1. Page 1 of 7

QE Intra-Day Movement

Qatar Commentary

The QE Index declined 2.9% to close at 12,942.0. Losses were led by the Real Estate and Consumer Goods & Services indices, declining 4.3% and 2.9%, respectively. Top losers were Salam International Inv. Co. and Mazaya Qatar Real Estate Dev., falling 7.5% and 5.8%, respectively. Among the top gainers, Qatar Navigation rose 1.3%, while Qatar Cinema & Film Distrib. was up 1.2%.

GCC Commentary

Saudi Arabia: The TASI Index fell 3.6% to close at 9,547.5. Losses were led by the Insurance and Transport indices, falling 7.3% and 6.4%, respectively. Saudi Arabia Refineries Co. and SABB Takaful were down 9.9% each.

Dubai: The DFM Index declined 4.9% to close at 4,270.4. The Services index fell 7.1%, while the Financial & Investment Services index was down 5.8%.Ekttitab Holding Co. fell 9.2%, while Shuaa Capital was down 9.1%.

Abu Dhabi: The ADX benchmark index fell 2.3% to close at 4,768.2. Real Est. index declined 5.1%, while the Inv. & Fin. Ser. index fell 4.4%. National Bank of Umm Al-Qaiwain fell 9.9%, while Abu Dhabi Ship Building declined 9.8%.

Kuwait: The KSE Index fell 1.7% to close at 7,410.3. The Technology index declined 4.1%, while the Basic Material index fell 3.7%. Metal & Recycling Co. declined 8.6%, while Al-Mazaya Holding Co. was down 7.1%.

Oman: The MSM Index declined 3.3% to close at 6,872.3. Losses were led by the Financial and Industrial indices, falling 5.3% and 2.7%, respectively. Al Sharqia Investment fell 9.9%, while Gulf Investment Services was down 9.8%.

Bahrain: The BHB Index fell 1.0% to close at 1,447.1. The Industrial index was down 3.8%, while the Investment index declined 0.8%. Aluminum Bahrain fell 3.9%, while Ithmaar Bank was down 2.6%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Navigation

93.40

1.3

30.5

12.5 Qatar Cinema & Film Distrib. Co. 43.50 1.2 1.2 8.5 Islamic Holding Group 125.70 0.9 118.5 173.3 Zad Holding Co. 86.50 0.6 1.1 24.5 Doha Insurance Co. 32.50 0.3 36.2 30.0

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group

18.44

(5.2)

3,980.3

8.5 Vodafone Qatar 19.89 (2.8) 1,515.0 85.7

Masraf Al Rayan

51.30

(3.0)

1,279.2

63.9 Mazaya Qatar Real Estate Dev. 21.00 (5.8) 627.9 87.8

QNB Group

201.20

(3.1)

612.6

17.0

Market Indicators 16 Oct 14 15 Oct 14 %Chg.

Value Traded (QR mn)

771.9

534.7

44.4 Exch. Market Cap. (QR mn) 699,385.4 718,892.9 (2.7)

Volume (mn)

14.3

9.7

47.0 Number of Transactions 7,522 5,421 38.8

Companies Traded

43

43

0.0 Market Breadth 5:36 3:39 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return

19,302.87

(2.9)

(6.4)

30.2

N/A All Share Index 3,282.50 (2.7) (6.1) 26.9 16.0

Banks

3,253.49

(2.8)

(4.9)

33.1

15.5 Industrials 4,266.43 (2.6) (7.0) 21.9 15.2

Transportation

2,220.52

(0.4)

(4.6)

19.5

14.2 Real Estate 2,557.42 (4.3) (9.1) 30.9 22.6

Insurance

3,986.39

(2.2)

(3.2)

70.6

12.6 Telecoms 1,572.10 (1.0) (5.9) 8.1 22.3

Consumer

7,076.78

(2.9)

(6.6)

19.0

26.4 Al Rayan Islamic Index 4,364.30 (2.6) (7.0) 43.7 18.7

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

IFA Hotels & Resorts Co.

Kuwait

0.21

5.0

53.6

(25.6) Mabanee Co. Kuwait 1.06 1.9 799.2 (0.6)

Commercial Facilities Co.

Kuwait

0.29

1.8

0.1

3.6 Qatar Navigation Qatar 93.40 1.3 30.5 12.5

Jazeera Airways

Kuwait

0.45

1.1

66.0

(10.1)

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Solidarity Saudi Takaful

Saudi Arabia

20.20

(9.9)

3,798.6

(22.0) Saudi Fisheries Saudi Arabia 32.00 (9.9) 1,069.8 3.6

NBQ

Abu Dhabi

2.93

(9.9)

2.2

(11.2) Saudi Public Transport Co Saudi Arabia 30.40 (9.7) 3,040.2 12.2

Saudi Enaya Coop. Ins.

Saudi Arabia

34.29

(9.4)

599.4

(14.9)

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Salam International Investment Co

17.30

(7.5)

513.6

33.0 Mazaya Qatar Real Estate Dev. 21.00 (5.8) 627.9 87.8

Qatari Investors Group

52.00

(5.5)

77.7

19.0 Ezdan Holding Group 18.44 (5.2) 3,980.3 8.5

Widam Food Co.

58.10

(4.9)

71.5

12.4

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

QNB Group

201.20

(3.1)

124,124.4

17.0 Industries Qatar 178.00 (2.7) 83,349.6 5.4

Ezdan Holding Group

18.44

(5.2)

74,436.4

8.5 Masraf Al Rayan 51.30 (3.0) 66,069.6 63.9

Qatar Electricity & Water Co.

179.50

(1.4)

42,005.8

8.6

Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield

Qatar*

12,942.00

(2.9)

(6.4)

(5.7)

24.7

211.95

192,051.2

17.2

2.1

3.6 Dubai 4,270.43 (4.9) (13.6) (15.3) 26.7 485.66 96,204.4 17.7 1.6 2.2

Abu Dhabi

4,768.15

(2.3)

(6.1)

(6.6)

11.1

113.76

131,880.0

13.5

1.7

3.5 Saudi Arabia 9,547.54 (3.6) (12.0) (12.0) 11.9 2,717.01 518,301.9 18.3 2.3 3.0

Kuwait

7,410.34

(1.7)

(3.1)

(2.8)

(1.8)

135.07

111,253.0

19.1

1.2

3.7 Oman 6,872.27 (3.3) (8.1) (8.2) 0.6 20.67 25,675.4 10.9 1.6 4.0

Bahrain

1,447.06

(1.0)

(1.6)

(2.0)

15.9

1.82

54,027.1

11.2

1.0

4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

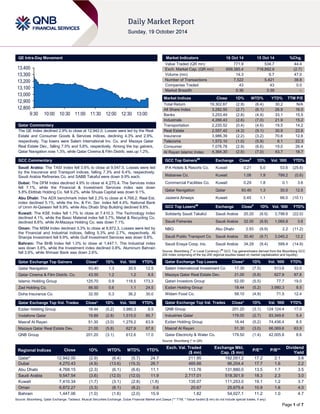

12,80012,90013,00013,10013,20013,30013,4009:3010:0010:3011:0011:3012:0012:3013:00

2. Page 2 of 7

Qatar Market Commentary

The QE Index declined 2.9% to close at 12,942.0. The Real Estate and Consumer Goods & Services indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari shareholders.

Salam International Investment Co. and Mazaya Qatar Real Estate Development were the top losers, falling 7.5% and 5.8%, respectively. Among the top gainers, Qatar Navigation rose 1.3%, while Qatar Cinema & Film Distribution Co. was up 1.2%.

Volume of shares traded on Thursday rose by 47.0% to 14.3mn from 9.7mn on Wednesday. Further, as compared to the 30-day moving average of 13.9mn, volume for the day was 2.7% higher. Ezdan Holding Group and Vodafone Qatar were the most active stocks, contributing 27.8% and 10.6% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

National Bank of Abu Dhabi (NBAD)

RAM

Abu Dhabi

FIR

AAA/P1

AAA/P1

–

Stable

–

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, FIR– Financial Institution Rating)

Earnings Releases Company Market Currency Revenue (mn)3Q2014 % Change YoY Operating Profit (mn) 3Q2014 % Change YoY Net Profit (mn) 3Q2014 % Change YoY Fitaihi Holding Group (FHG) Saudi Arabia SR – – 8.7 19.5% 6.4 22.9% Arabian Cement Co. (ACC) Saudi Arabia SR – – 143.3 2288.3% 133.9 697.0%

Al Alamiya For Cooperative Insurance Co. (Al Alamiya)*

Saudi Arabia

SR

122.9

–

–

–

1.2

– Insurance House (IH) * Abu Dhabi AED 67.5 -0.4% 3.2 -68.5% 7.2 -9.2%

Financial Services *

Oman

OMR

0.8

-2.2%

–

–

0.2

-47.2% Al Sharqia Investment Holding Co. (SIHC) * Oman OMR 1.6 20.8% – – 0.9 55.9%

Oman Oil Marketing Company (OOMS) *

Oman

OMR

264.6

19.0%

–

–

8.3

10.7% Salalah Beach Resort (SHCS) * Oman OMR 2.7 -0.7% – – 0.6 -8.6%

Fitaihi Holding Group (FHG)

Saudi Arabia

SR

–

–

8.7

19.5%

6.4

22.9%

Source: Company data, DFM, ADX, MSM (* 9M2014 results)

Global Economic Data Date Market Source Indicator Period Actual Consensus Previous

10/16

US

Department of Labor

Initial Jobless Claims

11-October

264.0K

290.0K

287.0K 10/16 US Federal Reserve Industrial Production MoM September 1.00% 0.40% -0.20%

10/16

US

Federal Reserve

Capacity Utilization

September

79.30%

79.00%

78.70% 10/16 US Federal Reserve Manufacturing (SIC) Production September 0.50% 0.30% -0.50%

10/16

US

Bloomberg

Bloomberg Consumer Comfort

12-October

36.2

–

36.8 10/16 US Bloomberg Bloomberg Economic Expectations October 51.0 – 41.5

10/16

US

National Ass. of Home B

NAHB Housing Market Index

October

54.0

59.0

59.0 10/16 US Department of Energy DOE US Crude Oil Inventories 10-October 8,923.0K 2,450.0K 5,015.0K

10/16

EU

Eurostat

Trade Balance SA

August

15.8B

13.3B

12.7B 10/16 EU Eurostat Trade Balance NSA August 9.2B – 21.6B

10/16

EU

Eurostat

CPI MoM

September

0.40%

0.40%

0.10% 10/17 EU Eurostat Construction Output MoM August 1.50% – 0.30%

10/17

EU

Eurostat

Construction Output YoY

August

-0.30%

–

0.50% 10/17 UK London Gold Mar. Fixing London Gold Market PM Fix 17-October 1,234.25 – 1,237.8

10/16

Italy

ISTAT

Trade Balance Total

August

2,056.0M

–

6,923.0M 10/16 Italy ISTAT Trade Balance EU August 339.0M – 3,378.0M

10/17

Italy

Banca D'Italia

Current Account Balance

August

2,312.0M

–

6,816.0M

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted

Overall Activity Buy %* Sell %* Net (QR)

Qatari

59.53%

47.12%

95,781,668.30 Non-Qatari 40.47% 52.88% (95,781,668.30)

3. Page 3 of 7

News

Qatar

QNBK: Qatar’s economy safe from deflation – According to a report by QNB Group (QNBK), Qatar is likely to remain well- insulated in the event a “great deflation” hits the global economy. A significant decline in commodity prices in recent weeks coupled with a worsening economic outlook and major corrections in equity markets could result in a great deflation or a vicious circle of price/asset deflation around the world. QNBK said that the risk of such a scenario occurring was rising as crude oil prices tumbled last week and major equity markets witnessed a significant correction. Although lower energy prices would imply smaller current account and fiscal surpluses, Qatar would have substantial financial resources to implement its ambitious investment program, leading to double-digit non- hydrocarbon growth, while keeping inflation firmly in the positive territory. (Gulf-Times.com)

MDPS Minister: Oil decline will not affect Qatar – Qatar’s Minister of Development Planning and Statistics, HE Dr Saleh Mohamed Saleh al-Nabit, said that Qatar’s development efforts will not be affected by the drop in oil prices. He said changes in oil prices take place from time to time and these are expected. For this reason, he added, Qatar implemented the basic principle of sustainability when it devised the development plan and that Qatar’s vision for the future would not be affected by such temporary changes. (Gulftimes.com)

QCB absorbs QR16bn liquidity through T-Bonds – According to the Qatar Central Bank’s (QCB) Fifth Financial Stability Review, a total of QR44bn worth of T-bills of various maturities were issued in 2013, while a similar amount matured. As a result, there was no net absorption of liquidity through T-bills. In contrast, the QCB absorbed QR16bn through issuance of T- bonds. QCB introduced a quarterly auction of 3-year and 5-year government bonds of QR2bn each since March 2013 in order to help in the formation of a yield curve for longer maturities. The issuance of such bonds was to facilitate the QCB’s liquidity management framework and provide a boost to the domestic debt market. As of end-2013, surplus liquidity declined to QR6.2bn as compared with QR13.5bn at end-2012. While net QMR (Qatar Monetary Rates) deposits declined sharply as compared to end-2012, excess reserves increased during the year. The decline in QMR deposits by the end of the year reflected auction of quarterly T-bonds in December 2013 and liquidity pressures due to negative spillovers from global developments. The QCB’s review report noted that since 2011, the central bank’s proactive liquidity management operations have helped in absorbing excess liquidity from the financial system, while facilitating credit flow to the productive sectors of the economy. (GulfBase.com)

QCB: QFC banks record rapid growth in 2013 – According to Qatar Central Bank (QCB), banks operating in the Qatar Financial Centre (QFC) saw rapid growth in 2013. The size of the QFC banking sector grew by 53.5% to $7.4bn at the end of 2013. Banks operating in QFC comprise 28 international, regional and domestic firms which are licensed as either branches or limited liability companies. Most of the medium-to- large QFC firms underwent an increase in their balance sheet throughout the year. Conventional banks represent 72.1% ($5.3bn) of the QFC banking system while Shari’ah-compliant banks comprise the remaining 27.9% ($2bn) of the sector. Not unlike the rest of Qatar or the GCC, the QFC banking sector is also concentrated primarily in the largest three banks, which on a combined basis represent almost 65% of the entire QFC banking sector. Gross loans and advances extended by QFC banks increased by approximately 58.2% to $4.2bn during 2013.

The increase in total loans and advances was due to increase in the financial institutions category and the other loans category which is predominantly comprised of term loans to corporate entities. Islamic contracts also experienced rapid growth throughout 2013. The majority of funding for QFC’s banking sector was attributable to the deposits category which represents 92.7% ($5.3bn) of total liabilities. (GulfBase.com)

Qatar’s insurance sector in upbeat mood – The gross written premium (GWP) of Qatar’s five listed insurance companies stood at $1.4bn in 2013. The density of insurance sector in Qatar increased to $686 in 2013 from $599 in 2012, indicating an increasing coverage. The Qatar Central Bank (QCB) in its latest ‘Financial Stability Review’ noted Qatar’s insurance sector is developing faster keeping in pace with the growth of the economy. The central bank restricts its analysis to the 5 listed insurance companies operating in Qatar. These companies are primarily involved in the non-life segments such as property, casualty, marine, engineering, motor and medical insurance. According to the QCB, the performance of one of the five companies helped the sector’s overall profit to reach to an overwhelming level of QR3.1bn in 2013. Marginal decline in net claim and increase in investment income, supported by manifold increase in net premium, helped the sector register the remarkable profit level in 2013. Extraordinary profit helped the sector to witness a comfortable ROE in 2013. The increase in net premium and marginal decline in net claim made the sector more resilient. The total gross premium of the five companies amounted to QR5.1bn in 2013, which accounted for roughly 0.7% of 2013 GDP. (Peninsula Qatar)

QGTS to disclose results on October 23 – Qatar Gas Transport Company (QGTS) will disclose its 3Q2014 financial statements on October 23, 2014. (QE)

DBIS to disclose results on October 29 – Dlala Brokerage & Investments Holding Company (DBIS) will disclose its 3Q2014 financial statements on October 29, 2014. (QE)

Qatari firms sign QR100mn contracts for Moroccan exports – Qatari and Moroccan traders have signed three commercial contracts worth QR100mn for the export of Qatar-manufactured plastic, irrigation, and other products. Qatar Development Bank (QDB) said that potential export opportunities were reviewed for promoting around 13 Qatari products that have a high demand in the Moroccan market, which include detergents, medical injections, aluminum, and plastic products. The 11 companies exporting these products include Qatar National Aluminum Panel Company, Qatar German Company for Medical Devices (QGMD), Qatar Polymer Industrial Company, Al Haya Waste Management & Projects, Gulf Plastic Company, International Company of Packaging, Qatar Integrated Plastic Bags Factory, Doha Plastic Company, Gulf Plastic Company, National Detergent Company, and Qatar Detergents Company. (Gulf- Times.com)

QA’s first A350 XWB completes maiden flight – The first Airbus A350-900 aircraft to be delivered to its launch-customer, Qatar Airways (QA), has completed its maiden flight at Airbus’ production and manufacturing facility in Toulouse (France). Following the successful flight, the extra wide-body aircraft will continue on its production phase before delivery by the year end. QA has placed 80 A350s on order, including 43 A350-900 and 37 of larger A350-1000 models. (Gulftimes.com)

Catalyst Qatar buys German tech firm Kunst Stoff – Catalyst Qatar, a company involved in the design & development of software applications and games, has acquired a German electronic media company, Kunst Stoff. Catalyst Qatar is one of

4. Page 4 of 7

the first private Qatari companies to invest in the technology sector. The company said it hopes to provide technical skills and specialized knowledge of technology, both uncommon in Qatar and the region. (Gulf-Times.com)

Qatar-German trade crosses €2bn – Qatar’s Minister of Economy & Commerce, HE Sheikh Ahmed bin Jassim bin Mohamed al-Thani said the volume of trade between Qatar and Germany is estimated at over €2bn, reflecting continued growth. Sheikh Ahmed observed that German investments in Qatar have increased and there are 27 German companies with 100% German ownership, in addition to 112 firms with joint Qatari- German capital. (GulfBase.com)

New operator sees growing demand for taxis in Qatar – Capital Taxis, the operator of Mowasalat’s latest taxi franchisee, has stressed that the demand for taxi services in the country has grown over the years and is expected to increase further in the coming years. Capital Taxis, whose grey-colored vehicles hit the roads recently, is run by Ibin Ajayan Group, a prominent automobile distributor in Qatar. Capital Taxis recently launched its first batch of 50 Skoda cars and it will add another 450 vehicles over the next few months. Skoda cars are distributed in the local market by Ibin Ajayan Group. (Gulf-Times.com)

International

Data on jobs, industrial output, consumer confidence show strength in US economy – The number of Americans filing new claims for jobless benefits fell to a 14-year low and the country’s industrial output rose sharply in September, which provided positive signals that helped ease fears over the economic outlook. The Labor Department said initial claims for state unemployment benefits dropped 23,000 to 264,000, the lowest level since 2000. A separate report from the Federal Reserve showed production at the nation's factories, mines and utilities advanced 1.0% in September, the biggest gain since November 2012. Meanwhile, consumer confidence in the US unexpectedly rose in October to the highest level in seven years, showing a brightening of moods as gas prices drop and the labor market gains traction. The Thomson Reuters/University of Michigan preliminary sentiment index for October increased to 86.4, the strongest since July 2007, from a final reading of 84.6 in September. The median projection in a Bloomberg survey of 67 economists called for 84. (Reuters, Bloomberg)

Fed considers using bank stress tests for crisis prevention – The US Federal Reserve is considering turning its annual health check for big banks into a tool that it could use to prevent a build-up of excessive financial risks. If deployed, the modified tests could force banks to retain billions of dollars that otherwise would have gone to shareholders. While the move would help cool off sectors at risk of overheating, it could spark the ire of bank executives, who complain of rising regulatory burdens. Since 2009, the Fed has conducted its stress tests on the largest US banks to judge whether they have enough capital to survive economic downturns. As the Fed ramps up its crisis- prevention ability, its officials are now discussing whether to shape the annual test to take aim at particular markets or sectors to address risks. Fed Chairperson Janet Yellen said the rising economic inequality in the US was not in keeping with American values and she hinted at a range of steps that could address it. (Reuters)

European banks to return €5.8bn in crisis loans; deflation hits peripheral Eurozone countries – European banks will return €5.82bn in crisis loans to the European Central Bank (ECB) next week after the central bank started offering lenders new four-year loans at cheap rates. This repayment is roughly the same as the €5.9bn banks repaid recently and beats the

€4.0bn sum expected by money market traders polled by Reuters. Banks are returning funds they took from the ECB in late 2011 and early 2012 to ride out a funding strain at the height of the debt crisis. Banks still hold about €309bn of the old crisis loans, and lenders are expected to move them into the new ECB loan facility before they mature in January and February. Meanwhile, deflation hit five peripheral Eurozone countries in September, as inflation slipped to its lowest for five years and exports faltered, offering little hope that the bloc will avoid its third recession in six years. While consumer inflation at 0.3% remained unchanged from Eurostat's September 30 estimate, Greece, Spain, Italy, Slovenia and Slovakia showed deflation due to persistently depressed household demand. With such a minimal cushion against deflation, calls on the ECB to consider US-style bond-buying, or quantitative easing, are likely to intensify. Deflation makes it even harder for the heavily indebted currency area to pay off borrowings that are a drag on growth. (Reuters)

China to inject $33bn three-month loans into banks – According to sources, China's central bank is set to inject about $32.66bn worth of three-month loans into five or six listed banks to maintain ample liquidity and support the slowing Chinese economy. The injection follows signs that Chinese investors are beginning to bet that the People’s Bank of China (PBoC) is going to reduce the official deposit rate, now fixed at 3%. This infusion came after a CNY500bn injection the PBoC made into China's top banks last month via its standard lending facility in the form of three-month loans. China has injected a net CNY44bn for the year through open market operations, compared with CNY113bn in 2013. However, it has begun to intensify its use of short-term facilities extended directly to banks in 2014, a method which some analysts criticize as being relatively opaque. (Reuters)

Regional

Ventures: GCC infrastructure contracts to top $45bn – According to a report by Ventures titled “GCC infrastructure Market 2014”, more than $45bn of infrastructure contracts will be awarded by the end of 2014, doubling over the $22.6bn awarded in 2012. The report gives a snapshot of the billions of dollars being spent across the region on five main areas – rail, roads, airports, ports and free trade zones. The report also stated that $97bn of rail contracts are already underway with all six GCC countries working toward completing the planned 2,117 kilometer GCC-wide rail network by 2018. Almost $300bn will be spent on airports in the Middle East over the next five years with passenger numbers among GCC countries expected to reach almost 4bn by 2017. Further, every GCC country is involved in expanding its seaports with an estimated $25bn of ports expansion and investments planned. (GulfBase.com)

IATA: Mideast aviation to grow at 4.9% until 2034 – According to the International Air Transport Association (IATA), Qatar, the UAE and Saudi Arabia will be the key drivers of the Middle Eastern air passenger market, which is expected to grow strongly at an average 4.9% until 2034. The UAE, Qatar and Saudi Arabia are set to enjoy strong growth of 5.6%, 4.8%, and 4.6% respectively and the total market size will be 383mn passengers. IATA projected that passenger numbers globally will reach 7.3bn by 2034. That represents a 4.1% average annual growth in demand for air connectivity, which will be more than double the 3.3bn passengers expected to travel in 2014. By 2034, the five fastest-growing markets will be China (856mn new passengers a year), the US (559mn), India (266mn), Indonesia (183mn) and Brazil (170mn). (GulfBase.com)

5. Page 5 of 7

MEED: New Gulf projects to hit $180bn in 2014 – According to a report by MEED Projects, about $180bn worth of contracts for new construction projects will be awarded in wealthy Gulf States in 2014, the largest amount for six years, despite falling oil prices. In 2013, $156bn worth of projects were awarded in the GCC region, largely by governments and state-backed companies, as most Gulf countries spent on major infrastructure projects designed to help their economies diversify beyond oil. At the peak of the boom in 2008, GCC contracts totaled about $200bn. The current concern for the construction industry is that oil prices could drop for an extended period below the break- even levels, which governments need to balance their budgets. (Reuters)

QNA: GCC a step closer to integration of capital markets – According to Qatar News Agency (QNA), GCC states are moving closer to having unified rules for listing of stocks and conventional and Islamic bonds on their equity exchanges as part of plans to integrate their capital markets. A MoU is likely to be signed by capital market regulators of the six member states at a meeting of the Ministerial Committee of GCC Capital Market Boards’ Chairmen, which is underway in Kuwait. Regulations for operation of mutual and other funds and launch of share promotions are also being unified as a part of the integration agenda. The integration will bolster in a big way investments in stocks, bonds, Sukuk and other instruments from within and outside the GCC region. (Peninsula Qatar)

ANB’s net profit rises 26.93% YoY in 3Q2014 – Arab National Bank (ANB) reported a net profit of SR747.9mn in 3Q2014 as compared to SR589.2mn in 3Q2013, reflecting a YoY increase of 26.93%. EPS as of September 30, 2014 amounted to SR2.25 as against SR1.99 a year earlier. The bank’s total assets stood at SR149.94bn at the end of September 2014 as against SR137.89bn a year ago. Loans & advances stood at SR96.045bn, while customer deposits stood at SR114.69bn. (Tadawul)

SABB reports 25.21% YoY rise in 3Q2014 net profit – The Saudi British Bank (SABB) reported a net profit of SR1.06bn in 3Q2014 as compared to SR845.78mn in 3Q2013, reflecting a YoY increase of 25.21%. EPS as of September 30, 2014 amounted to SR3.3 as against SR2.8 a year earlier. The bank’s total assets stood at SR182.96bn at the end of September 2014 as against SR166.28bn a year ago. Loans & advances stood at SR116.67bn, while customer deposits stood at SR143.69bn. (Tadawul)

NCB plans to convert completely into Islamic bank – National Commercial Bank’s (NCB) is planning to become a complete Islamic bank within a reasonable time as more than two-thirds of its business is already Shari’ah-compliant. NCB’s statement came amid the bank’s plans to sell shares on the Saudi Stock Exchange. The bank’s Shari’ah advisory council has declared the share offer to be acceptable under Islamic law. NCB’s prospectus says the bank will offer 300mn shares to the public at SR45 each, for a value of $3.6bn, while another 200mn shares will be allocated to the state pension agency, bringing the total to $6bn. (GulfBase.com)

ICD, SEAF sign MoU for SME financing – The Islamic Corporation for the Development of the Private Sector (ICD) has signed a MoU with US-based Small Enterprise Assistance Funds (SEAF) to foster the development of small & medium sized enterprises (SMEs) through the deployment of Shari’ah- compliant risk capital. Supporting this, ICD and SEAF are planning to establish country-focused SME funds in emerging and frontier markets of common interest, for encouraging private sector growth. In particular, ICD and SEAF will cooperate on

improving the feasibility of SME projects and enabling post- investment support for each portfolio investment and thereby the funds. ICD will also act as an advisor to the fund, including in regard to Islamic finance. (GulfBase.com)

Bawan signs SR550mn Islamic financing deal with SABB – Bawan Company has signed a contract for Islamic financing facilities in the form of Murabaha along with letters of credit for funding worth SR550mn through Saudi British Bank. The company intends to use the proceeds to finance working capital and the company’s expansion. The financing period ranges from month-to-month up to five years, which includes banking facilities accounting for 91% of the total with the remainder funding capital expansion and development. (GulfBase.com)

Maaden plans SR5.6bn capital increase – The Saudi Arabian Mining Company (Maaden) has invited its shareholders to attend the third EGM to be held on November 13, 2014 to approve board of director’s recommendation for increasing the company’s capital by SR5.6bn through the offering of rights issue. The offer price and the number of shares will be determined by the company during the EGM. The subscription to rights issue shares will be in accordance with the subscription terms set out in the prospectus approved by the Capital Market Authority (CMA). The rights will be issued to the shareholders who are registered at the end of the trading day of EGM. The objectives of the capital increase are to expand the company’s phosphate investment and to continue funding the aluminum projects specifically the Bauxite mine and Alumina refinery. (Tadawul)

ET concludes AED6mn contract with MAF Group – Emirates Transport (ET) has concluded a three-year contract worth AED6mn with Majid Al Futtaim (MAF) Group to provide shuttle services between 83 hotels and 5 of MAF’s malls in Dubai, Sharjah and Fujairah. (GulfBase.com)

Almaden to set up AED110mn facility in DSO – Dubai Silicon Oasis Authority (DSOA) has signed an agreement with Chinese solar firm Chang Zhou Almaden Limited (Almaden) to host its new AED110mn manufacturing and training facility in Dubai Silicon Oasis. Almaden will set up a 15,000 square meter factory in Dubai Silicon Oasis’ technology park. The facility is designed to produce up to 400,000 PV panels every year and will also host a training center for raising awareness on green energy and sustainable solutions in the MENA region. Set for completion in 1Q2015, the facility marks Almaden’s first entry into the MENA region. (GulfBase.com)

Damac signs exclusive deal with Paramount – Damac Properties has signed an exclusive deal with Paramount Hotels & Resorts to expand its branded hotels and serviced living concepts to new cities around the MENA region. The hotels & serviced residences will be launched over the next five years across Dubai, Abu Dhabi, Jeddah and Istanbul. The new agreement is a major expansion on the current deal, which has already seen four different projects announced in the UAE and Saudi Arabia. (GulfBase.com)

StanChart to abandon UAE portfolio sale – According to sources, Standard Chartered (StanChart) is no longer considering the sale of its $400mn portfolio in the UAE. (Bloomberg)

d3, Cisco sign MoU – Dubai Design District (d3) has signed a MoU with US-based Cisco to explore joint opportunities in deploying new smart services and applications in d3 based on Cisco’s Smart+Connected City solutions portfolio. (GulfBase.com)

6. Page 6 of 7

Atlantis signs enlarged $1.1bn loan deal – Atlantis, a Dubai- based hotel resort, has refinanced an $880mn loan to take advantage of favorable market conditions and secure a better interest rate, as well as reducing its borrowing cost. The hotel’s loan was also increased in size to $1.1bn. Reportedly, Atlantis' new seven-year loan will pay an interest rate of 375 basis points over the London interbank offered rate (Libor). The loan, which consisted of a $750mn conventional tranche and a $350mn piece compliant with Islamic finance principles, was provided by Dubai Islamic Bank, Emirates NBD, National Bank of Abu Dhabi and Standard Chartered. (Reuters)

Wasl launches Samari Community Retail Centre in Dubai – Wasl Properties announced the launch of Samari Retail Centre, a community center located at its residential project, Samari Residences. Surrounded by a mix of residential, commercial and leisure facilities, Samari Retail Centre is sited in close proximity to Dubai International Airport and Mushrif Park, a large recreational area of green space. (Bloomberg)

Adnec, MCI to strengthen partnership – Abu Dhabi National Exhibitions Company (Adnec) and MCI are in discussions to co- develop strategies that support the growth of Abu Dhabi as a global destination for the world’s leading MICE (meetings, incentives, conferences & events) industry events. (GulfBase.com)

Moody’s: NBK rating reflects dominant franchise, resilient core profitability – According to Moody’s latest credit opinion report, National Bank of Kuwait’s (NBK) rating (a long-term global local currency (GLC) deposit rating of Aa3) reflects its dominant domestic franchise, resilient core profitability, and robust financial fundamentals including consistently good asset quality metrics and strong capitalization. Moody’s stressed that NBK is well positioned to take advantage of new business opportunities as the Kuwaiti government’s development plan begins to gain traction in 2014 with more infrastructure projects being tendered than in previous years. Moody’s has recently affirmed NBK’s Aa3/ Prime- 1 long- and short-term deposit ratings and the bank’s C standalone bank financial strength rating (BFSR), equivalent to a baseline credit assessment of a3. The outlook on the ratings is stable. (GulfBase.com)

Kufpec launches $1bn loan – Kuwait Foreign Petroleum Exploration Company (Kufpec), a wholly-owned subsidiary of Kuwait Petroleum Corporation, has launched a $1bn loan into syndication. The deal is being led by a consortium of banks comprising Bank of Tokyo-Mitsubishi-UFJ, HSBC, JP Morgan, National Bank of Kuwait and Royal Bank of Scotland. The five- year amortizing term loan pays an interest margin of 130 basis points (bps) over Libor. (Reuters)

KCB loans hit KD7.14bn – Kuwait Credit Bank (KCB) has offered total loans amounting KD7.14bn since it was established till the end of July 2014, with 329,000 beneficiaries. (Bloomberg)

MEED: Oman’s projects opportunities at $26bn by 2015 – According to MEED Projects, Oman’s projects marketplace is set to receive a large boost as the Sultanate ramps up its investment in turnkey projects over the next few years. The year 2015 is expected to witness an influx of up to $26bn in capital expenditure and pipeline opportunities including the latest Duqm developments valued at $12.5bn and fisheries harbors valued at $13.6bn respectively. As much as $145bn worth of projects is currently under way or will be awarded in Oman. Among the projects at the forefront of Oman’s aggressive expansion program are: $26bn Khazzan & Makarem Fields projects, Suwaiq IWPP and Haima Solar Thermal Hybrid Power Plan. Furthermore, $13bn are to be invested in the Takamul downstream project and ORPIC’s Liwa Plastic Project Initiative

with another $12bn dedicated for the development of Duqm as the new energy, industrial, residential and tourism & leisure hub in Oman. (GulfBase.com)

Al Anwar sells 33.63% stake in TFC – Al Anwar Holding and its subsidiary have sold their entire stake of 33.63% in Taageer Finance Company (TFC) to Oman Investment Fund. (MSM)

7. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg, *$ adjusted returns.

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Sep-10 Sep-11 Sep-12 Sep-13 Sep-14

QE Index S&P Pan Arab S&P GCC

(3.6%)

(2.9%)

(1.7%)

(1.0%)

(3.3%)

(2.3%)

(4.9%)

(6.0%)

(5.0%)

(4.0%)

(3.0%)

(2.0%)

(1.0%)

0.0%

Saudi Arabia

Qatar

Kuwait

Bahrain

Oman

Abu Dhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD%

Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,238.32 (0.0) 1.2 2.7 DJ Industrial 16,380.41 1.6 (1.0) (1.2)

Silver/Ounce 17.26 (0.7) (0.7) (11.3) S&P 500 1,886.76 1.3 (1.0) 2.1

Crude Oil (Brent)/Barrel (FM

Future)

86.16 2.0 (4.5) (22.2) NASDAQ 100 4,258.44 1.0 (0.4) 2.0

Natural Gas (Henry

Hub)/MMBtu

3.72 (1.9) (3.5) (14.4) STOXX 600 318.68 2.4 0.1 (10.1)

LPG Propane (Arab Gulf)/Ton 91.00 (2.2) (4.2) (27.9) DAX 8,850.27 2.7 1.8 (14.3)

LPG Butane (Arab Gulf)/Ton 109.75 1.9 (3.5) (19.6) FTSE 100 6,310.29 2.0 (0.3) (9.2)

Euro 1.28 (0.4) 1.1 (7.1) CAC 40 4,033.18 2.49 0.0 (13.0)

Yen 106.88 0.5 (0.7) 1.5 Nikkei 14,532.51 (1.9) (4.0) (12.1)

GBP 1.61 0.0 0.1 (2.8) MSCI EM 976.76 0.6 (1.3) (2.6)

CHF 1.06 (0.4) 1.1 (5.7) SHANGHAI SE Composite 2,341.18 (0.5) (1.2) 9.4

AUD 0.87 (0.1) 0.7 (1.9) HANG SENG 23,023.21 0.5 (0.3) (1.3)

USD Index 85.11 0.2 (0.9) 6.3 BSE SENSEX 26,108.53 1.1 (0.8) 24.6

RUB 40.65 (0.5) 0.7 23.7 Bovespa 55,723.79 3.5 (0.7) 4.5

BRL 0.41 1.3 (1.0) (3.2) RTS 1,072.94 2.7 0.8 (25.6)

186.0

150.1

135.4