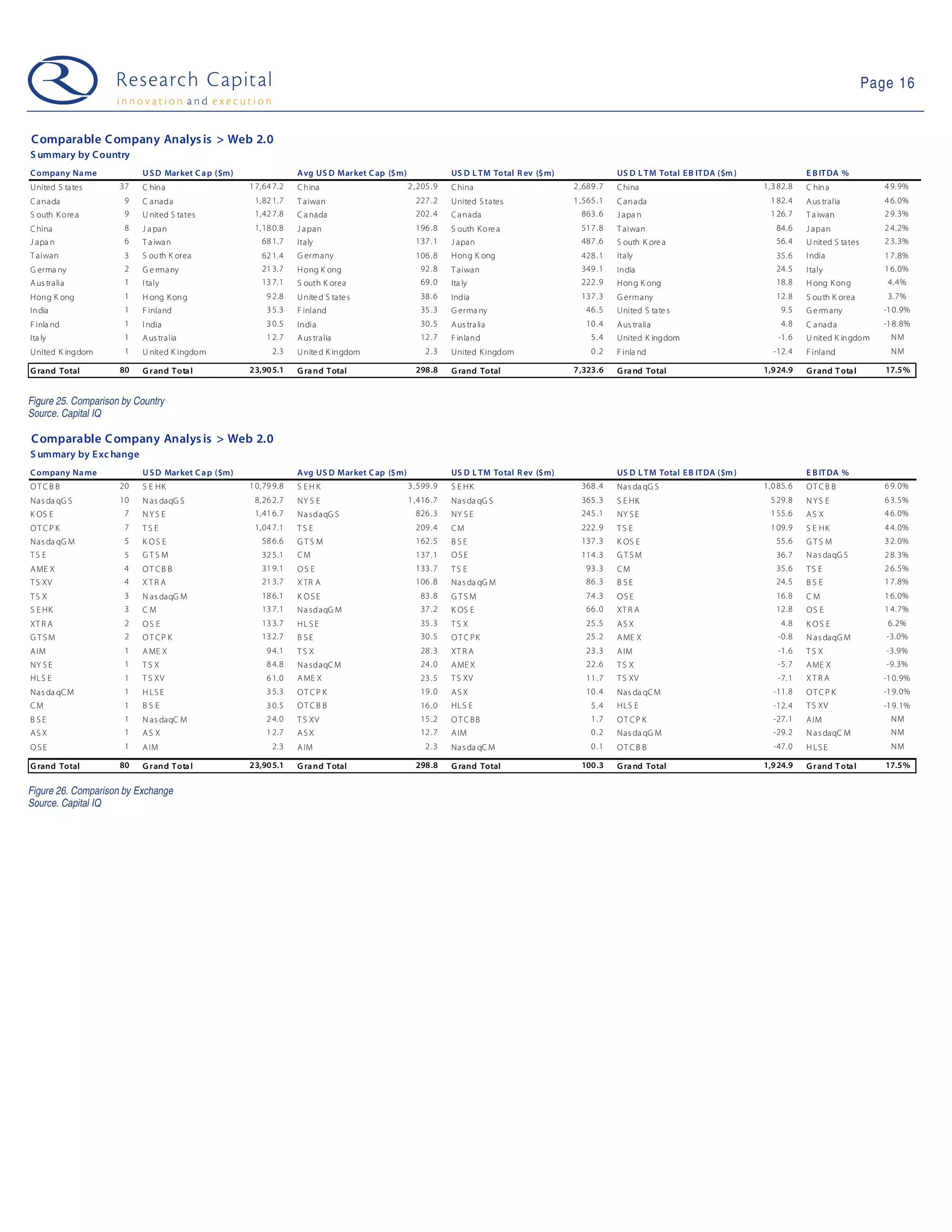

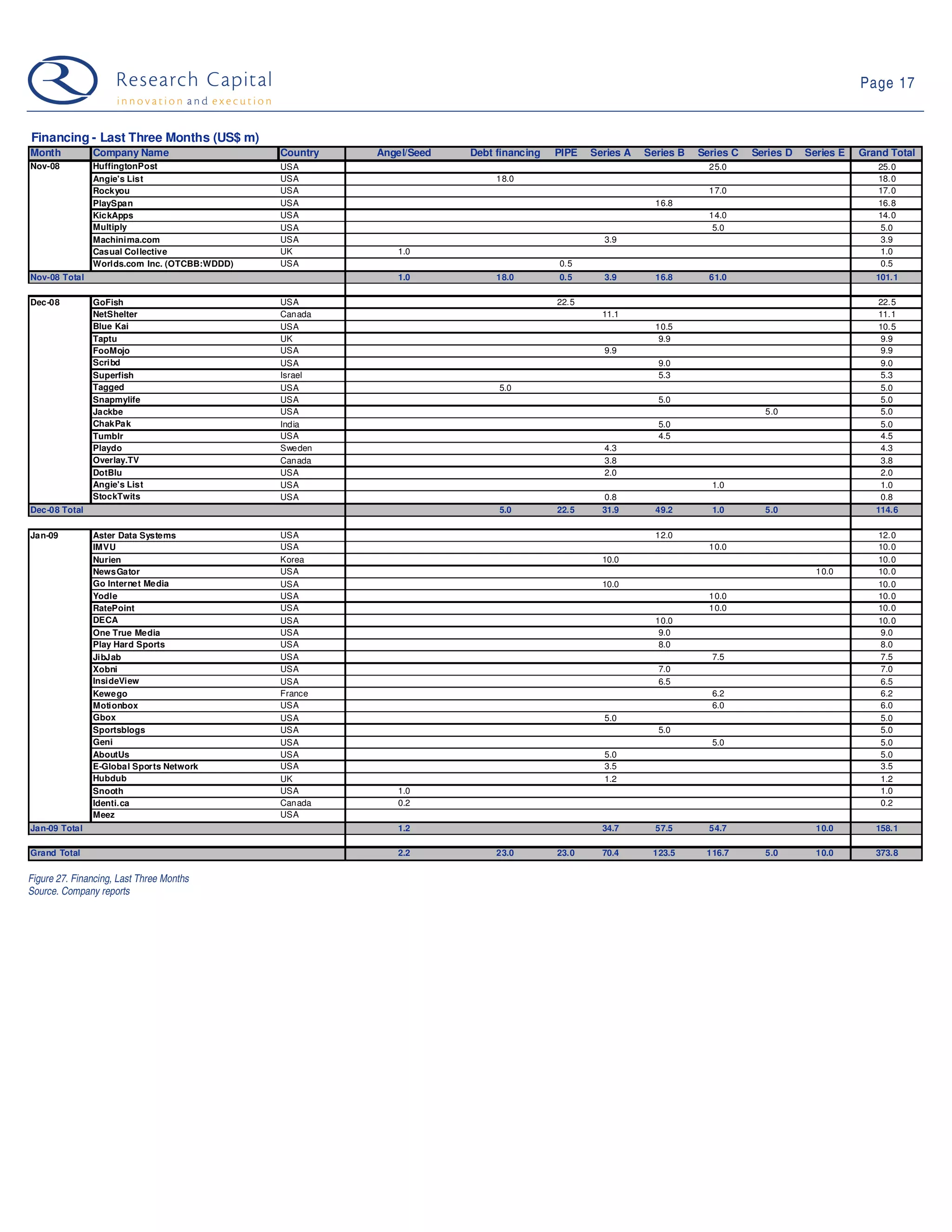

This document summarizes capital market activity in January 2009 for 80 public companies in the Web 2.0 sector. It notes that January saw 23 financings totaling $158.1 million, the highest number of financings since April 2008. The average financing was $6.9 million. Eight companies raised over $10 million each. Twitter is rumored to be raising over $20 million at a $250 million valuation. On average, the Web 2.0 companies have a $300 million market cap, $100 million in revenue, 17.5% EBITDA margins, and trade at 3.8x revenue and 8.4x EBITDA.

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)