1. Quick take

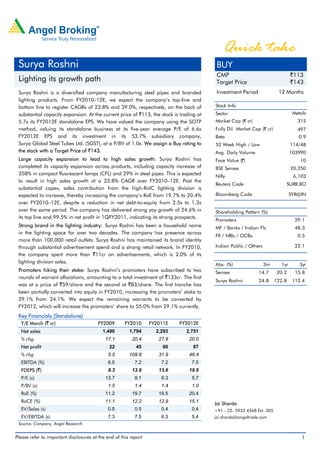

Surya Roshni BUY

CMP `113

Lighting its growth path Target Price `143

Surya Roshni is a diversified company manufacturing steel pipes and branded Investment Period 12 Months

lighting products. From FY2010–12E, we expect the company’s top-line and

bottom line to register CAGRs of 23.8% and 39.0%, respectively, on the back of Stock Info

substantial capacity expansion. At the current price of `113, the stock is trading at Sector Metals

5.7x its FY2012E standalone EPS. We have valued the company using the SOTP Market Cap (` cr) 315

method, valuing its standalone business at its five-year average P/E of 6.6x Fully Dil. Market Cap (` cr) 497

FY2012E EPS and its investment in its 53.7% subsidiary company, Beta 0.9

Surya Global Steel Tubes Ltd. (SGST), at a P/BV of 1.0x. We assign a Buy rating to 52 Week High / Low 114/48

the stock with a Target Price of `143. Avg. Daily Volume 103990

Large capacity expansion to lead to high sales growth: Surya Roshni has Face Value (`) 10

completed its capacity expansion across products, including capacity increase of BSE Sensex 20,250

358% in compact fluorescent lamps (CFL) and 29% in steel pipes. This is expected Nifty 6,103

to result in high sales growth at a 23.8% CAGR over FY2010–12E. Post the

Reuters Code SURR.BO

substantial capex, sales contribution from the high-RoIC lighting division is

expected to increase, thereby increasing the company’s RoE from 19.7% to 20.4% Bloomberg Code SYR@IN

over FY2010–12E, despite a reduction in net debt-to-equity from 2.5x to 1.3x

over the same period. The company has delivered strong yoy growth of 24.6% in Shareholding Pattern (%)

its top line and 99.5% in net profit in 1QFY2011, indicating its strong prospects.

Promoters 29.1

Strong brand in the lighting industry: Surya Roshni has been a household name MF / Banks / Indian Fls 48.3

in the lighting space for over two decades. The company has presence across

FII / NRIs / OCBs 0.5

more than 100,000 retail outlets. Surya Roshni has maintained its brand identity

through substantial advertisement spend and a strong retail network. In FY2010, Indian Public / Others 22.1

the company spent more than `11cr on advertisements, which is 2.0% of its

lighting division sales.

Abs. (%) 3m 1yr 3yr

Promoters hiking their stake: Surya Roshni’s promoters have subscribed to two Sensex 14.7 20.2 15.8

rounds of warrant allocations, amounting to a total investment of `133cr. The first

Surya Roshni 24.8 122.8 112.4

was at a price of `59/share and the second at `83/share. The first tranche has

been partially converted into equity in FY2010, increasing the promoters’ stake to

29.1% from 24.1%. We expect the remaining warrants to be converted by

FY2012, which will increase the promoters’ share to 55.0% from 29.1% currently.

Key Financials (Standalone)

Y/E March (` cr) FY2009 FY2010 FY2011E FY2012E

Net sales 1,490 1,794 2,293 2,751

% chg 17.1 20.4 27.8 20.0

Net profit 22 45 60 87

% chg 5.5 109.8 31.9 46.4

EBITDA (%) 6.5 7.2 7.2 7.5

FDEPS (`) 8.3 13.9 13.6 19.9

P/E (x) 13.7 8.1 8.3 5.7

P/BV (x) 1.5 1.4 1.4 1.0

RoE (%) 11.2 19.7 19.5 20.4

RoCE (%) 11.1 12.2 12.9 15.1 Jai Sharda

EV/Sales (x) 0.5 0.5 0.4 0.4 +91 - 22- 3952 4568 Ext. 305

EV/EBITDA (x) 7.3 7.5 6.3 5.4 jai.sharda@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Quick take

Surya Roshni

Investment arguments

Strong growth visibility

Substantial capacity expansion plans…

Surya Roshni is a diversified company having manufacturing presence in steel

tubes, cold rolled metal strips and the entire range of lighting products and

luminaries. The company has three manufacturing facilities—one in Kashipur

(Uttarakhand) for the lighting division, one in Bahadurgarh (Haryana) for the steel

division and one in Malanpur (Madhya Pradesh) that manufactures both lighting

and steel products.

In FY2010, Surya Roshni, under SGST, started a 200,000 tonne spiral pipe

manufacturing plant in Bhuj, Gujarat.

At its Kashipur facility, Surya Roshni recently expanded its manufacturing capacity

for a variety of products. Post the expansion, the company’s CFL manufacturing

capacity increased by 358.3% to 6.6cr pieces per annum (pcs p.a.). The capacity

for fluorescent tube lamps (FTL) expanded by 14.2% to 6.3cr pcs p.a. and that of

HPSV/HPMV lamps grew by 300.0% to 1.8mn pcs p.a. The company also

expanded its manufacturing capacity for components like glass shells.

Production at the company’s 11,000MT p.a. highmast facilty at Malanpur has

already started. Further, the company is planning to start production at its

72,000MT p.a. ERW pipes manufacturing facility in Malanpur.

Exhibit 1: Substantial capacity addition across products

Capacity Inc. in

Product capacity*

FY09 FY10 FY11E FY12E (%)

Pipes/Tubes (mt) 250,000 250,000 322,000 322,000 28.8

GLS lamps (cr) 18.7 18.7 18.7 18.7 -

Fluorescent tube lamps (cr) 5.5 6.3 6.3 6.3 14.2

HPSV/HPMV lamps (units) 450,000 1,800,000 1,800,000 1,800,000 300.0

CFL (cr) 1.4 6.6 6.6 6.6 358.3

PVC pipe (mt) - 17,500 17,500 17,500 NA

Highmast poles (mt) - - 11,000 11,000 NA

Source: Company, Angel Research; Note: *Increase in capacity over FY2009–12E

Surya Roshni has spent `224cr on Surya Roshni has spent `224cr on capex in FY2009 and FY2010. In comparison,

capex in FY2009 and FY2010. the total sales potential of the expanded capacity is `1,000cr, indicating the

In comparison, the total sales potential asset-light nature of the newly expanded capacity. As utilisation in the new facilities

of the expanded capacity is `1,000cr, increases, the company’s total asset-turnover is expected to increase from 2.4x to

indicating the asset-light nature of the 2.9x over FY2010–12E. Consequently, we expect the company’s RoE to rise from

newly expanded capacity 19.7% to 20.4% over FY2010–12E.

…to lead to strong top-line growth

Surya Roshni is poised for strong growth over the next few years, driven by

increased production from its expanded capacities across its product range.

We expect sales contribution from the lighting division to increase from 29.5% in

FY2010 to 33.6% in FY2012E.

October 8, 2010 2

3. Quick take

Surya Roshni

The lighting division is expected to witness The lighting division is expected to witness a 32.5% CAGR over FY2010–12E,

a CAGR of 32.5% over FY2010–12E, which is much higher than the estimated 20.5% CAGR for the steel division over

which is much higher than the estimated the same period. The lighting division’s growth is expected to be driven by higher

20.5% CAGR for the steel division over the sales in the fast-growing CFL segment. The company’s highmast poles facility is

same period also expected to start contributing to sales from FY2011. Growth in the steel

division is expected to be driven by the starting of production at the ERW pipes unit

in Malanpur.

Exhibit 2: CFL and highmast sales to drive lighting division’s growth

80.0

Contribution to Revenues (%) 71.2

70.0 64.2

60.0

53.3

47.7

50.0

40.0

28.8 42.0 39.9

30.0 35.8

20.0

12.5

10.0 4.7

0.0

FY09 FY10 FY11E FY12E

CFL Highmast Others

Source: Company, Angel Research

Overall, the company’s net revenue is expected to grow to `2,751cr in FY2012E

from `1,794cr in FY2010, registering a 23.8% CAGR over FY2010–12E. Robust

top-line growth (24.7% yoy) posted by the company in 1QFY2011 supports our

projections.

Exhibit 3: Revenue: Segmental and product-wise contribution

(` cr) FY07 FY08 FY09 FY10 FY11E FY12E

Lighting division sales 324 347 382 560 777 983

GLS lamps 112 106 106 123 126 129

Fluorescent tube lamps 122 120 103 108 114 121

CFL 19 43 110 200 326 392

Highmast poles - - - - 36 123

PVC pipes - - - - 28 59

Steel division sales 893 1,058 1,227 1,338 1,663 1,943

Pipes/Tubes 614 744 941 1,013 1,283 1,515

Overall gross sales 1,217 1,405 1,609 1,897 2,440 2,927

Overall Net Sales 1,099 1,272 1,490 1,794 2,293 2,751

Contribution to sales (%)

Lighting division 26.6 24.7 23.7 29.5 31.9 33.6

Steel division 73.4 75.3 76.3 70.5 68.1 66.4

Source: Company, Angel Research

October 8, 2010 3

4. Quick take

Surya Roshni

…and bottom-line growth

Surya Roshni’s overall margins are also The OPM of the company’s lighting division is much higher than that of the steel

expected to expand, since the division. Going ahead, since the contribution of the lighting division to the top line

contribution of the lighting division to is expected to increase, the company’s overall margins are also likely to expand.

the top line is expected to increase

We expect the company’s OPM to increase to 7.5% in FY2012E from 7.2% in

FY2010. In 1QFY2011, the company’s OPM improved by 40bp to 6.3% from

5.9% in 1QFY2010.

Exhibit 4: Overall EBITDA margin to increase

18.0

16.0 15.6 15.4

13.9 14.5 14.3 14.0 14.0

14.0

12.0

(%)

10.0

8.1 7.5

8.0 7.2 7.2 7.2

6.0 6.5

6.0

4.0 3.4 3.6

4.0 3.3 3.1 3.3 3.4

2.0

0.0

FY06 FY07 FY08 FY09 FY10 FY11E FY12E

Lighting Division OPM Steel Division OPM Overall OPM

Source: Company, Angel Research

Owing to strong top-line growth and an expansion in margins, we expect PAT to

grow at a 39.0% CAGR over FY2010–12E to `87cr. In 1QFY2011, net profit

nearly doubled to `8.4cr from `4.2cr in 1QFY2010.

Exhibit 5: PAT to grow at a 39.0% CAGR

100

90

80

70

(` cr)

60

50

40

30

20

10

0

FY06 FY07 FY08 FY09 FY10 FY11E FY12E

PAT

Source: Company, Angel Research

Strong brand name in the lighting space

Surya Roshni is a household name in the Indian lighting industry since the past two

decades. In the FTL and incandescent lamps segment, the company has historically

maintained a strong market share of over 20.0%. In FY2010, its market share was

~24.2% for both these products.

October 8, 2010 4

5. Quick take

Surya Roshni

Exhibit 6: Strong market share across lighting products

30.0

25.0

Market Share (%)

20.0

15.0

10.0

5.0

0.0

FY07 FY08 FY09 FY10 FY11E FY12E

CFL Flourescent Tube Lamps Incandescent Lamps

Source: Company, ELCOMA, Angel Research

In the CFL market, the company has increased its dominance as its market share

increased from 2.4% in FY2007 to 10.7% in FY2010. The company has already

become a bigger player than Bajaj Electricals in CFLs. We expect the company to

maintain its high growth rate in CFL sales on the back of high growth in

industry-wide CFL sales and further market share expansion.

CFL – Industry sales and Surya Roshni’s market share growth

We estimate the lighting industry’s total sales in volume terms across products to

continue growing at the historical growth rate of 5.9% p.a. In this, we expect the

special lamps category to grow at 15.8%, which is its historical growth rate.

However, there is no sales growth expected in the market for incandescent lamps

and FTL, as both these products are in a declining stage of their lifecycle, as they

are being replaced by CFLs, which are much better in terms of technology and

operating costs. The rest of the lighting industry’s growth is expected to come from

CFL. Hence, the estimated growth in the CFL industry over CY2009–11E is 24.8%.

Exhibit 7: CFL sales to grow at a 24.8% CAGR over CY209–11E

Volumes (cr pcs) CY06 CY07 CY08 CY09 CY10E CY11E CY12E

Incandescent lamps 75.7 77.9 73.4 76.6 76.6 76.6 76.6

Fluorescent lamps 18.6 19.0 18.6 17.9 17.9 17.9 17.9

CFL 10.0 14.0 19.9 25.5 32.4 39.7 47.4

Special lamps 1.4 1.7 2.1 1.8 2.1 2.4 2.8

Total 105.7 112.6 114.0 121.8 129.0 136.6 144.7

CFL growth rate (%) 49.3 40.0 42.1 28.1 27.1 22.5 19.4

Source: ELCOMA, Angel Research

We expect Surya Roshni’s market share in CFLs to increase to 14.0% by FY2012E

from 10.7% in FY2010, backed by higher advertisement spend and a strong retail

network.

October 8, 2010 5

6. Quick take

Surya Roshni

Exhibit 8: Surya Roshni likely to further increase market share in CFLs

CFLs (cr pcs) FY07 FY08 FY09 FY10 FY11E FY12E

Industry volume* 10.0 14.0 19.9 25.5 32.4 39.7

Surya Roshni’s volume 0.2 0.6 1.5 2.7 4.5 5.6

Market share (%) 2.4 4.0 7.4 10.7 14.0 14.0

Source: Company, Angel Research; Note:*Industry data for the corresponding calendar year

Surya Roshni’s products are available across the country at more than 100,000

retail outlets, which gives it a strong brand visibility. Further, management is

increasing its focus on advertising. In FY2010, the company spent ~2.0% of its

revenue from the lighting division on advertisement as compared to 0.6% in

FY2008. The higher allocation to advertisement expenses would further reinforce

the company’s brand presence among consumers.

Exhibit 9: Advertisement expense hiked in recent years

2.5 2.3

2.0 2.0

1.5 1.4

(%)

1.2 1.1

1.0

1.0

1.0

0.5

0.6

0.0

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10

Ad spend-to-Sales (Lighting division)

Source: Company, Angel Research

Promoters increasing their stake

The conversion of warrants is expected Surya Roshni’s promoters have issued two rounds of warrants, one of which has

to increase the promoters’ shareholding already been partially converted. In FY2010, in the first round, the company issued

to 55.0% from 29.1% currently 0.64cr warrants convertible at a price of `59/share, out of which 0.18cr warrants

were converted, thereby increasing the promoters’ stake to 29.1% from 24.1%

before the conversion. The second round of warrant allocation was carried out in

July 2010, where 1.14cr warrants were allocated to the promoters at a conversion

price of `83/share. We expect the remaining 0.46cr warrants of the first tranche of

warrants to be converted into equity shares in FY2011E. We expect the second

round of warrants also to be converted into equity shares by FY2012E. The

conversion of warrants is expected to increase the promoters’ shareholding to

55.0%, assuming there is no other change in the paid-up capital of the company.

October 8, 2010 6

7. Quick take

Surya Roshni

Exhibit 10: Promoters are increasing their stake

Conversion Amount Promoter shareholding (%)

Allocation date price invested Before Partial After

(`/share) (` cr) conversion conversion conversion

December14, 2009 59.0 24.1 29.1* 39.1

37.8

July 12, 2010 83.0 39.1 - 55.0

94.9

Source: Company, Angel Research; Note: *Current promoter shareholding

Financial outlook

Debt-to-Equity to reduce going ahead

Surya Roshni had net debt-to-equity of 2.5 in FY2010. However, owing to the

expected warrant conversion and lower capex requirements going ahead, we

expect this ratio to decline to 1.3x by FY2012E.

Exhibit 11: Net Debt/Equity expected to reduce going ahead

3.0

2.5

2.5 2.2 2.1

2.2 2.2

1.9

2.0

(x)

1.5 1.3

1.0

0.5

0.0

FY06 FY07 FY08 FY09 FY10 FY11E FY12E

Net Debt-to-Equity

Source: Company, Angel Research

Tax benefits to continue

Surya Roshni’s Kashipur unit is exempt from income tax, as it is located in

Uttaranchal, where it gets tax benefits due to local regulations. This unit is also

exempt from excise duty for a 10-year period, starting from the commissioning of

any capacity. As a result, the company’s effective tax rate has reduced from 35.4%

in FY2007 to 16.0% in FY2010. The newly added capacity in the Kashipur unit

would also enjoy these tax advantages. However, this benefit would be balanced

by the capacity expansion in the highmast and steel manufacturing units in the

non-tax exempt zone. Therefore, we expect the tax rate to remain at the current

levels of ~16.0% in FY2011E, before increasing marginally to 18.0% in FY2012E.

October 8, 2010 7

8. Quick take

Surya Roshni

Valuation

Currently, Surya Roshni is trading at 5.7x and 1.0x its FY2012E EPS and book

value, respectively. Historically, the company has traded in the range of 3.4x to

9.5x its one-year forward EPS, with the average of 6.6x one-year forward EPS.

We have valued the company using the SOTP method, valuing the standalone

business at 6.6x FY2012E EPS of `19.9 and valuing its investment in SGST at 1.0x

its FY2010 BV. We assign a Buy rating to the stock with a Target Price of `143.

Exhibit 12: One-year forward P/E band

250

200

150

(`)

100

50

0

Apr-02 Apr-03 Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

Price 2x 4x 6x 8x 10x 12x

Source: Company, Bloomberg, Angel Research

Exhibit 13: Peer comparison

Company Mcap CMP P/E (x) P/BV (x) RoE (%) CAGR (2010–12E)

(` cr) (`cr) (`) FY11E FY12E FY11E FY12E FY11E FY12E Sales PAT

Surya Roshni 315 113 8.3 5.7 1.4 1.0 19.5 20.4 23.8 39.0

Bajaj Electricals 3,263 333 19.7 15.9 5.2 4.1 30.3 29.6 20.6 32.1

Jindal Saw 5,850 212 12.0 10.0 1.5 1.3 14.2 14.0 9.2 34.9

Source: Company, Bloomberg, Angel Research

October 8, 2010 8

13. Quick take

Surya Roshni

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Surya Roshni

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

October 8, 2010 13

14. Quick take

Surya Roshni

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel: (022) 3952 4568 / 4040 3800

Research Team

Fundamental:

Sarabjit Kour Nangra VP-Research, Pharmaceutical sarabjit@angelbroking.com

Vaibhav Agrawal VP-Research, Banking vaibhav.agrawal@angelbroking.com

Vaishali Jajoo Automobile vaishali.jajoo@angelbroking.com

Shailesh Kanani Infrastructure, Real Estate shailesh.kanani@angelbroking.com

Anand Shah FMCG, Media anand.shah@angelbroking.com

Deepak Pareek Oil & Gas deepak.pareek@angelbroking.com

Sushant Dalmia Pharmaceutical sushant.dalmia@angelbroking.com

Rupesh Sankhe Cement, Power rupeshd.sankhe@angelbroking.com

Param Desai Real Estate, Logistics, Shipping paramv.desai@angelbroking.com

Sageraj Bariya Fertiliser, Mid-cap sageraj.bariya@angelbroking.com

Viraj Nadkarni Retail, Hotels, Mid-cap virajm.nadkarni@angelbroking.com

Paresh Jain Metals & Mining pareshn.jain@angelbroking.com

Amit Rane Banking amitn.rane@angelbroking.com

John Perinchery Capital Goods john.perinchery@angelbroking.com

Srishti Anand IT, Telecom srishti.anand@angelbroking.com

Jai Sharda Mid-cap jai.sharda@angelbroking.com

Sharan Lillaney Mid-cap sharanb.lillaney@angelbroking.com

Naitik Mody Mid-cap naitiky.mody@angelbroking.com

Amit Vora Research Associate (Oil & Gas) amit.vora@angelbroking.com

V Srinivasan Research Associate (Cement, Power) v.srinivasan@angelbroking.com

Mihir Salot Research Associate (Logistics, Shipping) mihirr.salot@angelbroking.com

Chitrangda Kapur Research Associate (FMCG, Media) chitrangdar.kapur@angelbroking.com

Pooja Jain Research Associate (Metals & Mining) pooja.j@angelbroking.com

Yaresh Kothari Research Associate (Automobile) yareshb.kothari@angelbroking.com

Shrinivas Bhutda Research Associate (Banking) shrinivas.bhutda@angelbroking.com

Sreekanth P.V.S Research Associate (FMCG, Media) sreekanth.s@angelbroking.com

Hemang Thaker Research Associate (Capital Goods) hemang.thaker@angelbroking.com

Nitin Arora Research Associate (Infra, Real Estate) nitin.arora@angelbroking.com

Technicals:

Shardul Kulkarni Sr. Technical Analyst shardul.kulkarni@angelbroking.com

Mileen Vasudeo Technical Analyst vasudeo.kamalakant@angelbroking.com

Derivatives:

Siddarth Bhamre Head - Derivatives siddarth.bhamre@angelbroking.com

Jaya Agarwal Derivative Analyst jaya.agarwal@angelbroking.com

Institutional Sales Team:

Mayuresh Joshi VP - Institutional Sales mayuresh.joshi@angelbroking.com

Abhimanyu Sofat AVP - Institutional Sales abhimanyu.sofat@angelbroking.com

Nitesh Jalan Sr. Manager niteshk.jalan@angelbroking.com

Pranav Modi Sr. Manager pranavs.modi@angelbroking.com

Sandeep Jangir Sr. Manager sandeepp.jangir@angelbroking.com

Ganesh Iyer Sr. Manager ganeshb.Iyer@angelbroking.com

Jay Harsora Sr. Dealer jayr.harsora@angelbroking.com

Meenakshi Chavan Dealer meenakshis.chavan@angelbroking.com

Gaurang Tisani Dealer gaurangp.tisani@angelbroking.com

Production Team:

Bharathi Shetty Research Editor bharathi.shetty@angelbroking.com

Simran Kaur Research Editor simran.kaur@angelbroking.com

Bharat Patil Production bharat.patil@angelbroking.com

Dilip Patel Production dilipm.patel@angelbroking.com

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE: INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM / CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

October 8, 2010 14