Financial Management

Financial Managementmeans planning, organizing,

directing and controlling the financial activities such

as procurement and utilization of funds of the

enterprise. It means applying general management

principles to financial resources of the enterprise.

3.

Functions of FinancialManagement

Financial decisions - They relate to the raising of finance from

various resources which will depend upon decision on type of

source, period of financing, cost of financing and the returns

thereby.

Investment decisions includes investment in fixed assets (called as

capital budgeting). Investment in current assets are also a part of

investment decisions called as working capital decisions.

Dividend decision - The finance manager has to take decision with

regards to the net profit distribution. Net profits are generally

divided into two:

Dividend for shareholders- Dividend and the rate of it has to be decided.

Retained profits- Amount of retained profits has to be finalized which will

depend upon expansion and diversification plans of the enterprise.

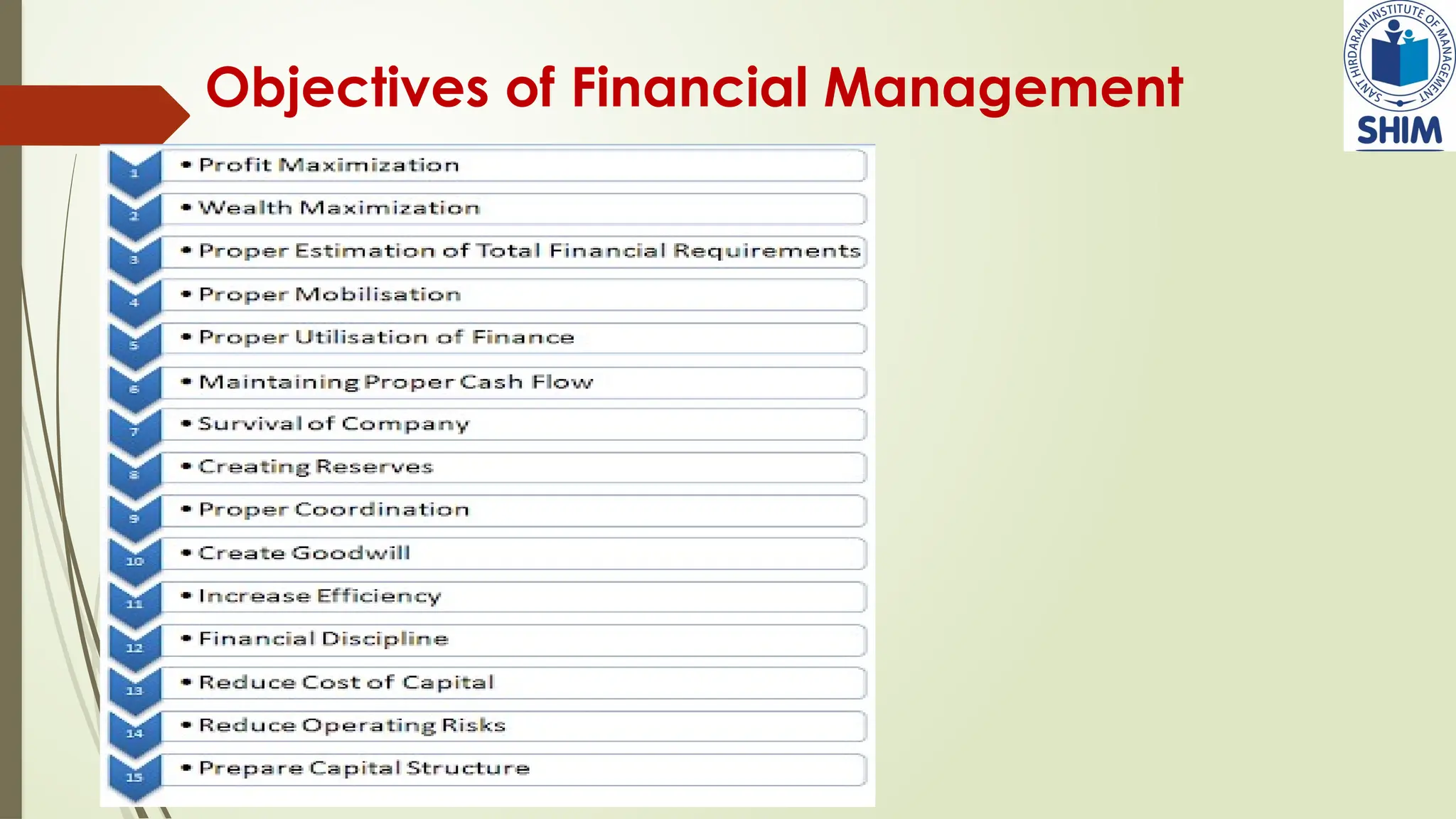

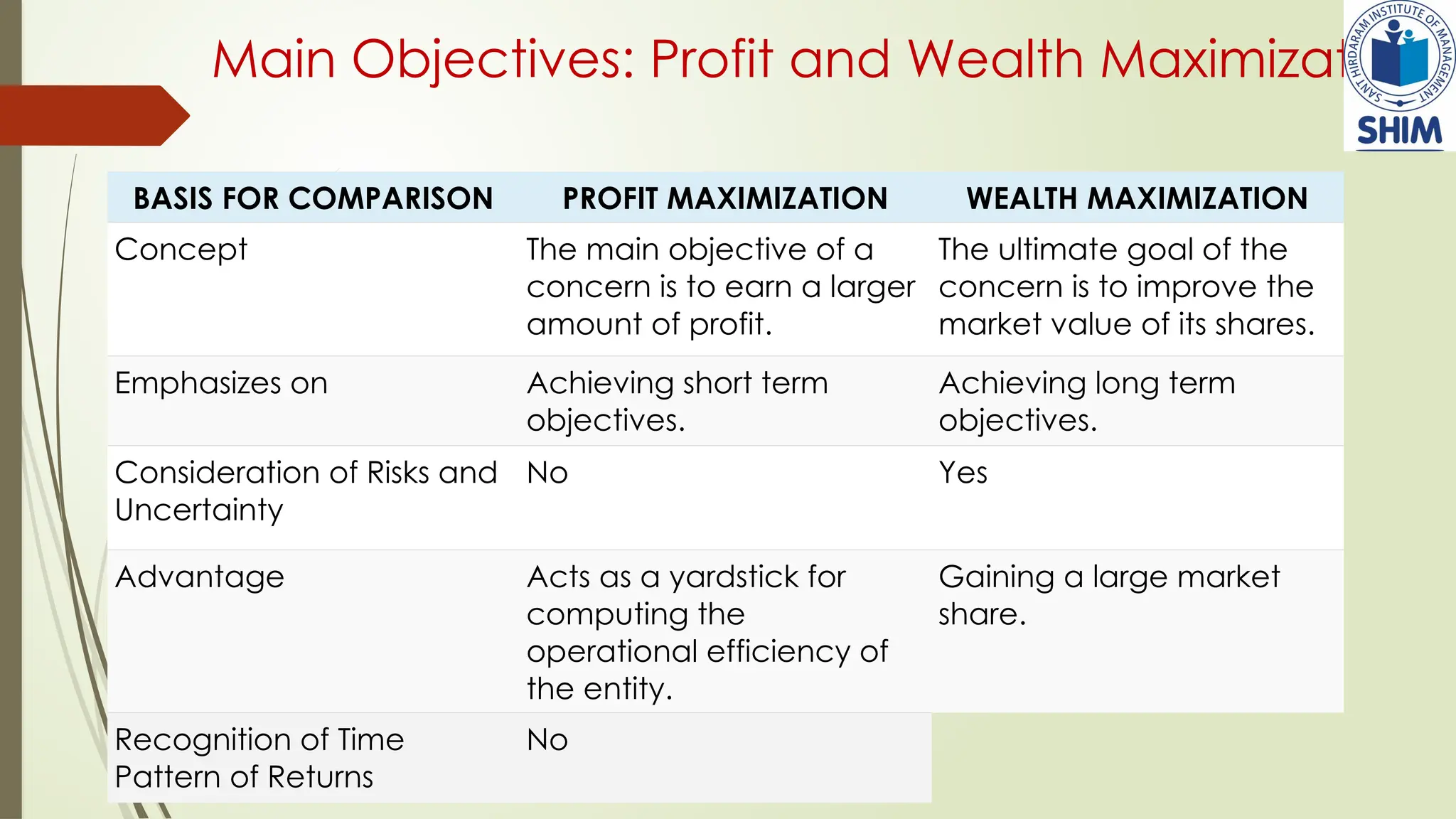

Main Objectives: Profitand Wealth Maximization

BASIS FOR COMPARISON PROFIT MAXIMIZATION WEALTH MAXIMIZATION

Concept The main objective of a

concern is to earn a larger

amount of profit.

The ultimate goal of the

concern is to improve the

market value of its shares.

Emphasizes on Achieving short term

objectives.

Achieving long term

objectives.

Consideration of Risks and

Uncertainty

No Yes

Advantage Acts as a yardstick for

computing the

operational efficiency of

the entity.

Gaining a large market

share.

Recognition of Time

Pattern of Returns

No

6.

Functions of FinancialManagement

Estimation of capital requirements: A finance manager has to make estimation with

regards to capital requirements of the company. This will depend upon expected costs

and profits and future programmes and policies of a concern. Estimations have to be

made in an adequate manner which increases earning capacity of enterprise.

Determination of capital composition: Once the estimation have been made, the

capital structure have to be decided. This involves short- term and long- term debt

equity analysis. This will depend upon the proportion of equity capital a company is

possessing and additional funds which have to be raised from outside parties.

Choice of sources of funds: For additional funds to be procured, a company has many

choices like-

Issue of shares and debentures

Loans to be taken from banks and financial institutions

Public deposits to be drawn like in form of bonds.

7.

Continued…..

Investment offunds: The finance manager has to decide to allocate funds into profitable

ventures so that there is safety on investment and regular returns is possible.

Disposal of surplus: The net profits decision have to be made by the finance manager. This

can be done in two ways:

Dividend declaration - It includes identifying the rate of dividends and other benefits like bonus.

Retained profits - The volume has to be decided which will depend upon expansional, innovational,

diversification plans of the company.

Management of cash: Finance manager has to make decisions with regards to cash

management. Cash is required for many purposes like payment of wages and salaries,

payment of electricity and water bills, payment to creditors, meeting current liabilities,

maintainance of enough stock, purchase of raw materials, etc.

Financial controls: The finance manager has not only to plan, procure and utilize the funds

but he also has to exercise control over finances. This can be done through many techniques

like ratio analysis, financial forecasting, cost and profit control, etc.

8.

Financial Statement Analysis

Financial Statement Analysis involves examining financial statements to

understand the financial health of an organization.

Objectives:

- Assess past performance

- Determine present financial position

- Forecast future performance

- Evaluate profitability, liquidity, and solvency

9.

Key Financial Statements

- Income Statement

- Balance Sheet

- Cash Flow Statement

- Statement of Changes in Equity

These statements provide a complete overview of a company’s financial

position and performance.

10.

Standards of Comparison

Comparisons in financial analysis are made using:

- Intracompany comparison (same firm over time)

- Intercompany comparison (competitor analysis)

- Industry standards or benchmarks

- Rule-of-thumb ratios

11.

Tools of FinancialAnalysis

- Ratio Analysis

- Horizontal Analysis (Trend Analysis)

- Vertical Analysis (Common-Size Statements)

- Comparative and Common-size Statements

12.

Ratio Analysis Categories

1. Liquidity Ratios:

- Current Ratio, Quick Ratio

2. Profitability Ratios:

- Net Profit Margin, Return on Assets (ROA), Return on Equity (ROE)

3. Activity Ratios:

- Inventory Turnover, Accounts Receivable Turnover

4. Leverage Ratios:

- Debt to Equity, Interest Coverage Ratio

5. Market Ratios:

- Earnings per Share (EPS), Price-Earnings Ratio

13.

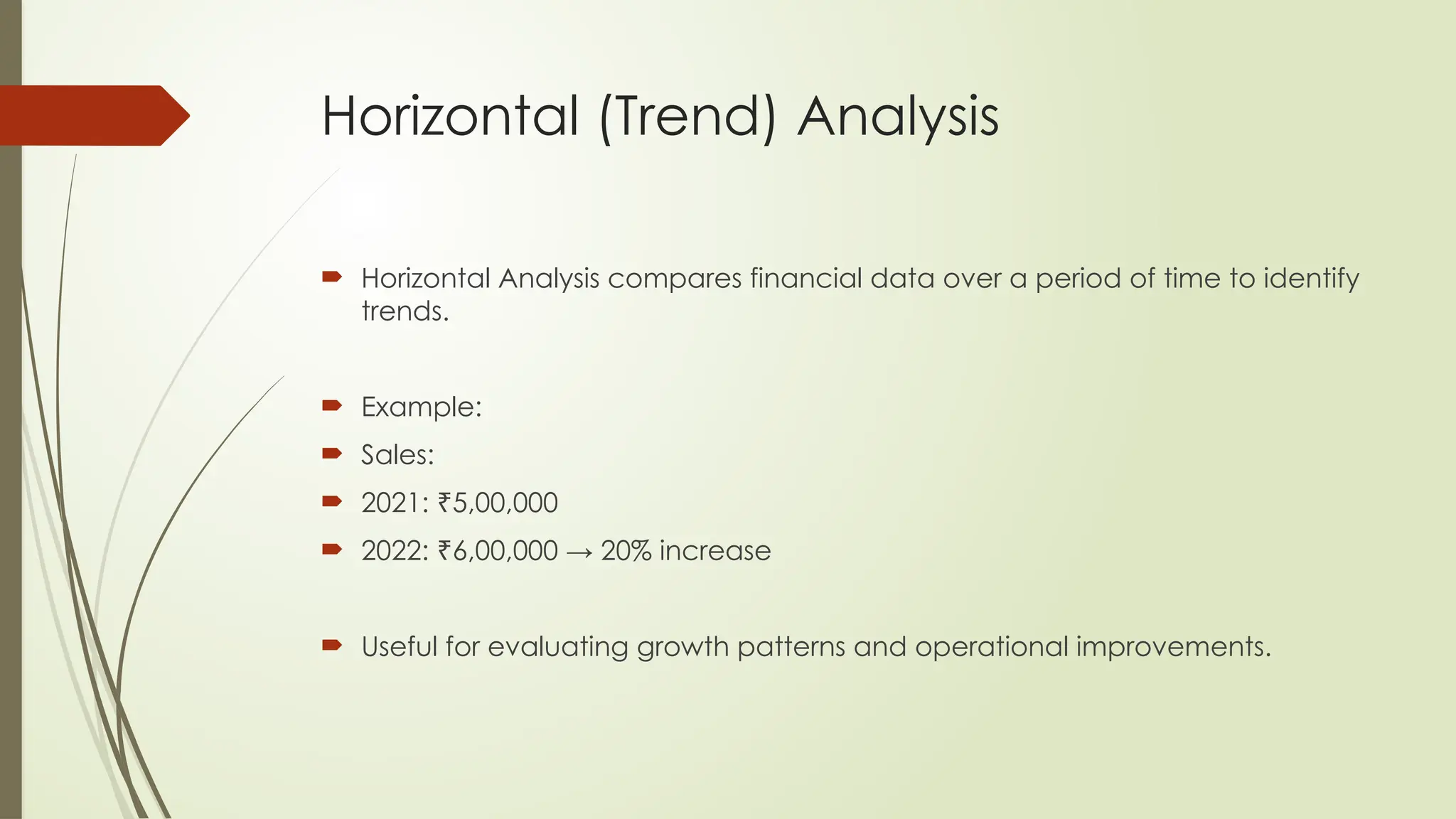

Horizontal (Trend) Analysis

Horizontal Analysis compares financial data over a period of time to identify

trends.

Example:

Sales:

2021: 5,00,000

₹

2022: 6,00,000 → 20% increase

₹

Useful for evaluating growth patterns and operational improvements.

14.

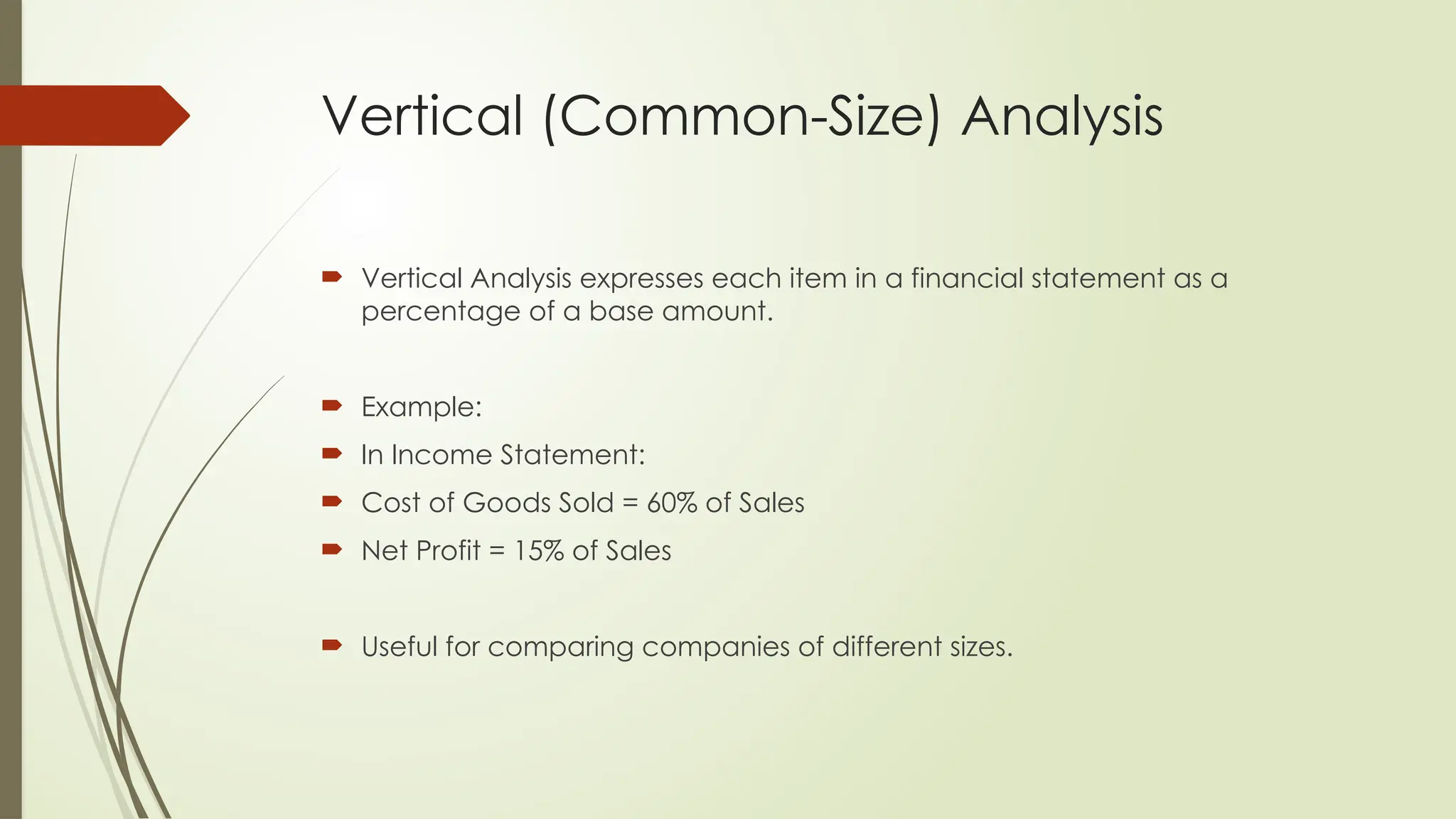

Vertical (Common-Size) Analysis

Vertical Analysis expresses each item in a financial statement as a

percentage of a base amount.

Example:

In Income Statement:

Cost of Goods Sold = 60% of Sales

Net Profit = 15% of Sales

Useful for comparing companies of different sizes.

15.

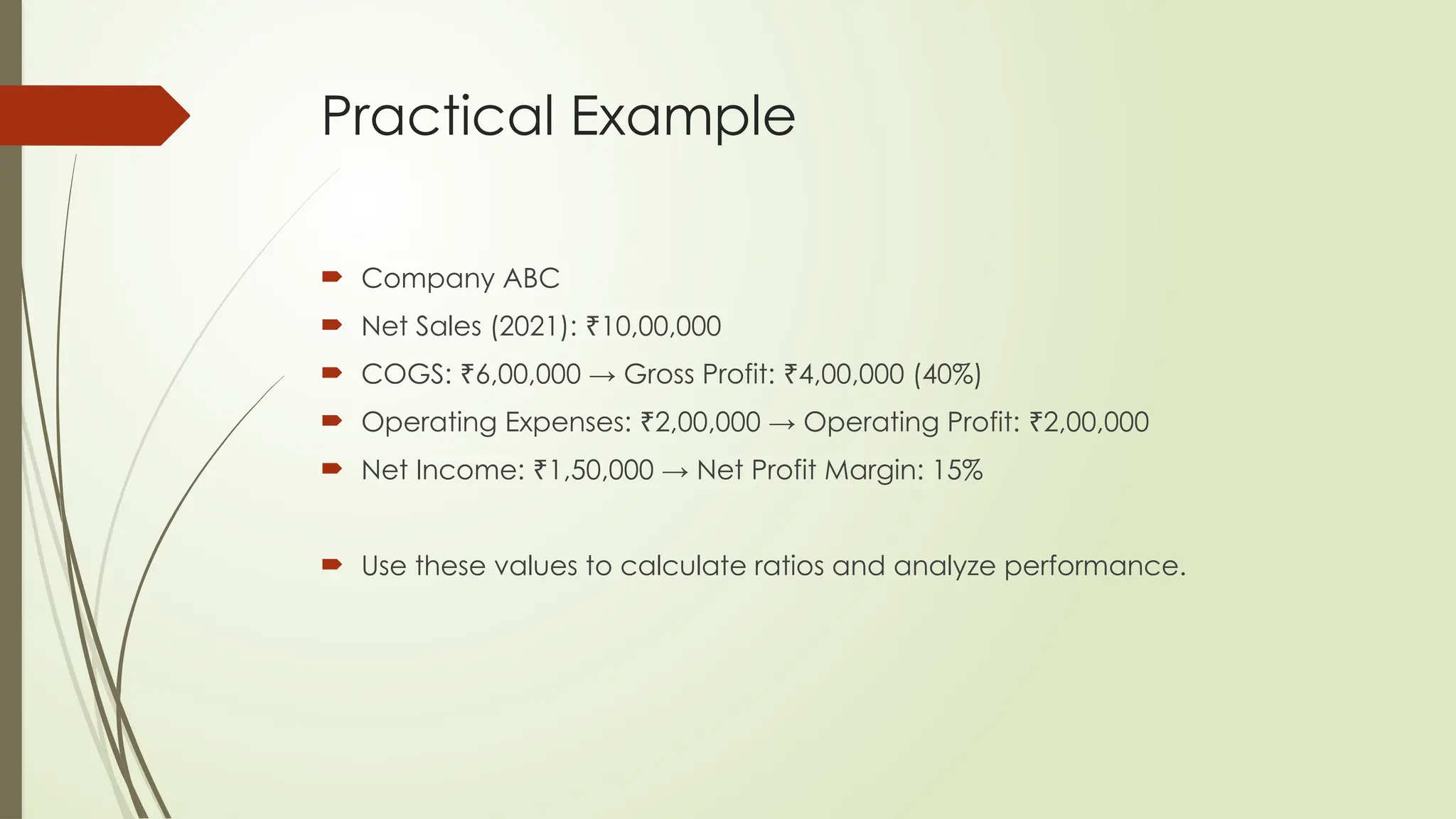

Practical Example

CompanyABC

Net Sales (2021): 10,00,000

₹

COGS: 6,00,000 → Gross Profit: 4,00,000 (40%)

₹ ₹

Operating Expenses: 2,00,000 → Operating Profit: 2,00,000

₹ ₹

Net Income: 1,50,000 → Net Profit Margin: 15%

₹

Use these values to calculate ratios and analyze performance.

16.

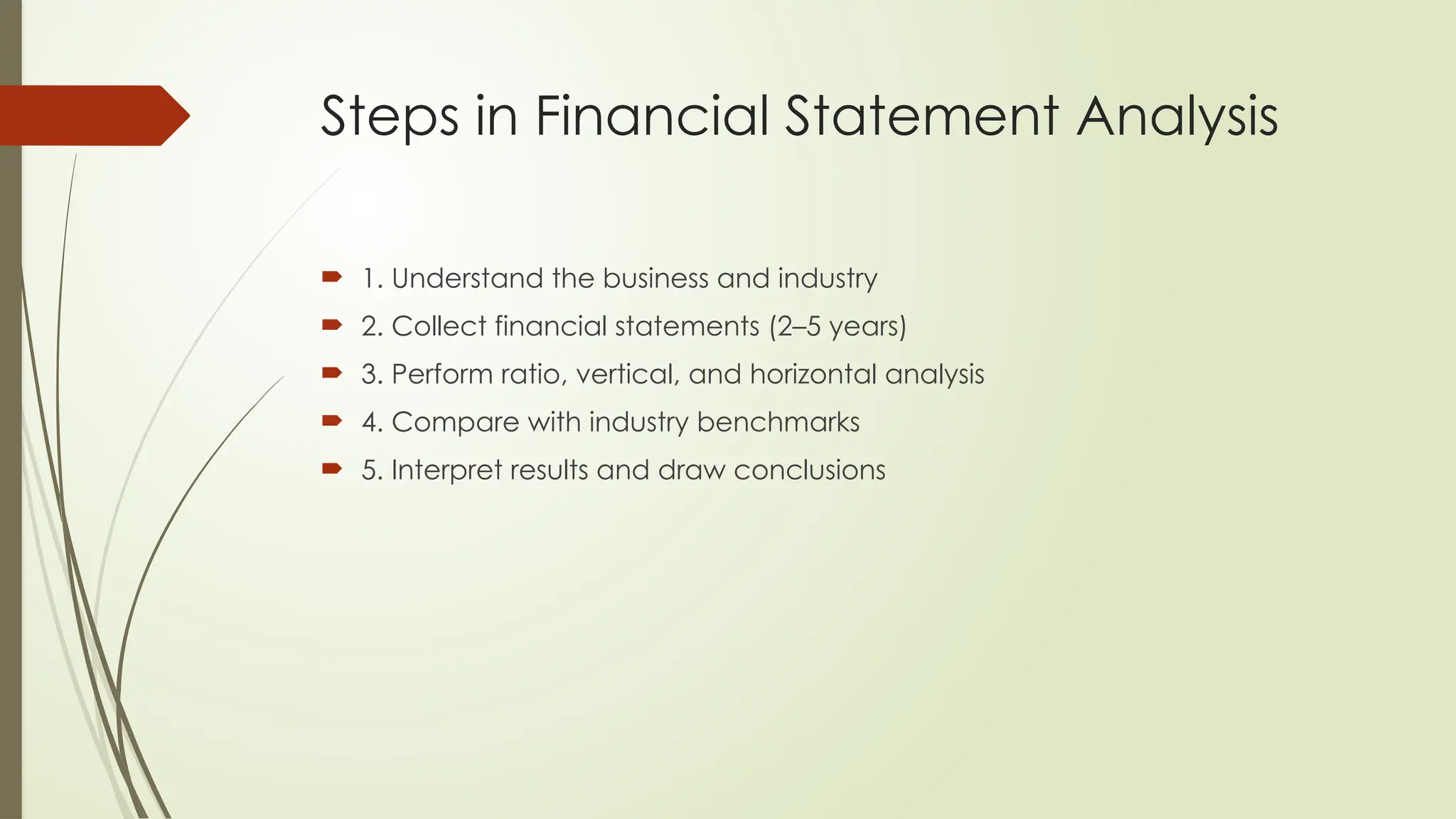

Steps in FinancialStatement Analysis

1. Understand the business and industry

2. Collect financial statements (2–5 years)

3. Perform ratio, vertical, and horizontal analysis

4. Compare with industry benchmarks

5. Interpret results and draw conclusions

17.

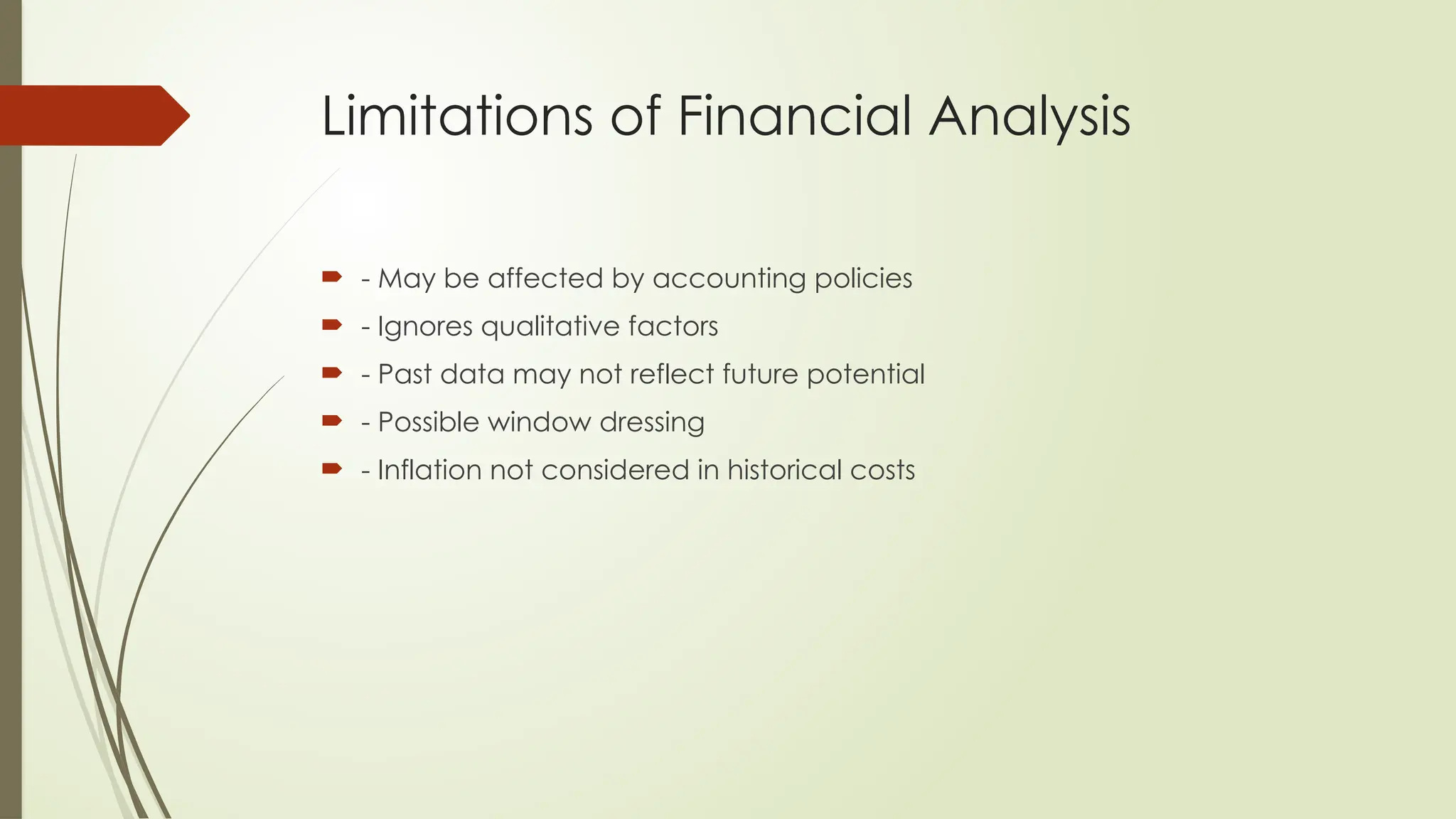

Limitations of FinancialAnalysis

- May be affected by accounting policies

- Ignores qualitative factors

- Past data may not reflect future potential

- Possible window dressing

- Inflation not considered in historical costs

18.

Conclusion & KeyTakeaways

- Financial statement analysis provides a clear view of a company’s

financial health

- Tools like ratio, vertical, and horizontal analysis aid decision-making

- Use multiple years of data and industry standards for better insights

- Be cautious of limitations and ensure holistic interpretation