VIP Call Girls Thane Sia 8617697112 Independent Escort Service Thane

QE Intraday Index Movement

1. Page 1 of 7

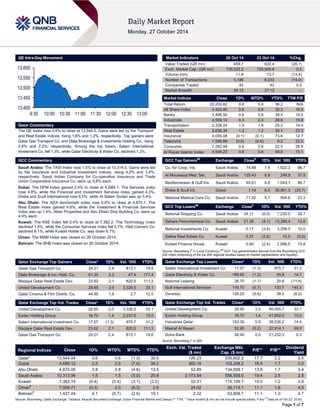

QE Intra-Day Movement

Qatar Commentary

The QE Index rose 0.6% to close at 13,544.0. Gains were led by the Transport and Real Estate indices, rising 1.6% and 1.2%, respectively. Top gainers were Qatar Gas Transport Co. and Dlala Brokerage & Investments Holding Co., rising 2.4% and 2.2%, respectively. Among the top losers, Salam International Investment Co. fell 1.3%, while Qatar Electricity & Water Co. declined 1.2%.

GCC Commentary

Saudi Arabia: The TASI Index rose 1.5% to close at 10,314.0. Gains were led by the Insurance and Industrial Investment indices, rising 4.2% and 3.4%, respectively. Saudi Indian Company for Co-operative Insurance and Trade Union Cooperative Insurance Co. were up 9.8% each.

Dubai: The DFM Index gained 2.5% to close at 4,689.1. The Services index rose 4.8%, while the Financial and Investment Services index gained 4.3%. Drake and Scull International rose 6.5%, while Al Salam Sudan was up 5.4%.

Abu Dhabi: The ADX benchmark index rose 0.8% to close at 4,870.1. The Real Estate index gained 4.6%, while the Investment & Financial Services index was up 1.4%. Aldar Properties and Abu Dhabi Ship Building Co. were up 4.9% each.

Kuwait: The KSE Index fell 0.4% to close at 7,382.2. The Technology index declined 1.0%, while the Consumer Services index fell 0.7%. Hilal Cement Co. declined 8.1%, while Kuwait Hotels Co. was down 6.7%.

Oman: The MSM Index was closed on 26 October 2014.

Bahrain: The BHB Index was closed on 26 October 2014.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Gas Transport Co.

24.21

2.4

813.1

19.6 Dlala Brokerage & Inv. Hold. Co. 61.30 2.2 47.4 177.4 Mazaya Qatar Real Estate Dev. 23.62 2.1 820.5 111.3 United Development Co. 28.65 2.0 3,328.5 33.1 Qatar Cinema & Film Distrib. Co. 44.90 1.8 2.7 12.0

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

United Development Co.

28.65

2.0

3,328.5

33.1 Ezdan Holding Group 18.70 1.4 2,237.6 10.0

Salam International Investment Co.

17.07

(1.3)

975.7

31.2 Mazaya Qatar Real Estate Dev. 23.62 2.1 820.5 111.3

Qatar Gas Transport Co.

24.21

2.4

813.1

19.6

Market Indicators 26 Oct 14 23 Oct 14 %Chg.

Value Traded (QR mn)

459.7

622.4

(26.1) Exch. Market Cap. (QR mn) 730,525.2 726,545.6 0.5

Volume (mn)

11.8

13.7

(13.4) Number of Transactions 5,186 6,033 (14.0)

Companies Traded

42

42

0.0 Market Breadth 24:12 27:12 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return

20,200.82

0.6

0.6

36.2

N/A All Share Index 3,423.40 0.6 0.6 32.3 16.5

Banks

3,406.50

0.6

0.6

39.4

16.0 Industrials 4,509.13 0.3 0.3 28.8 15.8

Transportation

2,328.24

1.6

1.6

25.3

14.4 Real Estate 2,638.39 1.2 1.2 35.1 23.3

Insurance

4,055.08

(0.1)

(0.1)

73.6

12.7 Telecoms 1,586.89 (0.6) (0.6) 9.2 22.5

Consumer

7,283.48

0.6

0.6

22.5

28.9 Al Rayan Islamic Index 4,548.22 0.6 0.6 49.8 19.1

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Co. for Coop. Ins.

Saudi Arabia

74.68

7.8

1,622.3

96.7 Al Mouwasat Med. Ser. Saudi Arabia 135.43 6.8 249.9 37.8

Mediterranean & Gulf Ins.

Saudi Arabia

69.61

6.8

1,043.1

86.7 Drake & Scull Int. Dubai 1.14 6.5 39,961.3 (25.7)

National Medical Care Co.

Saudi Arabia

71.02

5.7

504.8

23.3

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

National Shipping Co.

Saudi Arabia

34.11

(6.0)

7,230.5

28.7 Sahara Petrochemical Co. Saudi Arabia 21.38 (4.1) 13,289.4 12.6

National Investments Co.

Kuwait

0.17

(3.4)

3,208.5

10.0 Salhia Real Estate Co. Kuwait 0.37 (2.6) 15.0 (5.0)

Kuwait Finance House

Kuwait

0.80

(2.4)

2,856.5

15.8

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Salam International Investment Co

17.07

(1.3)

975.7

31.2 Qatar Electricity & Water Co. 189.60 (1.2) 55.8 14.7

National Leasing

26.70

(1.1)

20.6

(11.4) Gulf International Services 119.70 (0.7) 120.7 145.3

Ooredoo

126.20

(0.6)

38.0

(8.0)

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

United Development Co.

28.65

2.0

95,055.7

33.1 Ezdan Holding Group 18.70 1.4 41,602.0 10.0

Industries Qatar

193.30

0.9

38,536.2

14.4 Masraf Al Rayan 52.90 (0.2) 22,914.1 69.0

Doha Bank

58.40

0.0

21,232.3

0.3

Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield

Qatar*

13,544.04

0.6

0.6

(1.3)

30.5

126.23

200,602.2

17.7

2.2

3.5 Dubai 4,689.12 2.5 2.5 (7.0) 39.2 360.16 103,208.2 18.5 1.7 2.0

Abu Dhabi

4,870.06

0.8

0.8

(4.6)

13.5

52.89

134,558.1

13.8

1.7

3.4 Saudi Arabia 10,313.96 1.5 1.5 (5.0) 20.8 2,173.64 558,509.5 19.4 2.5 2.8

Kuwait

7,382.19

(0.4)

(0.4)

(3.1)

(2.2)

52.31

110,109.7

19.0

1.2

3.8 Oman# 7,009.71 (0.3) 2.0 (6.3) 2.6 24.02 26,114.1 11.1 1.6 4.0

Bahrain#

1,437.04

0.1

(0.7)

(2.6)

15.1

2.32

53,908.7

11.1

1.0

4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any # Data as of Oct 23, 2014)

13,40013,45013,50013,55013,6009:3010:0010:3011:0011:3012:0012:3013:00

2. Page 2 of 7

Qatar Market Commentary

The QE Index rose 0.6% to close at 13,544.0. Transport and Real Estate indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari shareholders.

Qatar Gas Transport Co. and Dlala Brokerage & Invest. Holding Co. were the top gainers, rising 2.4% and 2.2%, respectively. Among the top losers, Salam International Investment Co. fell 1.3%, while Qatar Electricity & Water Co. declined 1.2%.

Volume of shares traded on Sunday fell by 13.4% to 11.8mn from 13.7mn on Thursday. Further, as compared to the 30-day moving average of 13.7mn, volume for the day was 13.4% lower. United Development Co. and Ezdan Holding Group were the most active stocks, contributing 28.1% and 18.9% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings

Earnings Releases Company Market Currency Revenue (mn)3Q2014 % Change YoY Operating Profit (mn) 3Q2014 % Change YoY Net Profit (mn) 3Q2014 % Change YoY Hail Cement Co. (HCC) Saudi Arabia SR – – 25.5 52.1% 25.1 48.2% Tabuk Agriculture Development Co. (TADCO) Saudi Arabia SR – – 0.7 -49.4% 3.3 211.0%

Saudi Basic Industries Corp. (SABIC)

Saudi Arabia

SR

–

–

1041.0

-7.6%

6180.0

-4.5% Saudi Printing and Packaging Co. (SPPC) Saudi Arabia SR – – 14.6 -43.4% 12.1 -16.0%

Southern Province Cement Co. (SPCC)

Saudi Arabia

SR

–

–

175.0

-6.9%

285.0

52.4% Saudi Orix Leasing Co. (SOLC) Saudi Arabia SR – – 46.7 18.1% 29.6 20.4%

Sahara Petrochemical Co. (Petrochemical)

Saudi Arabia

SR

–

–

1.9

-97.3%

17.1

-88.5% Saudi Arabian Amiantit Co. (Amiantit) Saudi Arabia SR – – 21.6 -51.3% 17.6 -0.1%

Abdullah Al Othaim Markets Co. (A.Othaim Market)

Saudi Arabia

SR

–

–

36.8

4.0%

45.3

8.0% The National Shipping Co. of Saudi Arabia (Bahri) Saudi Arabia SR – – 92.4 -30.4% 84.9 -49.9%

Wataniya Insurance Co. (Wataniya)

Saudi Arabia

SR

115.5

-6.3%

–

–

3.1

771.0% Saudi Transport and Investment Co. (mubarrad) Saudi Arabia SR – – 26.0 NA 32.8 2594.3%

Saudi Electricity Co. (Saudi Electric.)

Saudi Arabia

SR

–

–

2586.0

-5.3%

2668.0

-6.5% Ash-Sharqiyah Development Co. (Sharqiya Dev Co.) Saudi Arabia SR – – -0.9 NA -0.2 NA

Allied Cooperative Insurance Group (ACIG)

Saudi Arabia

SR

50.4

-21.9%

–

–

1.9

-44.0% Saudi Vitrified Clay Pipes Co. (SVCP) Saudi Arabia SR – – 26.2 44.8% 26.0 48.6%

Mohammad Al Mojil Group Co. (MMG)*

Saudi Arabia

SR

–

–

-367.6

NA

-432.0

NA Nama Chemicals Co. (Nama Chemicals) Saudi Arabia SR – – -21.0 33.5% -23.4 NA

Alabdullatif Industrial Investment Co. (AlAbdullatif)

Saudi Arabia

SR

–

–

48.5

-24.3%

46.3

-29.3% Basic Chemical Industries Co. (BCI) Saudi Arabia SR – – 8.1 -36.7% 1.2 -81.0%

Halwani Bros (H B)

Saudi Arabia

SR

–

–

33.6

29.2%

20.5

20.6% RAK Properties Abu Dhabi AED – – – – 23.0 17.3%

Source: Company data, DFM, ADX, MSM (* 9M2014 results)

Overall Activity Buy %* Sell %* Net (QR)

Qatari

69.84%

77.76%

(36,406,466.50) Non-Qatari 30.15% 22.24% 36,406,466.50

3. Page 3 of 7

News

Qatar

QEWS to boost desalination capacity at Ras Laffan (clarification on the Bloomberg article) – Qatar Electricity & Water Company (QEWS) has increased the planned desalination capacity at its Ras Laffan project to 65mn gallons per day. This project will start operating from mid-2017 onward and QEWS will own 60% of the project. Previously, this project was expected to possess a desalination capacity of around 36 MIGD. QEWS’ other near-term project, RAF A2, should begin from mid-2015 as planned and will supply 36 MIGD of water at a 100%-ownership stake to the company. We note the article in Bloomberg (picked up from Al-Sharq) is ambiguous. (QNBFS Research, Bloomberg)

QNCD posts net profit of QR332mn for 9M2014 – Qatar National Cement (QNCD) posts net profit of QR332mn for the nine months period ended September 30, 2014 in comparison to a net profit of QR322mn for the corresponding period last year. The company’s EPS amounted to QR6.76 for the period ended September 30, 2014 versus QR6.56 for the corresponding period in 2013. (QE)

ERES reports net profit of QR296.9mn in 3Q2014 – Ezdan Holding Group Company (ERES) reported a net profit of QR296.9mn in 3Q2014, reflecting an increase of 15.3% on a QoQ basis (+24.3% on a YoY basis). The YoY increase in net profit was primarily led by rise in rental income and higher net gain on sale of available-for-sale financial assets. Revenue stood at QR360.5mn in 3Q2014, showing an increase of 2.6% on QoQ basis (+35.3% on a YoY basis). ERES’s EPS for 3Q2014 amounted to QR0.11 versus QR0.09 in 3Q2013. (QE)

QOIS’ net profit declines by 48.7% QoQ in 3Q2014 – Qatar Oman Investment Company (QOIS) reported a net profit of QR3.0mn in 3Q2014, indicating a decline of 48.7% on a QoQ basis (+28.9% on a YoY basis). EPS amounted to QR0.7 for the 9M2014 as compared to QR0.5 for the 9M2013. Net investment & interest income fell by 39.9% QoQ to QR4.1mn in 3Q2014. (QE)

UDCD’s net profit rises 11% YoY to QR559mn in 9M2014 – United Development Company (UDCD) posted an 11% YoY increase in net profit to QR559.0mn in 9M2014. Gross profit was reported at QR909.7mn, compared to QR747mn for 9M2013. UDCD’ EPS reached QR1.58 for 9M2014 from QR1.43 in 9M2013. (Peninsula Qatar)

QGRI posts net profit of QR172.2mn for 9M2014 – Qatar General Insurance and Reinsurance Company (QGRI) posted a net profit of QR172.2mn for the nine months of 2014 vs. QR761.2mn for the corresponding period last year. The company’s Earnings per Share (EPS) amounted to QR2.49 for the period ended September 30, 2014 versus QR11.00 for the corresponding period in 2013. (QE)

GDI places new jack-up rig Dukhan into service for QP – Gulf Drilling International (GDI), a wholly-owned subsidiary of Gulf International Services (GISS), has announced that the new jack-up drilling rig “Dukhan” has been accepted by its client, Qatar Petroleum (QP), and left NKOM Shipyard at Ras Laffan in route to its first location. “Dukhan" is the ninth offshore jack-up rig in GDI’s fleet and the third jack-up rig to be under contract to QP, joining the jack-up rigs “Al Doha” and “Al Zubarah”. GDI took delivery of the rig from Keppel Fells Shipyard in Singapore last August and had it dry towed to Qatar September 2014. While undergoing final commissioning and testing in NKOM Shipyard, various third party equipment was installed and drill

pipe loaded onto the rig to achieve QP’s final acceptance. The rig has been customized to meet QP’s requirements and is capable of performing drilling operations anywhere in Qatar. It has 150 man accommodation, high volume centrifuges, high capacity for bulk mud treatment, and the capability of drilling wells up to 30,000 feet depth. (QE)

Ashghal awards QR1.1bn healthcare contracts – The Public Works Authority (Ashghal) has awarded different contracts worth QR1.1bn for a number of new projects in the country’s healthcare sector, including a 500-bed annex to Al Khor Hospital of the Hamad Medical Corporation. Ashghal authorities also announced the awarding of design & construction supervision work for five new health centers across the country. The new facilities include a QR208mn simulation center at Hamad Medical City, equipped with the latest audio-visual systems, which is expected to be completed by early 2016. The design contract for Al Khor Hospital annex has been awarded for QR222.6mn and the work has to be completed by 2Q2017. Other proposed projects include an annex at the emergency section of the Hamad General Hospital and design & construction supervision of the National Health Laboratory at Mesaimeer. Two new health centers will also be constructed in Al Waab and Al Jamiaa at a cost of QR253mn, which should be ready by 3Q2016. Another two health centers will be built in Muaither and Al Wajba at a cost of QR289.5mn and their work should be completed by 3Q2016. (Gulf-Times.com)

QTA: Qatari tourism sector surges ahead in 1H2014 – According to the Qatar Tourism Authority (QTA), visitor arrivals to Qatar grew by 8% YoY to reach 1.42mn and the average hotel occupancy rate increased by 7% YoY to 74% in 1H2014. According to QTA data, more than half a million GCC nationals (536,264) visited Qatar during this period, representing around 38% of tourists. The increase in the hotel occupancy rate was assisted by a 1.9% decline in available rooms due to renovation- related closures. The average room rate was estimated at QR721 for five-star hotels, QR389 for four-star hotels, QR277 for three-star hotels, QR273 for two-star hotels and QR212 for one-star hotels. The revenue per available room increased by 8.5% to QR544 among five-star hotels. QTA said that all key indicators of the tourism sector in Qatar demonstrated improvement, showing that the industry is continuing its strong performance. (Gulf-Times.com)

MDPS: PPI falls 7.5% YoY in August – According to the Ministry of Development Planning & Statistics (MDPS), the monthly Producer Price Index (PPI) of the industrial sector for August 2014 stood at 163.9, showing a decline of 2.0% MoM (-7.5% on a YoY basis). The index, which covers mining, electricity & water and manufacturing activities, is a measure of the average selling prices received by domestic producers for their inputs. The mining group’s PPI (77% weight) showed a decline of 1.8% MoM (-7.7% on a YoY basis), whereas the manufacturing group’s PPI (21% weight) fell 3.0% MoM (-7.1% on a YoY basis). The PPI of electricity and water (2% weight) declined 0.8% MoM (-3.0% on a YoY basis) (MDPS, Peninsula Qatar)

International

US Fed to enter new 'normal' with expected QE stimulus end – The US Federal Reserve is likely to make a final push into the post-crisis era this week with a decision to finally wind up its six-year-old economic stimulus operations. A few worrisome clouds looming over the global economy might give the Federal Open Market Committee a pause when they meet on October 28 and 29. According to analysts, after repeatedly signaling the end this month of the bond-buying program known as

4. Page 4 of 7

quantitative easing (QE), the Fed is unlikely to change course. The Fed is currently adding $15bn in cheap funds to the economy every month under QE, down from $85bn in December 2013. This injection of billions of dollars each month into the economy to repress longer term interest rates has had less and less real impact, while generating what some worry are fresh bubbles in stock markets. (ET)

ECB fails 25 banks in stress test but problems largely solved; investors welcome Europe's bank tests – The European Central Bank (ECB) said roughly one in five of the Eurozone's top lenders failed the landmark health checks at the end of 2014, but most have since repaired their finances. Painting a brighter picture than had been expected, the ECB found the biggest problems in Italy, Cyprus and Greece, but concluded that capital holes among banks had since been plugged, leaving only a modest €10bn to be raised. The test was designed to mark a clean start before the ECB takes on supervision of these banks next month. Italy faces the biggest challenge with nine of its banks falling short and two still needing to raise funds. The exercise provides the clearest picture yet of the health of the Eurozone's banks more than seven years after the eruption of a financial crisis that almost bankrupted a few countries and threatened to fracture the currency bloc. While 25 of the Eurozone's 130 biggest banks failed the health check at the end of 2013 with a total capital shortfall of €25bn, a dozen have already raised €15bn this year to make repairs. Meanwhile, investors gave a cautious thumbs-up to the ECB health check, describing it as a step in the right direction rather than the final word on the state of the bloc's financial system. The number of banks that failed the test and the size of their capital shortfall were in line with expectations after news leaked that 25 lenders would flunk the year-long review. With no major bank caught short and a relatively small capital hole to fill, markets were expected to take the results in their stride, although Italian bonds and bank shares could come under pressure. (Reuters)

Regional

GPCA: GCC petchem capacity set to grow to 170mn tones in five years – Gulf Petrochemicals & Chemicals Association’s (GPCA) board member Dr Abdulrahman al-Jawahery said that the petrochemical sector has grown into a 100mn ton business in 30 years with capacity expected to grow to 170mn tons in the next five years. He added that the Middle East holds an estimated 45% of the world’s oil & gas reserves, but only 10% of the global petrochemical capacity. According to the GPCA’s inaugural Sustainability Report, petrochemical producers in the Gulf region have made great strides in improving their sustainability performance. For example, GCC chemical producers have reduced energy consumption per tons by 8% in the last two years through technical renovations. (Gulf- Times.com)

IMF: Gulf States risk deficit as oil price falls – The International Monetary Fund’s (IMF) Managing Director, Christine Lagarde said oil-dependent Gulf States will face budget shortfalls if the recent decline in oil prices persists. A sustained decline of $25 a barrel in oil prices would reduce the revenues of most Gulf countries by 8% of gross domestic product (GDP), and put many of them into a fiscal deficit situation. But the six nations of the Gulf Cooperation Council (GCC) have built up fiscal buffers to cope with the immediate impact of the reduction in revenues. The combined GDP of the GCC last year reached $1.64tn, so in this scenario the annual revenue of the six nations could plunge by roughly $130bn. As per the IMF estimates, the total revenue of the GCC states, 90% of which come from oil more than doubled from $317bn in 2008

to $756bn in 2012. It declined slightly to $729bn in 2013. The GCC groups – Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UAE – together pump 17mn barrels of crude oil per day and depend on oil for around 90% public revenues. (GulfBase.com)

NCB IPO 18% subscribed at end of fifth day – According to the financial advisers and lead managers GIB Capital and HSBC Saudi Arabia, National Commercial Bank’s (NCB) IPO was 18% covered by the end of the fifth day. About 432,000 investors bought shares at a total value of SR2.29bn. The subscription of the shares allotted to investors began on October 19, 2014. The offering is scheduled to run for 15 days until the end of November 2, 2014. Saudi retail investors started subscribing 300mn shares, representing 15% of the bank’s capital. The total number of shares offered is 500mn, representing 25% of the capital. (GulfBase.com)

Mobily Ventures invests in hellofood – Mobily Ventures, the corporate venture capital fund of Etihad Etisalat Company (Mobily), has invested in hellofood Middle East, the leading food ordering marketplace in the region. The investment will allow hellofood to expand in Saudi Arabia and other markets in the region. The company is currently active in Saudi Arabia, Jordan, Lebanon and Qatar. (GulfBase.com)

Amiantit Group acquires remaining 20% stake in PWT and remaining 25% in Ductile – International Infrastructure Development Management & Operation Company Ltd., a wholly-owned subsidiary of Saudi Arabian Amiantit Company (Amiantit Group), has acquired remaining 20% shares of PWT Wasser-und Abwassertechnik (PWT) with registered seat in Zwingenberg (Germany), taking its total investment in this company from 80% to 100 % of the shares. The shares were purchased from the previous minority shareholders for a total value of approximately SR6.2mn equivalent, while the corresponding book value of such shares amounts to SR11.6mn. The difference of SR5.4mn will be booked as a long term provision on certain ongoing projects. Under the same transaction, Amiantit Group acquired 25% of Ductile Technology Company (Ductech), with registered seat in Manama (Bahrain), for an amount of SR0.2mn, corresponding to the book value of the acquired shares. This deal will bring the total investment of the Group in this company from 75% to 100 % of the shares. PWT is engaged in EPC contracts for water and sewage treatment plants mostly in Germany, Turkey, Azerbaijan, Turkmenistan and Iraq, while Ductech is the company owing the premises of PWT in Germany. Both the transactions will not have a financial impact on Amiantit’s results for the year 2014. (Tadawul)

NMCC announces progress regarding use of proceeds – National Medical Care Company (NMCC) has announced the actual used for proceeds from its IPO shares subscription until the end of the period as compared with what was declared in IPO prospectus: the actual used amount was SR120.9mn (69%) from the net of proceeds which has been calculated at SR174.6mn after deduction of the company’s part of the IPO- related expenses at SR7.6m. (Tadawul)

UNB joins DMCC Tradeflow platform – Union National Bank (UNB) has joined the DMCC Tradeflow platform, in order to conduct Commodity Murabaha transactions for corporate customers dealing according to Shari’ah guidelines. This electronic platform enables UNB to create operational efficiencies and help improve execution of its transactions. (GulfBase.com)

MAF to invest $683mn in Egypt mall – Majid Al Futtaim (MAF) is set to invest $683mn in the construction of a mall in Egypt. The two-level mall will span a gross leasable area (GLA) of

5. Page 5 of 7

165,000 square meters and will include over 420 stores presenting offerings from a variety of international and local brands. (GulfBase.com)

UAE Central Bank signs MoU with National Bank of Kazakhstan – The Central Bank of the UAE has signed a MoU with the National Bank of Kazakhstan on cooperation and exchange of regulatory information. Under the terms of the MoU, both the entities will cooperate on regulatory matters, supervision of banks and other financial institutions operating in both jurisdictions. (GulfBase.com)

Dewa awards AED108mn water transmission network contract – Dubai Electricity & Water Authority (Dewa) has awarded an AED108mn contract to supply, extend, and launch a 16 kilometer main water distribution network between Jebel Ali and Al Quoz. The project includes extending the 1,200mm Glass Reinforced Epoxy (GRE) water transmission pipeline by a further 16km: from Jebel Ali, through Al Khail Road, to the main pumping station in Al Quoz. The project also includes a remote control and monitoring system to enhance transmission capacity between Jebel Ali and the main pumping stations in Al Quoz. (GulfBase.com)

CBI reports AED171mn net profit in 9M2014 – Commercial Bank International (CBI) reported a net profit of AED171mn for 9M2014, representing an increase of 25% from AED136mn in 9M2013, wherein the CBI’s net operating profit recorded AED353mn, an increase of 55.5% from AED227mn for the same period in 2013. The bank achieved profitability partially due to a growth in assets, which stood at AED18.6bn at the end of September 2014, an increase of 25% as compared to AED14.8bn at the end of December 2013. Loans & advances increased by 21% to AED12.8bn as of September 30, 2014, as compared to AED10.6bn at the end of December2013, while customer deposits increased by 24% to reach AED13bn at the end September 2014 as against AED10.5bn in December 2013. Shareholders' equity increased by 9% to AED2.4bn as compared to AED2.2bn at the end of December 2013. EPS increased by 29% to AED0.103 at the end of September 2014. Net fee and commission income have increased by 10% to AED148mn, driven by an increase in LCs and acceptances. (ADX, Zawya)

Aldar leases Gate and Arc Towers in Shams Abu Dhabi – Aldar Properties announced that The Gate and Arc Towers on Al Reem Island are fully leased after being on the market for just under a year, highlighting the increasing demand for quality residential property in the capital. The Gate and Arc Towers development located in the landmark district of Shams Abu Dhabi are made up of 3,533 units, of which Aldar retained over 1,300 units as part of their recurring-income portfolio. The Arc comprises studios, one and two bedroom apartments with its unique arc-like design. (ADX)

Abu Dhabi to tap sour gas with $10b Shah gas project – Abu Dhabi Gas Development Company Limited (Al Hosn Gas), which is developing the Shah gas field said it will have a capacity to supply half a billion standard cubic feet per day of network gas when fully developed. The gas field located about 210 kilometers south-west of Abu Dhabi is targeted for full production in late 2014 and will contribute significantly to the energy needs of Abu Dhabi and the UAE for over a period of 30 years. (GulfBase.com)

Abu Dhabi ports prepare for 25% more cruise liners – Abu Dhabi Ports Company (ADPC) is expecting to receive around 25% more cruise ships and 16% additional passengers to visit the capital this season as compared with 2013, following the issuance of multiple entry visas to the UAE. In 2014 ADPC

expects 93 ships to call at Zayed Port, up from 75 last season and around 220,000 passengers from 189,709 in 2013. For Dubai, cruise tourist numbers reached at least 300,000 in the previous season. ADPC expects a steady increase in cruise tourists over the next few years. The company expects 130 ships and 300,000 passengers to call on Abu Dhabi in the 2019- 2020 seasons. (GulfBase.com)

Warba Bank increases revenue by 71.6% for 9M2014 – Warba Bank reported a growth of 71.6% in 9M2014 to reach KD13.21mn in its operating revenues, as compared to KD7.70mn in 9M2013. The bank posted a net profit of KD0.32mn for the nine months ending September 30, 2014 reflecting an increase of 110% as compared to the same period of 2013. The bank’s total assets grew at 31% to reach KD507.1mn as of September 30, 2014 as compared to KD386.7mn a year ago. This growth was achieved while maintaining a high level asset quality. Warba’s financing portfolio grew by 90% to reach KD346.75mn in 3Q2014, as compared to KD182.45mn in 3Q2013. The capital adequacy ratio at the end of 3Q2014 reached a high rate far exceeding the designated ratio stipulated by Basel III requirements and the Central Bank of Kuwait instructions. This reflects the bank's robust and solid financial position that supports its future business growth. (GulfBase.com)

JA mulls big stake acquisition in KA – Jazeera Airways’ (JA) Chairman, Marwan Boodai said that JA is preparing to bid for a big stake in Kuwait Airways (KA). If the deal goes through, it will be a sign that the business scene is changing in the Gulf. (Reuters )

CBK reports KD25.3mn net profit in 9M2014 – Commercial Bank of Kuwait (CBK) reported an operating profit of KD73.5mn, before provisions for the nine months ended September 30, 2014 (KD 72.8 million in same period of 2013). KD47mn of these profits was allocated as specific and judgmental provisions against the loan and investment portfolios, leading to a net profit of KD25.3mn in 9M2014, which was KD17.6mn (228%) higher than that in the same period last year (KD7.7mn). The earnings per share reached 18.0 fils as against 5.5 fils for the corresponding period of the previous year. CBK’s total assets reached KD3.9bn, with shareholders’ equity of KD578.4mn. The minimum capital adequacy ratio mandated by CBK (Under Basel II 12%) was exceeded with a ratio of 18.16% at the end of September 2014. This is also more than twice the minimum ratio required by the Basel Committee (Basel II). (Kuna)

NBO: Islamic finance grows faster than conventional banking – National Bank of Oman (NBO)’s Chairman, Mohammed Mahfoodh Al Ardhi said Islamic finance is growing at twice the rate of the traditional banking industry in its core markets, which include Malaysia, Indonesia, Turkey and the GCC countries. The industry currently boasts of $1.6tn in banking system assets. He added that GCC countries have committed to actively strengthen their positions in the Islamic finance market, with Saudi Arabia currently in the lead. He stated that NBO has been doing significant work in the Islamic finance domain and achieved considerable success as part of the broader plans to diversify Oman’s economy. Bahrain and Dubai are also emerging as notable offshore centers. (GulfBase.com)

CBO issues tenders worth OMR240mn – Certificates of deposit (CoD) tender was held at the Central Bank of Oman (CBO) this week and the total amount allotted for issue No. 888 was OMR240mn. According to the CBO, the average interest rate of these certificates was 0.13% while the maximum

6. Page 6 of 7

accepted interest rate was 0.13%. The tenure of these certificates is 28 days, so their maturity date is November 19, 2014. The CoD issued to licensed banks by the CBO as a monetary policy instrument is aimed at absorbing excess liquidity in the banking sector in particular and maintaining stability of the interest rate and the money market in general. The repo rate from October 22, 2014 to October 28, 2014 is 1%. (GulfBase.com)

Oman may start cutting costly subsidies next year – Oman’s Minister for Financial Affairs Darwish al-Balushi, said the government is likely to start cutting some state subsidies next year as the decline in global oil prices pressures its finances. The country’s original budget plan for 2014 assumed the government would run a deficit with an average oil price of $85 a barrel. For most of this year oil prices have been much higher, but in the last few months it had dropped steeply to as low as $82. (GulfBase.com)

Commercial banks in Oman report robust growth – Oman- based commercial banks’ financial health in terms of asset quality, provision coverage, capital adequacy and profitability continued to improve in recent years. The balance sheet of commercial banks further strengthened in 2014 due to the robust growth in both deposits and credit. On the macroeconomic front, Oman’s GDP at current prices grew 4.6% in 1Q2014 when compared to 1Q2013. The annual inflation rate measured by movement in the average Consumer Price Index (CPI) for Oman stood at 1% from January to July 2014. The total assets of commercial banks increased 11% to OMR24.3bn in August 2014 from OMR21.9bn a year ago. Of the total assets, credit disbursement accounted for 67% and increased 7.9% at the end of August 2014 to OMR16.3bn. The overall investment of commercial banks in securities rose by 38.3% to OMR3.42bn at the end of August 2014 from OMR2.48bn a year ago. Of the total investment, CBO CDs stood at OMR1.8bn while investment in government development bonds (GDBs) stood at OMR566.2mn at the end of August 2014. Investments of commercial banks in foreign securities increased 15.6% to OMR688.1mn in August 2014. (GulfBase.com)

7. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg (# Data as of 23 October 2014)

Source: Bloomberg Source: Bloomberg, *$ adjusted returns.

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Sep-10 Sep-11 Sep-12 Sep-13 Sep-14

QE Index S&P Pan Arab S&P GCC

1.5%

0.6%

(0.4%)

0.1%

(0.3%)

0.8%

2.5%

(0.8%)

0.0%

0.8%

1.6%

2.4%

3.2%

Saudi Arabia

Qatar

Kuwait

Bahrain #

Oman #

Abu Dhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD%

Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,230.90 (0.1) (0.6) 2.1 DJ Industrial 16,805.41 0.8 2.6 1.4

Silver/Ounce 17.20 0.0 (0.4) (11.6) S&P 500 1,964.58 0.7 4.1 6.3

Crude Oil (Brent)/Barrel (FM

Future)

86.13 (0.8) (0.0) (22.3) NASDAQ 100 4,483.72 0.7 5.3 7.4

Natural Gas (Henry

Hub)/MMBtu

3.53 (1.8) (5.0) (18.7) STOXX 600 327.17 (0.2) 1.8 (8.5)

LPG Propane (Arab Gulf)/Ton 85.63 (0.1) (5.9) (32.3) DAX 8,987.80 (0.5) 0.7 (13.7)

LPG Butane (Arab Gulf)/Ton 106.75 0.0 (1.5) (21.4) FTSE 100 6,388.73 (0.2) 1.1 (8.2)

Euro 1.27 0.2 (0.7) (7.8) CAC 40 4,128.90 (0.55) 1.5 (11.8)

Yen 108.16 (0.1) 1.2 2.7 Nikkei 15,291.64 1.1 3.9 (8.7)

GBP 1.61 0.4 (0.0) (2.8) MSCI EM 984.38 0.3 0.8 (1.8)

CHF 1.05 0.2 (0.6) (6.2) SHANGHAI SE Composite 2,302.28 0.0 (1.6) 7.7

AUD 0.88 0.4 0.6 (1.4) HANG SENG 23,302.20 (0.1) 1.2 (0.1)

USD Index 85.73 (0.1) 0.7 7.1 BSE SENSEX 26,851.05 0.0 2.9 28.2

RUB 41.81 0.2 2.9 27.2 Bovespa 51,940.73 4.0 (7.9) (3.7)

BRL 0.41 1.8 (1.1) (4.2) RTS 1,036.68 0.1 (3.4) (28.1)

194.6

158.4

142.4