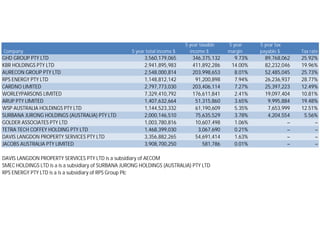

Corporate tax transparency: report of entity tax information

This data, which lists public and foreign entities (including foreign private companies) with total income of $100 million or more, as well as Australian-owned resident private entities with a total income of $200 million or more, is part of a much wider domestic and global focus on improved corporate transparency. It is intended to inform public debate about tax policy, particularly in relation to the corporate tax system.

There are legislative limits to the information in this report and it is important to note that the aggregate figures listed cannot reflect the complexity of the tax system, the calculations behind the numbers shown or the extent and nature of any ATO activity.

This entity by entity level report does not reflect actual economic or accounting groupings and we encourage all readers to refer to guidance material at ato.gov.au (link beneath) for a better understanding."

As the legislation does not allow for the reporting of an amount of zero or less these fields are left blank.

Confidentiality provisions prevent the ATO providing any additional information about particular taxpayers in the report. However, some entities may provide further context and explanation on their own websites, or in financial or tax reports.

More information: www.ato.gov.au/Tax_Transparency

Voluntary Tax Transparency Code:

https://www.ato.gov.au/Business/Large-business/In-detail/Tax-transparency/Voluntary-Tax-Transparency-Code/

7. Data source: https://data.gov.au/data/dataset/corporate-transparency

Corporate tax transparency: report of entity tax information

More information: www.ato.gov.au/Tax_Transparency

Voluntary Tax Transparency Code:

https://www.ato.gov.au/Business/Large-business/In-detail/Tax-transparency/Voluntary-Tax-Transparency-Code/

Confidentiality provisions prevent the ATO providing any additional information about particular taxpayers in the report. However, some entities may

provide further context and explanation on their own websites, or in financial or tax reports.

As the legislation does not allow for the reporting of an amount of zero or less these fields are left blank.

This data, which lists public and foreign entities (including foreign private companies) with total income of $100 million or more, as well as Australian-owned

resident private entities with a total income of $200 million or more, is part of a much wider domestic and global focus on improved corporate

transparency. It is intended to inform public debate about tax policy, particularly in relation to the corporate tax system.

There are legislative limits to the information in this report and it is important to note that the aggregate figures listed cannot reflect the complexity of the

tax system, the calculations behind the numbers shown or the extent and nature of any ATO activity.

This entity by entity level report does not reflect actual economic or accounting groupings and we encourage all readers to refer to guidance material at

ato.gov.au (link beneath) for a better understanding.