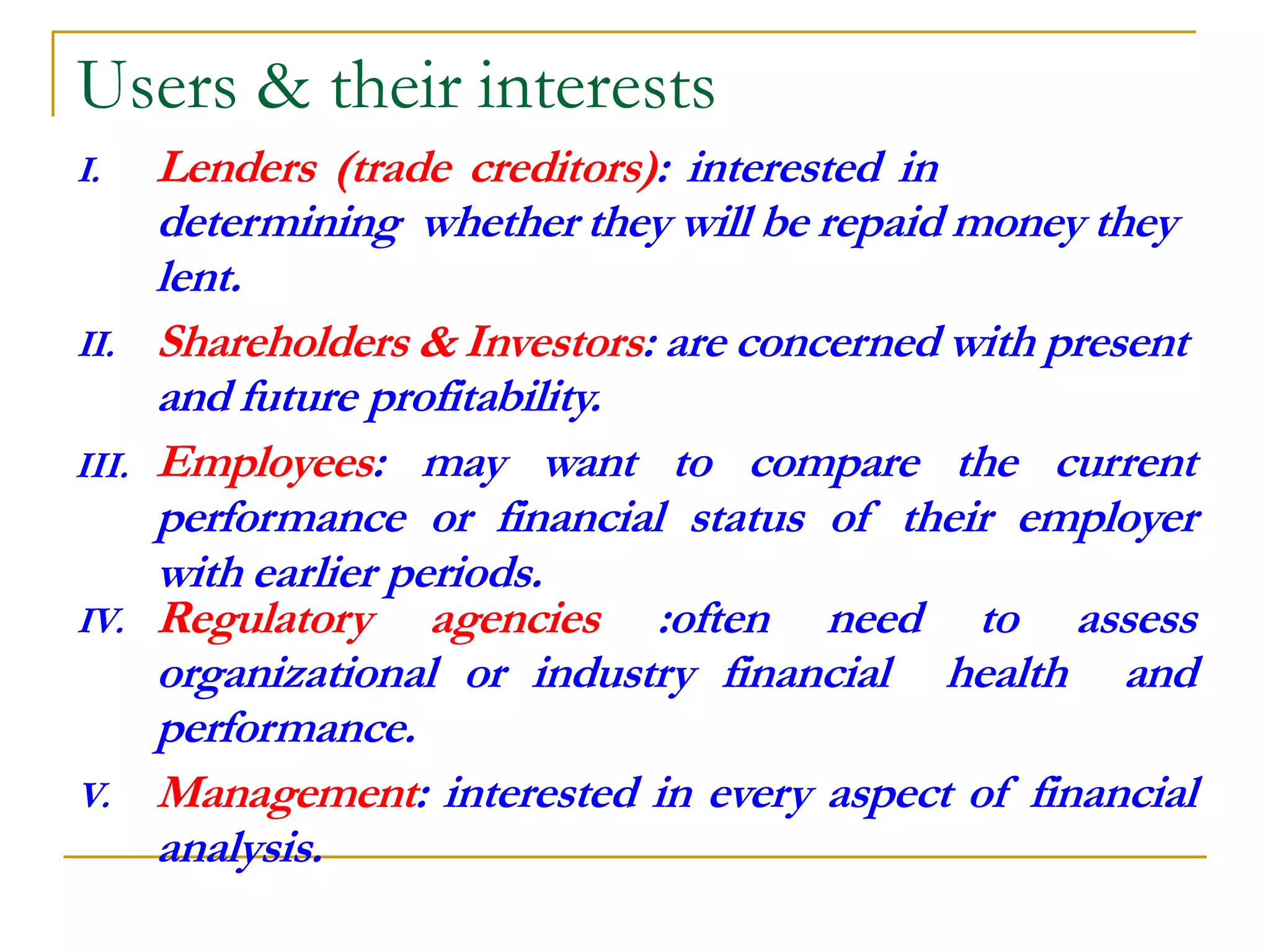

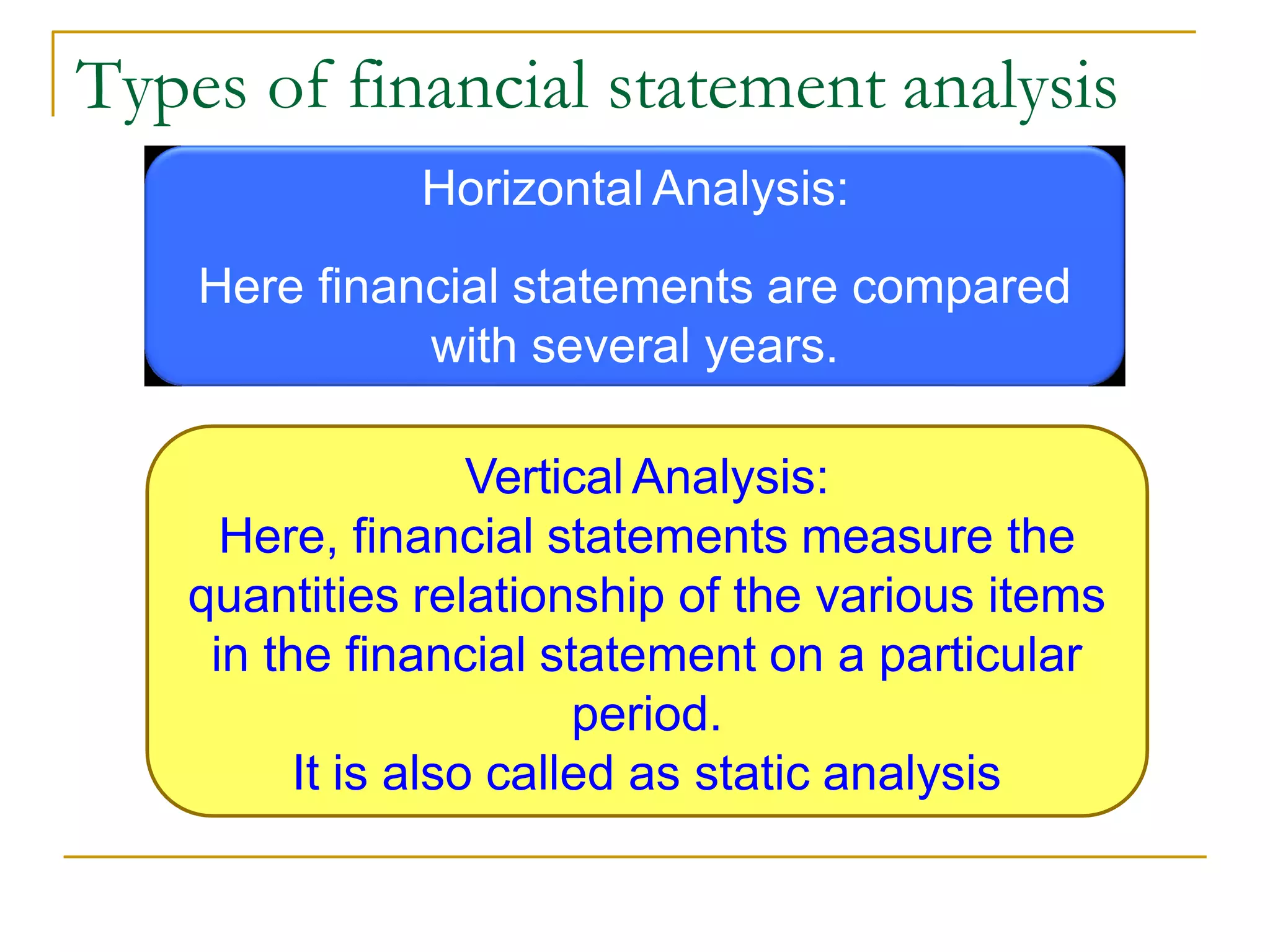

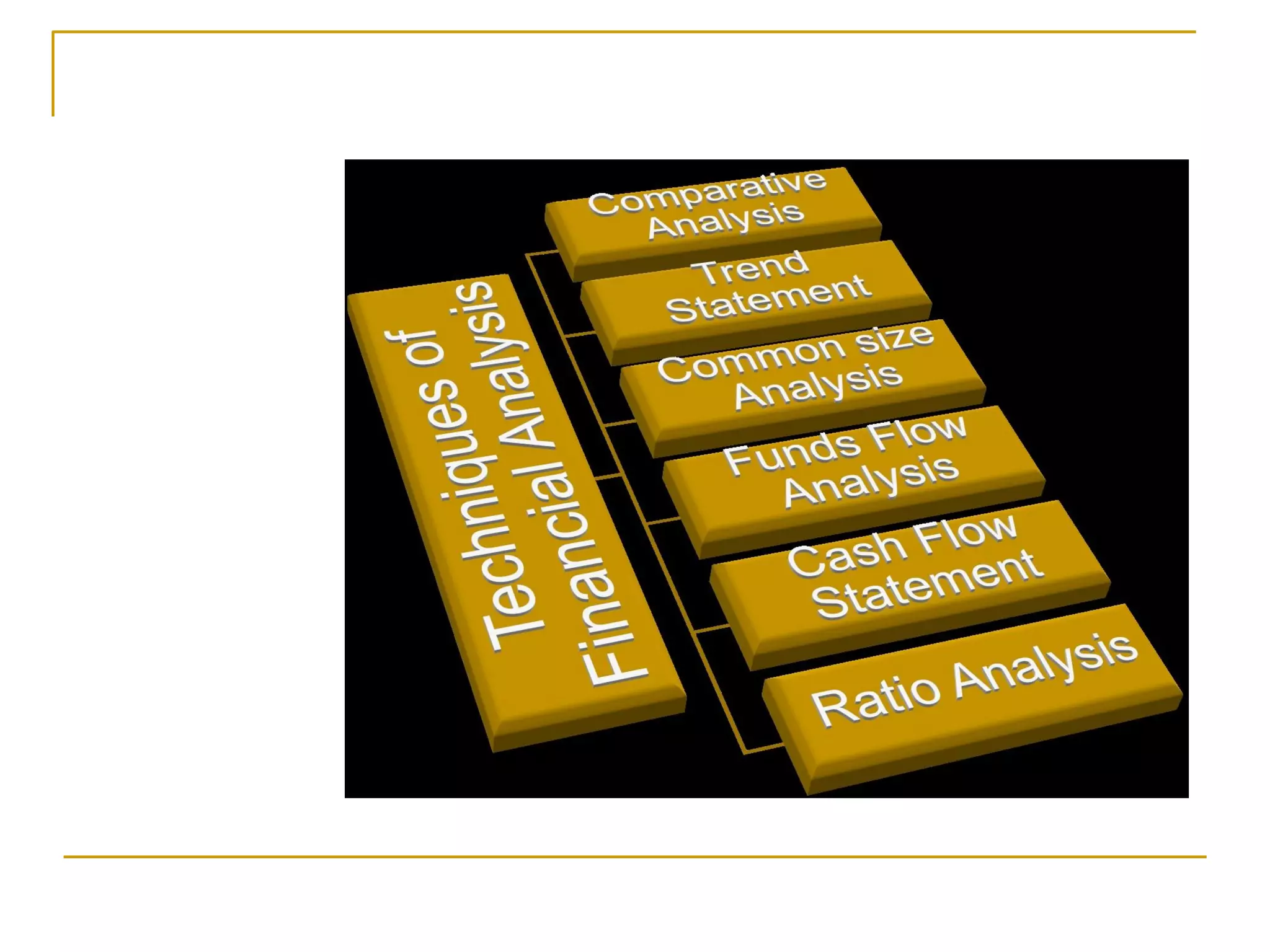

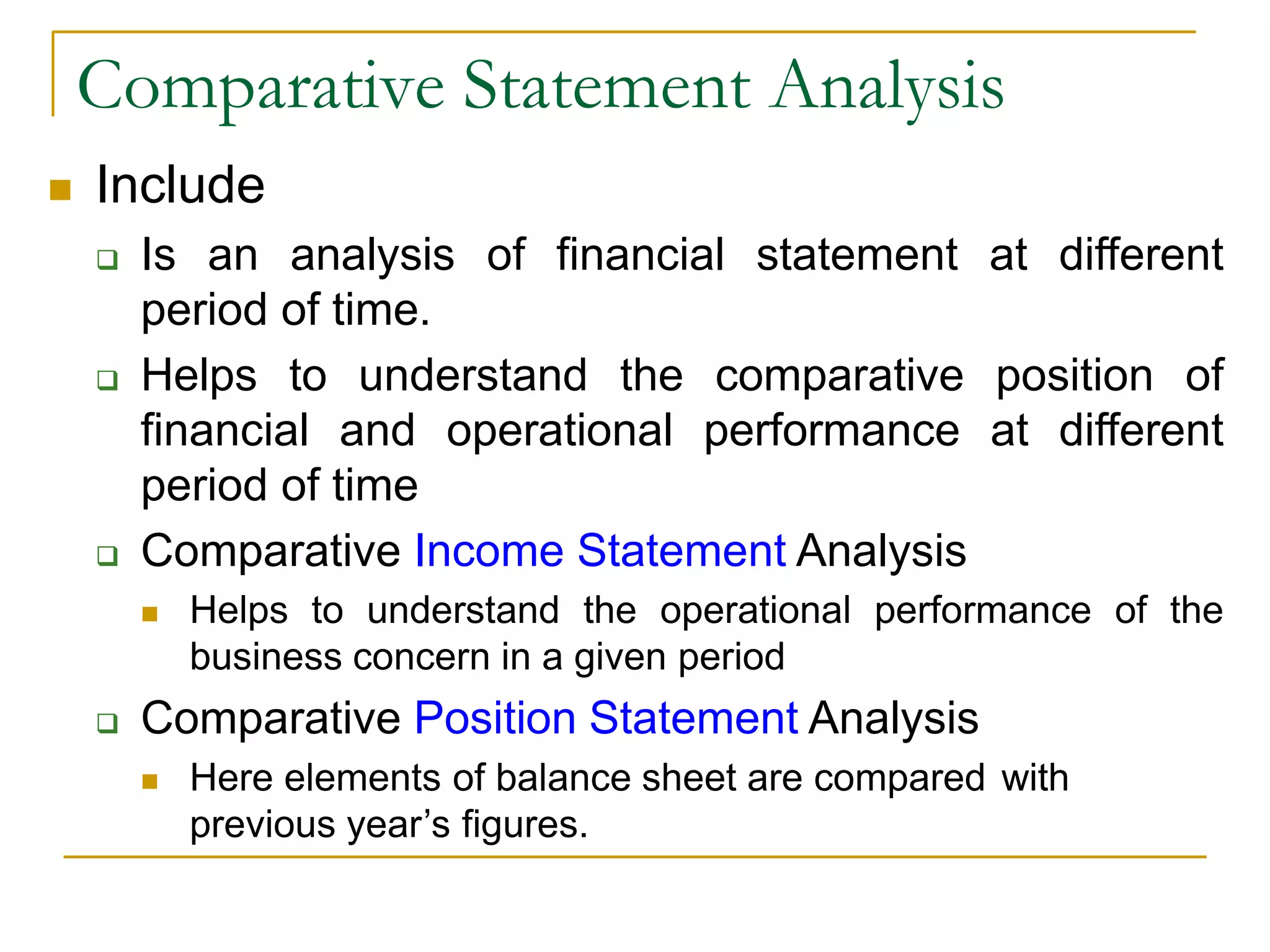

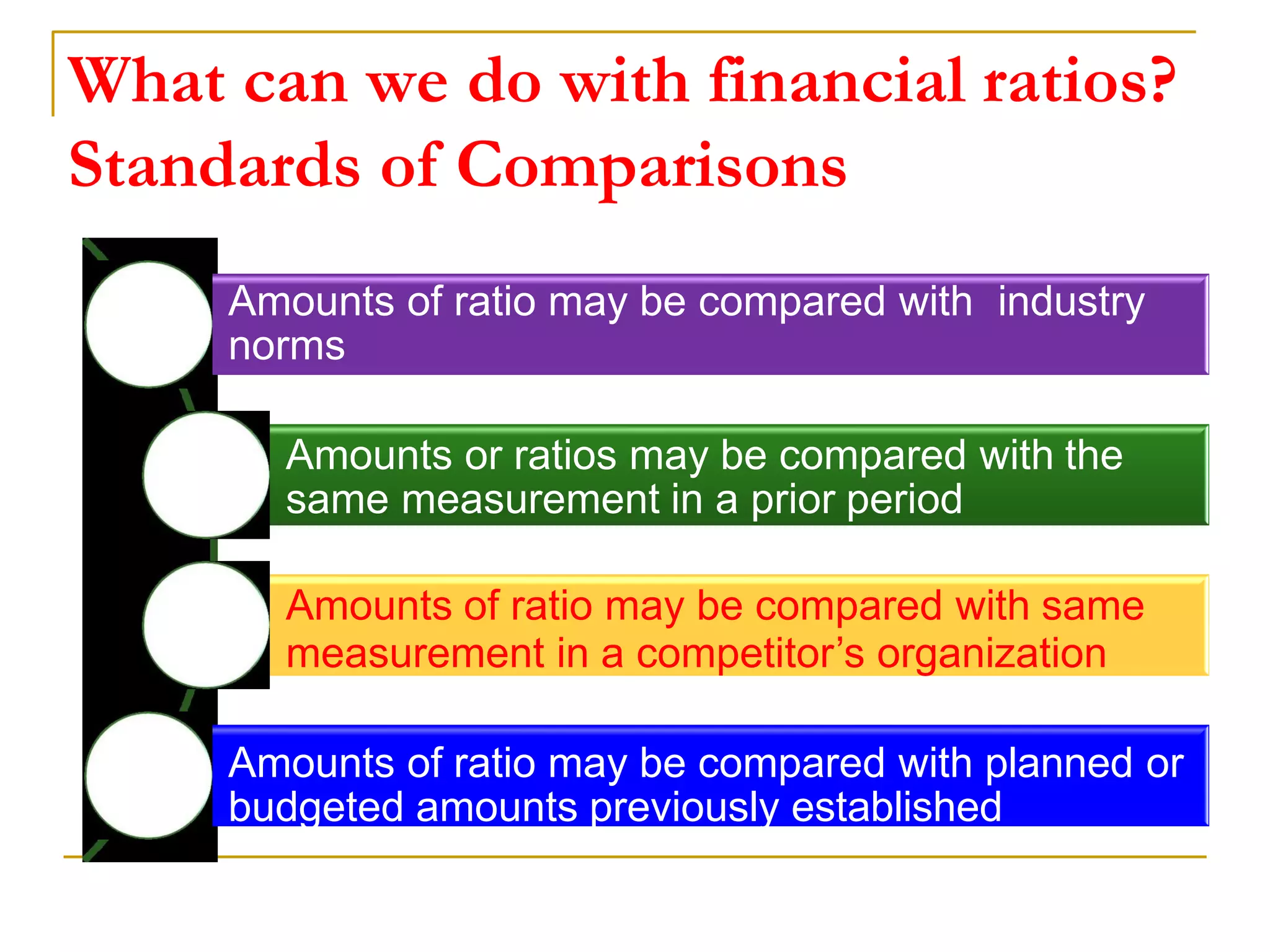

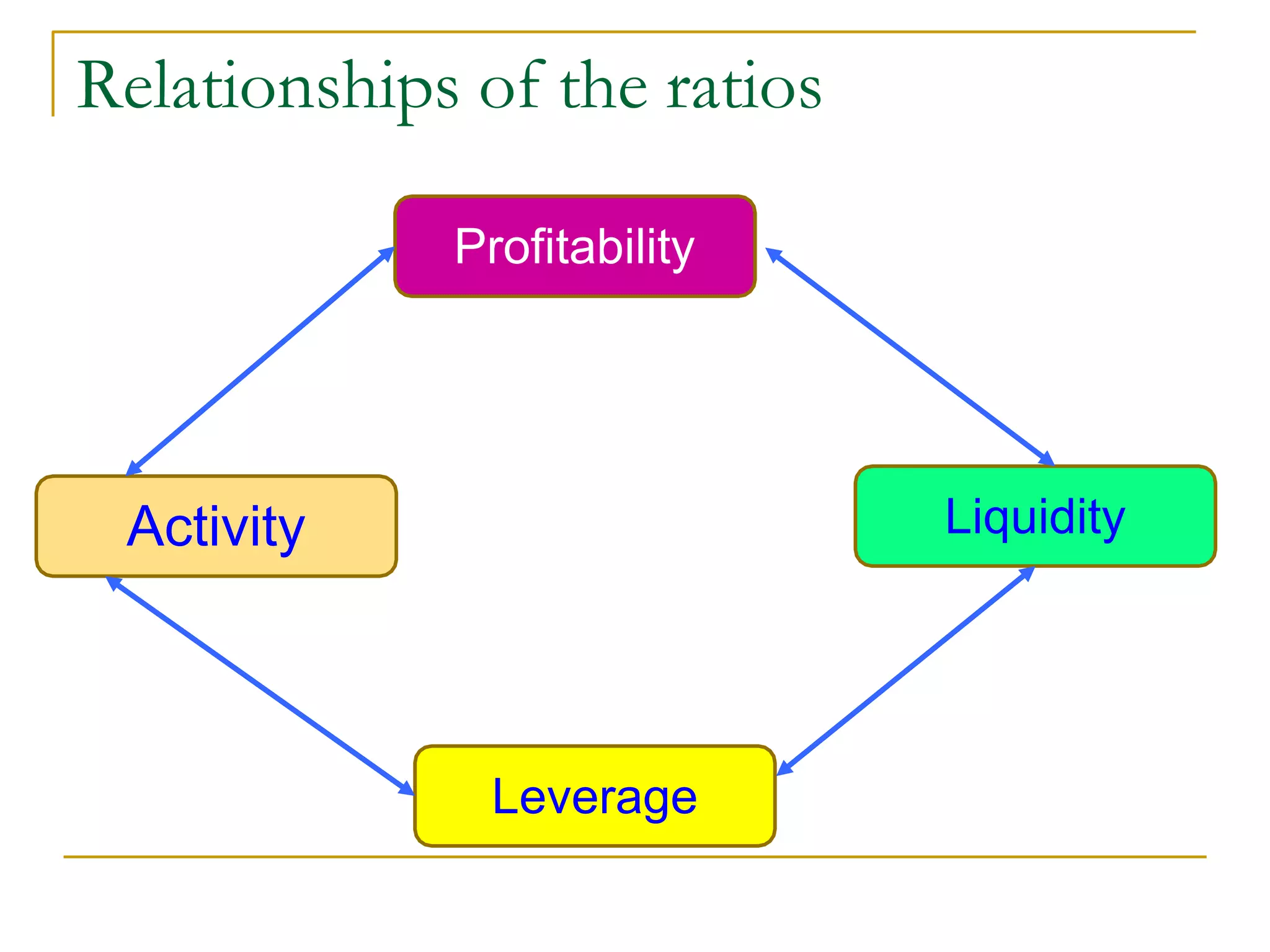

This document provides an overview of financial statement analysis. It discusses the different types of financial statement analysis including horizontal analysis, vertical analysis, comparative statement analysis, trend analysis, common size analysis, funds flow analysis, cash flow statement analysis, and ratio analysis. It outlines the different ratios used in financial analysis including liquidity ratios, activity ratios, solvency/leverage ratios, and profitability ratios. It also discusses the different users of financial statement analysis and their interests including lenders, shareholders/investors, employees, regulatory agencies, and management.

![Need for FSA

Financial statement analysis is used to identify the

trends and relationships between financial statement

items.

Both internal management and external users (such as

analysts, creditors, and investors) of the financial

statements need to evaluate a company's profitability,

liquidity, and solvency.

Nature of Analysis: The nature of the analysis depends

upon their [users] purpose or requirement. They [users]

make the necessary analysis and take the decision,

based on their assessment of the results obtained.](https://image.slidesharecdn.com/chap-231003200729-02524095/75/Financial-and-Managerial-Accounting-Note-3-2048.jpg)