Log your LOA pain with Pension Lab's brilliant campaign

6 May Daily market report

1. Page 1 of 6

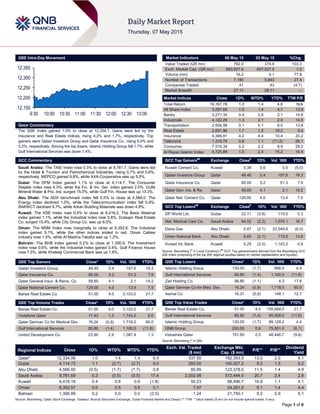

QSE Intra-Day Movement

Qatar Commentary

The QSE Index gained 1.0% to close at 12,334.1. Gains were led by the

Insurance and Real Estate indices, rising 4.2% and 1.7%, respectively. Top

gainers were Qatari Investors Group and Qatar Insurance Co., rising 5.4% and

5.2%, respectively. Among the top losers, Islamic Holding Group fell 1.7%, while

Gulf International Services was down 1.4%.

GCC Commentary

Saudi Arabia: The TASI Index rose 0.3% to close at 9,781.7. Gains were led

by the Hotel & Tourism and Petrochemical Industries, rising 0.7% and 0.6%,

respectively. MEPCO gained 9.8%, while AXA-Cooperative was up 5.5%.

Dubai: The DFM Index gained 1.1% to close at 4,114.7. The Consumer

Staples index rose 4.3%, while the Fin. & Inv. Ser. index gained 2.4%. Gulfa

Mineral Water & Pro. Ind. surged 15.0%, while Gulf Fin. House was up 13.3%.

Abu Dhabi: The ADX benchmark index fell 0.5% to close at 4,566.0. The

Energy index declined 1.0%, while the Telecommunication index fell 0.9%.

RAKWCT declined 9.7%, while Arkan Building Materials was down 4.8%.

Kuwait: The KSE Index rose 0.4% to close at 6,416.2. The Basic Material

index gained 1.1%, while the Industrial index rose 0.8%. Dulaqan Real Estate

Co. surged 15.4%, while City Group Co. was up 8.0%.

Oman: The MSM Index rose marginally to close at 6,352.6. The Industrial

index gained 0.1%, while the other indices ended in red. Oman Cables

Industry rose 1.5%, while Al Madina Takaful was up 1.2%.

Bahrain: The BHB Index gained 0.2% to close at 1,390.9. The Investment

index rose 0.6%, while the Industrial index gained 0.4%. Gulf Finance House

rose 7.5%, while Khaleeji Commercial Bank was up 1.8%.

QSE Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatari Investors Group 49.40 5.4 197.6 19.3

Qatar Insurance Co. 85.00 5.2 51.3 7.9

Qatar General Insur. & Reins. Co. 58.60 4.1 2.1 14.2

Qatar National Cement Co. 129.00 4.0 13.4 7.5

Barwa Real Estate Co. 51.00 4.0 3,103.0 21.7

QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD%

Barwa Real Estate Co. 51.00 4.0 3,103.0 21.7

Vodafone Qatar 17.43 1.3 1,743.3 6.0

Qatar German Co for Medical Dev. 16.24 (0.9) 1,718.0 60.0

Gulf International Services 85.80 (1.4) 1,100.5 (11.6)

United Development Co. 23.90 2.9 1,087.4 1.3

Market Indicators 06 May 15 05 May 15 %Chg.

Value Traded (QR mn) 762.0 374.9 103.3

Exch. Market Cap. (QR mn) 663,827.9 657,527.5 1.0

Volume (mn) 16.2 9.1 77.8

Number of Transactions 7,190 5,643 27.4

Companies Traded 41 43 (4.7)

Market Breadth 27:11 28:11 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,167.78 1.0 1.4 4.6 N/A

All Share Index 3,297.69 1.0 1.4 4.7 13.9

Banks 3,271.34 0.4 0.9 2.1 14.8

Industrials 4,122.29 1.3 2.1 2.0 14.5

Transportation 2,504.98 0.1 0.1 8.0 13.8

Real Estate 2,651.96 1.7 1.2 18.2 9.4

Insurance 4,369.81 4.2 4.4 10.4 20.2

Telecoms 1,319.78 0.6 1.1 (11.2) 26.1

Consumer 7,519.34 0.2 2.2 8.9 29.2

Al Rayan Islamic Index 4,725.89 1.5 2.4 15.2 14.4

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Kuwait Cement Co. Kuwait 0.38 5.6 0.5 (5.0)

Qatari Investors Group Qatar 49.40 5.4 197.6 19.3

Qatar Insurance Co. Qatar 85.00 5.2 51.3 7.9

Qatar Gen. Ins. & Re. Qatar 58.60 4.1 2.1 14.2

Qatar Nat. Cement Co. Qatar 129.00 4.0 13.4 7.5

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

DP World Ltd. Dubai 22.11 (3.9) 119.5 5.3

Nat. Medical Care Co. Saudi Arabia 64.02 (2.2) 1,070.1 16.7

Dana Gas Abu Dhabi 0.47 (2.1) 22,549.9 (6.0)

Union National Bank Abu Dhabi 6.60 (2.1) 719.5 13.8

Kuwait Int. Bank Kuwait 0.25 (2.0) 1,143.2 0.8

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

QSE Top Losers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 130.00 (1.7) 666.4 4.4

Gulf International Services 85.80 (1.4) 1,100.5 (11.6)

Zad Holding Co. 98.80 (1.1) 4.3 17.6

Qatar German Co for Med. Dev. 16.24 (0.9) 1,718.0 60.0

Aamal Co. 16.31 (0.8) 148.1 12.7

QSE Top Value Trades Close* 1D% Val. ‘000 YTD%

Barwa Real Estate Co. 51.00 4.0 155,668.0 21.7

Gulf International Services 85.80 (1.4) 95,508.0 (11.6)

Islamic Holding Group 130.00 (1.7) 89,129.2 4.4

QNB Group 200.00 0.6 75,851.0 (6.1)

Industries Qatar 151.90 2.0 48,446.7 (9.6)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,334.06 1.0 1.4 1.4 0.4 337.50 182,353.5 13.0 2.0 4.1

Dubai 4,114.73 1.1 (2.7) (2.7) 9.0 283.50 100,027.2 9.2 1.5 5.2

Abu Dhabi 4,566.00 (0.5) (1.7) (1.7) 0.8 85.95 123,378.0 11.5 1.4 4.9

Saudi Arabia 9,781.69 0.3 (0.5) (0.5) 17.4 2,002.06 572,444.0 20.7 2.4 2.8

Kuwait 6,416.18 0.4 0.6 0.6 (1.8) 50.23 98,496.7 16.8 1.1 4.1

Oman 6,352.57 0.0 0.5 0.5 0.1 7.07 24,261.0 9.1 1.4 4.4

Bahrain 1,390.89 0.2 0.0 0.0 (2.5) 1.24 21,750.1 9.2 0.9 5.1

Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,150

12,200

12,250

12,300

12,350

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QSE Index gained 1.0% to close at 12,334.1. The Insurance

and Real Estate indices led the gains. The index rose on the

back of buying support from non-Qatari shareholders despite

selling pressure from Qatari and GCC shareholders.

Qatari Investors Group and Qatar Insurance Co. were the top

gainers, rising 5.4% and 5.2%, respectively. Among the top

losers, Islamic Holding Group fell 1.7%, while Gulf International

Services was down 1.4%.

Volume of shares traded on Wednesday rose by 77.8% to

16.2mn from 9.1mn on Tuesday. Further, as compared to the 30-

day moving average of 9.0mn, volume for the day was 80.5%

higher. Barwa Real Estate Co. and Vodafone Qatar were the

most active stocks, contributing 19.2% and 10.8% to the total

volume respectively.

Source: Qatar Stock Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn) 1Q2015

% Change

YoY

Operating Profit

(mn) 1Q2015

% Change

YoY

Net Profit (mn)

1Q2015

% Change

YoY

International Financial

Advisors (IFA)*

Dubai KD 17.1 -66.6% – – -34.1 NA

Source: Company data, DFM, ADX, MSM (FY2014 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

05/06 US MBA MBA Mortgage Applications 1-May -4.60% – -2.30%

05/06 US ADP ADP Employment Change April 169K 200K 175K

05/06 EU Eurostat Retail Sales MoM March -0.80% -0.70% 0.10%

05/06 EU Eurostat Retail Sales YoY March 1.60% 2.40% 2.80%

05/06 UK Markit Markit/CIPS UK Services PMI April 59.5 58.5 58.9

05/06 UK Markit Markit/CIPS UK Composite PMI April 58.4 58.1 58.7

05/06 Spain Markit Markit Spain Services PMI April 60.3 57.4 57.3

05/06 Spain Markit Markit Spain Composite PMI April 59.1 – 56.9

05/06 Italy Markit Markit/ADACI Italy Services PMI April 53.1 52.0 51.6

05/06 Italy Markit Markit/ADACI Italy Composite PMI April 53.9 52.7 52.4

05/06 China Markit HSBC China Composite PMI April 51.3 – 51.8

05/06 China Markit HSBC China Services PMI April 52.9 – 52.3

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QP invites firms to bid for Al-Shaheen field – Qatar

Petroleum (QP) has initiated an evaluation process for the

selection of a partner to undertake the future development of the

Maersk Oil-operated Al Shaheen field, as the current agreement

expires in mid-2017. Maersk Oil has been operator of the Al

Shaheen field since 1992 and together with QP has been

successfully unlocking the potential of the field for more than 20

years producing around 300,000 barrels per day, some 40% of

Qatar’s daily oil production. Al Shaheen is located off the

northeast coast of Qatar in the Persian Gulf, 180 kilometers

north of Doha. (Gulf-Times.com, Bloomberg)

Al Rayan Bank’s operating income jumps 168% in 2014 – Al

Rayan Bank, formerly known as Islamic Bank of Britain (IBB),

announced its strongest financial performance to date, resulting

in the Bank more than doubling its operating income and posting

its first profit since its inception in 2004. The bank’s operating

income increased 168% to £11.8mn in 2014 from £4.4mn in

2013. The bank saw 86% increase in total customer financing,

to £450.3mn. Retail deposits increased 59% to £509.8mn and

wholesale deposits increased 53% to £31.7mn. Al Rayan Bank’s

achievements follow its acquisition by Masraf Al Rayan (MARK)

in early 2014. This was accompanied by a £75mn additional

investment by MARK and the implementation of a number of

strategic initiatives in order to help the Bank achieve sustained

profitability. (Peninsula Qatar)

MERS, LREDC sign MoU – Al Meera Consumer Goods

Company (MERS) has signed a MoU with Lusail Real Estate

Development Company (LREDC) to operate two community

retail locations/plots as community facilities to serve the local

community by offering a supermarket and supporting stores to

service the day-to-day needs of the residents. (QSE)

QSE inclusion in MSCI, S&P gets $1.25bn inflow – The CEO

of Qatar Stock Exchange (QSE), Rashid bin Ali Al Mansoori said

inclusion of the QSE in the coveted MSCI and S&P Emerging

Market indices in 2014 has led to an inflow of an impressive

$1.25bn into the market and a near-trebling of average daily

turnover. The QSE, in collaboration with QNB Financial Services

and HSBC, opened a two-day road-show in London to enhance

investor relations between international investment institutions

and Qatari listed companies. Al Mansoori also said that in

addition to ongoing work on the infrastructure side, Qatar has

Overall Activity Buy %* Sell %* Net (QR)

Qatari 60.61% 66.42% (44,274,099.71)

GCC 6.43% 6.74% (2,309,752.69)

Non-Qatari 32.96% 26.84% 46,583,852.40

3. Page 3 of 6

taken concrete steps to improve access to foreign investors

pursuant to the Emiri Decree in 2015, raising the foreign

ownership limit in Qatari stocks. (Peninsula Qatar)

Al Attiyah: Qatar 'well positioned' to meet rising energy

demand in Asia – HE the former Deputy Premier, Abdullah bin

Hamad Al Attiyah said with long-term energy demand in Asia set

to rise, Qatar is “well positioned” to supply existing and new

customers in the region, going forward. Al Attiyah said that

Qatar will continue to employ a flexible marketing position for its

customers, but as a supplier it will also keep in mind its limited

gas reserves and the sales price will be set accordingly. Al

Attiyah further added that Qatar is committed to its National

Vision 2030, which aims to create a balance between an oil-

based and a knowledge-based economy, and therefore seeks to

build a sustainable economy for future generations. Qatar’s

energy sector will play a critical role in supporting the National

Vision by ensuring responsible and sustainable exploitation of

the country’s hydrocarbon resources, and diversifying into other

forms of energy such as renewables. (Gulf-Times.com)

QA forms JV with Royal Air Maroc, eyes stake in India's

IndiGo – Qatar Airways (QA) has entered into a joint venture

(JV) with Morocco’s flagship airline, Royal Air Maroc. QA CEO

Akbar Al Baker said that this will be a joint business partnership

and will provide QA a huge access into Africa, especially into

western and central Africa. Royal Air Maroc will begin operating

three flights a week between Casablanca and Doha under the

deal. Together, the two carriers will fly 10 times weekly on the

route. Meanwhile, Akbar Al Baker said that QA would be

interested in buying up to 49% stake in India's IndiGo though the

owners of the sub-continent's largest carrier by market share

have no immediate plans to sell. (GulfBase.com, Bloomberg)

26-year-old ministerial decree amended – A 26-year-old

ministerial decree on technical specifications related to

electricity conservation in Qatar's buildings has been amended,

as a result of the joint efforts of the Qatar General Electricity &

Water Corporation (Kahramaa) and Ministry of the Municipality

and Urban Planning. According to Kahramaa, the new

ministerial decree No.108/2015 has now replaced the provisions

of the Ministerial decree No 6/1989 and made good thermal

insulation mandatory. Kahramaa termed the decree amendment

as a vital step toward achieving a comprehensive economic and

environmental development in the country in line with the goals

of the Qatar National Vision 2030. (Gulf-Times.com)

International

US private payrolls growth eases; productivity falls – Private

employers in the US have hired the fewest number of workers in

more than a year in April, which could raise concerns over the

economy's potential to strongly rebound from the 1Q2015

slump. According to the ADP National Employment Report,

private payrolls increased by 169,000 in April, which was the

lowest since January 2014; and far below the economists'

expectations for a gain of 200,000 jobs. March payrolls were

revised down to show 14,000 fewer jobs created than previously

reported. Meanwhile, the report was jointly developed with

Moody's Analytics, and was released ahead of the government's

more comprehensive employment report on Friday. Although it

has a poor track record of predicting non-farm payrolls, the ADP

report poses a downside risk to economists' expectations for

non-farm payrolls growth of 224,000 in April. Further, yields on

the US Treasuries have risen and the US stock index futures

traded slightly higher after the data. The dollar was weaker

against a basket of currencies. A combination of cold weather, a

strong dollar, port disruptions and deep spending cuts by energy

companies have held down 1Q2015 economic growth to a 0.2%

annual pace. (Reuters)

Markit: Eurozone business contributes toward healthy

growth in 2Q2015 – According to a survey, Eurozone

businesses have contributed to a healthy growth in 2Q2015

since a buoyant order book again has encouraged them to hire

more. Any sign that the bloc's recovery is gaining traction will be

welcomed by the European Central Bank, which had embarked

on a trillion-euro bond buying stimulus program in March,

although the survey has indicated that firms were still cutting

prices. Markit's final composite Purchasing Managers' Index that

is seen as a good guide to growth was 53.9 in April, which is

ahead of an earlier flash reading of 53.5 but just behind March's

11-month high of 54.0. Meanwhile, the recent data showed that

Eurozone retail sales were weaker than expected in March,

turning negative on a monthly basis for the first time since last

September. The European Union's statistics office Eurostat said

retail sales in the Eurozone fell 0.8% MoM for a 1.6% YoY rise.

Reuters had expected only a 0.7% monthly fall and a 2.4%

annual increase. Further, a decline in the sales was observed

despite a sharp improvement of sentiment both among

consumers and in the retail sector in March, as measured by the

European Commission's monthly economic sentiment survey.

(Reuters)

Greece unemployment rate eases to 25.4% in February –

According to the statistics agency ELSTAT, the rate of

unemployment in Greece dropped slightly to 25.4% in February

from a downwardly revised 25.6% rate in April. February's

reading, which is based on seasonally adjusted data, is the

lowest since July 2012 when the rate of unemployment was

25.3%. The rate of unemployment hit a record high of 27.9% in

September 2013. Unemployment has come down from record

high rates as the economy stabilized in 2014 after a severe

slump, but has remained more than double the Eurozone's

average of 11.3% in February. According to the latest EU

Commission forecasts, Greece's economy, which grew at 0.7%

in 2014, is expected to expand by just 0.5% in 2015. (Reuters)

China HSBC services’ PMI hits 2015 high in April –

According to a private survey, China's services sector has

expanded at its fastest pace in April due to a sizzling stock

market rally that helped boost consumer confidence and

spending. The HSBC/Markit China Services Purchasing

Managers' Index (PMI) has indicated that final prices of services

hit a 15-month low in April as some firms were forced to cut

prices to lift sales. However, the services PMI rose to a four-

month high of 52.9 in April from 52.3 in March, comfortably

above the 50-point level on a monthly basis. Meanwhile, some

companies stated that part of the pick-up in new business is

attributable to the strong stock market, which hit a seven-year

peak in April, suggesting that the wealth effect had seeped into

parts of the world's second-biggest economy. However, other

firms reported greater stress. Final prices charged slipped to

49.2 in April, a low not seen since January 2014 and pointing to

further pressure on profit margins. Companies also pared their

business expectations, though the subindex remained a good

way above the 50-point level. Meanwhile, the International

Monetary Fund said China should allow greater flexibility in its

exchange rate policy by reducing intervention, as part of its

efforts to secure a gradual moderation in growth while pursuing

economic reforms. (Reuters)

PMI: Indian services growth loses more steam in April –

According to a business survey, growth in India's dominant

services industry continued to lose momentum in April as

domestic demand softened. Coupled with a slowing

manufacturing sector and falling inflation, the findings are likely

4. Page 4 of 6

to strengthen expectations that the Reserve Bank of India will

cut interest rates for the third time in 2015, possibly before its

next scheduled policy review on June 2. The HSBC Services

Purchasing Managers' Index (PMI), compiled by Markit, fell to a

three-month low of 52.4 in April from 53.0 in March, but

remained well at the 50 level and has been above that level for a

year. The index monitoring new business fell to a six-month low

of 51.6 from March's 53.5, prompting some firms to cut jobs.

Some respondents also reported tougher competition. Further, a

slowdown in the services & manufacturing industries could

further amplify calls for much-needed economic reforms in India.

India's GDP is expected to have grown 7.4% in 1Q2015, down

from 7.5% in 4Q2014. (Reuters)

Regional

Al Alamiya seeks shareholders’ nod for not distributing

dividend – Al Alamiya For Cooperative Insurance Company (Al

Alamiya) has invited its shareholders to consider and approve

the recommendation not to distribute dividend payout for the

year ended December 31, 2014. Shareholders will also consider

approval of the transactions with related parties and insurance

contracts. (Tadawul)

KACST: KSA plans to increase petrochemicals production –

King Abdulaziz City for Science & Technology’s (KACST)

President Prince Turki bin Saud bin Mohammed Al-Saud, said

that Saudi Arabia is planning to increase its petrochemicals

production capacity to around 100mn tons per year. He said

such an increase would make the Kingdom contribute 10% of

the world production, thus becoming the third largest global

exporter of petrochemicals. (GulfBase.com)

IMF: Boosting productivity next big challenge for Gulf

states – According to the International Monetary Fund’s (IMF)

Chief Economist for the Middle East, Masood Ahmed, boosting

productivity is the next big challenge for Gulf States accustomed

to swapping oil wealth for industrial development. A lot of the

growth of Gulf countries has come from increasing the total

amount of capital and labor that is, by hiring more expats and

building new skyscrapers rather than increasing productivity.

The GCC states need to start looking at the effectiveness of

money spent on education, and to think about ways to get more

output from it. (GulfBase.com)

JMC announces dividend for 1Q2015 – Jarir Marketing

Company (JMC) has announced that Arab National Bank (ANB)

will distribute the dividend for 1Q2015 (SR 2.25 per share) to all

eligible shareholders registered in Jarir’s share registry by the

end of April 28, 2015 (record date). The dividend payment

process will start on May 7, 2015 (payment date). The due

dividends will be deposited in the current accounts of all eligible

shareholders. (Tadawul)

HSBC: Saudi mid-market firms generate $232bn turnover –

According to a report released by HSBC Group, Saudi Arabia’s

mid-market enterprises (MMEs), defined as firms with annual

sales between $50mn and $500mn, generated $232bn turnover.

The study is part of a 15-country research sponsored by HSBC

Group and developed with Oxford Economics, and is considered

the first of its kind in terms of its focus on MMEs. With a 10.3%

share in Saudi Arabia GDP, MMEs provide 930,000 jobs

representing 13.9% of the national number of jobs. Nearly

28.7% of MMEs are in the Saudi manufacturing sector, followed

by the wholesale and retail sectors which accounted for 19.9%

of all MMEs. With an estimated $66bn in turnover, the

manufacturing sector enjoyed the largest share of MME turnover

in Saudi Arabia. (GulfBase.com)

SEC eyes investment options – Saudi Electricity Company

(SEC) is looking for investment opportunities to offset the

financial pressures on its core electricity business. SEC CEO

Ziyad Al-Shiha said that the company is in desperate need of

financial resources, and would like to diversify its portfolio

through investment opportunities, to make a good rate of return

that can make it stronger. (GulfBase.com)

Shurooq unveils AED80mn Al Noor Island in Sharjah – The

Sharjah Investment & Development Authority (Shurooq) has

launched the AED80mn tourism project on Al Noor Island in

Sharjah’s Khalid Lagoon. The project is in line with the emirate’s

aggressive plans of developing its tourism sector. The move is

part of Shurooq’s commitment to develop the emirate, raise its

economic and social merits as well as reinforce its position as a

leading cultural, tourism and investment destination in the region

that serves the ambition of its residents and visitors and meets

their interests. (Maktoob)

FCA: UAE’s non-oil trade reaches AED1.07tn – The Federal

Customs Authority’s (FCA) preliminary statistical data revealed

an increase in the total non-oil direct trade of the UAE to

AED1.07tn during 2014, reflecting an increase of 1% YoY. As

per the FCA data, the share of imports of the UAE’s total direct

non-oil trade amounted to AED696.4bn during 2014, showing an

increase of 2% YoY. The value of exports amounted to about

AED132.2bn, and the value of re-exports stood at AED243.7bn

with a growth rate of 5% YoY. The FCA declared that the UAE

direct non-oil trade is witnessing an increasing growth in recent

years, given the solid economic growth achieved by the country.

(GulfBase.com)

MoF signs MoU with Rakia – The Ministry of Finance (MoF)

has signed a MoU with the Ras Al Khaimah Investment

Authority (Rakia) to ensure the implementation of international

standards of transparency in the exchange of information for tax

purposes, as per the Organisation for Economic Cooperation

and Development (OECD) regulations and principles.

(GulfBase.com)

JLL & BCG: Dubai among top-5 most improved cities –

Dubai has made it to the list of top-five most improved cities

since 2010, which has been compiled by global property expert

Jones Lang LaSalle (JLL) in partnership with The Business of

Cities Group (BCG). According to a study conducted by property

expert Jones Lang LaSalle (JLL) in partnership with the

Business of Cities Group (BCG), Dubai was among the top-5

most improved cities worldwide since 2010. In terms of the most

improved cities, the UAE emirate showed marked progress

climbing up the global ranking in respect of two diverse

indicators, financial services and innovation. (GulfBase.com)

Arabtec appoints new Chairman – Arabtec said that its board

has elected Abu Dhabi businessman Mohamed Thani Murshed

Ghannam al-Rumaithi as new Chairman. Rumaithi, who is also

Chairman of the Abu Dhabi Chamber of Commerce and

Industry, replaces Khadem Abdulla al-Qubaisi, who was not

nominated for renewed board membership in April 2015. (Gulf-

Base.com, Bloomberg)

DI plans to increase market share in Qatar – Dubai

Investments (DI) is planning to increase its market share in the

Qatari market for its innovative and diversified product portfolio

in the building materials sector to cater to the current

construction boom in the country. In order to reinforce its

commitment, DI is making a mark with strong presence in

Project Qatar 2015, and its participation is part of the strategy to

further expand its footprint internationally. (DFM)

5. Page 5 of 6

IFA BoD recommends non-distribution of dividends –

International Financial Advisors’ (IFA) board of directors has

recommended not to distribute dividend for the year ended

December 31, 2014. Meanwhile, IFA’s BoD recommended

writing-off accumulated losses of KD65.5mn for the financial

period ended December 31, 2014, through KD30.86mn from

legal reserves, KD30.56mn from voluntary reserves and

KD4.08mn against share premium. (DFM)

DPR signs MoU with Dnata – Dubai Parks & Resorts (DPR)

has signed a MoU with Dnata to be the preferred travel partner

for the destination, which will open in October 2016. The

commercial agreement allows DPR access to Dnata’s extensive

travel portfolio to support them in the sale & distribution of

tickets and visitor packages to customers across the globe.

(DFM)

Tabreed seeks shareholders’ nod for bond buyback –

National Central Cooling Company (Tabreed) is planning to

convene an ordinary general assembly (OGM), where it would

present a proposal to shareholders to buy back 28% of the

mandatory convertible bonds (MCB) currently held by Mubadala.

In the proposal, Tabreed will seek shareholders’ approval to buy

back 854mn MCB at a cost of AED1bn. The MCB were issued

to Mubadala as part of Tabreed’s 2011 recapitalization program.

The buyback will be financed through a new loan which Tabreed

secured during its 2014 refinancing, and which has a lower cost

of servicing than the MCB. (DFM)

RP Global breaks ground on AED1.5bn Dubai tower – RP

Global, a part of RP Group of Companies, has broken ground on

its AED1.5bn RP Heights, a multi-storey residential tower

project. The developer will initially work on two big projects

worth AED5.5bn in Dubai. RP Heights, the first project in

Downtown Dubai is a multi-storey residential tower, while the

second project, RP One will be a mixed-use development on

Sheikh Zayed Road, which will be unveiled in 2H2015.

(GulfBase.com)

DLD: Dubai real estate transactions plunge 51.8% in April

2015 – According to the Dubai Land Department (DLD), the total

number of property transactions in Dubai plunged 51.8% YoY to

7,311 in April 2015. The total value of transactions in April 2015

stood at AED35.3bn, down 37.1% YoY. Sales numbers in Dubai

have been falling steadily since 2014-end after the Dubai

government introduced tough new mortgage caps and higher

transaction fees in an attempt to slow what had been one of the

fastest rising housing markets in the world. (GulfBase.com)

KFH mulls selling Malaysia unit – Kuwait Finance House

(KFH) may sell some of its investments, including KFH Malaysia

and has picked Credit Suisse to advise it on the matter.

(Reuters)

Fincorp launches Finxpress Trade & Islamic IB services –

The Financial Corporation (Fincorp) has launched Shari’ah-

compliant Islamic investment banking (IB) services and a new

mobile application ‘Finxpress Trade’. This application will enable

the users to trade in the Muscat Securities Market from their

smartphones. Shari’ah-compliant Islamic investment banking

services will cover brokerage, asset management, corporate

finance and advisory services. (MSM)

BMB reports $1.4mn net profit in 1Q2015 – Bahrain Middle

East Bank (BMB) reported a net profit of $1.4mn in 1Q2015 as

compared to $1.5mn in 1Q2014. The bank’s total operating

income reached $2.8mn in 1Q2015 as compared to $3.0mn in

1Q2014. BMB’s total assets stood at $172.5mn at the end of

March 31, 2015 as compared to $172.8mn at the end of

December 31, 2014. Loans & advances reached $129.9mn,

while deposits from financial institutions and customers stood at

$124.2mn and $14.2mn, respectively. EPS was amounted to

0.58 US cents in 1Q2015 versus 0.63 US cents in 1Q2014.

(Bahrain Bourse)

ABC Islamic Bank’s net profit surges 75% YoY in 1Q2015 –

ABC Islamic Bank reported a net profit of $6.1mn in 1Q2015,

showing an increase of 75% YoY and 68% QoQ. The bank’s

total operating income rose to $7.7mn, up 50% YoY. Operating

expenses remained flat at $1.6mn. ABC Islamic Bank’s total

assets stood at $1.38bn at the end of March 31, 2015 as

compared to $1.33bn at the end of December 31, 2014.

(GulfBase.com)

6. Contacts

Saugata Sarkar Sahbi Kasraoui QNB Financial Services SPC

Head of Research Head of HNI Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6534 Tel: (+974) 4476 6544 PO Box 24025

saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa Doha, Qatar

Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the

Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is

not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability

whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically

engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report

has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any

representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis,

expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical

technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment

decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg (*$ adjusted returns; Marked closed on May 6. 2015)

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Mar-11 Mar-12 Mar-13 Mar-14 Mar-15

QSE Index S&P Pan Arab S&P GCC

0.3%

1.0%

0.4%

0.2%

0.0%

(0.5%)

1.1%

(1.0%)

(0.5%)

0.0%

0.5%

1.0%

1.5%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,192.22 (0.1) 1.2 0.6 MSCI World Index 1,772.82 (0.0) (0.8) 3.7

Silver/Ounce 16.52 (0.2) 2.2 5.2 DJ Industrial 17,841.98 (0.5) (1.0) 0.1

Crude Oil (Brent)/Barrel (FM

Future)

67.77 0.4 2.0 18.2 S&P 500 2,080.15 (0.4) (1.3) 1.0

Crude Oil (WTI)/Barrel (FM

Future)

60.93 0.9 3.0 14.4 NASDAQ 100 4,919.65 (0.4) (1.7) 3.9

Natural Gas (Henry

Hub)/MMBtu

2.75 (0.5) 3.0 (8.3) STOXX 600 388.68 0.5 (0.2) 6.2

LPG Propane (Arab Gulf)/Ton 51.63 (2.6) (4.8) 5.4 DAX 11,350.15 1.3 0.1 7.8

LPG Butane (Arab Gulf)/Ton 61.00 (2.8) (3.6) (2.8) FTSE 100 6,933.74 0.3 0.0 3.2

Euro 1.13 1.4 1.3 (6.2) CAC 40 4,981.59 1.2 (0.3) 9.1

Yen 119.46 (0.3) (0.6) (0.3) Nikkei#

19,531.63 0.0 0.0 11.2

GBP 1.52 0.4 0.6 (2.1) MSCI EM 1,040.44 (0.7) (0.5) 8.8

CHF 1.09 1.1 1.8 8.5 SHANGHAI SE Composite 4,229.27 (1.5) (4.8) 30.9

AUD 0.80 0.3 1.5 (2.5) HANG SENG 27,640.91 (0.4) (1.8) 17.1

USD Index 94.09 (1.0) (1.3) 4.2 BSE SENSEX 26,717.37 (3.1) (1.1) (3.5)

RUB 50.82 0.6 (2.1) (16.3) Bovespa 57,103.14 (1.5) (0.1) (1.1)

BRL 0.33 0.8 (0.7) (12.6) RTS 1,066.19 (0.6) 3.6 34.8

177.2

144.1

130.2