3. 3

Cost Allocation

Learning Objective 4: Understand criteria to guide cost-allocation decisions

Value Chain Analysis

VCA-Customer linkages

Learning Objective 1: Discuss why a company’s revenues and costs differ across customers

Learning Objective 2: Identify the importance of customer-profitability profiles

Learning Objective 3: Understand the cost-hierarchy-based operating income statement

Learning Objective 5: Discuss decision faced when collecting and allocating indirect costs to

customers

Sales Profitability Analysis

Learning Objective 6: Subdivide the sales-variance into the sales-mix variance and the sales-quantity

variance into the market share variance and the market size variance

Week 3: Learning objective summary

Cost Allocation Value Chain Analysis Sales Profitability Analysis

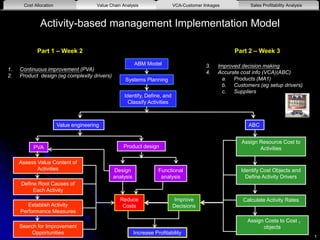

4. Activity-based management Implementation Model

5

ABM Model

Systems Planning

Identify, Define, and

Classify Activities

Reduce

Costs

Improve

Decisions

Increase Profitability

ABC

1. Continuous improvement (PVA)

2. Product design (eg complexity drivers)

3. Improved decision making

4. Accurate cost info (VCA)(ABC)

a. Products (MA1)

b. Customers (eg setup drivers)

c. Suppliers

PVA

Assess Value Content of

Activities

Define Root Causes of

Each Activity

Establish Activity

Performance Measures

Search for Improvement

Opportunities

Part 1 – Week 2 Part 2 – Week 3

Assign Resource Cost to

Activities

Identify Cost Objects and

Define Activity Drivers

Calculate Activity Rates

Assign Costs to Cost

objects

Product design

Value engineering

Design

analysis

Functional

analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

5

5. 6

1. What is Cost Allocation?

Assigning indirect costs to cost objects

These costs are not traced

Indirect costs often comprise a large percentage of Total Overall Costs

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Learning Objective 1:

Understand the criteria to guide cost-

allocation decisions. Identify four

purposes for allocating costs to cost

objectives

4(1&2)

6. 7

2. What are the purposes of cost allocation?

1

2

3

4

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

7. Purposes of Cost Allocation

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

8

8. 9

3. What are the criteria for cost allocations?

1

2

3

4

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

9. 10

Exercise: Criteria for Cost-allocation decisions

Cause and Effect

Benefits Received

Fairness (Equity)

Ability to Bear

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

10. 11

Exercise: Criteria for Cost-allocation decisions

The basis for establishing a price satisfactory to the government and

its suppliers

Most credible to operating managers

costs are allocated in proportion to the cost object’s ability to bear

them

Integral part of ABC

Generally, larger or more profitable objects receive proportionally more

of the allocated costs

Cost allocation here is viewed as a “reasonable” or “fair” means of

establishing selling price

the beneficiaries of the outputs of the cost object are charged with

costs in proportion to the benefits received

variables are identified that cause resources to be consumed

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

11. 12

Exercise: Criteria for Cost-allocation decisions

Cause and Effect

variables are identified that cause resources to be consumed

Most credible to operating managers

Integral part of ABC

Benefits Received

the beneficiaries of the outputs of the cost object are charged with costs in proportion

to the benefits received

Fairness (Equity)

the basis for establishing a price satisfactory to the government and its suppliers

Cost allocation here is viewed as a “reasonable” or “fair” means of establishing selling

price

Ability to Bear

costs are allocated in proportion to the cost object’s ability to bear them

Generally, larger or more profitable objects receive proportionally more of the

allocated costs

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

13. 14

Value Chain Analysis - Product Costing Definitions

Long-Term Pricing Decisions

Product-Mix Decisions

Life cycle product costing

Strategic Profitability Analysis

Short-Term Pricing Decisions

Product-Mix Decisions

Strategic Design Decisions

Tactical Profitability Analysis

Short-Term Pricing

Decisions

External Financial

Reporting

Production

Value-Chain Product Costs Operating Product Costs Traditional Product Costs

Production

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Research &

Development

Production

Marketing

Distribution

Outsourcing/suppliers

Customer service

Warranty claims

Design

Lawsuits

Learning Objective 3:

Understand the broader relevant costs

across the value chain and the

decisions impacted

(3)

14. 15

Profit and Loss Statement

Sales

Cost of Goods Sold

Begin Inventory

Cost of Goods Manufactured

Begin WIP

Total Manufacturing costs

Direct materials

Direct labor

Manufacturing overhead

Ending WIP

End Inventory

Gross Profit on Sales

Operating (period) expenses

Selling

Administration

Financing

Net Profit on Sales

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

15. 16

Customer

Profitability

Analysis

Customer

Revenue Analysis

Customer

Cost Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Learning Objective 1:

Discuss why a

company’s revenues

and costs differ

across customers

… revenues can differ

because of differences in

the quantity purchased

and the price discounts

while costs differ

because of different

demands placed on a

company’s resources

(P.572)

1(4)

16. 17

Customer Profitability Analysis

ABC/ABM product costing can be extended to customer profitability

analysis to identify the best customers

Customer profitability analysis focuses on selling, general, and

administrative costs

Customer profitability analysis analyzes activities, identifies proper cost

drivers, and determines realized profits from customers

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

17. 18

Customer Profitability Matrix

Companies do not have to target all types of customers in order to be successful. One way to think

about which customers to target is by using a customer profitability matrix.

Insert Exhibit 5.16

(Profitability Matrix)

Here

18

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

18. 19

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Managers are increasingly finding it important to:

https://www.youtube.com/watch?v=_IznwZYvrAE (Equation)

https://www.youtube.com/watch?v=EYboh3f6gsU (SAP)

The banking industry is changing and financial institutions are suffering

increasing pressures. To survive in an increasingly competitive market,

banks are forced to become more flexible, they must innovate to meet

customers' needs whose behaviors and expectations are changing.

Want to stay competitive in the eyes of your customer? How to

customize your service offerings to meet the changing needs of your

customers? By implementing a relationship-based and a la carte

pricing! Discover how a predictive analysis of your customer combined

with a flexible pricing engine allows you to set up the appropriate

service offerings and to reward customer's loyalty while maintaining

your profitability.

19. 20

1. E.g. raise prices for “demanders” or discount to gain more volume with low

“cost-to-serve” customers

2. Identify the most profitable customers

3. Providing better services to highly profitable customers (e.g. offer the

customer profit-positives service level options)

4. Securing highly profitable customers from competitors

5. Establish a surcharge for or re-pricing of expensive activities

6. Negotiating with customers to reach mutually beneficial levels of service

7. Choose various kinds of after-sale services to provide)

8. Abandon (reduce) products, services, or customers (e.g. conceding

permanent “loss customers” to competitors

9. Introduce new products and services

10. Manage each customer’s “costs-to-serve” to a lower level (e.g. Improve

their processes)

11. select the customer mix (e.g. shift the customer’s purchase mix toward

richer, higher-margin products and service lines)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Managers are increasingly finding it important to:

20. 21

Customer Profitability Analysis – Task 1

Customer profitability analysis allows managers to:

1. Strategic customer acquisition

2. Continuous improvement

3. Setting prices based on the cost to serve

4. Value added service management

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

21. 22

Customer Profitability Analysis – Task 1

Customer profitability analysis allows managers to:

1. Strategic customer acquisition

1. Identify the most profitable customers

2. Securing highly profitable customers from competitors

3. Abandon (reduce) products, services, or customers (e.g. conceding permanent “loss customers” to

competitors

2. Continuous improvement

1. Manage each customer’s “costs-to-serve” to a lower level (e.g. Improve their processes)

3. Setting prices based on the cost to serve

1. E.g. raise prices for “demanders” or discount to gain more volume with low “cost-to-serve” customers

2. Establish a surcharge for or re-pricing of expensive activities

4. Value added service management (i.e. choose various kinds of after-sale services to provide)

1. Select the customer mix (e.g. shift the customer’s purchase mix toward richer, higher-margin products and

service lines)

2. Introduce new products and services

3. Providing better services to highly profitable customers (e.g. offer the customer profit-positives service level

options)

4. Negotiating with customers to reach mutually beneficial levels of service

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

22. In practice #1: Banks - U.S. Millionaires Told

Go Away as Tax Evasion Rule Looms

“I don’t open U.S. accounts, period,” said Su Shan Tan, head

of private banking at Singapore-based DBS, Southeast Asia’s

largest lender, who described reg attitudes toward U.S.

clients as “Draconian.”

Bank of Singapore, the private-banking arm of Oversea-

Chinese Banking Corp. (OCBC), ranked strongest in the

world for the last two years by Bloomberg Markets magazine,

has turned away millions of dollars from Americans because

it doesn’t want to deal with the regulatory hassle, according

to Chief Executive Officer Renato de Guzman. The bank had

$32 billion under management as of the beginning of the

year.

http://www.bloomberg.com/news/2012-05-08/u-s-millionaires-told-go-away-as-

tax-evasion-rule-looms.html 23

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

23. 25

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

In practice #1: Customer stop light feedback indicators

Companies use stop lights to give instant feedback to service operators (phone operators) so as to

help them deal with the type of customer in the appropriate way.

24. 26

In practice #2: Oops, what happened here?

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

25. 27

In practice #2: Customer profitability in an Insurance company

Figure 1 occurs in virtually every customer profitability study ever done,

in which:

15 percent to 20 percent of the customers generate 100 percent (or

more) of the profits.

In this case,

1. the most profitable 40 percent of customers generate 130 percent of annual

profits;

2. the middle 55 percent of customers break even, and

3. the least profitable 5 percent of customers incur losses equal to 30 percent

of annual profits.

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

26. 28

In practice #2: Customer Profitability in an Insurance Company

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

27. 29

In practice #2: Customer profitability in an Insurance company –

decisions made

1. With its most profitable customers, the company worked harder to

ensure their continued loyalty and to generate more business from them.

2. For customers in the middle break-even group, it would improve its

processes to lower its cost of serving them.

3. It focused most of its attention on the 5 percent-loss customers, taking

actions to re-price services and asking them for more business in

higher-margin product lines. If the company could not transform these

customers into profitable ones by these actions, it was prepared to drop

the accounts.

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

29. Example 1: Customer Profitability Analysis –

Spring Distribution Co – Retail Channel (14th ed Exb14-5)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

31

30. Example 1: Customer Profitability Analysis

Spring Distribution Co – Retail & Wholesale Channel

(14th ed Exb14-6)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

32

31. Example 1: Customer Profitability Analysis Spring

Distribution Co – Retail Channel (14th ed Exb14-7)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

33

32. Example 1: Customer Profitability Analysis

(14th ed Exb14-8)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

34

34. 36

Customer Revenue Analysis

Customer revenue analysis considers all activities that affect the net

amount received from the customers

Customer revenue analysis traces prices and discounts (including sales

and cash discounts) to customers and identifies financing costs

associated with customer revenues

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

35. Example 2: Customer Profitability Analysis –

Astel Computers

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

37

36. Example 2: Customer Profitability Analysis –

Astel Computers

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

38

37. 39

Not all customers require the same type of activities. Examples

of customer-specific activities include:

order processing costs

billing, collection and payment processing costs

accounts receivable and carrying costs

customer service costs

return or allowance processing costs

restocking costs

selling and marketing costs

Customer Cost Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

38. 40

Customer cost analysis identifies activities and cost drivers to

service customers

Traditionally, these costs are hidden in the customer support,

marketing, and sales function

Customer cost can be classified into the following categories:

1. customer unit-level cost

2. customer batch-level cost (e.g. order size)

3. customer-sustaining cost (e.g. visits)

4. distribution-channel cost (e.g. commercial vs. retail)

5. sales-sustaining costs (e.g. maintaining firm sales capability)

Customer Cost Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

39. Example 2: Customer Profitability Analysis –

Astel Computers

Provalue division cost and cost driver information

(Exhibit 14-2)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

41

40. Example 2: Customer Profitability Analysis –

Astel Computers

Provalue quantity of cost drivers, select customers

Next, we must determine how much of each resource the various

customers consumed. That information is reported here.

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

42

41. Example 2: Customer Profitability Analysis –

Astel Computers

Customer-profitability analysis for provalue-

wholesale customers

Now that we’ve identified the activities that drive

costs and determined the usage for those

activities for our select customers, we can

calculate profitability by customer.

In this example, we’ll look at Provalue’s 4

wholesale customers and compare profitability.

14-43

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

42. Example 2: Customer Profitability Analysis –

Astel Computers

Looking at this chart, if you were the manager, what would you do?

(Exhibit 14-3)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

44

43. Customer profitability profiles are a useful tool for

managers.

Cumulative customer profitability profiles provide

information that shows what percentage of operating

income each additional customer contributes.

Customers are presented in order of contribution to

operating income so any customers in a loss position are

highlighted at the bottom of the analysis.

14-45

Example 2: Customer Profitability

Analysis – Astel Computers

Customer Profitability Profiles

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

2

Learning Objective 2:

Identify the importance

of customer-

profitability profiles

44. Example 2: Customer Profitability Analysis –

Astel Computers

Customer profitability profiles, cont’d

Customer profitability profiles can be presented in

graphical form as well as table form.

14-46

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

46. 48

What other factors need to be considered in evaluating

customer profitability?

1.

2.

3.

4.

5.

6.

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

47. 49

Other Factors in Evaluating Customer Profitability

Likelihood of customer retention

Potential for sales growth

Importance of having the firm as a customer for future sales

references

Long-run customer profitability

Increases in overall demand from having well-known customers

Ability to learn from customers

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

48. Example 2: Customer Profitability Analysis –

Astel Computers

Customer profitability profiles, concluded

Managers must explore ways to make unprofitable

customers profitable. When doing so, they should

include factors other than the current profitability level

including:

Likelihood of customer retention.

Potential for sales growth.

Long-run customer profitability.

Increases in overall demand from having well-known customers

(if applicable).

Ability to learn from customers.

14-50

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

49. 51

External Linkages - Issues to consider

Reward loyalty – Longer term customers are loyal customers

Growth opportunities – Small customers can grow into large customers

Reputation – Must judge the impact on firm reputation among community (e.g.

Citibank versus Hang Seng Bank in Hong Kong.)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

50. Cost hierarchy-based

operating income statement

We’ve assigned customer-level costs to customers

but what about corporate costs, R&D and design

costs, etc.

Customer actions do not influence these costs which

raises two important questions:

1. Should these costs be allocated to customers when

calculating customer profitability, and

2. If they are allocated, on what basis should they be allocated

given the weak cause-and-effect relationship between these

costs and customer actions?

14-52

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

3(6)

Learning Objective 3:

Apply the concept of

cost hierarchy to

customer costing

51. Cost hierarchy-based operating

income statement, concluded

Some managers and management accountants advocate

fully allocating all costs to customers and distribution

channels because all costs are incurred to support the

sales of products to customers.

Sometimes only those corporate and other costs that are

widely perceived as causally related to customer actions

or that provide explicit benefits to customer profitability

are allocated.

Let’s take a look at some criteria to guide cost

allocations.

14-53

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

52. Cost hierarchy-based operating income statement

Example 3: Astel Computers (Exhibit 14-6)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

54

53. Cost hierarchy-based operating income statement

Example 3: Astel Computers (Exhibit 14-7)

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

55

54. Fully allocated customer profitability

Recall that the first purpose of cost allocation is

to provide information for economic decisions,

such as pricing, by measuring the full costs of

delivering products to different customers

based on an ABC system.

Cost categories can be summarized into:

Corporate costs

Division costs

Channel costs.

14-56

5

Learning Objective 5:

Discuss decisions

faced when collecting

and allocating indirect

costs to customers

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

55. Overview diagram for allocation of corporate,

division and channel costs

Follow the arrows to determine how the costs are allocated:

14-57

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

56. Beginning with the last row in the prior screen, we continue

with the allocation.

14-58

Overview diagram for allocation of corporate,

division and channel costs, concluded

What issues, if any, should Astel’s management consider

as they accumulate and allocation these costs?

57. Issues in allocating corporate costs to

divisions/customers

Let’s take a look at two questions, then we’ll

contemplate the better answers:

1. When allocating corporate costs to divisions, should

a company allocate only costs that vary with division

activity or assign fixed costs as well?

2. When allocating costs to divisions, channels and

customers, how many cost pools should be used?

14-59

58. Issues in allocating corporate costs to

divisions/customers, concluded

Companies should look to their particular situations, but

the probable best answers to these questions are:

1. To make good long-run decisions, managers need

to know the cost of all resources (variable or fixed

in the short-run) required to sell products to

customers, taking into account only relevant costs

for the specific decision.

2. Managers must balance the benefit of using a

multiple cost-pool system against the cost of

implementing it. Advances in IT technology make it

more likely that a multiple cost-pool system will

pass the cost-benefit test.

14-60

59. What type of decision?

What type of decision?

What type of decision?

Sales Variance Analysis

61

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Learning outcome 6: Discuss why customer level costs differ across customers

6 (7&8)

SMA

60. 62

Level 1: Static-budget variance – the difference between an actual result

and the static-budgeted amount - Ouch!

– What happened?

– How much did we make vs. expected (budget)?

Level 2: Flexible-budget variance – the difference between an actual result

and the flexible-budgeted amount - Ouch!

– what happened?

- How much was due to change in contribution margin (rev – costs)?

Level 2: Sales-volume variance

- How much was due to change in volume?

Level 3: Sales Quantity variance

- How much was due to change in quantity?

Level 3: Sales Mix variance

- How much was due to change in mix?

Level 4: Market Size variance

- How much was due to change in market size?

Level 4: Market Share variance

- How much was due to change in market share?

Sales Variance Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

MA

61. 63

Measures shifts between selling more or less of higher or lower

profitable products

Budgeted

Sales-Mix

Percentage

Actual

Sales-Mix

Percentage

X

Budgeted

Contribution

Margin per Unit

Sales-Mix

Variance =

Actual

Units of

All

Products

Sold

X

Sales Variance Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Learning Objective 6:

Subdivide the sales-volume variance into the sales-mix

variance

…the variance arises because actual sales mix differs from

budgeted sales mix

and the sales-quantity variance

… this variance arises because actual total unit sales differ from

budgeted total unit sales (P.591)

7

62. 64

Budgeted

Units of all

Products

Sold

Actual

Units of All

Products

Sold

Budgeted

Contribution

Margin per Unit

Sales-

Quantity

Variance

=

Budgeted

Sales-Mix

Percentage

X X

Sales Variance Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

63. Level 2: Change in margin

Change in volume

Example: Flexible-budget and sales-volume variances

65

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

MA1

64. Level 3: Change in mix – Which product makes you more money? Did you

sell a higher or lower proportion of this product?

Change in volume

Example: Sales-mix and sales-quantity variances

66

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

7

65. What type of decision?

What type of decision?

What type of decision?

Sales Variance Analysis

67

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Learning outcome 6: Discuss why customer level costs differ across customers

7

8

MA1

66. 68

Budgeted

Market

Share

Actual

Market

Share

X

Budgeted

Contribution

Margin per

Composite Unit

for Budgeted

Mix

Market-

Share

Variance

=

Actual

Market

Size in

Units

X

Do you have control over this?

Market-share variance

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Learning Objective 6:

Subdivide the sales-

quantity variance into

the market-share

variance

…the variance arises

because actual market

share differs from

budgeted market share

and the market-size

variance

… this variance arises

because actual market

size differ from budgeted

market size

(P.591)

8

67. 69

Budgeted

Market

Size

Actual

Market

Size

Budgeted

Contribution

Margin per

Composite Unit

for Budgeted

Mix

Market-Size

Variance =

Budgeted

Market

Share

X X

1. Management can only change what they can control?

2. So the value of information is dependent on how well you separate out those

uncontrollable.

3. Do you have control over this?

Market-size variance

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

68. Which variance can you control?

Example: Market-share and Market-size variance

70

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

8

69. What type of decision?

What type of decision?

What type of decision?

Sales Variance Analysis

71

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

Learning outcome 6: Discuss why customer level costs differ across customers

7

8

MA1

70. 72

Cost Allocation

Learning Objective 4: Understand criteria to guide cost-allocation decisions

Value Chain Analysis

VCA-Customer linkages

Learning Objective 1: Discuss why a company’s revenues and costs differ across customers

Learning Objective 2: Identify the importance of customer-profitability profiles

Learning Objective 3: Understand the cost-hierarchy-based operating income statement

Learning Objective 5: Discuss decision faced when collecting and allocating indirect costs to

customers

Sales Profitability Analysis

Learning Objective 6: Subdivide the sales-variance into the sales-mix variance and the sales-quantity

variance into the market share variance and the market size variance

Week 3: Learning objective summary

Cost Allocation Value Chain Analysis Sales Profitability Analysis

75. 77

Customer Revenue Analysis

Customer revenue analysis considers all activities that affect

the net amount received from the customers

Customer revenue analysis traces prices and discounts

(including sales and cash discounts) to customers and identifies

financing costs associated with customer revenues

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

76. 78

Example 3: Customer Revenue Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

77. 79

Example 3: Customer Revenue Analysis

Insert Exhibit 5.18

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

79. 81

Not all customers require the same type of activities. Examples

of customer-specific activities include:

order processing costs

billing, collection and payment processing costs

accounts receivable and carrying costs

customer service costs

return or allowance processing costs

restocking costs

selling and marketing costs

Customer Cost Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

80. 82

Customer cost analysis identifies activities and cost drivers to service

customers

Traditionally, these costs are hidden in the customer support, marketing,

and sales function

Customer cost can be classified into the following categories:

1. customer unit-level cost

2. customer batch-level cost (e.g. order size)

3. customer-sustaining cost (e.g. visits)

4. distribution-channel cost (e.g. com vs. retail)

5. sales-sustaining costs (e.g. maintaining firm sales capability)

Customer Cost Analysis

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

81. 83

Example 3: Customer Cost Analysis

Insert Exhibit 5.19

(Customer-Related Activity)

Here

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

82. 84

Insert Exhibit 5.20

Example 3: Customer Cost Analysis

Which customer has higher batch level (order) activity costs?

Which customer has higher customer sustaining level (visits) activity costs?

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages

83. 85

Example 3: Customer Cost Analysis

Insert Exhibit 5.21

Cost Allocation Value Chain Analysis Sales Profitability AnalysisVCA-Customer linkages