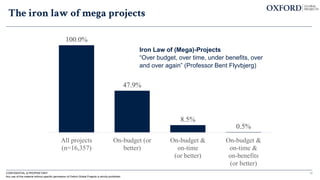

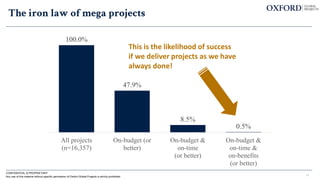

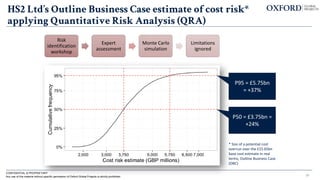

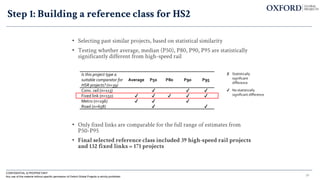

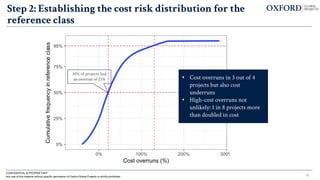

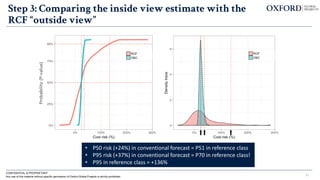

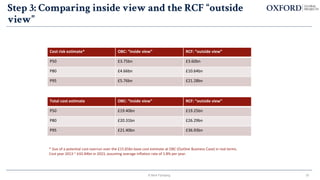

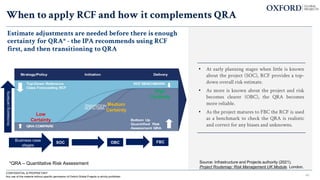

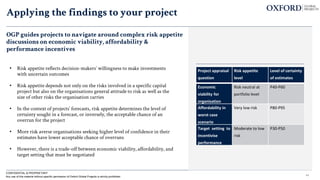

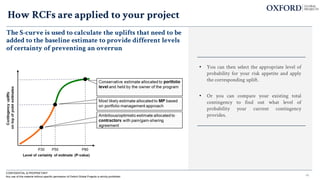

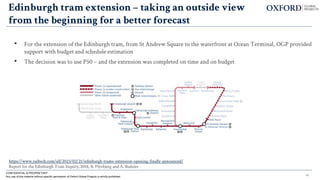

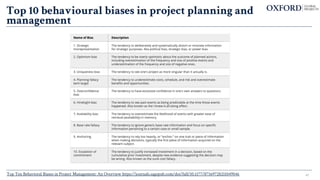

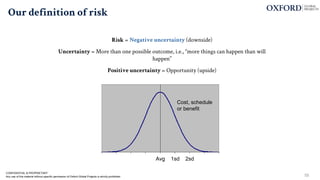

The document discusses the use of Reference Class Forecasting (RCF) as a method to improve the accuracy of cost and risk estimates for mega projects, which are crucial for achieving net zero targets. It highlights the common pitfalls of predicting project outcomes, such as optimism bias and strategic misrepresentation, and provides case studies showing the importance of using data from similar past projects to inform forecasts. The presentation concludes with practical steps for applying RCF and addressing misconceptions about its methodology.

![A planner on cost underestimation

“…as a planner, you will often know the real

costs. You know that the budget is too low, but it

is difficult to pass such a message to the

counsellors [politicians] and the private actors.

They know that high costs reduce the chances

of national funding.”

18

CONFIDENTIAL & PROPRIETARY

Any use of this material without specific permission of Oxford Global Projects is strictly prohibited](https://image.slidesharecdn.com/apmtalkoct2023slides-231019104454-b4e7cd99/85/Reference-Class-Forecasting-useful-method-or-random-number-generator-webinar-18-320.jpg)

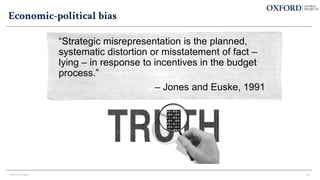

![56

M+ Museum in Hong Kong

• Hong Kong's M+ Museum (set opening date at RCF80;

managed to hit that target).

• From an initial HK$21.6 billion ($2.75 billion) to more

than HK$47.1 billion ($6 billion) after a reevaluation in

2013 and almost HK$70 billion ($8.91 billion) in 2021.

(M+ itself had an initial cost of HK$5.9 billion [$750

million] that city authorities confirmed has been

exceeded). On a broader scale, despite the district’s built

progress, there is still a lack of clear proposed public

policy that would foster local art production, a void

which paints the scheme as tourism-oriented rather than

for the benefit of the city’s arts scene.

CONFIDENTIAL & PROPRIETARY

Any use of this material without specific permission of Oxford Global Projects is strictly prohibited

https://www.scmp.com/news/hong-kong/hong-kong-economy/article/3103507/head-hong-kongs-west-kowloon-cultural-district](https://image.slidesharecdn.com/apmtalkoct2023slides-231019104454-b4e7cd99/85/Reference-Class-Forecasting-useful-method-or-random-number-generator-webinar-56-320.jpg)