VIP Independent Call Girls in Bandra West 🌹 9920725232 ( Call Me ) Mumbai Esc...

9 April Daily Market Report

1. Page 1 of 5

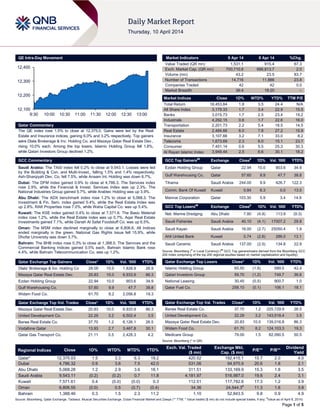

QE Intra-Day Movement

Qatar Commentary

The QE index rose 1.5% to close at 12,375.0. Gains were led by the Real

Estate and Insurance indices, gaining 6.0% and 3.2% respectively. Top gainers

were Dlala Brokerage & Inv. Holding Co. and Mazaya Qatar Real Estate Dev.,

rising 10.0% each. Among the top losers, Islamic Holding Group fell 1.8%,

while Qatari Investors Group declined 1.2%.

GCC Commentary

Saudi Arabia: The TASI index fell 0.2% to close at 9,543.1. Losses were led

by the Building & Con. and Multi-Invest., falling 1.5% and 1.4% respectively.

Ash-Sharqiyah Dev. Co. fell 7.5%, while Anaam Int. Holding was down 6.7%.

Dubai: The DFM index gained 0.9% to close at 4,786.3. The Services index

rose 2.9%, while the Financial & Invest. Services Index was up 2.3%. The

National Industries Group gained 5.7%, while Arabtec Holding was up 3.9%.

Abu Dhabi: The ADX benchmark index rose 1.2% to close at 5,068.3. The

Investment & Fin. Serv. index gained 5.4%, while the Real Estate Index was

up 2.8%. RAK Properties rose 7.0%, while Waha Capital Co. was up 5.4%.

Kuwait: The KSE index gained 0.4% to close at 7,571.6. The Basic Material

index rose 1.2%, while the Real Estate index was up 0.7%. Aqar Real Estate

Investments gained 7.1%, while Danah Al Safat Foodstuff Co. was up 6.5%.

Oman: The MSM index declined marginally to close at 6,806.6. All Indices

ended marginally in the green. National Gas Rights Issue fell 15.9%, while

Dhofar University was down 3.7%.

Bahrain: The BHB index rose 0.3% to close at 1,388.5. The Services and the

Commercial Banking Indices gained 0.5% each. Bahrain Islamic Bank rose

4.4%, while Bahrain Telecommunication Co. was up 1.2%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Dlala' Brokerage & Inv. Holding Co 28.05 10.0 1,828.9 26.9

Mazaya Qatar Real Estate Dev. 20.83 10.0 6,933.9 86.3

Ezdan Holding Group 22.94 10.0 903.6 34.9

Gulf Warehousing Co. 57.60 9.9 47.7 38.8

Widam Food Co. 61.70 8.2 2,056.8 19.3

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Mazaya Qatar Real Estate Dev. 20.83 10.0 6,933.9 86.3

United Development Co. 22.29 3.2 6,502.4 3.5

Barwa Real Estate Co. 37.70 1.2 6,126.1 26.5

Vodafone Qatar 13.93 2.7 3,467.8 30.1

Qatar Gas Transport Co. 21.11 0.5 2,428.3 4.2

Market Indicators 9 Apr 14 8 Apr 14 %Chg.

Value Traded (QR mn) 1,531.1 915.4 67.3

Exch. Market Cap. (QR mn) 700,710.6 686,813.7 2.0

Volume (mn) 43.2 23.5 83.7

Number of Transactions 14,716 11,886 23.8

Companies Traded 42 42 0.0

Market Breadth 36:4 18:20 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,453.84 1.8 3.5 24.4 N/A

All Share Index 3,179.33 1.7 3.4 22.9 15.5

Banks 3,015.73 1.7 2.5 23.4 15.2

Industrials 4,292.15 0.6 1.7 22.6 16.0

Transportation 2,201.73 2.2 5.4 18.5 14.5

Real Estate 2,484.66 6.0 7.8 27.2 15.9

Insurance 3,107.66 3.2 7.1 33.0 8.2

Telecoms 1,673.69 2.3 6.0 15.1 23.7

Consumer 7,451.14 0.6 5.5 25.3 30.3

Al Rayan Islamic Index 3,949.44 2.5 6.6 30.1 18.2

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ezdan Holding Group Qatar 22.94 10.0 903.6 34.9

Gulf Warehousing Co. Qatar 57.60 9.9 47.7 38.8

Tihama Saudi Arabia 244.00 9.9 426.7 122.3

Comm. Bank Of Kuwait Kuwait 0.84 6.3 0.0 13.5

Mannai Corporation Qatar 103.30 5.9 3.4 14.9

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Nat. Marine Dredging Abu Dhabi 7.80 (4.9) 113.9 (9.3)

Saudi Fisheries Saudi Arabia 40.10 (4.1) 17007.2 29.8

Saudi Kayan Saudi Arabia 16.00 (2.7) 25050.4 1.9

Ahli United Bank Kuwait 0.74 (2.6) 286.0 13.1

Saudi Ceramic Saudi Arabia 137.00 (2.5) 134.8 22.9

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 65.50 (1.8) 589.5 42.4

Qatari Investors Group 59.70 (1.2) 749.7 36.6

National Leasing 30.45 (0.5) 900.7 1.0

Qatar Fuel Co. 258.10 (0.1) 106.1 18.1

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Barwa Real Estate Co. 37.70 1.2 225,729.9 26.5

United Development Co. 22.29 3.2 143,518.4 3.5

Mazaya Qatar Real Estate Dev. 20.83 10.0 139,016.8 86.3

Widam Food Co. 61.70 8.2 124,103.3 19.3

Medicare Group 79.00 1.5 82,090.5 50.5

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,375.03 1.5 3.3 6.3 19.2 420.52 192,415.1 15.7 2.0 4.0

Dubai 4,786.32 0.9 3.6 7.5 42.0 531.06 94,970.9 20.6 1.8 2.1

Abu Dhabi 5,068.28 1.2 2.9 3.6 18.1 311.51 133,169.9 15.3 1.8 3.5

Saudi Arabia 9,543.11 (0.2) (0.2) 0.7 11.8 4,181.97 516,987.0 19.6 2.4 3.1

Kuwait 7,571.61 0.4 (0.0) (0.0) 0.3 112.51 117,782.6 17.3 1.2 3.9

Oman 6,806.55 (0.0) 0.5 (0.7) (0.4) 34.36 24,544.3#

11.3 1.6 3.9

Bahrain 1,388.46 0.3 1.5 2.3 11.2 1.10 52,843.5 9.8 0.9 4.9

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any;

#

Value as of April 8, 2014)

12,100

12,200

12,300

12,400

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 5

Qatar Market Commentary

The QE index rose 1.5% to close at 12,375.0. The Real Estate

and Insurance indices led the gains. The index rose on the back

of buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Dlala Brokerage & Inv. Holding Co. and Mazaya Qatar Real

Estate Dev. were the top gainers, rising 10.0% each. Among the

top losers, Islamic Holding Group fell 1.8%, while Qatari

Investors Group declined 1.2%.

Volume of shares traded on Wednesday rose by 83.7% to

43.2mn from 23.5mn on Tuesday. Further, as compared to the

30-day moving average of 18.2mn, volume for the day was

137.8% higher. Mazaya Qatar Real Estate Dev. and United

Development Co. were the most active stocks, contributing

16.1% and 15.1% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn)1Q2014

% Change

YoY

Operating Profit

(mn) 1Q2014

% Change

YoY

Net Profit (mn)

1Q2014

% Change

YoY

National Company for Glass

Industries (ZOUJAJ)

Saudi SR – – 7.7 48.1% 14.8 72.1%

Nakheel Dubai AED 1,370.00 NA – – 629.0 28.1%

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

04/09 US MBA MBA Mortgage Applications 4-April -1.60% – -1.20%

04/09 US US Census Bureau Wholesale Inventories MoM February 0.50% 0.50% 0.80%

04/09 US US Census Bureau Wholesale Trade Sales MoM February 0.70% 1.00% -1.80%

04/09 Germany Destatis Trade Balance February 16.3B 17.5B 15.0B

04/09 Germany Deutsche Bundesbank Exports SA MoM February -1.30% -0.50% 2.20%

04/09 Germany Deutsche Bundesbank Imports SA MoM February 0.40% 0.10% 4.10%

04/09 UK BRC BRC Shop Price Index YoY March -1.70% -1.50% -1.40%

04/09 UK ONS Trade Balance February -£2058 -£2100 -£2203

04/09 Spain INE House transactions YoY February -27.60% – -23.20%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QNBK reports QR2.4bn net profit in 1Q2014 – QNB Group

(QNBK) reported a net profit of QR2.4bn in 1Q2014, up by

13.7% YoY. This was driven by operating income, including the

share of results from associates, which increased to QR3.7bn,

up by 26.2% YoY. Net interest income increased by 25.7% YoY

to reach QR3.0bn, with net fee and commission income and net

gain from foreign exchange reaching QR0.5bn and QR0.2bn.

Moreover, QNB Group maintained its cost-to-income ratio at

21.7%. Total assets increased by 20.6% YoY to reach

QR458bn, the highest ever achieved by the Group. This was

due to a strong growth rate of 22.5% (YoY) in loans and

advances which reached QR317bn. At the same time, QNB

Group increased customer funding by 23.4% to QR346bn. This

led to a loans to deposits ratio of 92%. The Group was able to

maintain the ratio of non-performing loans to gross loans at

1.6% while the coverage ratio reached 126%. The Group started

implementing updated QCB and Basel III requirements for the

calculation of the Capital Adequacy Ratio (CAR) from 1Q2014.

The ratio stood at 16.3% as at 31 March 2014, higher than the

regulatory minimum requirements of the QCB. The Group is

keen to maintain a strong capitalization in order to support future

strategic plans. (QNB Group Press Release)

QIGD 1Q2014 net profit up by 10.4% YoY – Qatari Investors

Group (QIGD) reported a net profit of QR58.6mn in 1Q2014 vs.

QR53.1mn in 1Q2013. EPS amounted to QR0.47 as of March

31, 2014 versus QR0.43 during the same period last year. (QE)

MPHC to disclose 1Q2014 results on April 22 – Mesaieed

Petrochemical Holding Company (MPHC) has announced that it

will disclose its 1Q2014 financial results on April 22, 2014. (QE)

MCCS to disclose 1Q2014 financials on April 23 – Mannai

Corporation Company (MCCS) has announced its intent to

disclose its 1Q2014 financial results on April 23, 2014. (QE)

IQCD to disclose 1Q2014 results on April 27 – Industries

Qatar (IQCD) has announced that it will disclose its 1Q2014

financial results on April 27, 2014. (QE)

QNNS to disclose 1Q2014 results on April 28 – Milaha

(QNNS) has announced that it will disclose its 1Q2014 financial

results on April 28, 2014. (QE)

NLCS to disclose 1Q2014 results on April 30 – Alijarah

Holding Company (NLCS) has announced that it will disclose its

1Q2014 financial results on April 30, 2014. (QE)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 71.83% 74.69% (43,656,480.37)

Non-Qatari 28.16% 25.31% 43,656,480.37

3. Page 3 of 5

Qatar Cool buys Cool Tech, I2I to sustain market leadership

– Qatar District Cooling Company (Qatar Cool) has acquired

Cool Tech Qatar as well as Installation Integrity 2006 (I2I) as

part of its strategy to maintain leadership in providing district

cooling & related services in local and regional markets. Qatar

Cool acquired the remaining 49% stake from an Emirati

shareholder to make it a wholly-owned subsidiary. The company

currently provides district cooling services for several prominent

developments in Qatar, including The Pearl-Qatar and West Bay

residential and business district. I2I is a commissioning

specialist for plants, buildings, and installations, handling all

non-process mechanical, electrical and plumbing installations as

well as HVAC systems. (Gulf-Times.com)

QA moves into Tokyo's Narita Airport T2 – Qatar Airways

(QA) has moved from Terminal 1 to Terminal 2 of Tokyo’s Narita

International Airport in order to join its fellow Oneworld alliance

partners. The move to Terminal 2, which is the airport’s most

modern terminal, will bring additional advantages to QA

including shared facilities with fellow Oneworld partners, such as

check-in and transfer desks, lounges and baggage services.

These factors make the travel experience for its customers

smoother and more efficient, while reducing costs. Further, QA

will add its third route to the Japanese market from June 18,

2014, when it will begin operating non-stop daily flights on a

Boeing 787 Dreamliner to Haneda International Airport, the

second major airport that serve the Greater Tokyo Area.

(Bloomberg)

First Qatar invests in Hilton’s project on Pearl Qatar – The

First Qatar Real Estate Development Company (First Qatar) has

signed a management agreement for its property on the Pearl

Island with Hilton Worldwide. In the next few years, First Qatar

will be investing up to $390mn in the new hotel, which will be

located on the artificial island, The Pearl. (Bloomberg)

Emir appoints CEO of Qatar Media Corp – HH the Emir

Sheikh Tamim bin Hamad al-Thani has appointed HE Sheikh

Abdurrahman bin Hamad bin Jassim bin Hamad al-Thani as the

Chief Executive Officer of Qatar Media Corporation. (Gulf-

Times.com)

International

Fed member sees little need for rapid US rate hike – A

member of the US Federal Reserve’s Board of Governors,

Daniel Tarullo said the modest pace of the US economic growth

in recent years suggests that when the time comes to raise

interest rates, the Fed will be able to do so without fearing a

sudden surge in inflation. Many economists had expected the

US economy to roar back after the Great Recession, requiring a

rapid tightening of policy at some point. Since that scenario

never happened, Tarullo said the US is less likely to experience

a growth spurt in the next couple of years that would engender

concerns about rapid wage pressures and changes in inflation

expectations. Tarullo further said that the monetary policy could

lay the groundwork for improving the potential growth rate by

reducing labor market slack. (Reuters)

German imports rise to highest level since reunification –

Germany’s imports climbed to their highest level since

reunification while exports fell in February, in a sign that

domestic demand in Europe's largest economy is gathering

pace. Figures from the Federal Statistics Office showed

seasonally-adjusted imports climbed by 0.4% to €77.6bn, their

highest level since Germany was reunified in January 1991. A

Reuters poll of economists had expected imports to increase by

a smaller 0.1%. However, German exports dropped by a larger-

than-expected 1.3% as compared to 0.5% forecast, with

economists attributing it to the turbulence in emerging markets

and the Crimean crisis. (Reuters)

BoJ: Consumer spending will put upward pressure on

prices – The Bank of Japan’s (BOJ) board member Ryuzo

Miyao stated that gains in consumer spending in Japan are

being driven by an improvement in underlying demand, which

will place an upward pressure on prices. Miyao said Japanese

economy and consumer prices are moving broadly in line with

the central bank's forecasts. So the economy can continue to

grow above its potential despite the temporary shock from a

sales tax hike on April 1. Meanwhile, the BoJ voted unanimously

to maintain its pledge of increasing base money – its key policy

gauge – at an annual pace of 60tn to 70tn yen ($582-679bn).

The BoJ has stood pat since launching an intense burst of

stimulus in April 2013, when it pledged to accelerate inflation to

2% in roughly two years through aggressive asset purchases in

a country mired in deflation for 15 years. (Reuters)

Regional

GIH: GCC corporate earnings rose by 12.4% YoY to $61.8bn

– According to a study by Global Investment House (GIH),

corporate earnings in GCC countries rose by 12.4% YoY to

$61.8bn in 2013. The UAE led overall earnings by posting a

21.3% YoY increase and contributing 4.4% to the incremental

rise in earnings in the region. Saudi Arabia came in second with

a 6.8% YoY followed by Qatar with a 9.7%. Qatar’s corporate

earnings rose by 9.7% YoY to reach $11.2bn during 2013 as

compared to $10.2bn during 2012. Consolidated earnings of

firms listed on the Bahrain Stock Exchange increased by 18.6%

YoY to reach $1.8bn in 2013 primarily driven by the banking

sector. Kuwaiti firms' consolidated earnings rose by 23.3% YoY

to reach $5.5bn in 2013, primarily led by the financial services

and real estate sectors. Corporate earnings in Oman rose

21.1% YoY to $2.1bn in 2013, mainly due to improvements in

the earnings of banks and investment firms. In Saudi Arabia,

TASI’s consolidated earnings rose 6.8% to $27.4bn in 2013

driven by a robust 31.8% growth in telecommunication and IT

companies. (GulfBase.com)

Saudi telco regulator to re-tender piggyback mobile licence

– Saudi Arabia's telecom regulator will re-tender a licence for

piggyback services on mobile operator Zain Saudi's network,

nearly a year after naming Dubai-based retailer Axiom Telecom

as the provisional winner. The Communications and Information

Technology Commission's (CITC) decision, is a setback for Zain

Saudi, which is facing competition from other mobile virtual

network operators (MVNO) that will launch soon on rivals'

platforms but will not be in a position to collect revenue from its

own. (Reuters)

RSH signs LoA for SR75mn housing construction – Red

Sea Housing Services Company (RSH) has signed a Letter of

Acceptance (LoA) with the Government of Papua New Guinea

to construct housing units in Port Moresby for SR75mn. The

agreement to construct houses for Bomana Police Housing

Estate is expected to be finalized during 2Q2014. (Tadawul)

SABB’s profit reaches SR1.08bn in 1Q2014 – The Saudi

British Bank (SABB) has reported a net profit of SR1.08bn in

1Q2014 as compared to SR947.9mn in 1Q2013, reflecting an

increase of 14%. The bank’s operating income increased by

12.8% to SR1.62bn in 1Q2014 as compared to SR1.44bn in

1Q2013. Loans & advances stood at SR109.9bn, increasing by

8.6% over SR101.2bn in 1Q2013. Customer deposits grew by

12.2% to SR137bn from SR122bn. Total assets stood at

SR175bn as against SR159bn a year ago. The bank’s EPS

amounted to SR1.08 in 1Q2014 as compared to SR0.95 in

1Q2013. (Tadawul)

4. Page 4 of 5

ANB reports SR713mn net profit in 1Q2014 – The Arab

National Bank’s (ANB) net profit increased by 5% to SR713mn

in 1Q2014 as compared to SR679mn in 1Q2013. The total

assets stood at SR151bn as against SR134bn a year ago.

Loans & advances grew to SR87bn as compared to SR86bn in

1Q2013, while customer deposits grew to SR118bn as

compared to SR109bn a year ago. EPS stood at SR0.71 at the

end of first quarter. (Tadawul)

Alinma Bank’s profit reaches SR293mn in 1Q2014 – Alinma

Bank has reported a net profit of SR293mn in 1Q2014 as

compared to SR221mn in 1Q2013, reflecting an increase of

32.6%. The bank’s total assets at the end of the quarter ended

March 31, 2014 stood at SR65.4bn as compared to SR56.2bn a

year ago. Loans & advances grew to SR45.8bn from SR39.4bn,

while customer deposits grew to SR45.1bn from SR34.4bn. EPS

stood at SR0.2 at the end of 1Q2014. (Tadawul)

KFH-Saudi to be financial advisor for Murabaha – Murabaha

Company has signed a deal with Saudi-Kuwaiti Finance House

(KFH-Saudi) to serve as its financial advisor in order to take

steps toward offering 30% of its shares in a public offering.

(Gulfbase.com)

SEC succeeds in pricing, allocating of $2.5bn instruments –

The Saudi Electricity Company (SEC) has successfully

completed the pricing and allocation of instruments worth a total

value of $2.5bn. This issuance included two tranches of

certificates first instruments worth $1.5bn and a maturity of 10

years with a yield of 4% and the second valued $1bn and a

maturity of 30 years with a yield of 5.5 %. The yield for each

tranche shall be paid every six months. The instruments were

issued upon an arrangement by Deutsche Bank, HSBC and JP

Morgan. The final size of the subscription amounted to $12.5bn,

representing more than five times the required amount.

(GulfBase.com)

Lama Group, Carfare merge to form AED365mn company –

UAE-based Lama Group and Carfare have merged to create a

travel & mobility company worth AED365mn. Both entities will

retain their brand names but will operate under BK Group

Holdings Company and offer travel & mobility solutions to

around 2.5mn customers of the group. As a result of this

merger, the group will have a fleet of 3,500 cars, 200

limousines, a large fleet of 4x4 vehicles, three campsites, two

cruises and two yachts. The company will have 650 employees

working across a network of 14 branches in the UAE and 9

branches abroad. BK Group Holdings Company will expand

both the companies’ operations into a new head office in Dubai

Investment Park spread over 40,000 square feet. (Bloomberg)

du Telecom declares AED0.19 dividend per share for

2H2013 – Emirates Integrated Telecommunications Company’s

(du Telecom) AGM has approved the distribution of cash

dividend of AED0.19 per share for 2H2013. (DFM)

Emirates NBD declares 25% dividend – Emirates NBD’s AGM

has approved the distribution of 25% cash dividend (25 fils per

share) for the year ended December 31, 2013. (DFM)

NGI declares 20% dividend – The National General Insurance

Company’s (NGI) AGM has approved its board’s

recommendation for the distribution of 20% cash dividend to the

shareholders. (DFM)

Dubai exports to Kingdom reach AED9bn in March –

According to the figures published by the Dubai Chamber,

exports from Dubai to Saudi Arabia crossed AED9bn in March

2014, representing 16% YoY growth and 33% MoM growth.

Dubai’s total exports touched AED25.5bn, higher by 7% than

AED23.9bn recorded in February with a YoY increase of 5%

compared to March 2013. The GCC was Dubai’s largest export

destination with total exports to the region reaching AED15.8bn,

with Saudi Arabia taking 57% of the total GCC exports. Kuwait

was second to Saudi Arabia, with exports to the country of

AED1.8bn representing a growth of 23% MoM and 10% YoY.

Meanwhile, exports to Qatar declined to AED1.8bn registering a

significant MoM drop of 37% from the previous month’s

AED2.9bn. YoY growth was also down at 6%, from AED1.9bn a

year ago. Exports to Oman and Bahrain posted significant MoM

growth of 33% and 32% and YoY growth of 11% and 64%

respectively. (GulfBase.com)

GIH: Abu Dhabi’s corporate earnings up 14.5% to $9bn –

According to a study by Global Investment House, Abu Dhabi’s

corporate earnings increased by 14.5% YoY to reach $9bn in

2013. This rise was driven by 13.6% YoY growth in the banking

sector’s earnings to $5.5bn in 2013, accounting for more than

60% growth in consolidated earnings. The real estate sector

posted a growth of 53.1% YoY, accounting for 8.3% of the

consolidated 2013 earnings. The insurance sector also

contributed significantly during 2013, with its earnings growing

62.4% YoY. The consumer staples sector posted the largest

decline in earnings with 58.9% YoY. (GulfBase.com)

Brazil's BRF raises stake in Federal Foods – Brazil-based

BRF has raised its stake in Abu Dhabi's Federal Foods with a

$27.8mn investment meant to expand its international reach. In

January 2013, BRF had purchased 49% stake in Federal Foods

for $37.1mn. BRF started building a processed food plant in Abu

Dhabi in 2012, which it hopes to launch in 1H2014. The plant is

meant to give the company an access to distant Asian markets

like Indonesia. (Reuters)

Al-Ahleia Insurance declares KD6.2mn dividend – Al-Ahleia

Insurance Company’s AGM has approved the distribution of

KD6.2mn cash dividend (KD0.32 per share) to the shareholders.

(Bloomberg)

Oman signs OMR77mn loan deal with Arab Fund – The

Oman Housing Bank (OHB) has signed an agreement with the

Arab Fund for Economic & Social Development (AFESD) to

avail a loan facility worth OMR55mn to partly meet the annual

loan programs provided by the housing bank. The loan with a

term of 23 years will be repaid in 37 bi-monthly installments after

a four-year grace period from the date of disbursing the first

portion of the loan. Another agreement was signed where the

Public Establishment for Industrial Estates will obtain

OMR21.9mn to finance costs of the infrastructure projects in

Sumail Industrial Zone. The loan, which has a term of 21 years,

aims at developing the industrial sector and providing small &

medium enterprises with their needs. (Bloomberg)

ASBB boosts share capital – Al Salam Bank-Bahrain (ASBB)

has increased its authorized share capital to BHD250mn and its

issued & paid-up share capital to BHD214mn. The bank’s share

capital has been increased as part of its acquisition of BMI

Bank. (GulfBase.com)

Batelco completes 46% acquisition in Quality Net – Batelco

Group announced that it has finalized the acquisition of Ali

Aighanim & Sons General Trading & Contracting Company’s

46% shareholding in Quality Net. This acquisition increases

Batelco Group's equity stake in Quality Net from 44% to 90%.

(Bahrain Bourse)

5. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

(0.2%)

1.5%

0.4% 0.3%

(0.0%)

1.2%

0.9%

(0.8%)

0.0%

0.8%

1.6%

2.4%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,311.78 0.2 0.6 8.8 DJ Industrial 16,437.18 1.1 0.1 (0.8)

Silver/Ounce 19.88 (0.8) (0.4) 2.1 S&P 500 1,872.18 1.1 0.4 1.3

Crude Oil (Brent)/Barrel (FM

Future)

107.98 0.3 1.2 (2.5) NASDAQ 100 4,183.90 1.7 1.4 0.2

Natural Gas (Henry

Hub)/MMBtu

4.66 2.3 4.0 7.3 STOXX 600 335.16 0.4 (1.2) 2.1

LPG Propane (Arab Gulf)/Ton 110.75 1.4 2.5 (12.5) DAX 9,506.35 0.2 (2.0) (0.5)

LPG Butane (Arab Gulf)/Ton 122.25 (0.2) 0.4 (9.9) FTSE 100 6,635.61 0.7 (0.9) (1.7)

Euro 1.39 0.4 1.1 0.8 CAC 40 4,442.68 0.4 (0.9) 3.4

Yen 102.00 0.2 (1.2) (3.1) Nikkei 14,299.69 (2.1) (5.1) (12.2)

GBP 1.68 0.3 1.3 1.4 MSCI EM 1,014.83 0.3 1.3 1.2

CHF 1.14 0.4 1.4 1.5 SHANGHAI SE Composite 2,105.24 0.3 2.3 (0.5)

AUD 0.94 0.3 1.1 5.3 HANG SENG 22,843.17 1.1 1.5 (2.0)

USD Index 79.48 (0.3) (1.2) (0.7) BSE SENSEX 22,702.34 1.6 1.5 7.2

RUB 35.65 (0.1) 1.1 8.5 Bovespa 51,185.40 (0.9) 0.2 (0.6)

BRL 0.45 0.1 2.0 7.5 RTS 1,190.13 (0.5) (3.5) (17.5)

177.8

152.7

138.5