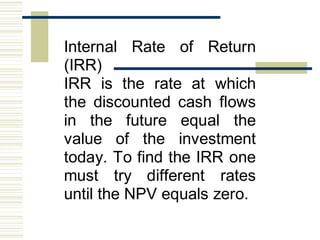

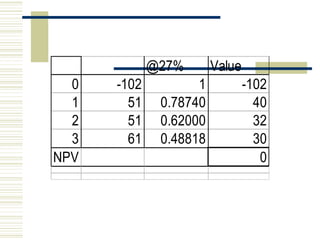

The document discusses various topics related to financial management. It covers the scope and objectives of financial management, types of financial decisions, sources of finance, analysis of financial statements and cash flow statements. It also describes various ratios used in financial analysis like liquidity ratios, leverage ratios, turnover ratios and profitability ratios. Capital budgeting techniques like payback period, NPV, IRR are also summarized along with the phases of capital budgeting.