Downloaded 368 times

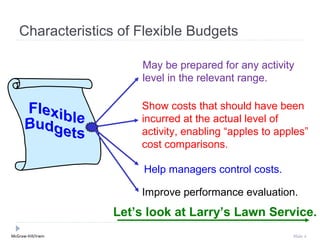

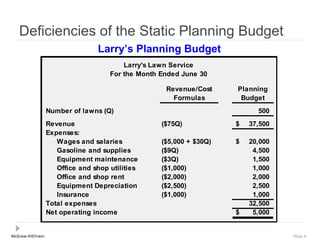

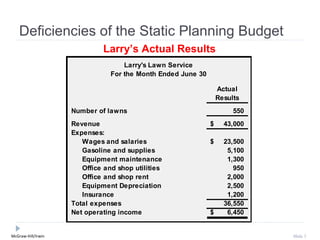

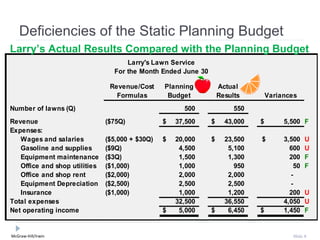

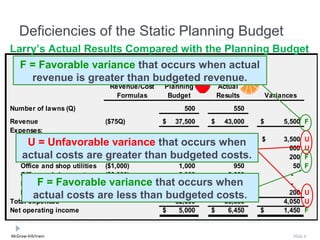

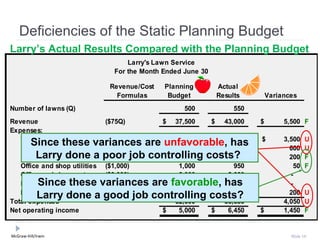

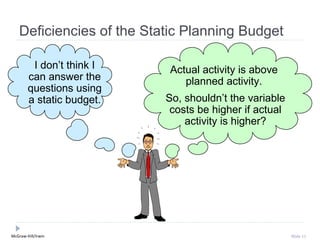

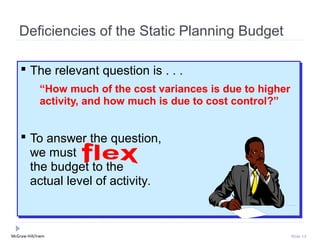

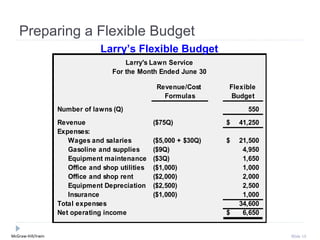

The document discusses flexible budgets and their advantages over static planning budgets. Flexible budgets can be prepared for any actual level of activity, allowing for "apples to apples" cost comparisons. They show costs that should have been incurred at the actual activity level, helping managers better evaluate performance and control costs. The document uses an example of a lawn care business to illustrate how a flexible budget accounts for actual activity being different than planned and allows for a more accurate analysis of variances.