Downloaded 3,371 times

![WHAT?

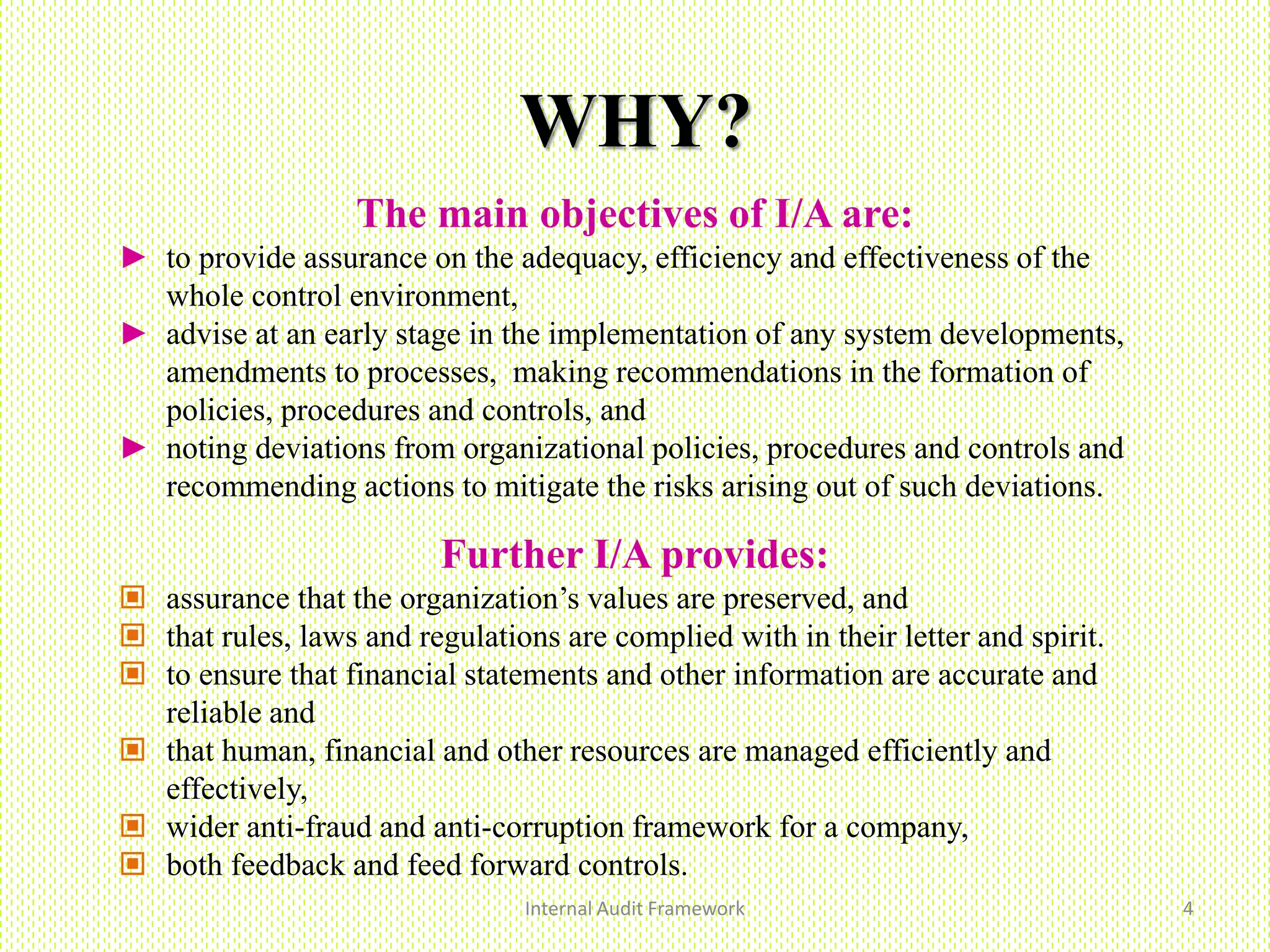

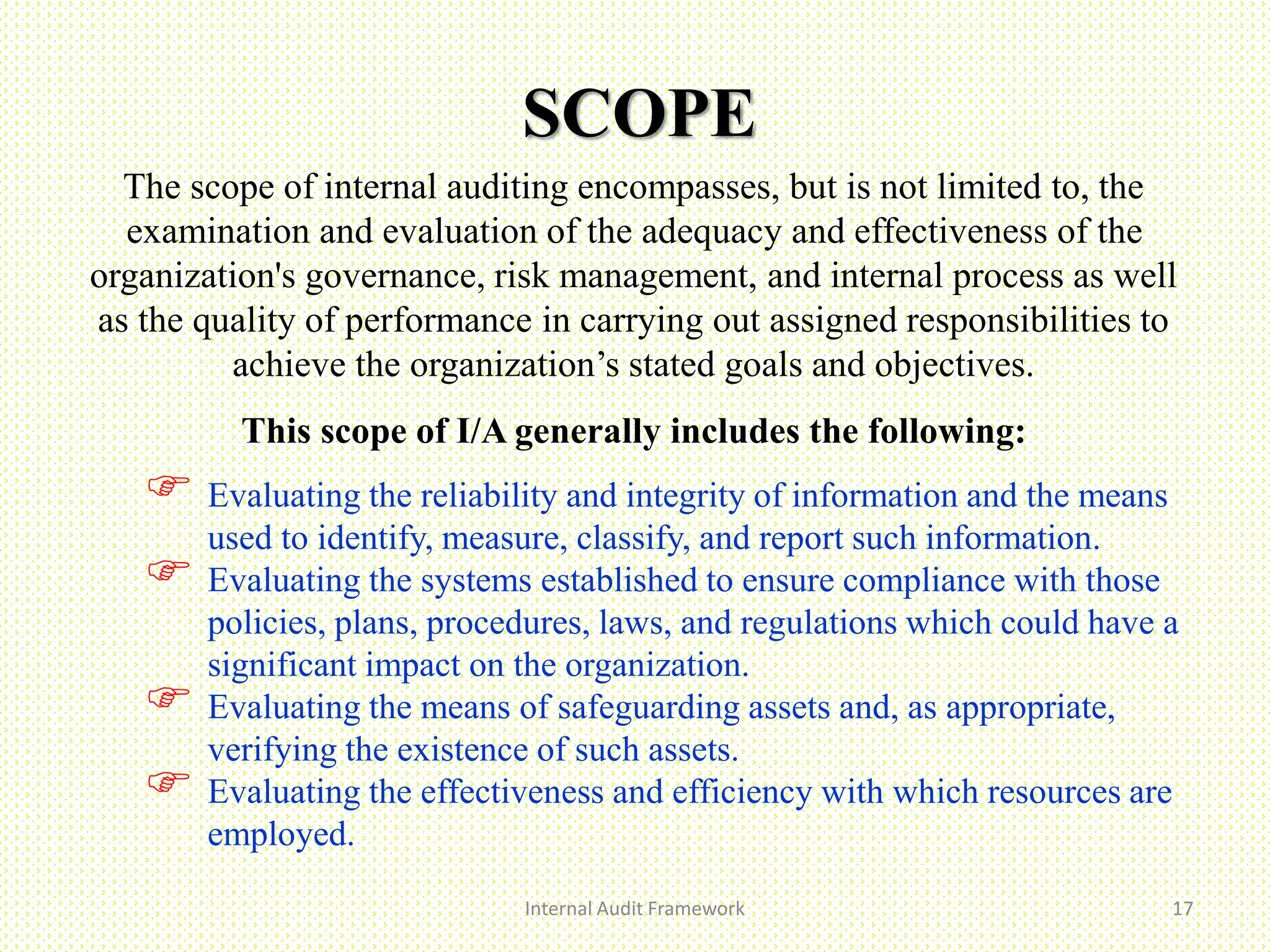

Internal auditing is an independent, objective assurance

and consulting activity designed to add value and

improve an organization's operations. It helps an

organization accomplish its objectives by bringing a

systematic, disciplined approach to evaluate and

improve the effectiveness of risk management, control,

and governance processes.

[The Institute of Internal Auditors, USA]

Remember,

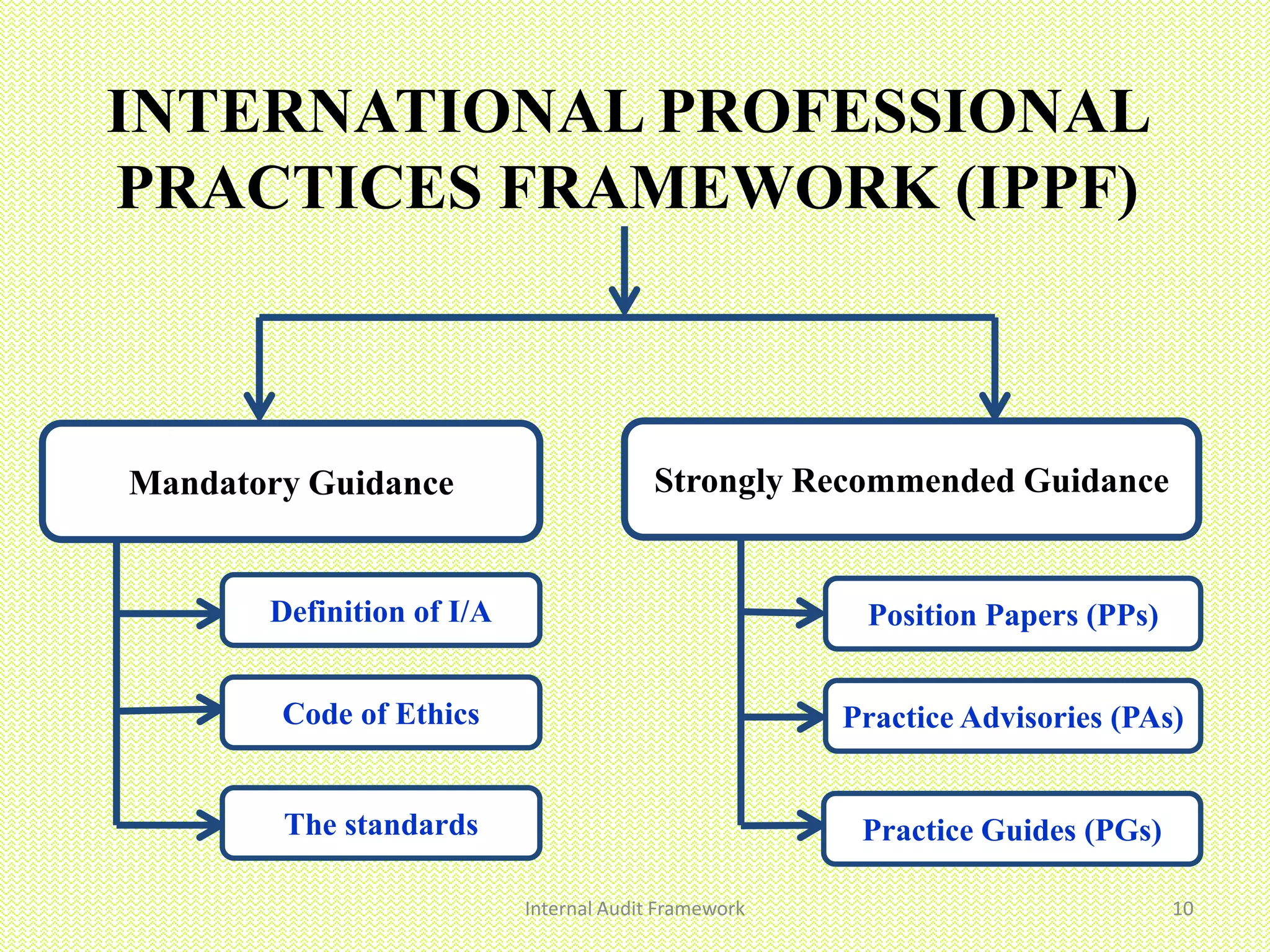

The definition of I/A provides comprehensive guidelines for the framework of

internal audit. It should always be kept in mind while I/A work is being carried out.

It helps in devising the complete internal audit approach.

Internal Audit Framework 3](https://image.slidesharecdn.com/internalaudit-140511003829-phpapp02/75/The-Internal-Audit-Framework-3-2048.jpg)

The document outlines the internal audit framework which serves as a systematic approach for organizations to evaluate and improve risk management, control, and governance processes. It details the roles and responsibilities of internal auditors, the types of audits, and emphasizes the importance of independence and objectivity. Additionally, it includes guidance on risk management processes, audit planning, and how the internal audit team contributes to the overall governance structure of the organization.