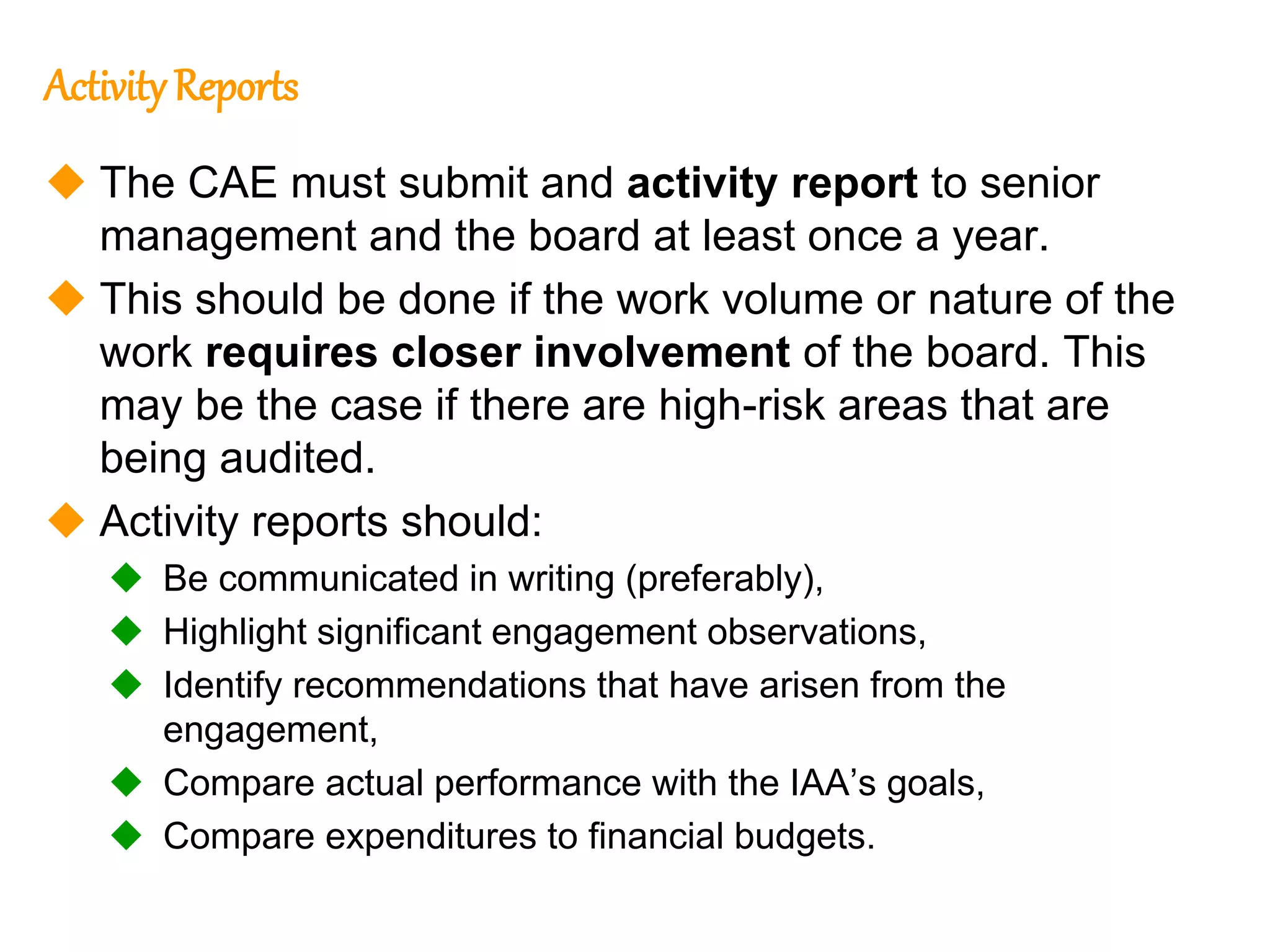

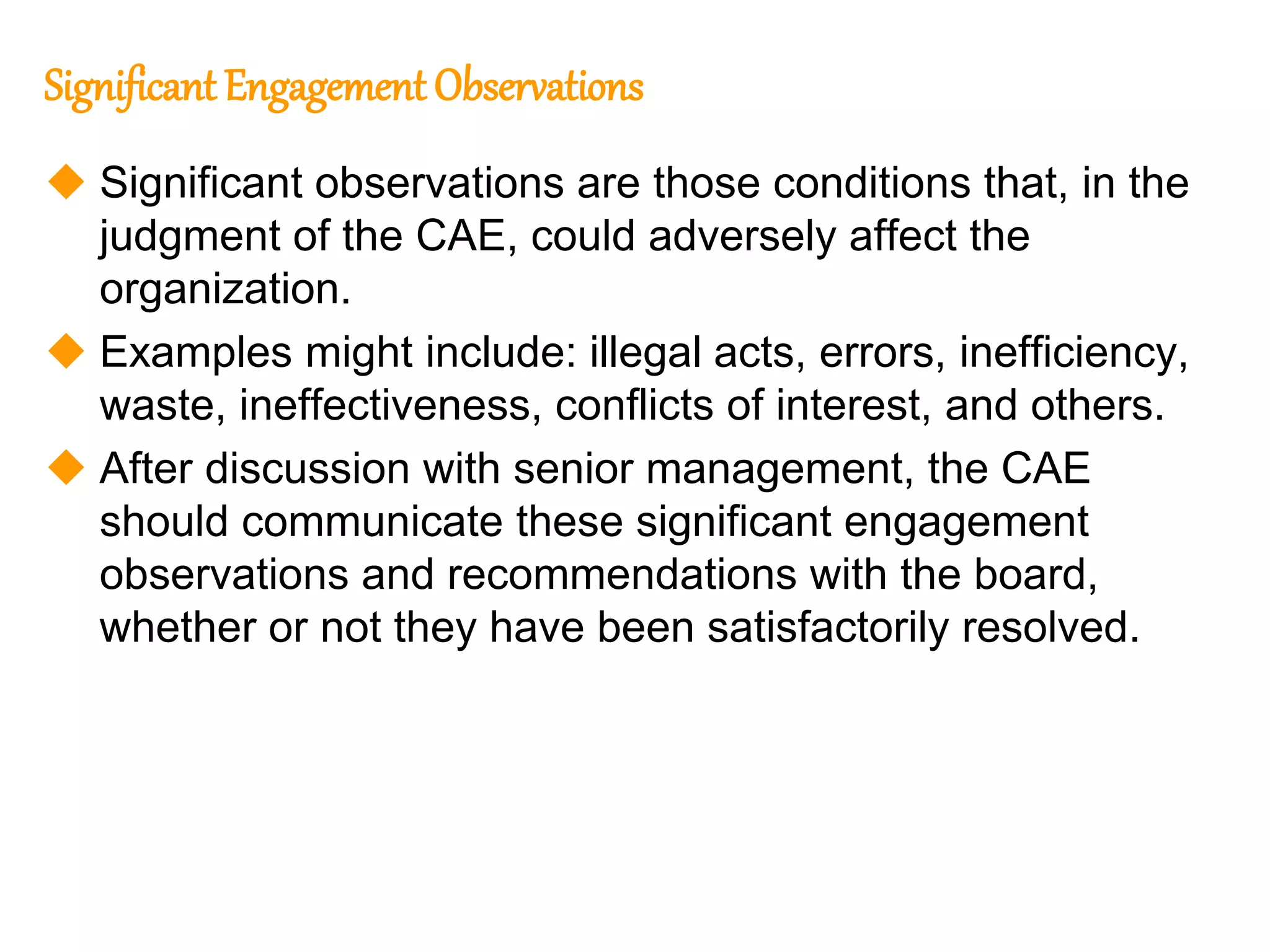

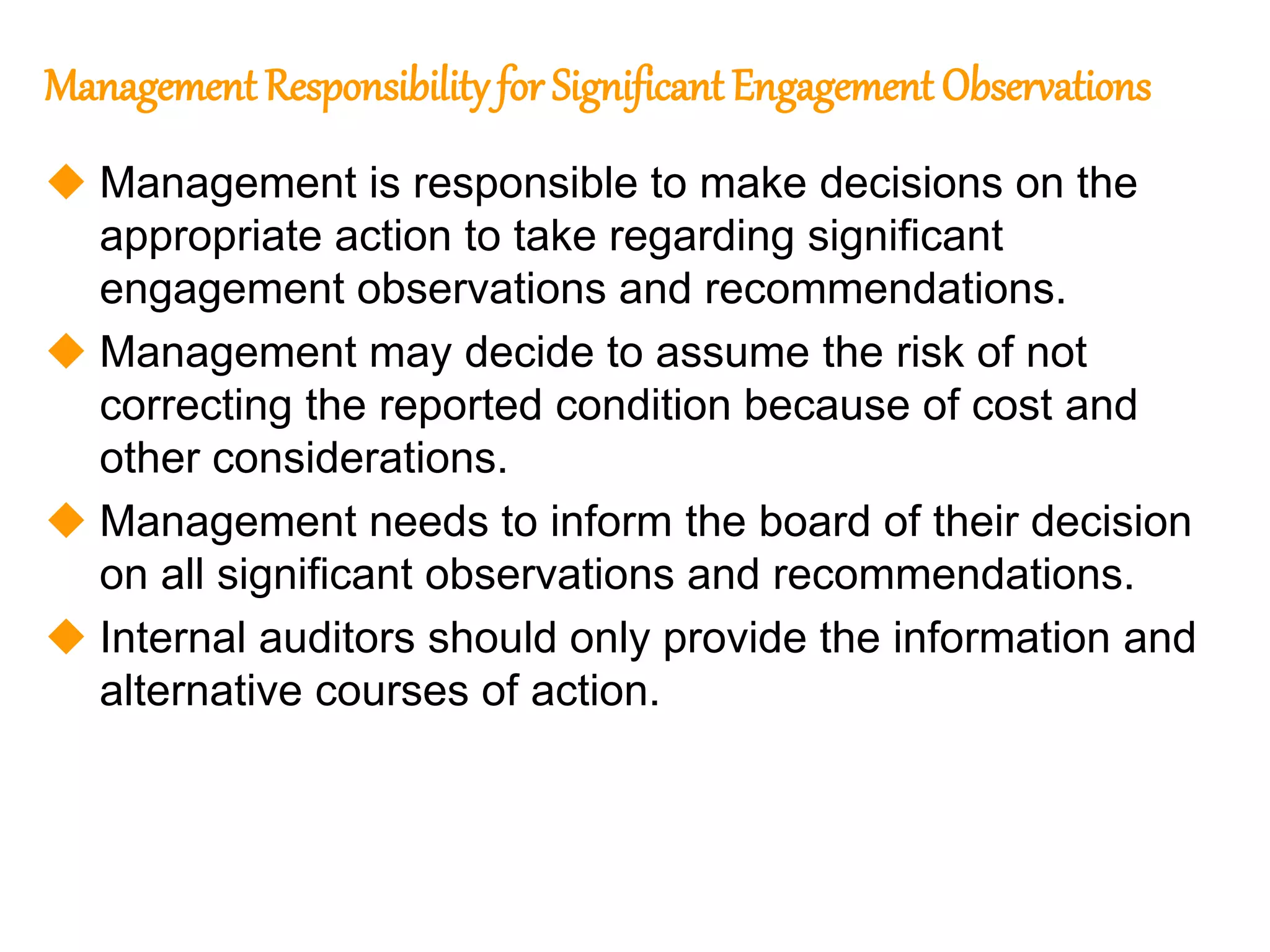

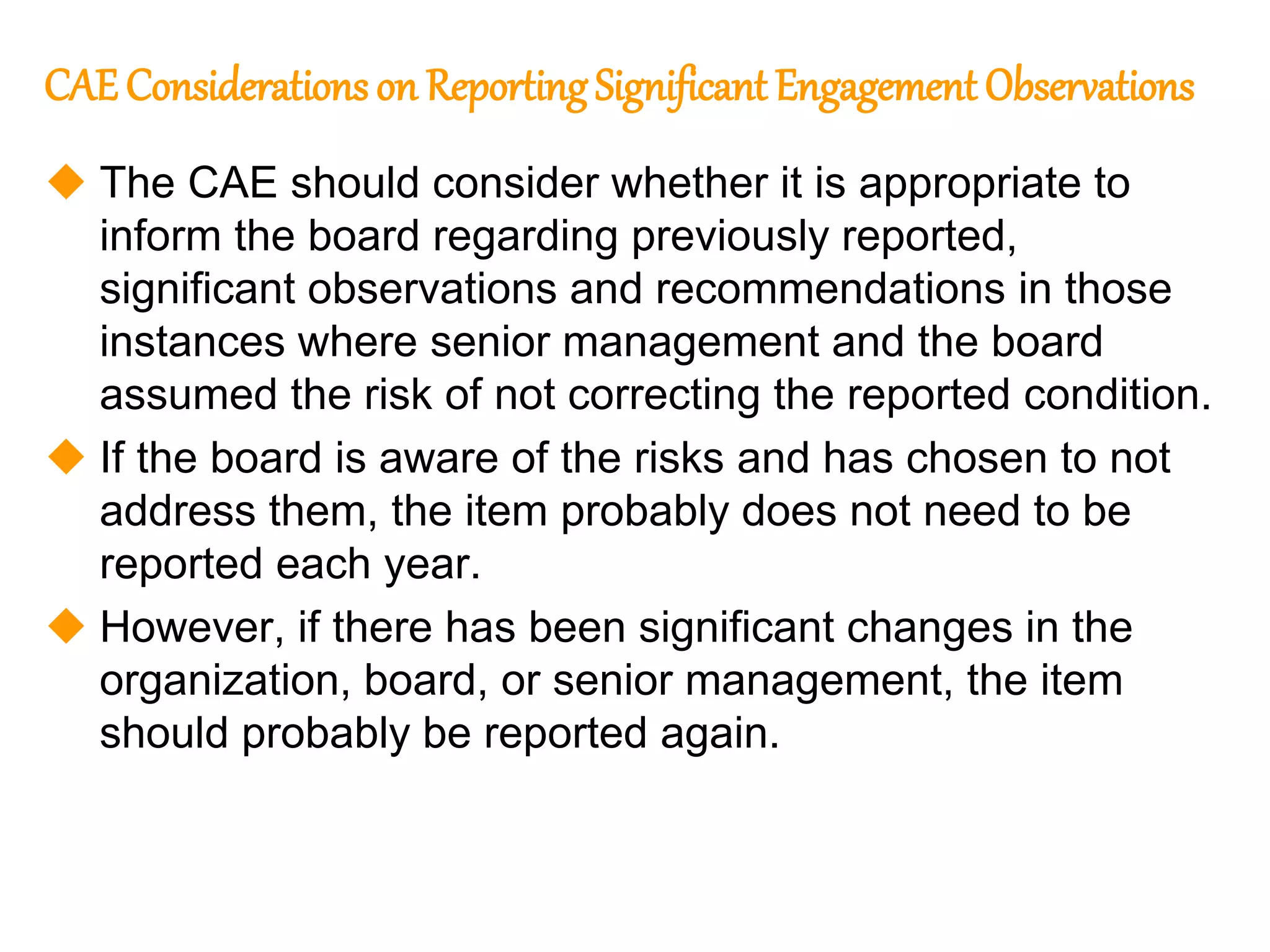

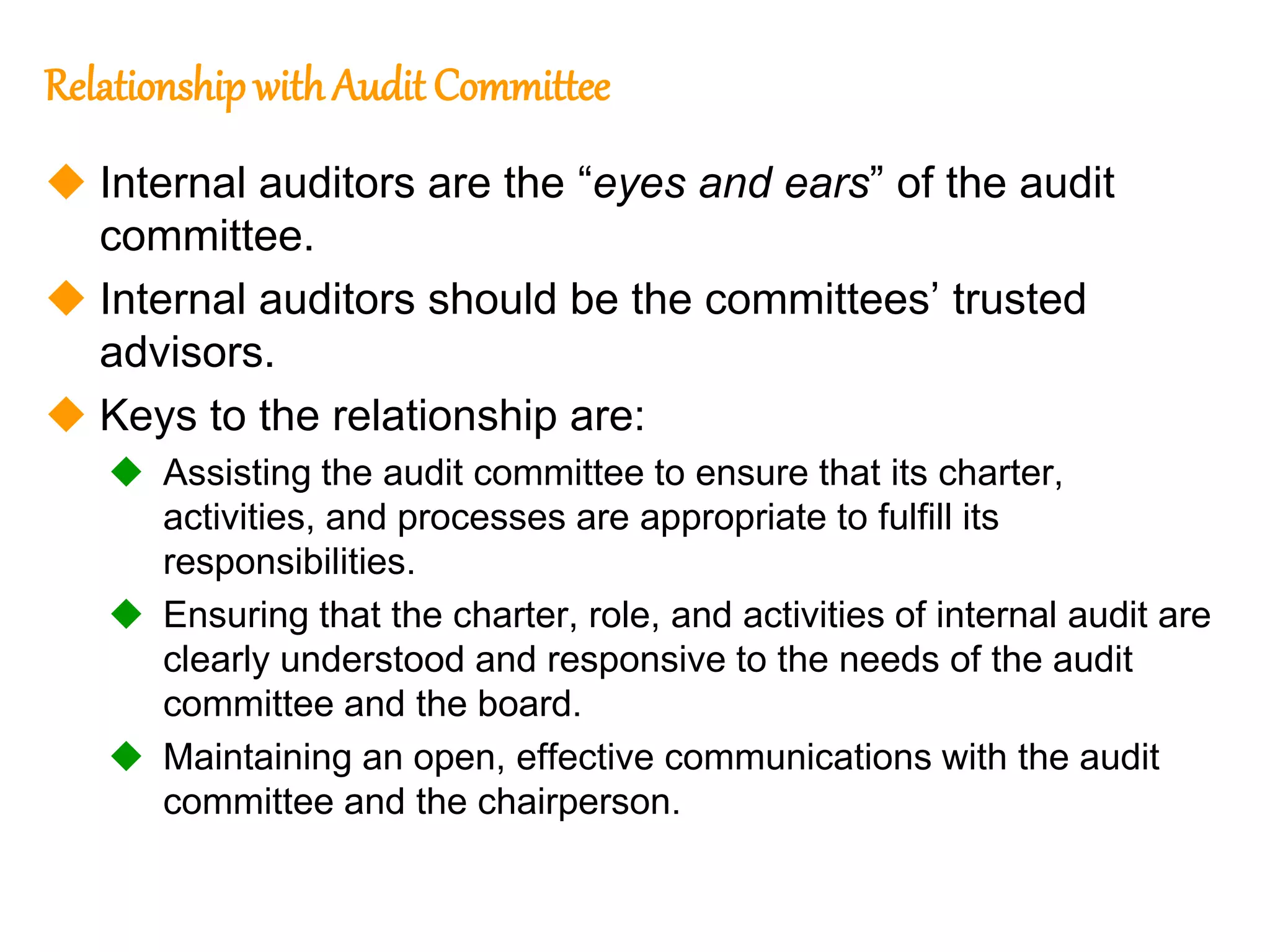

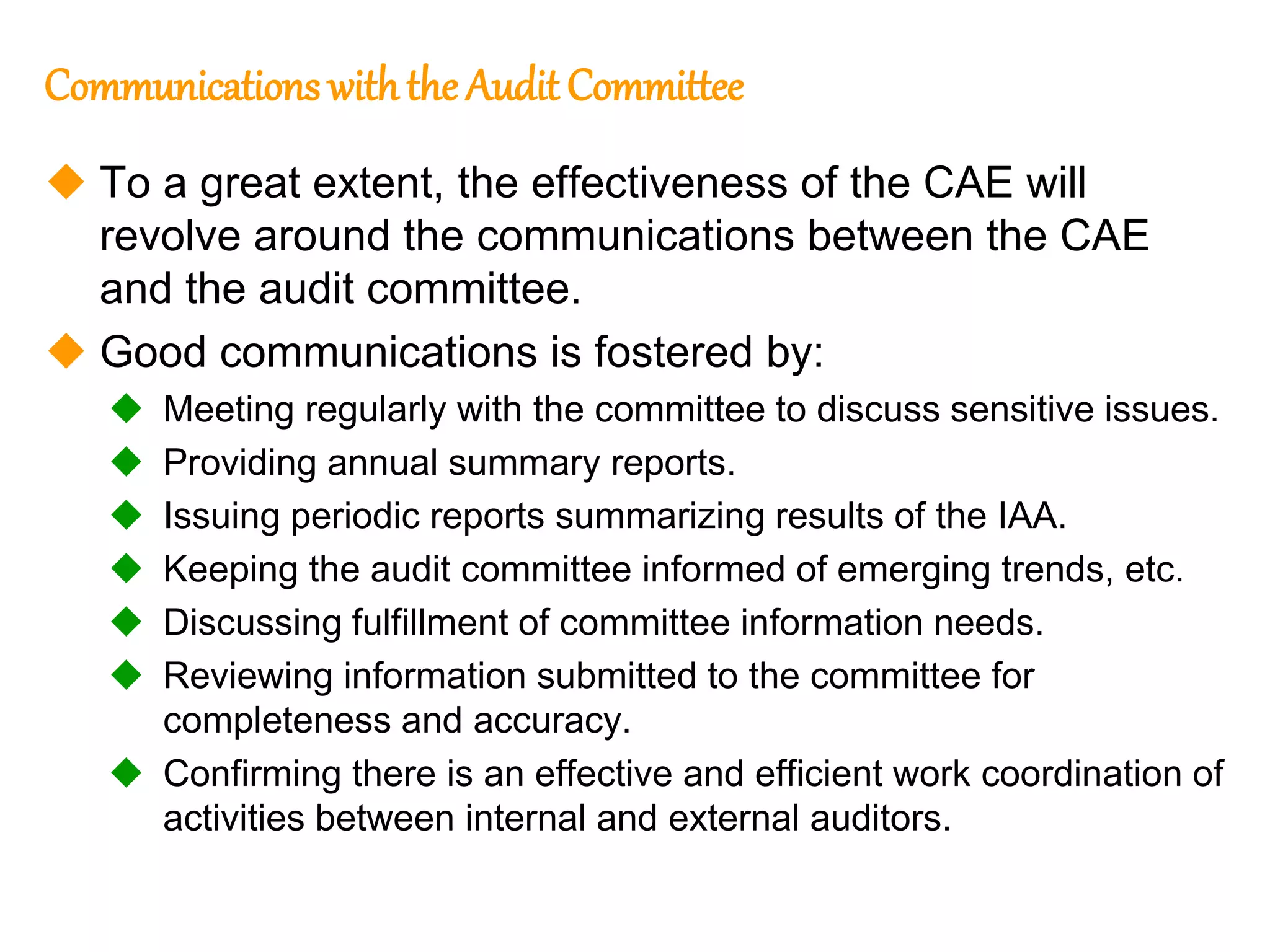

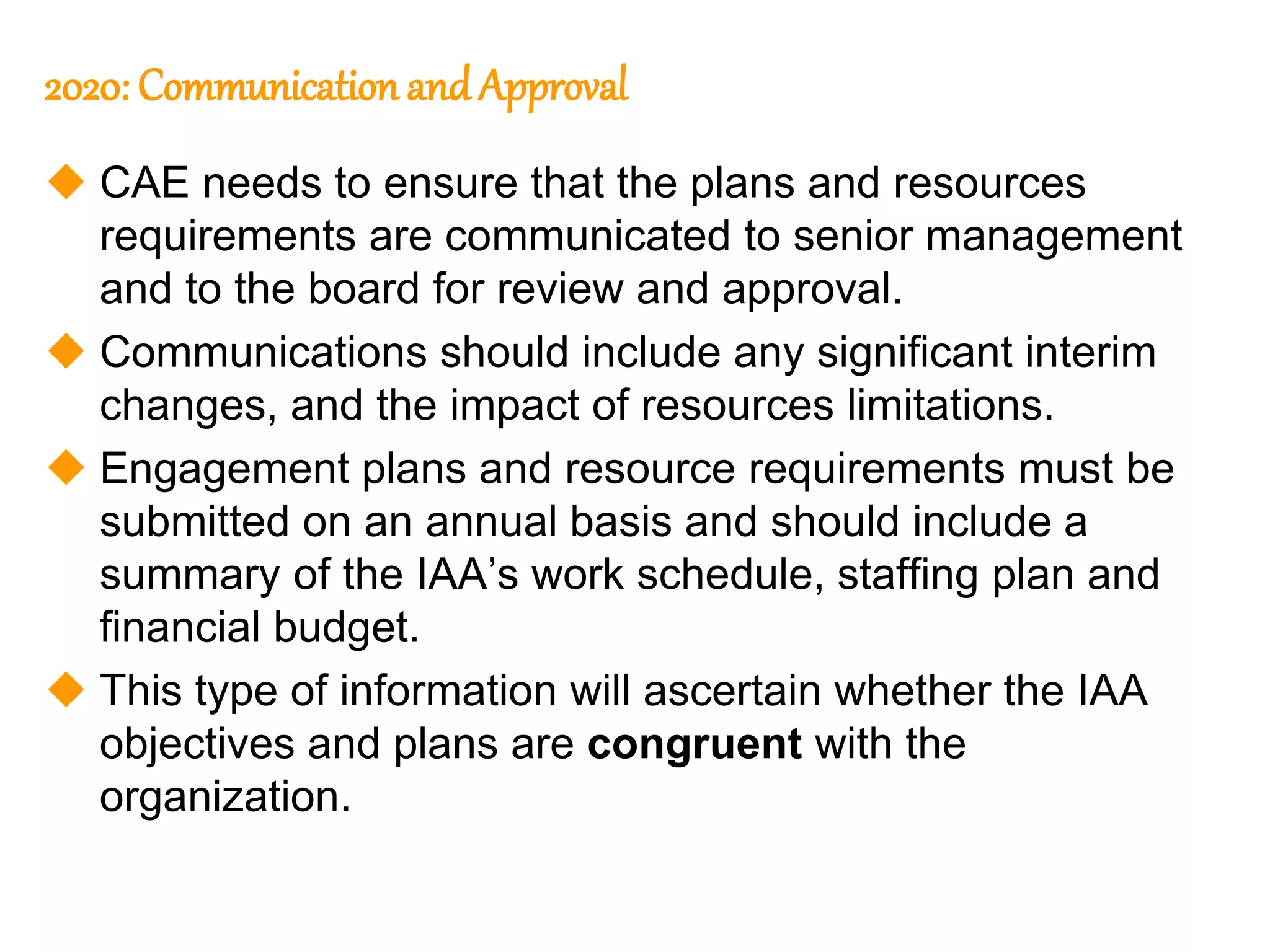

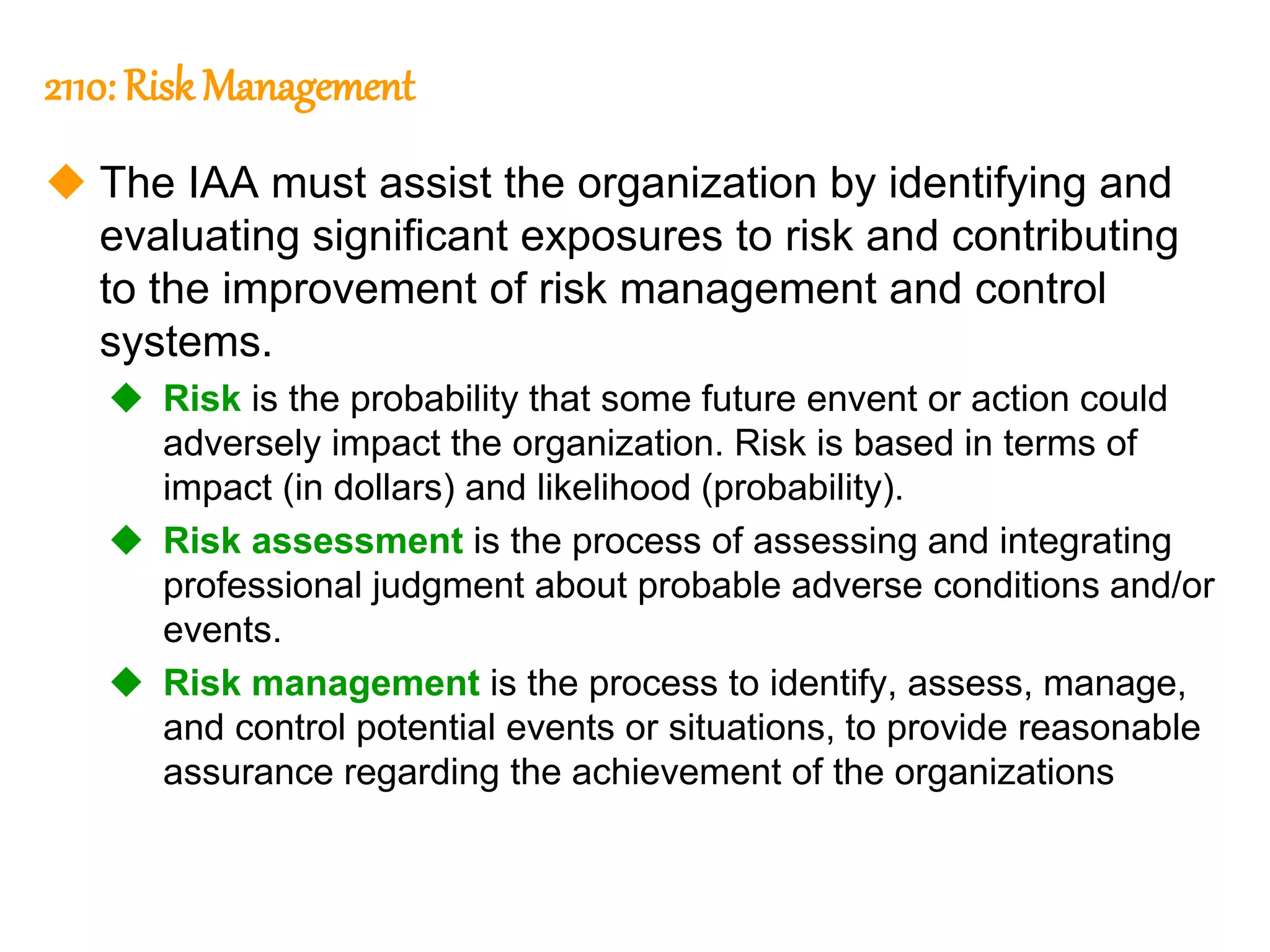

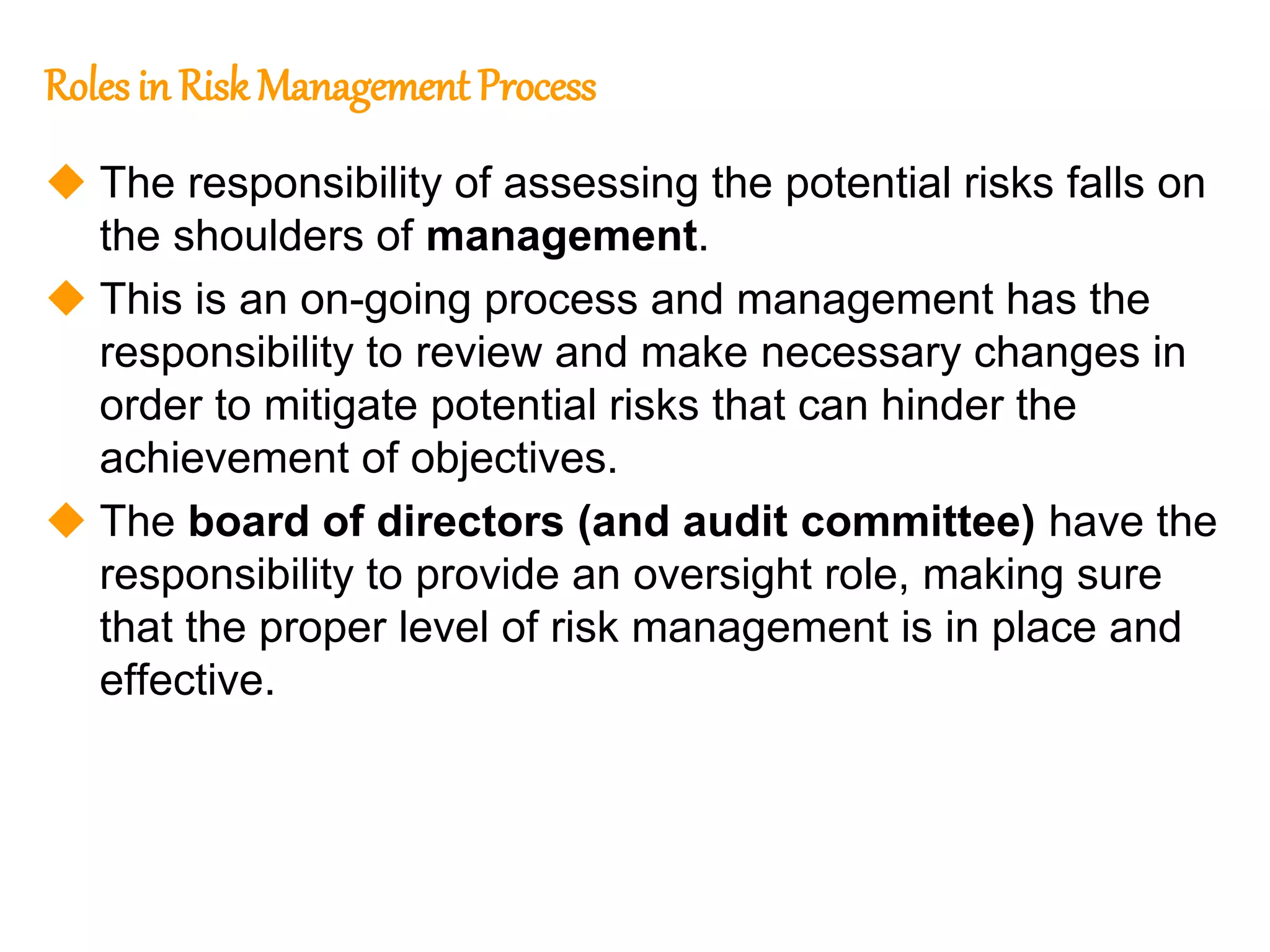

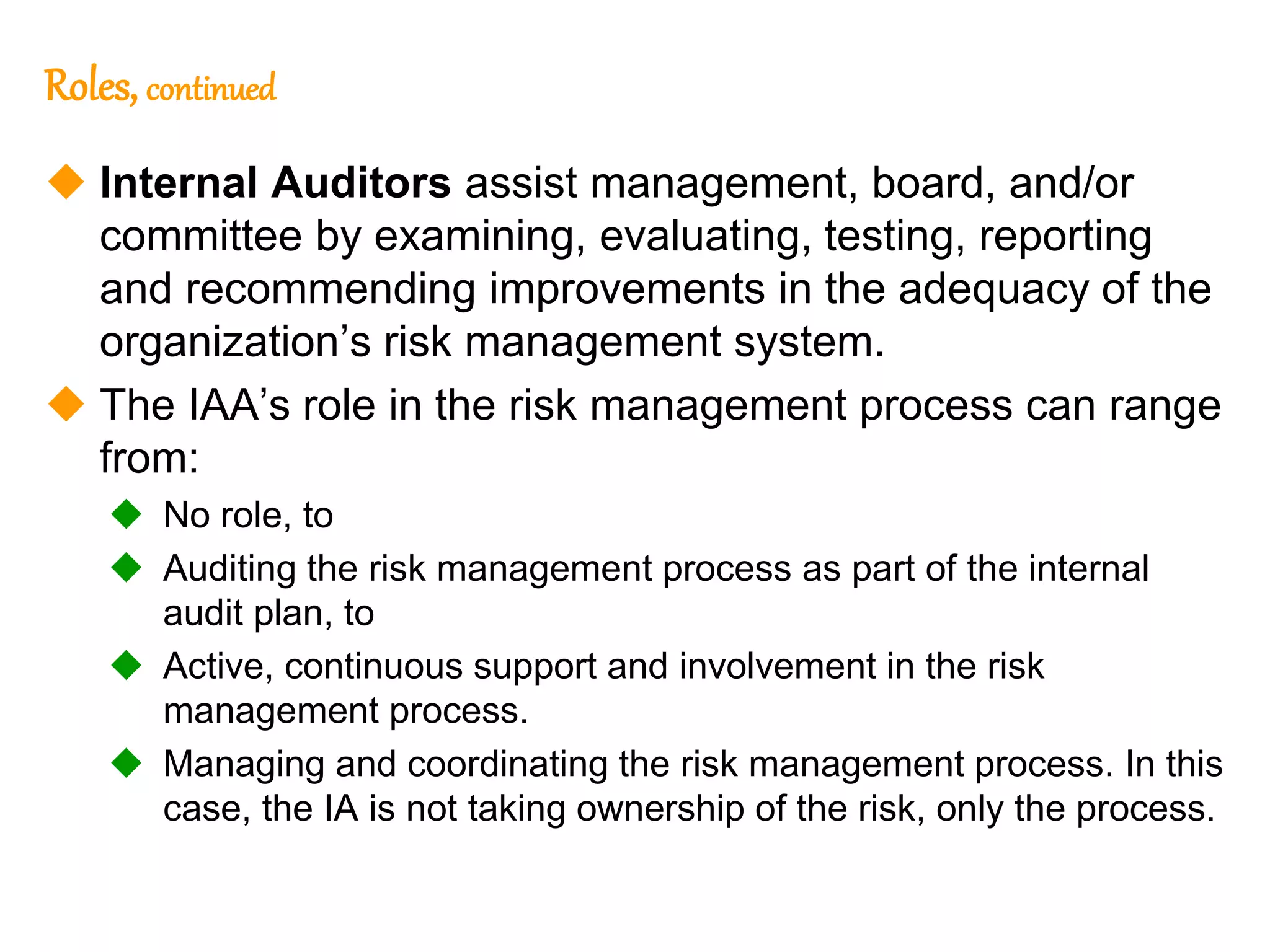

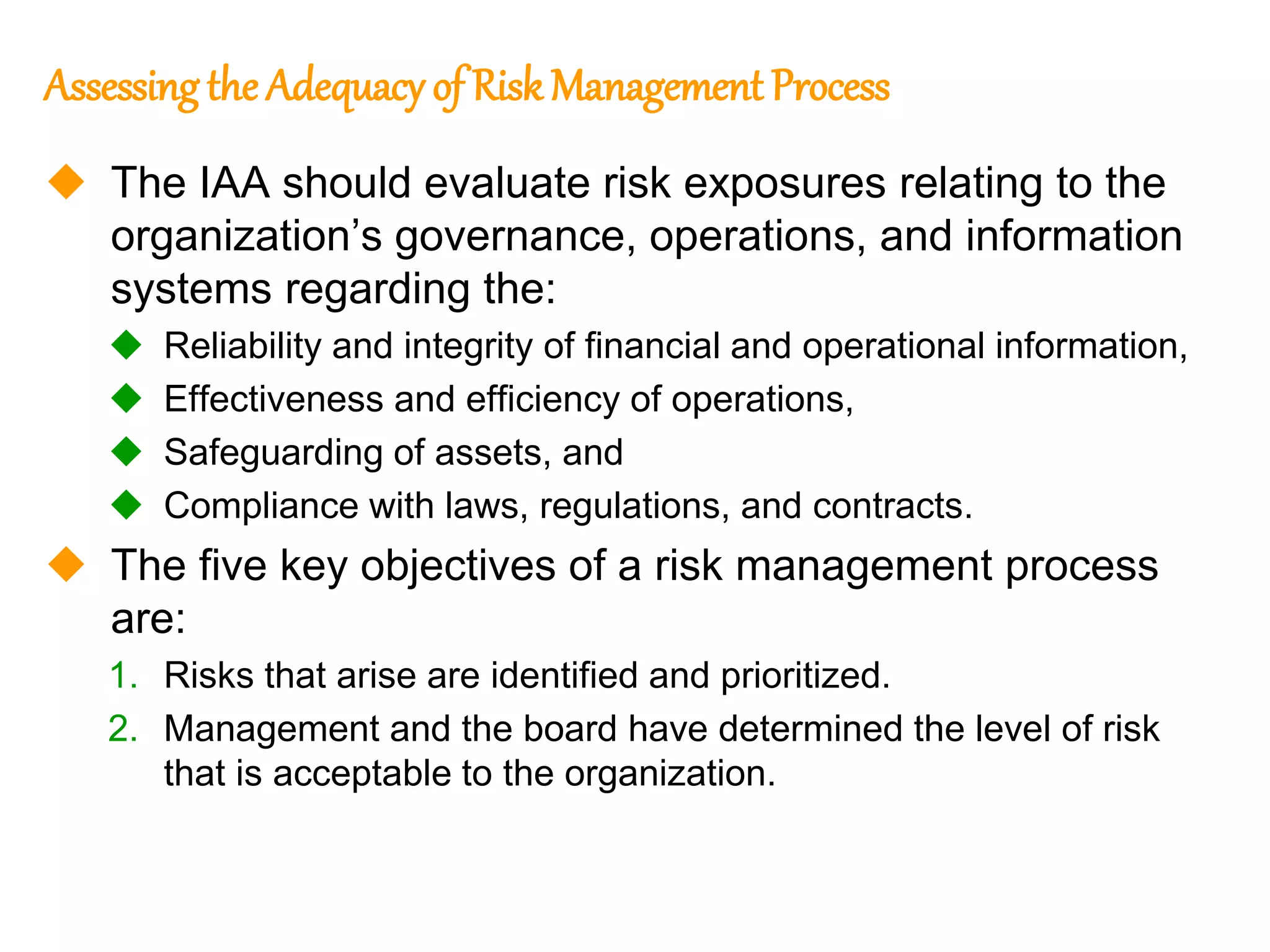

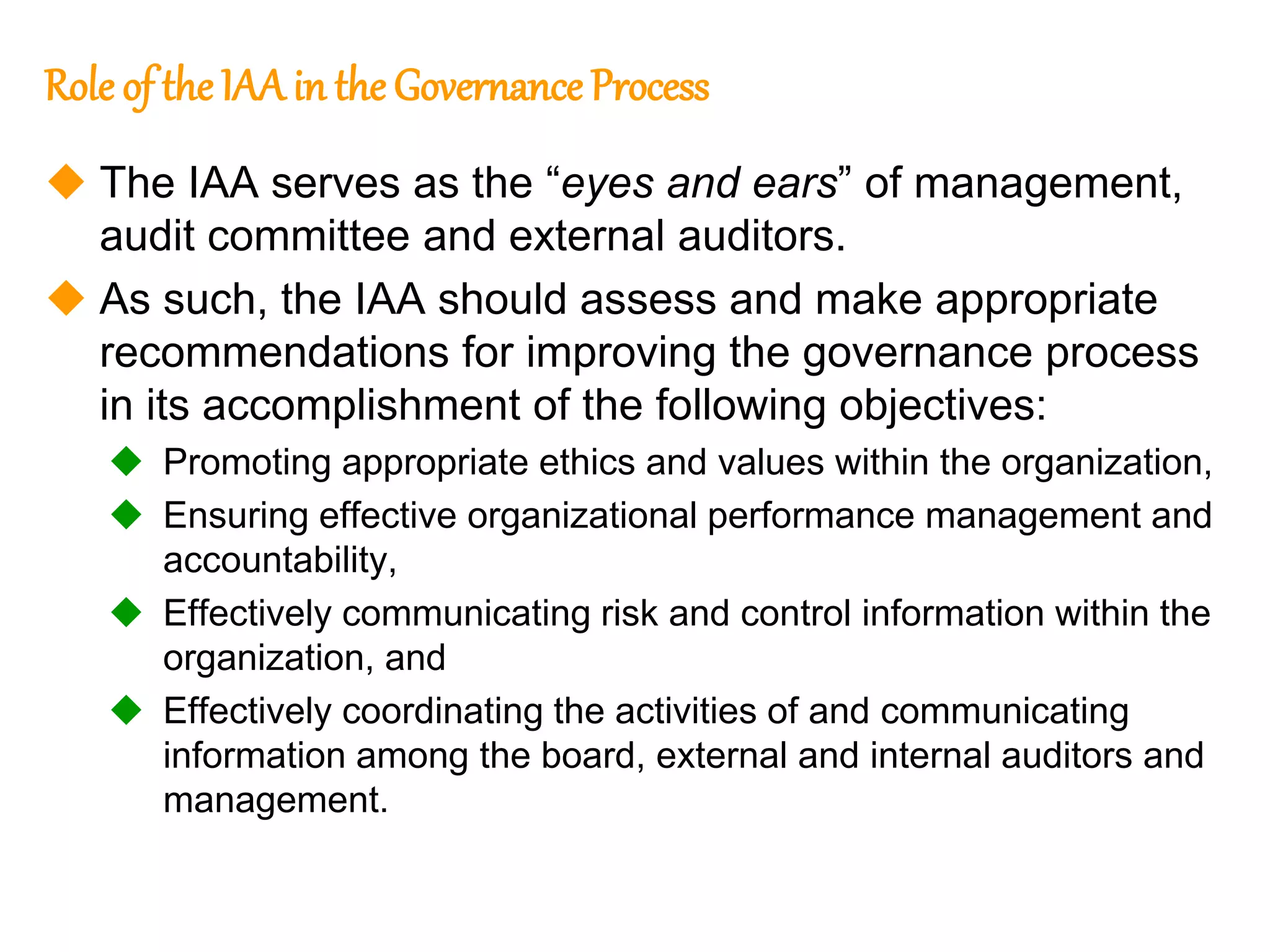

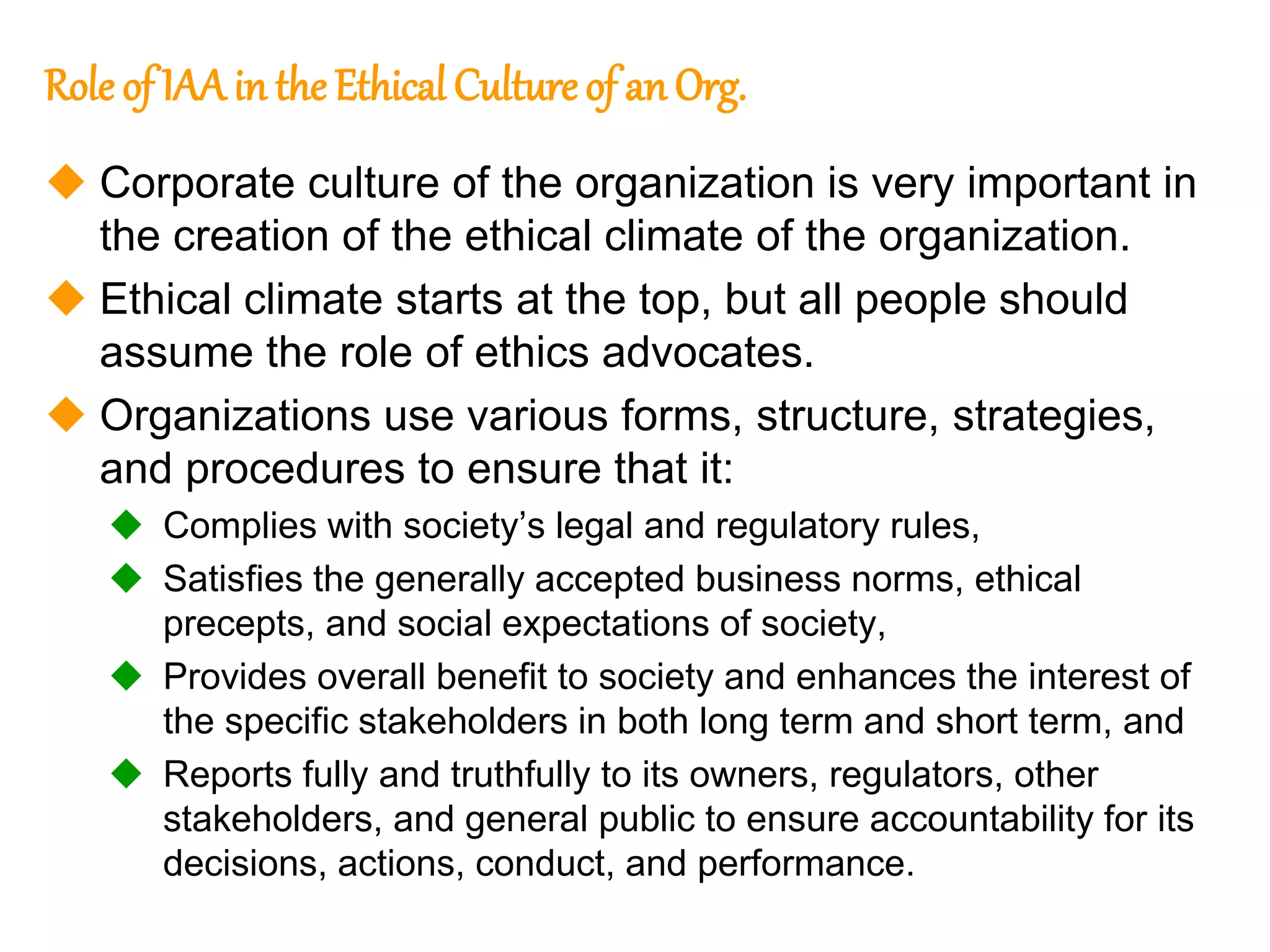

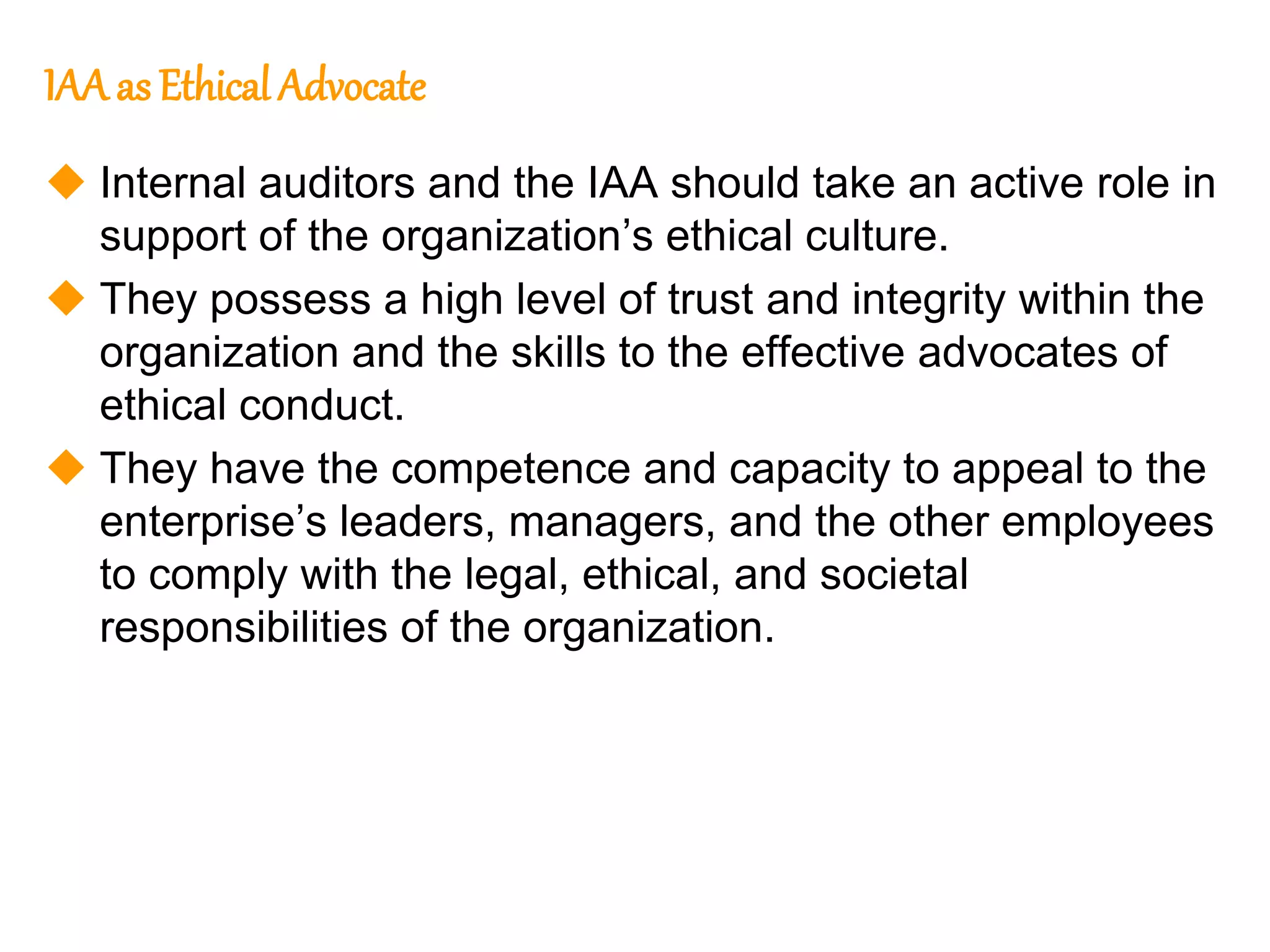

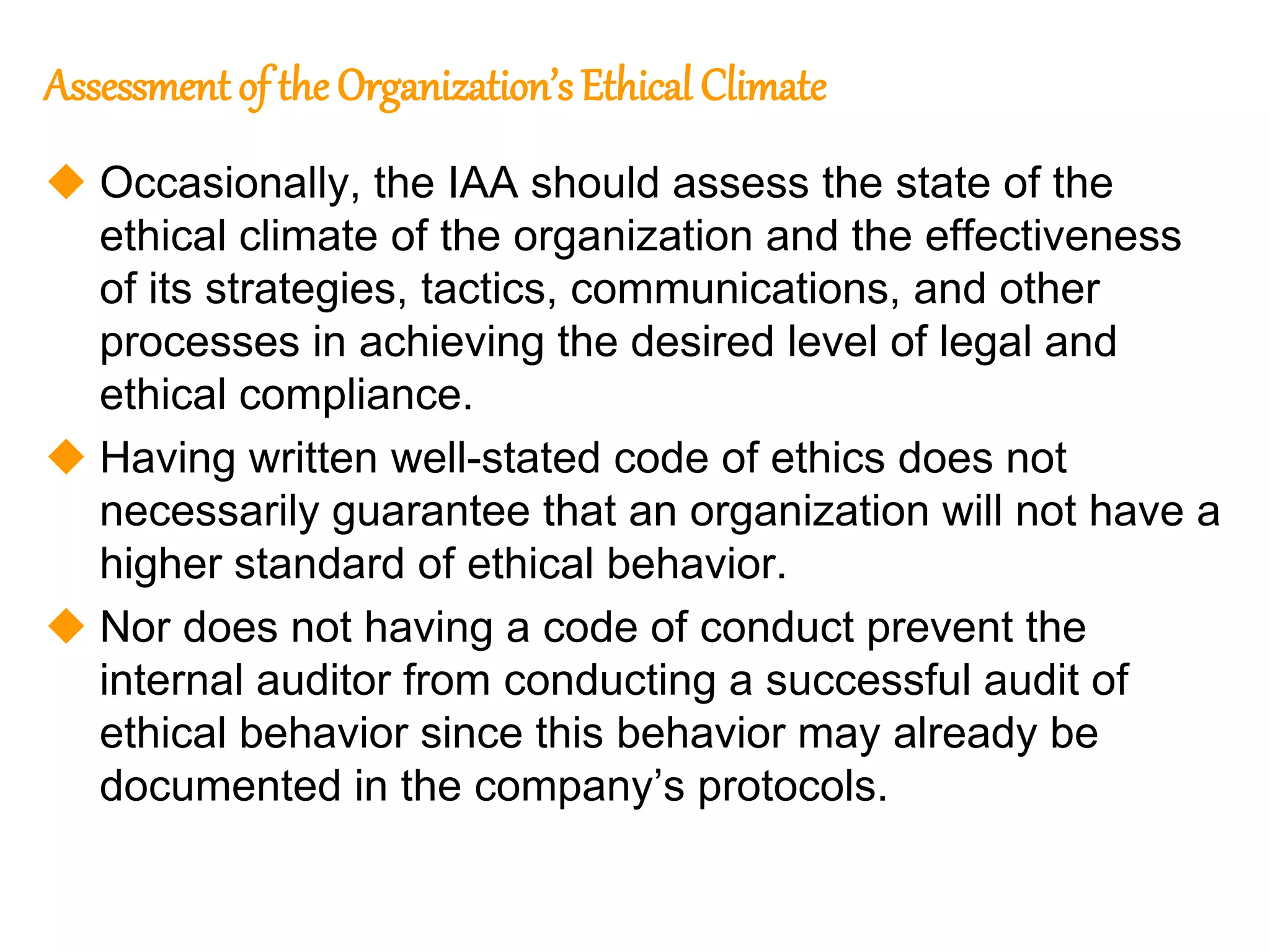

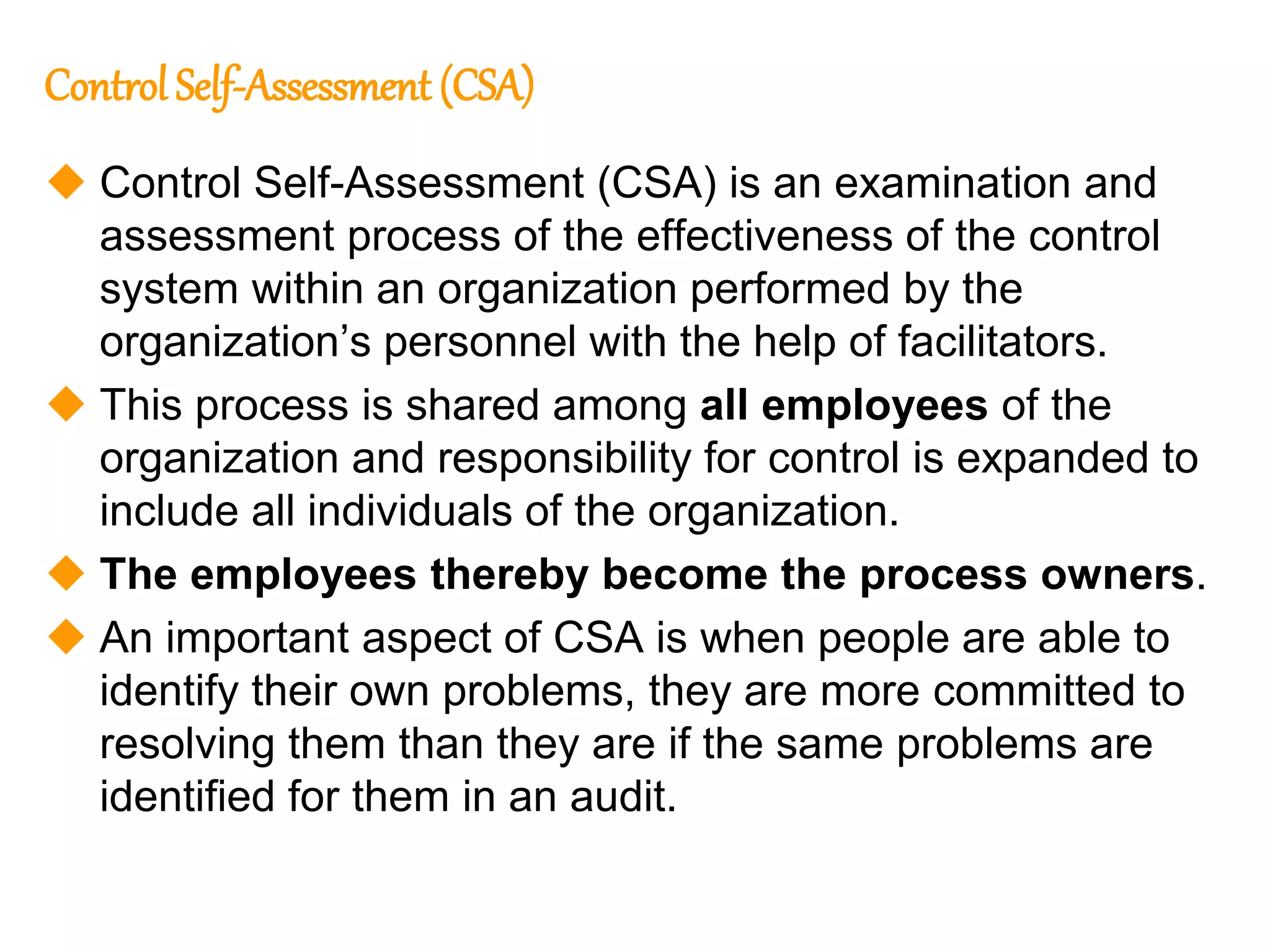

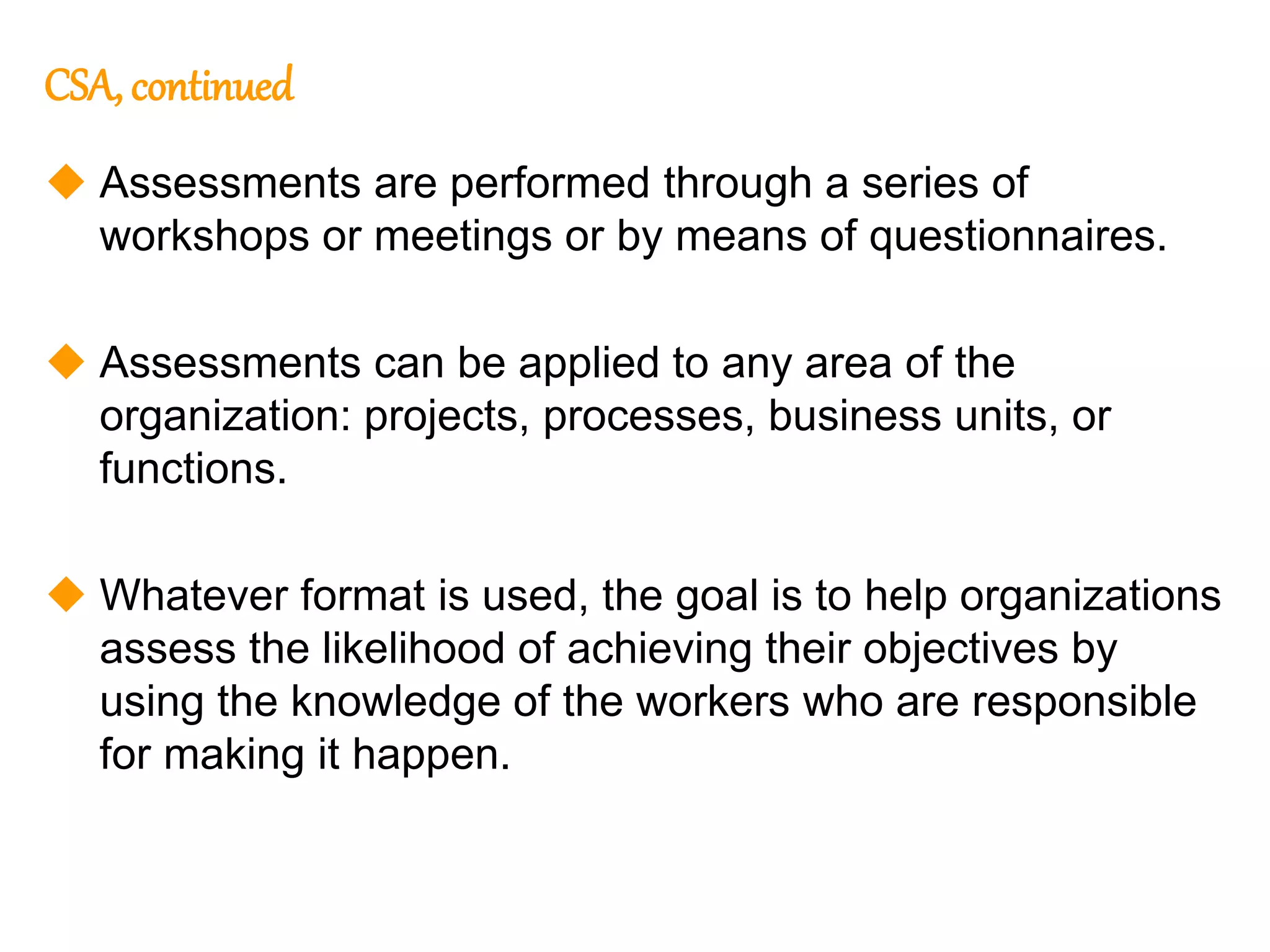

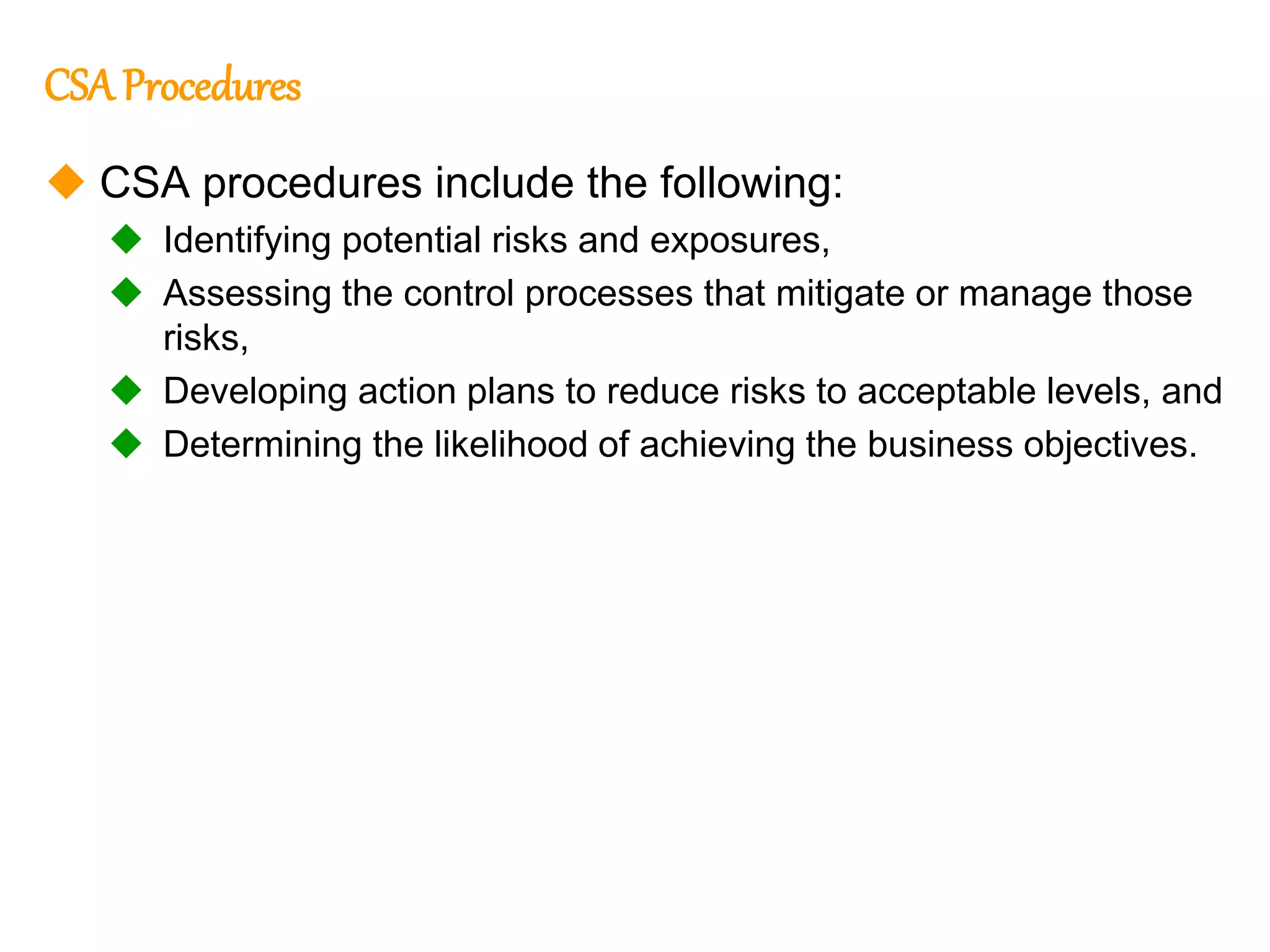

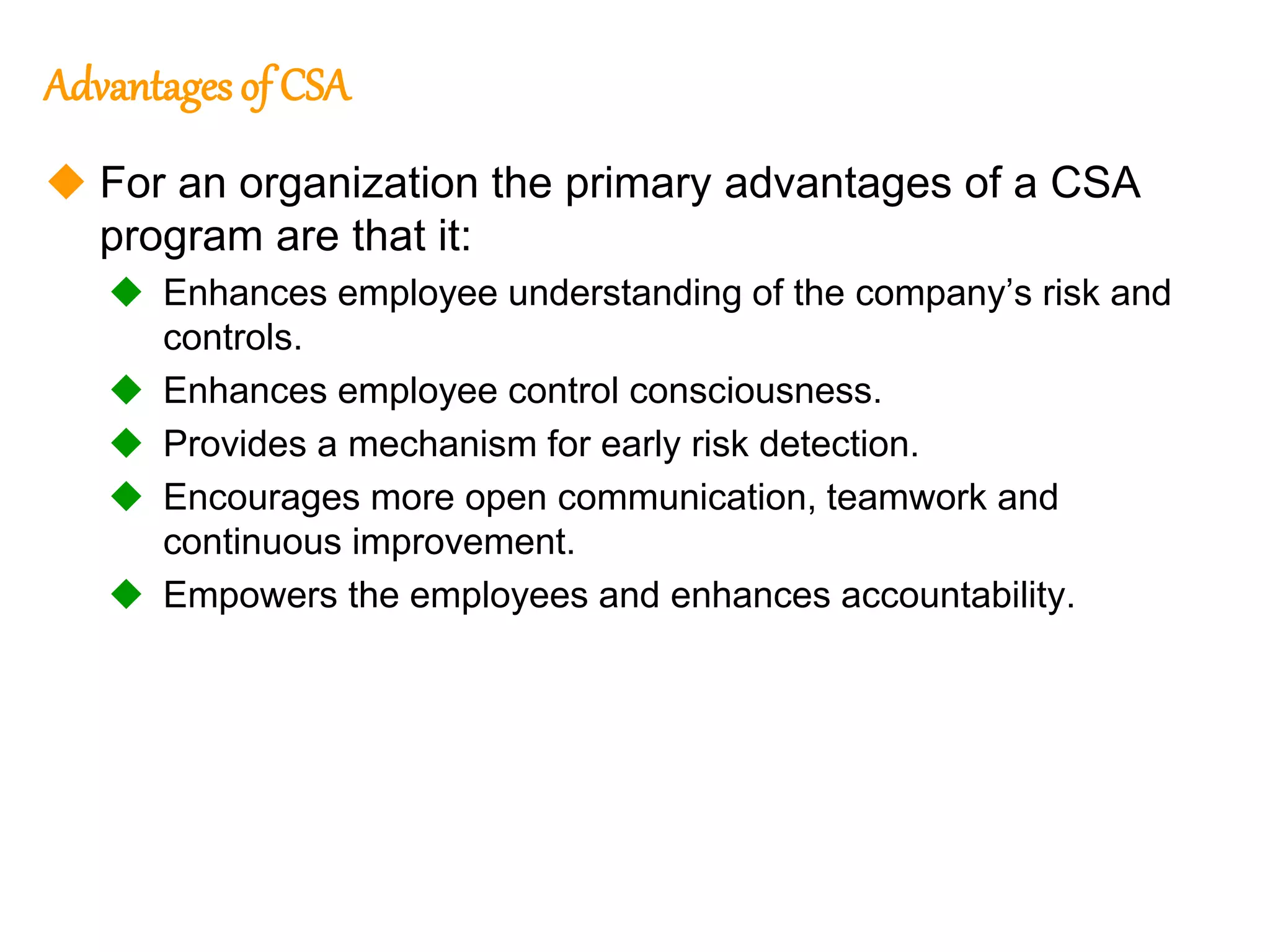

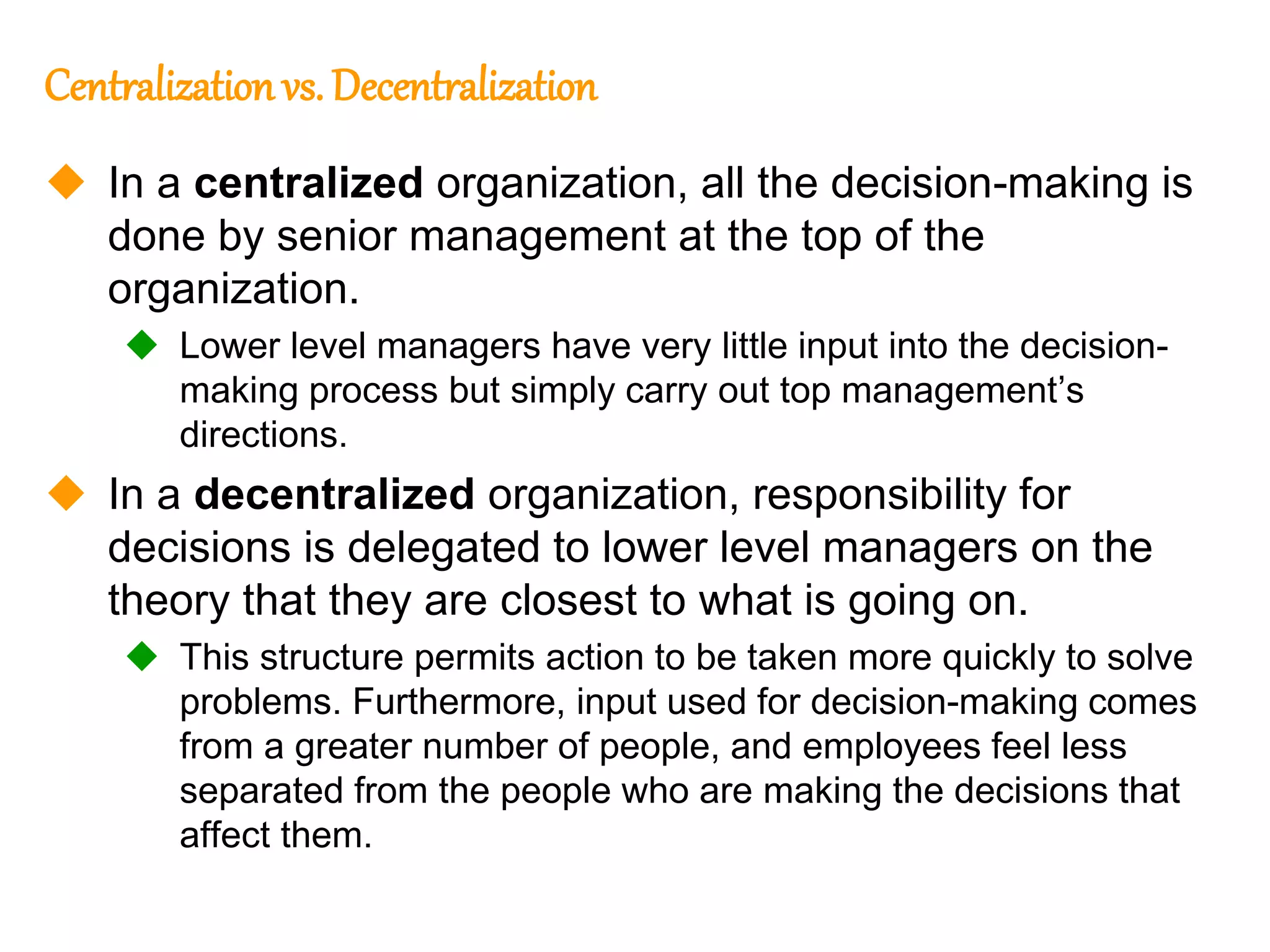

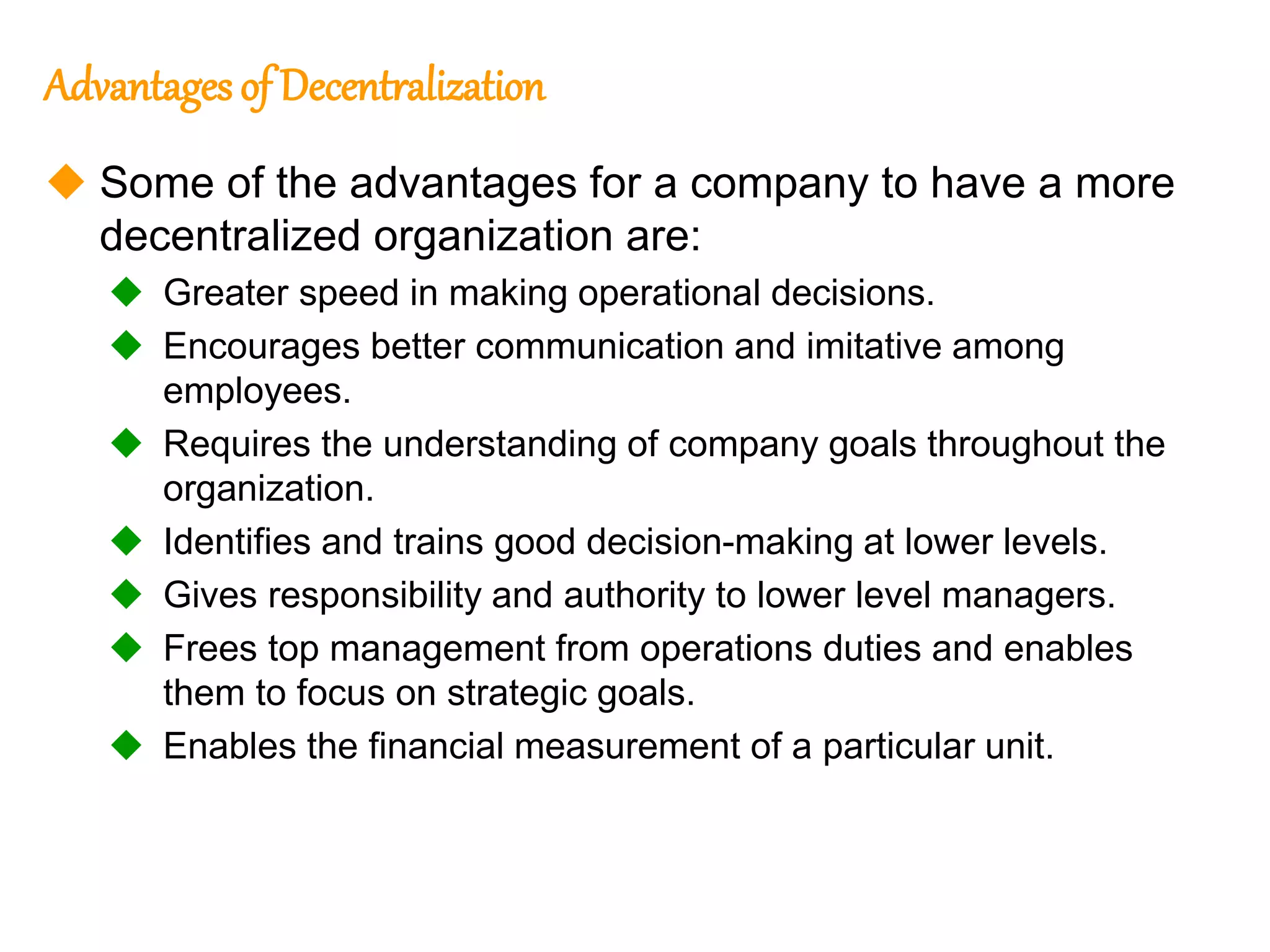

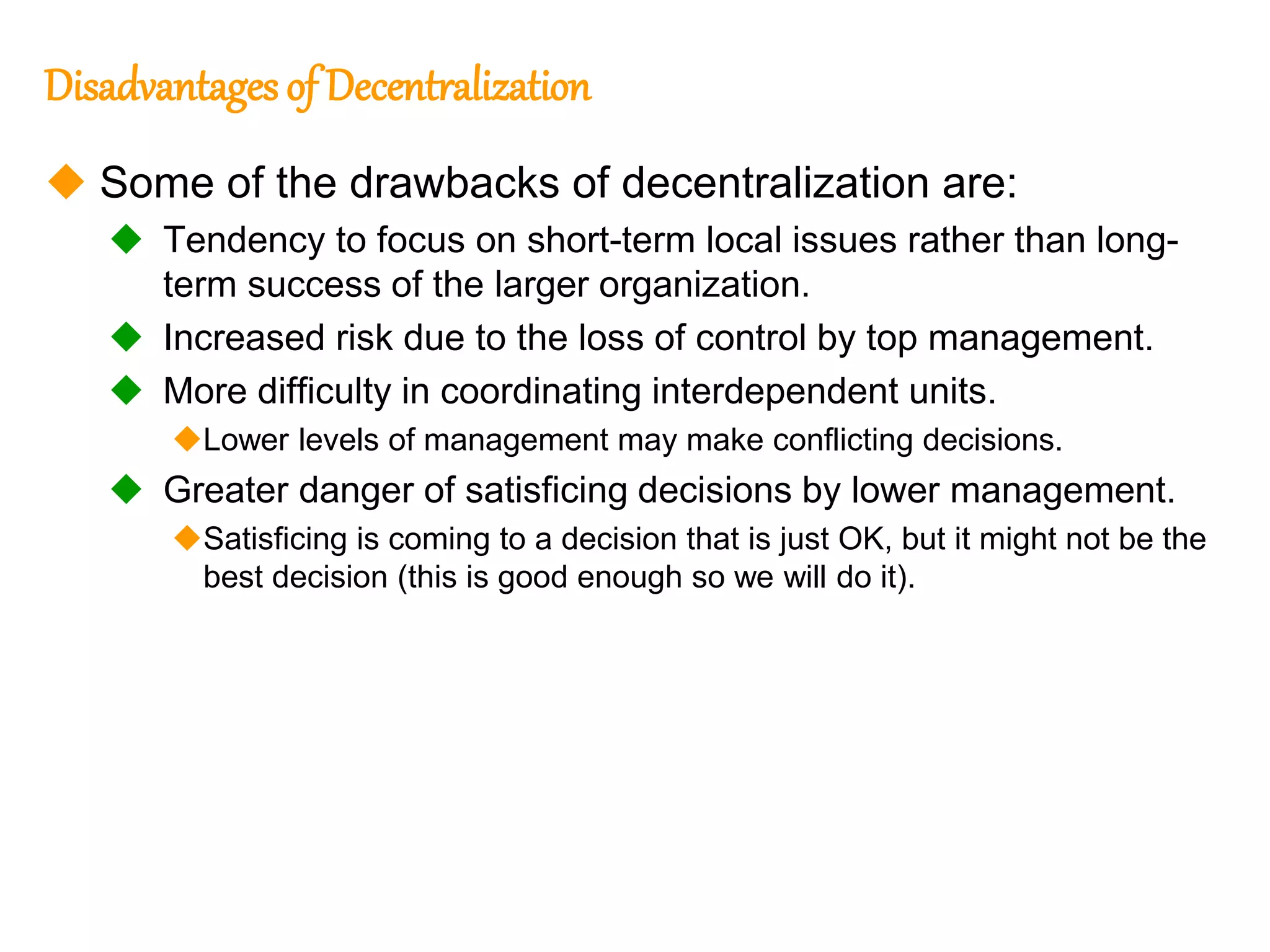

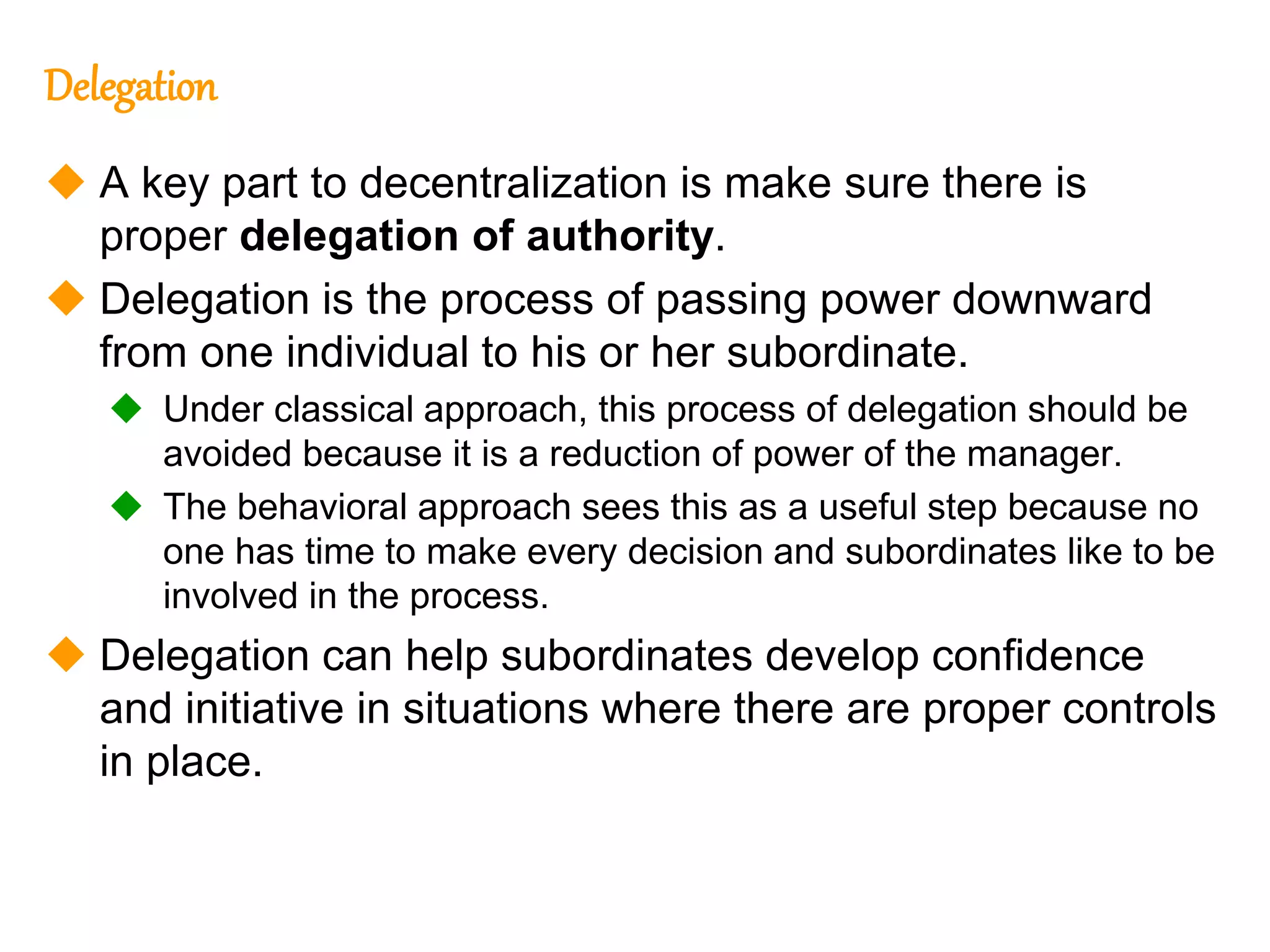

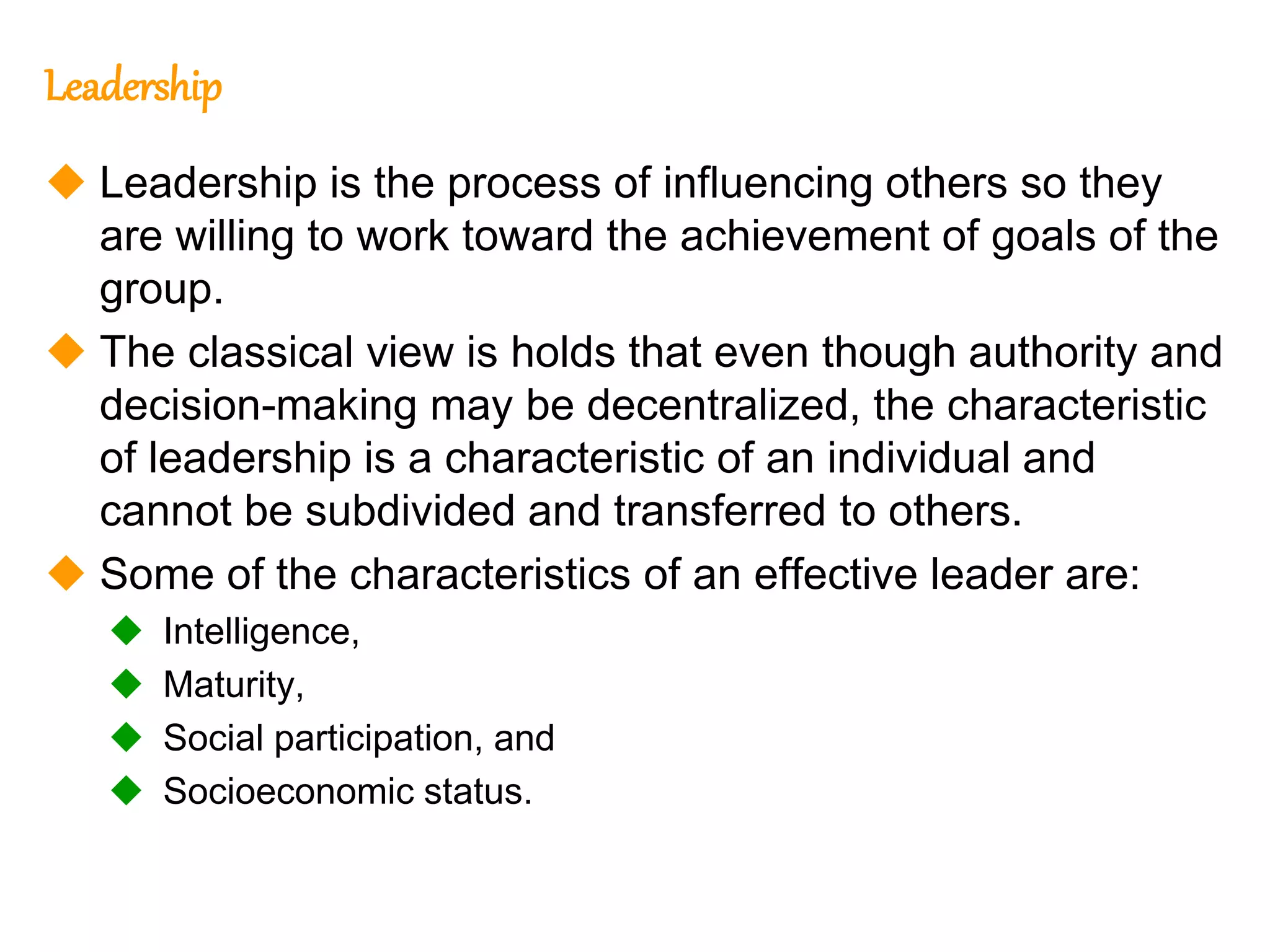

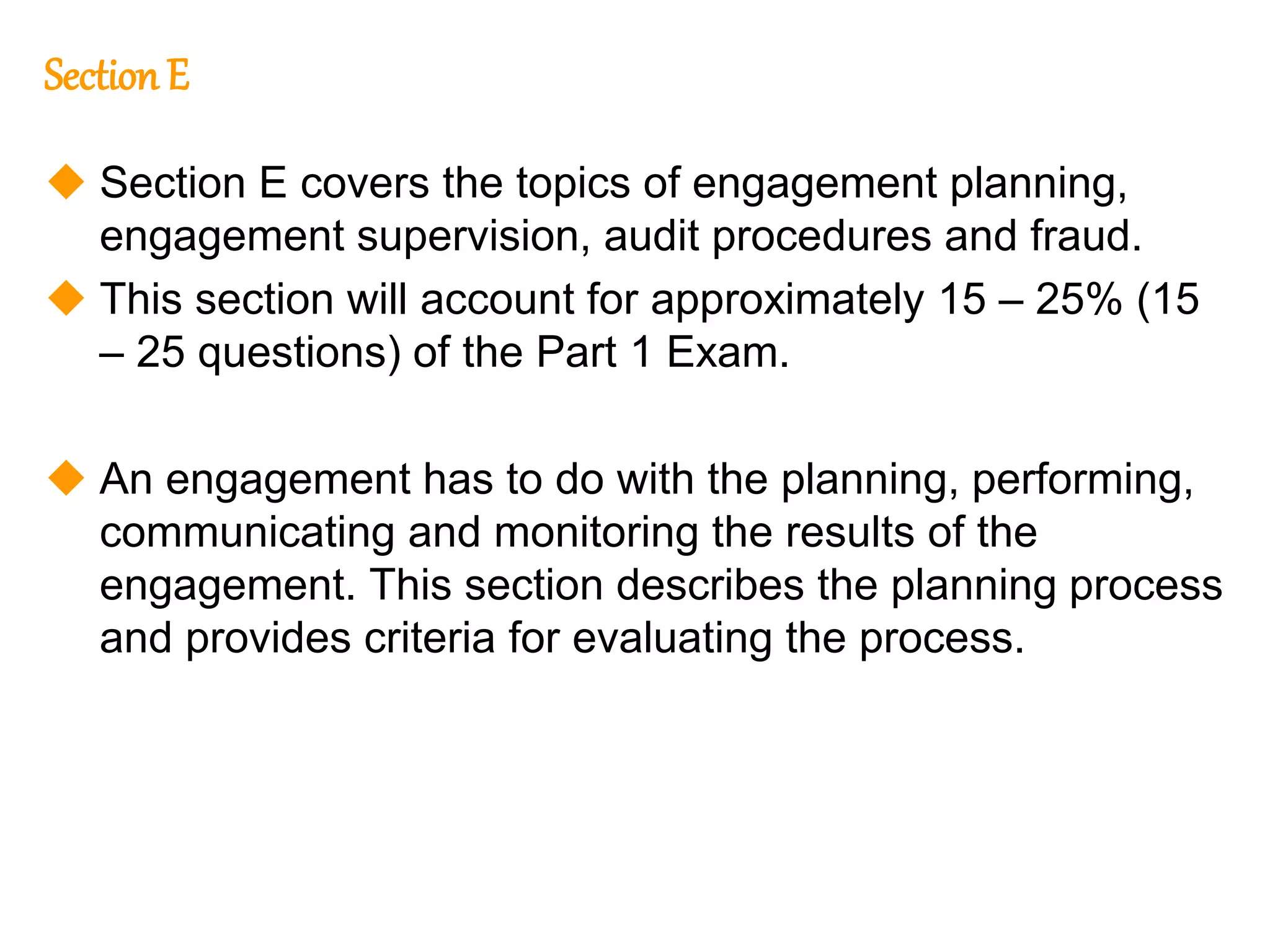

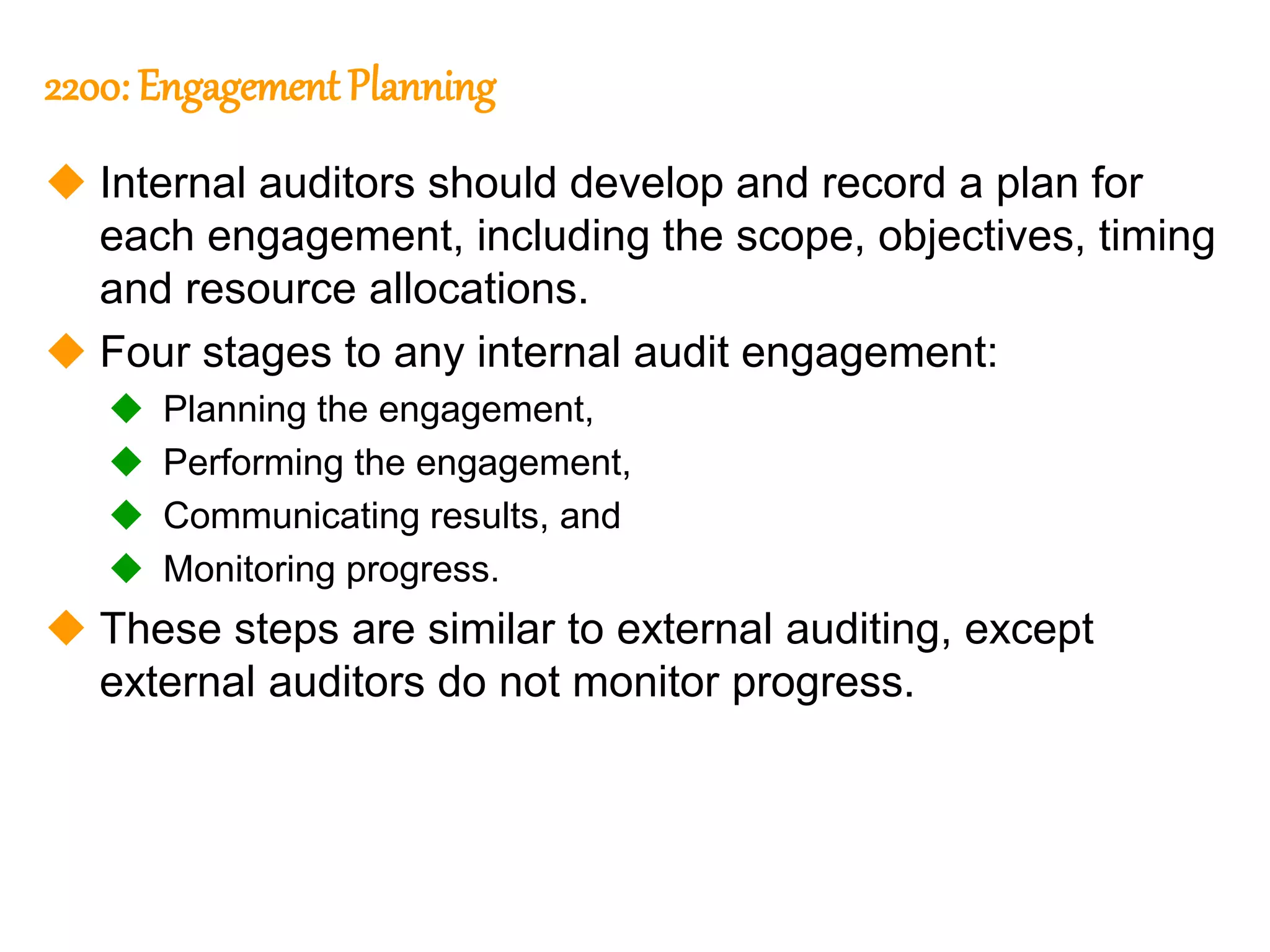

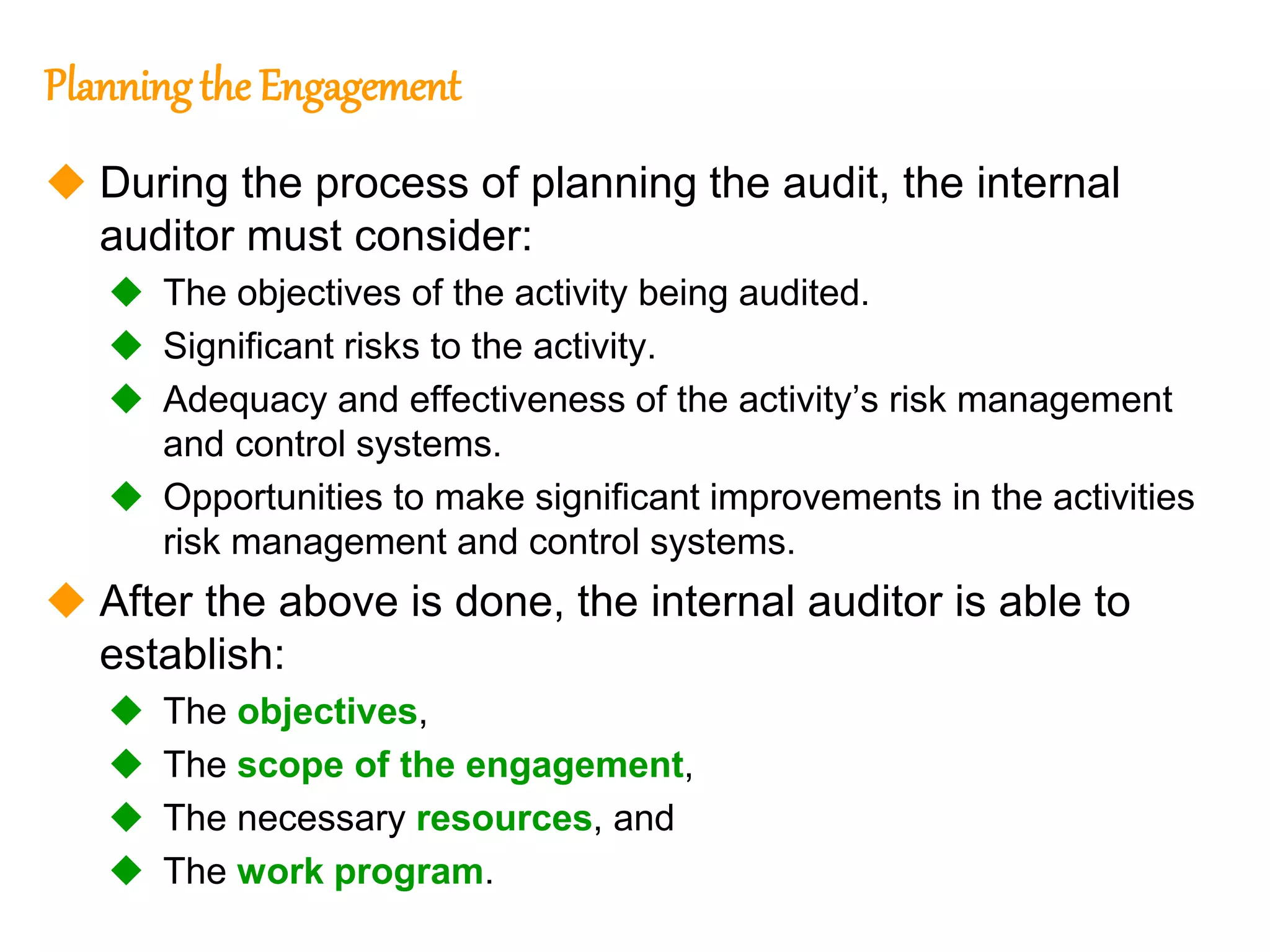

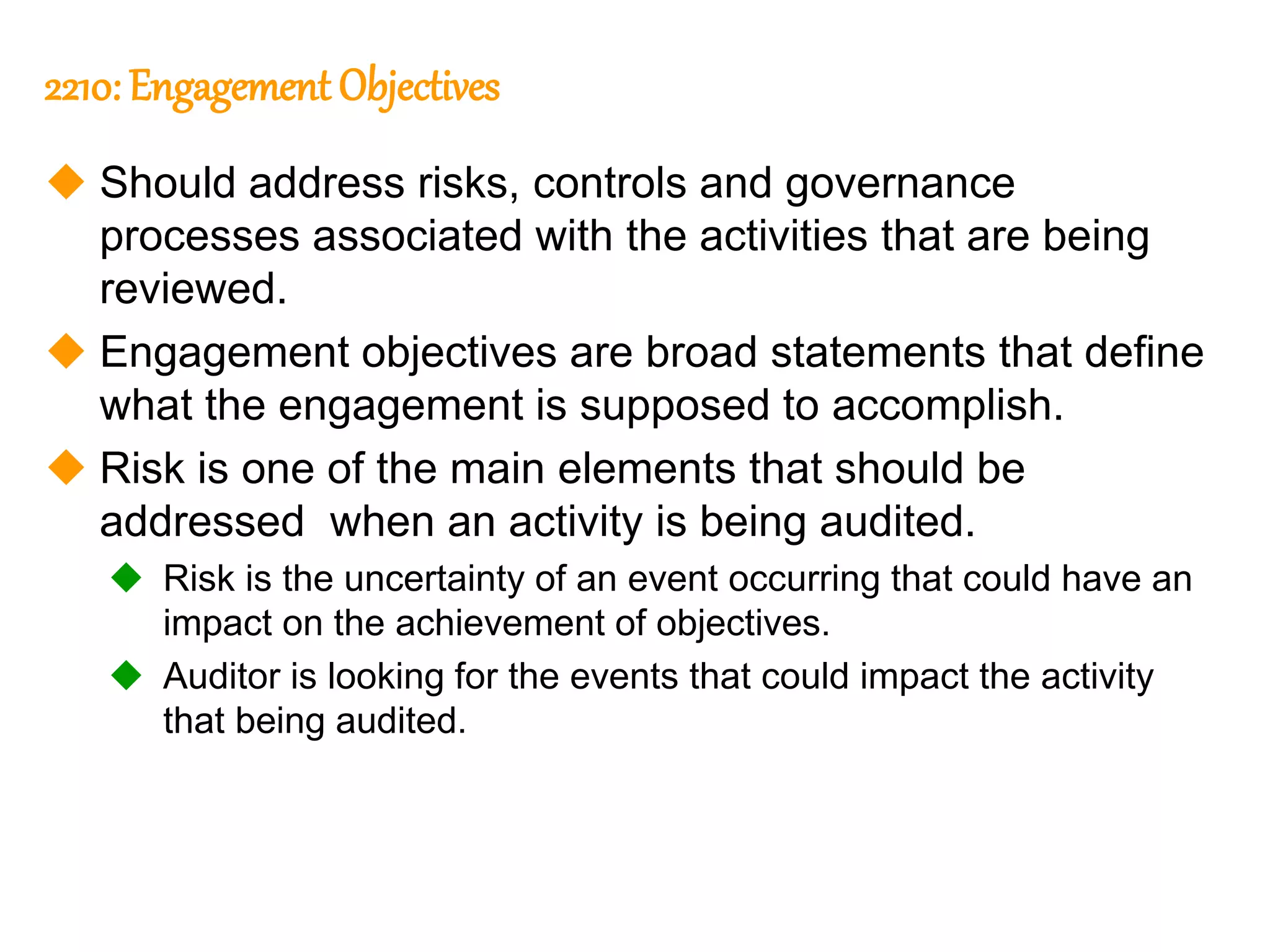

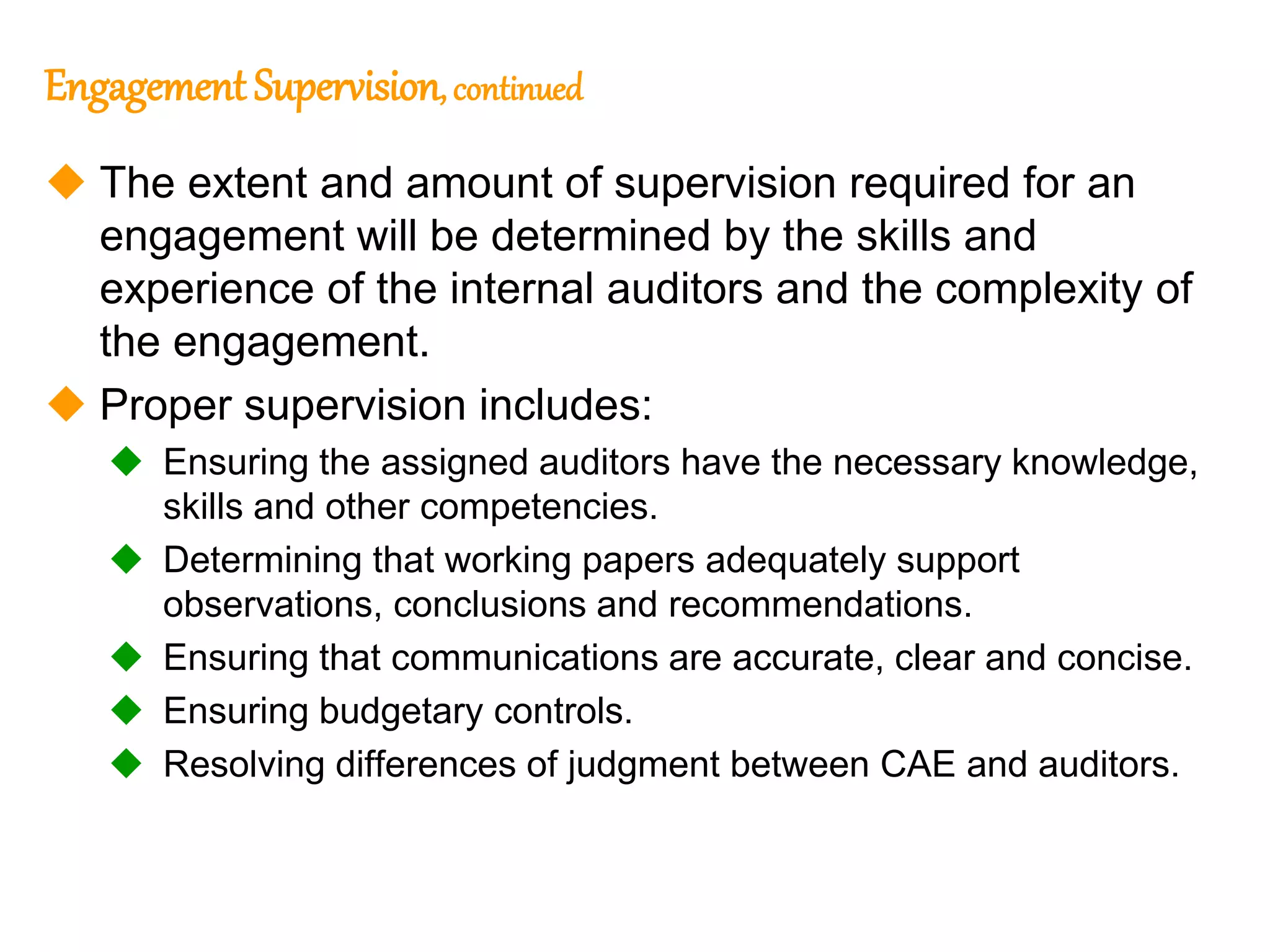

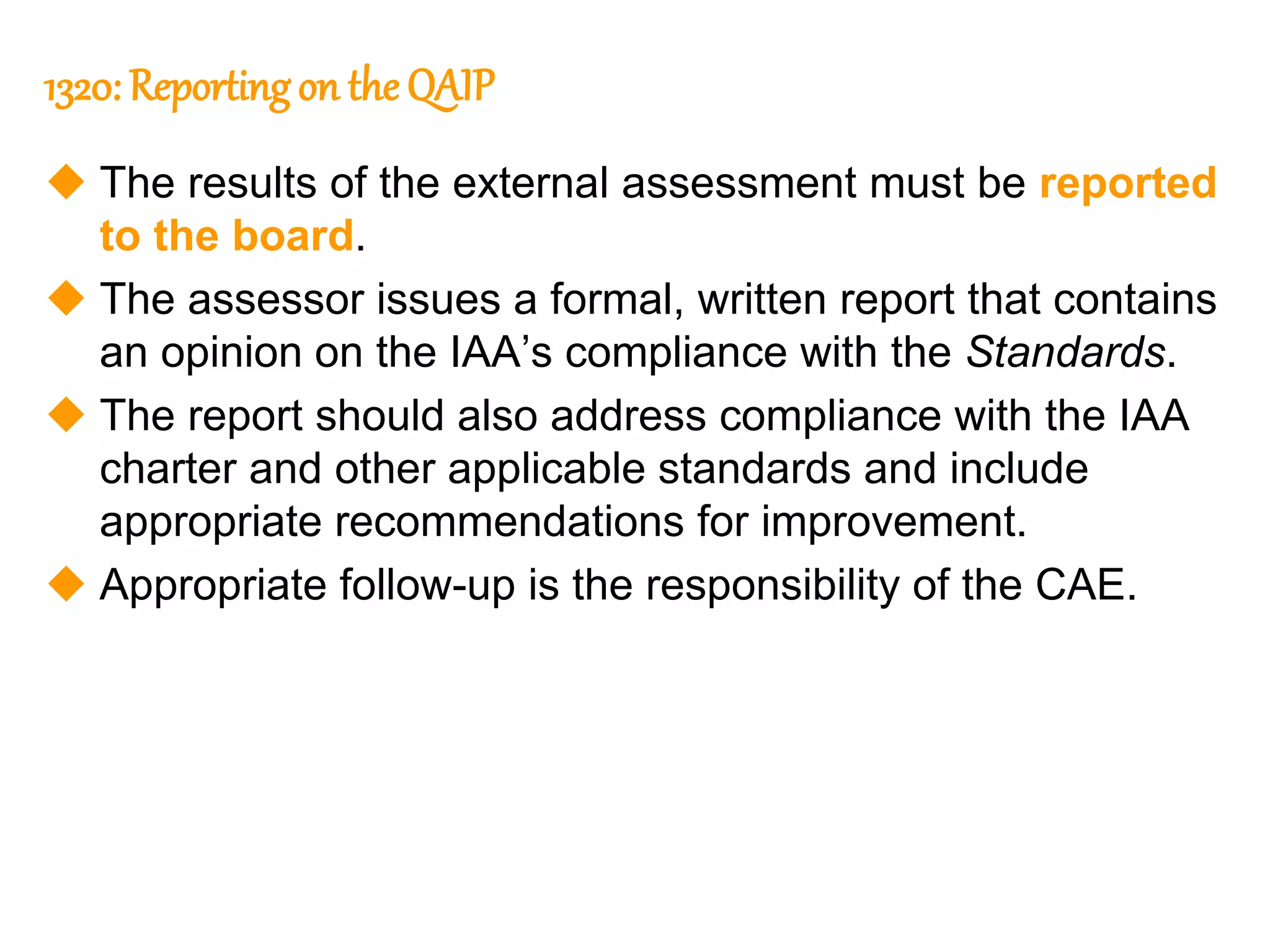

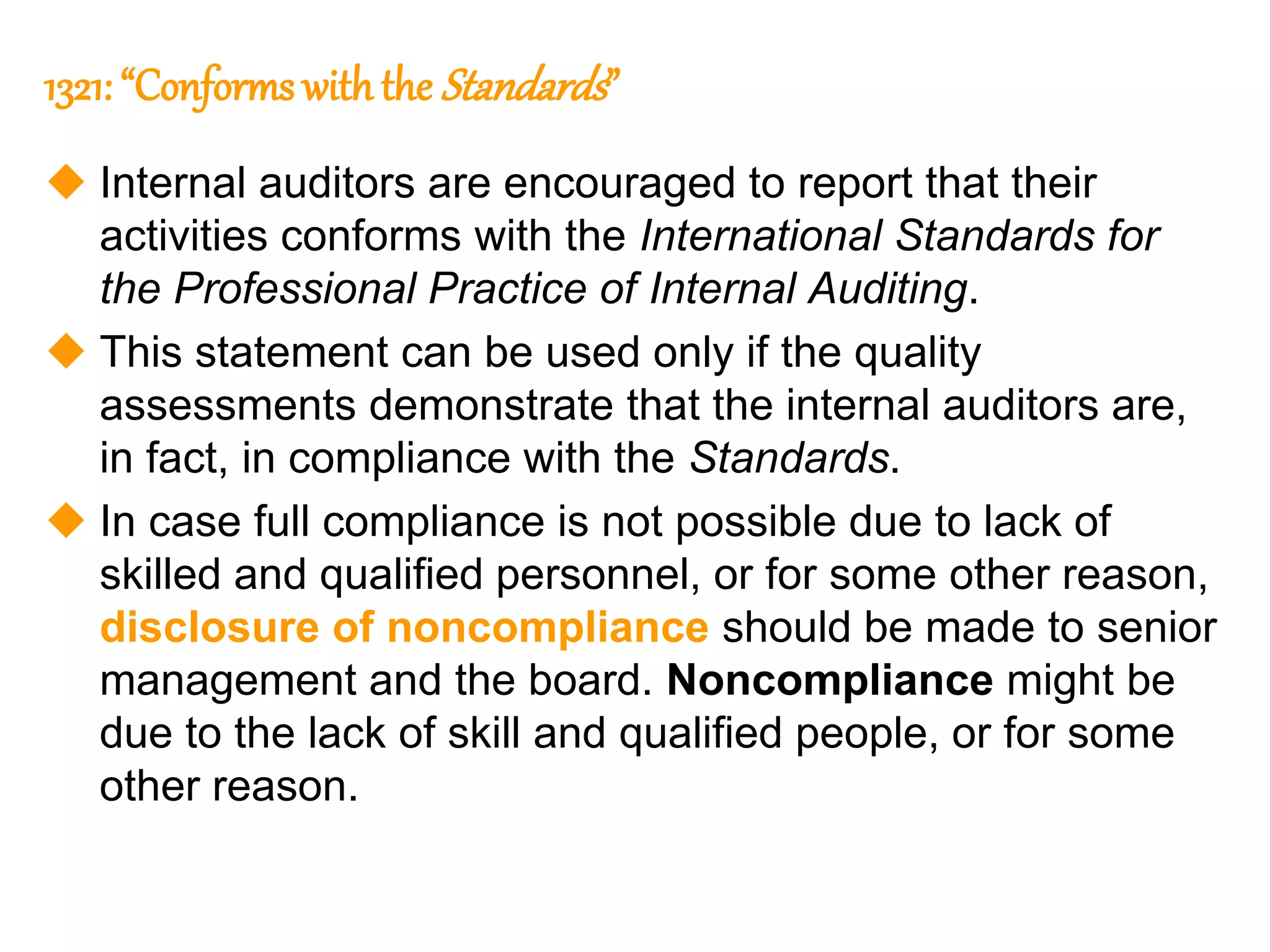

This document discusses the internal audit activity's role in governance, risk, and control. It covers several topics:

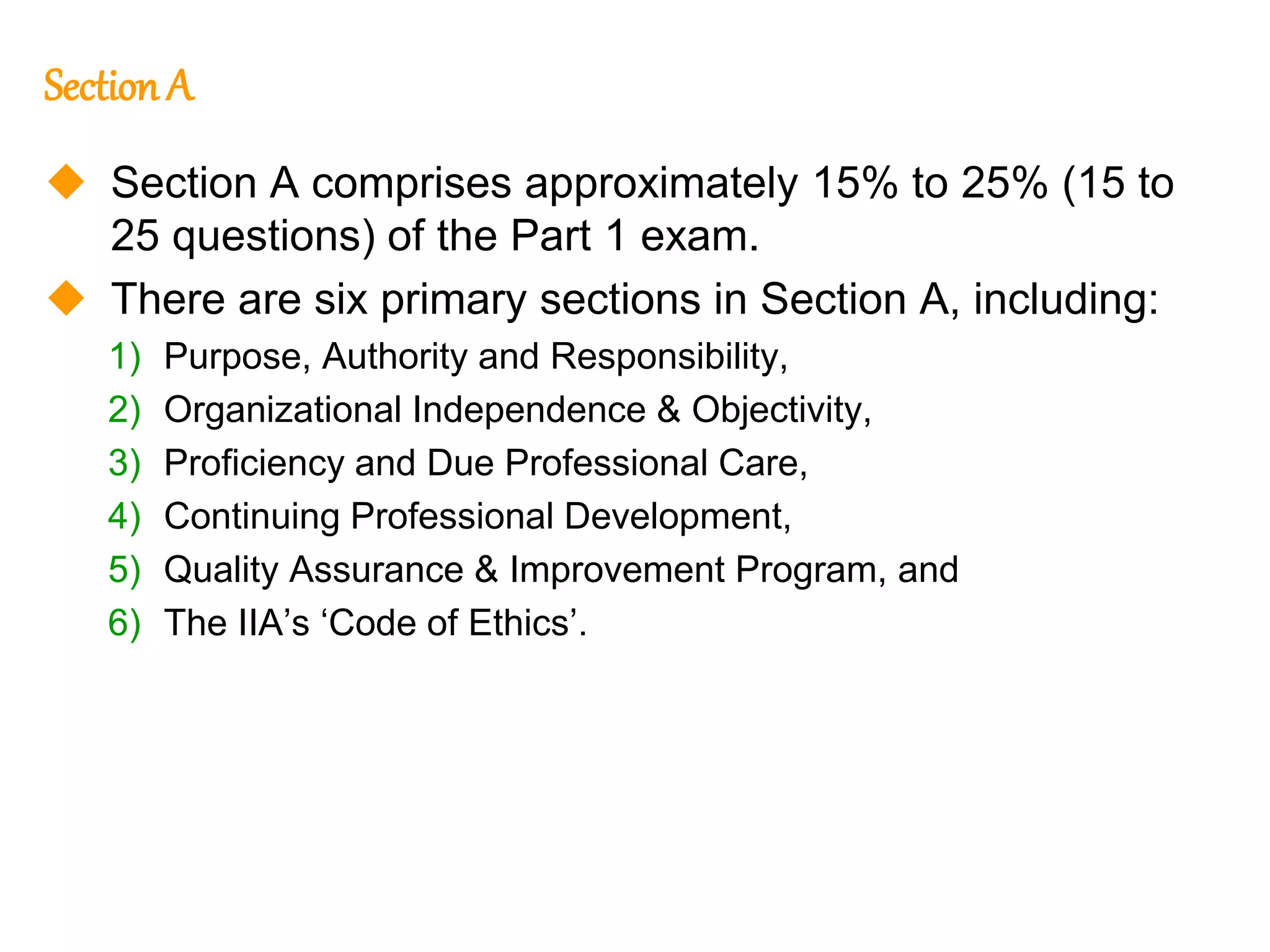

- Section A of Part 1 of the CIA exam focuses on complying with the Attribute Standards of the IIA.

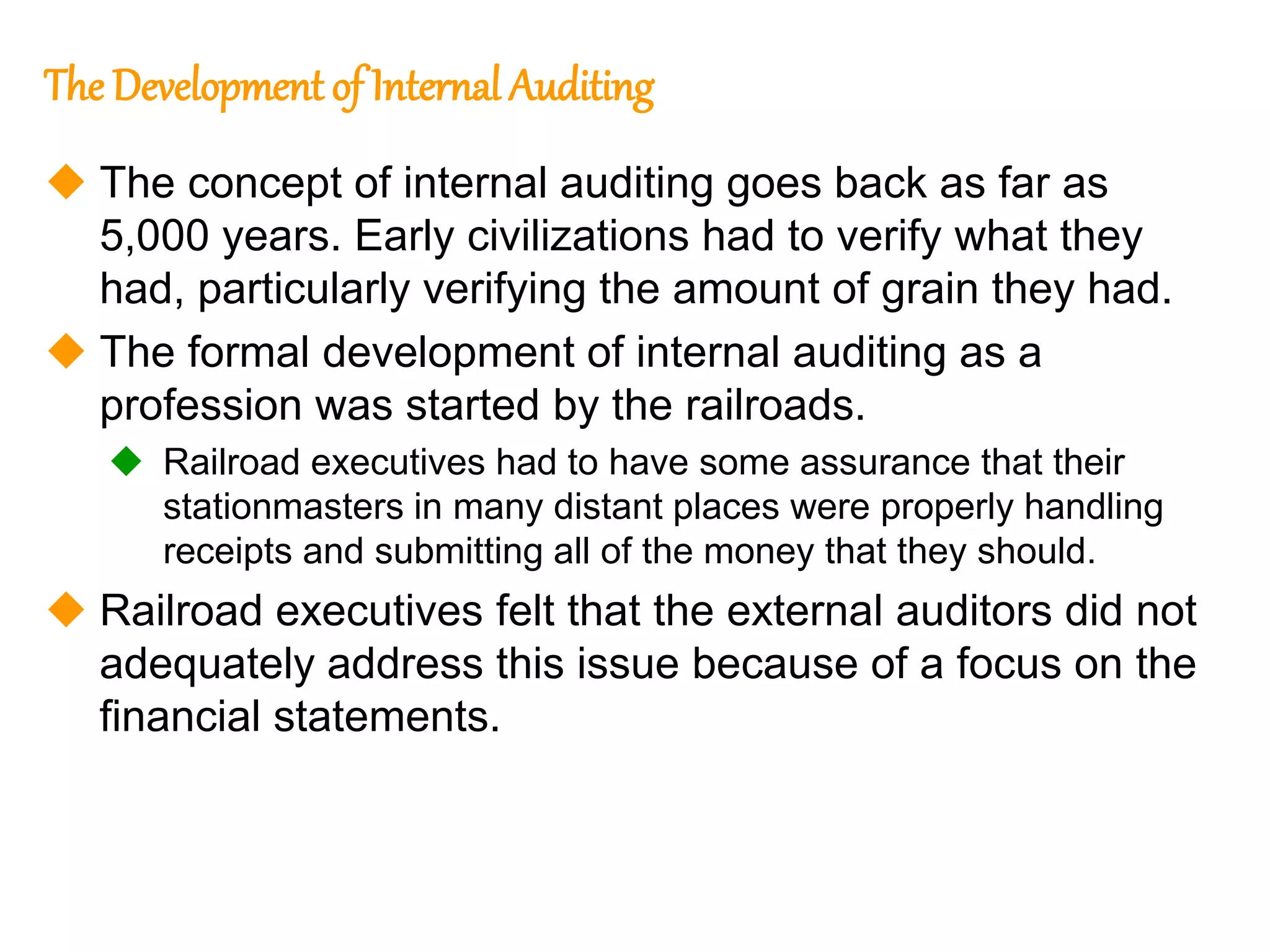

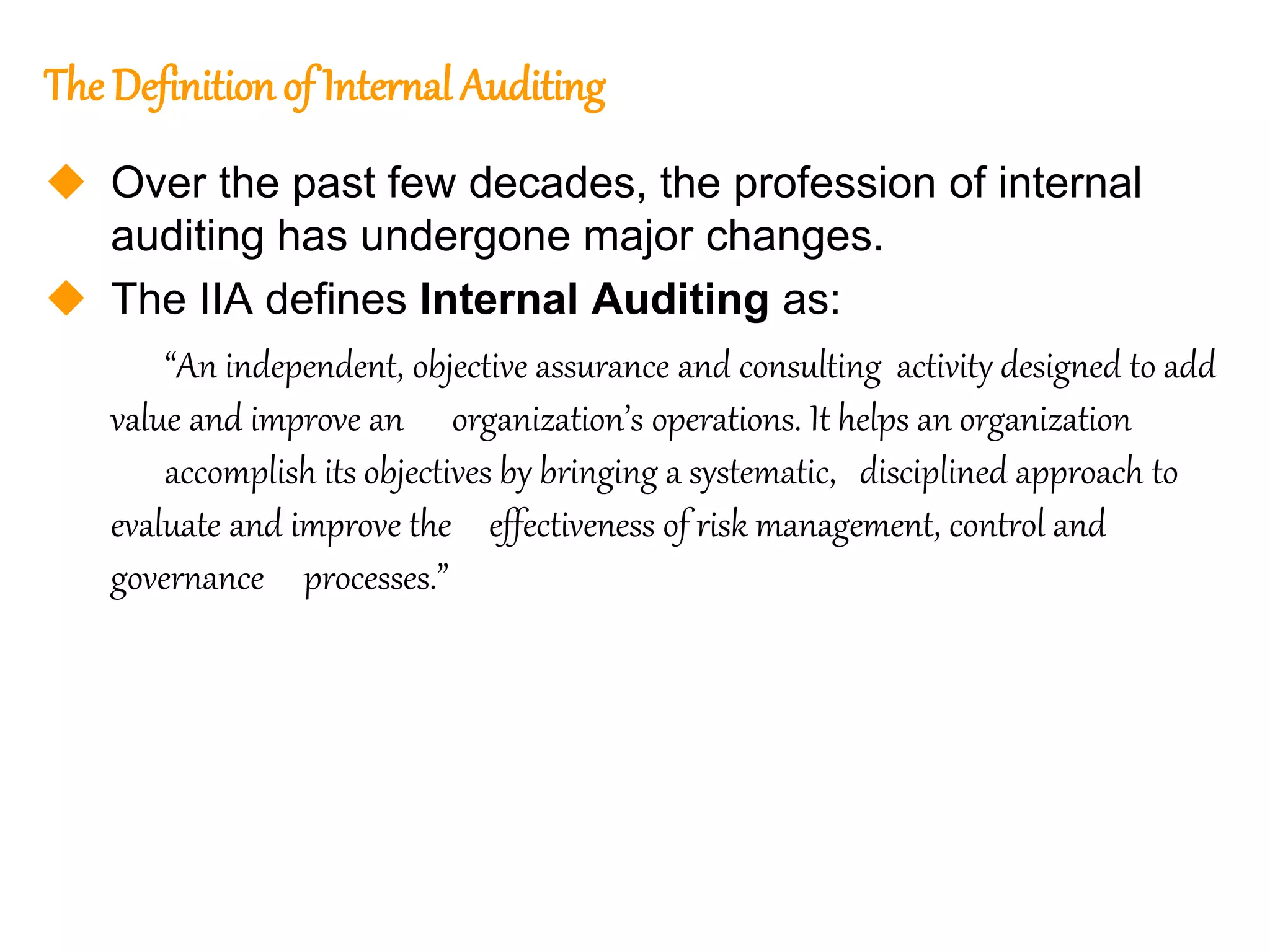

- The development of internal auditing as a profession began with railroad executives needing assurance about stationmasters handling receipts.

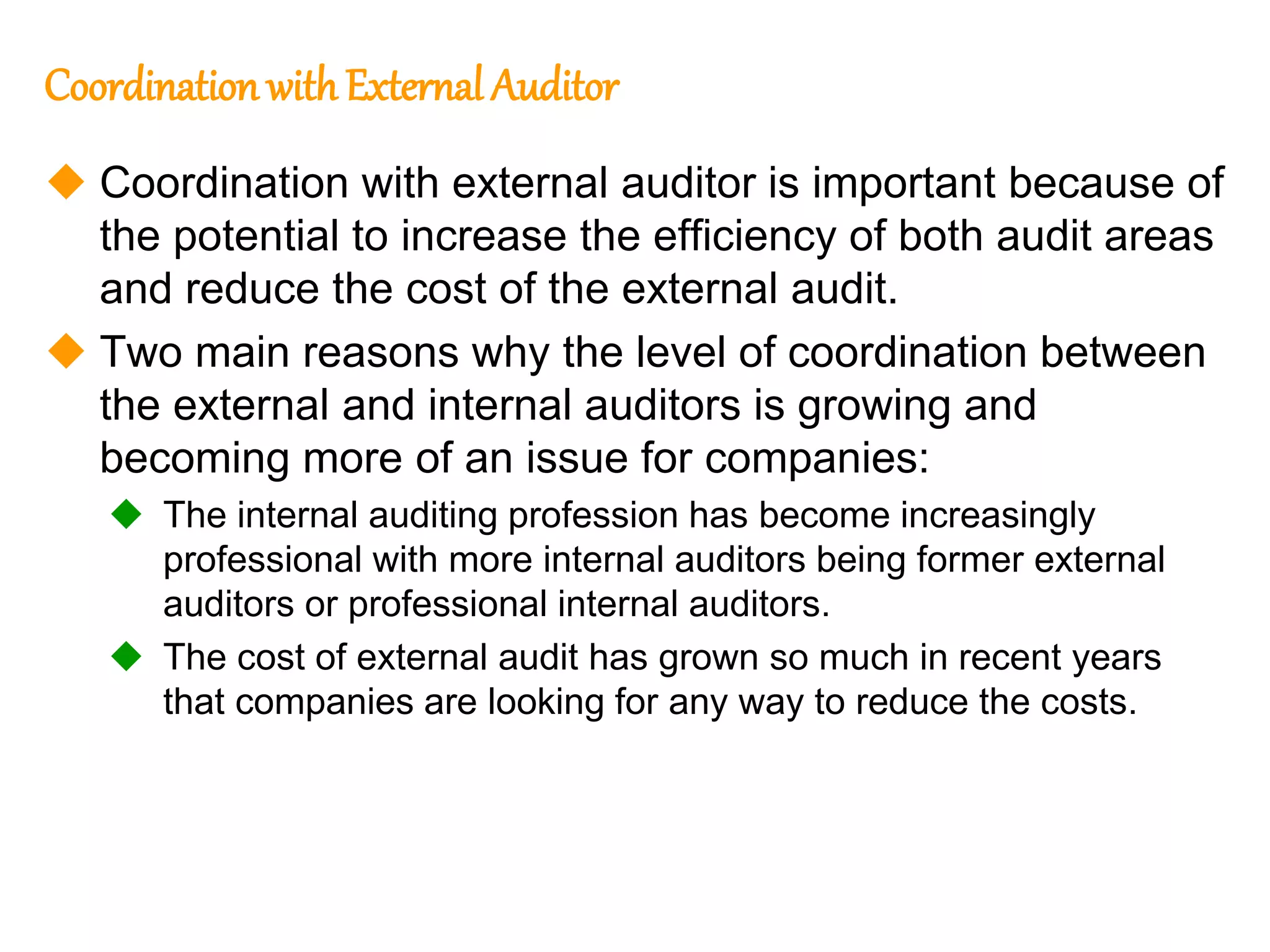

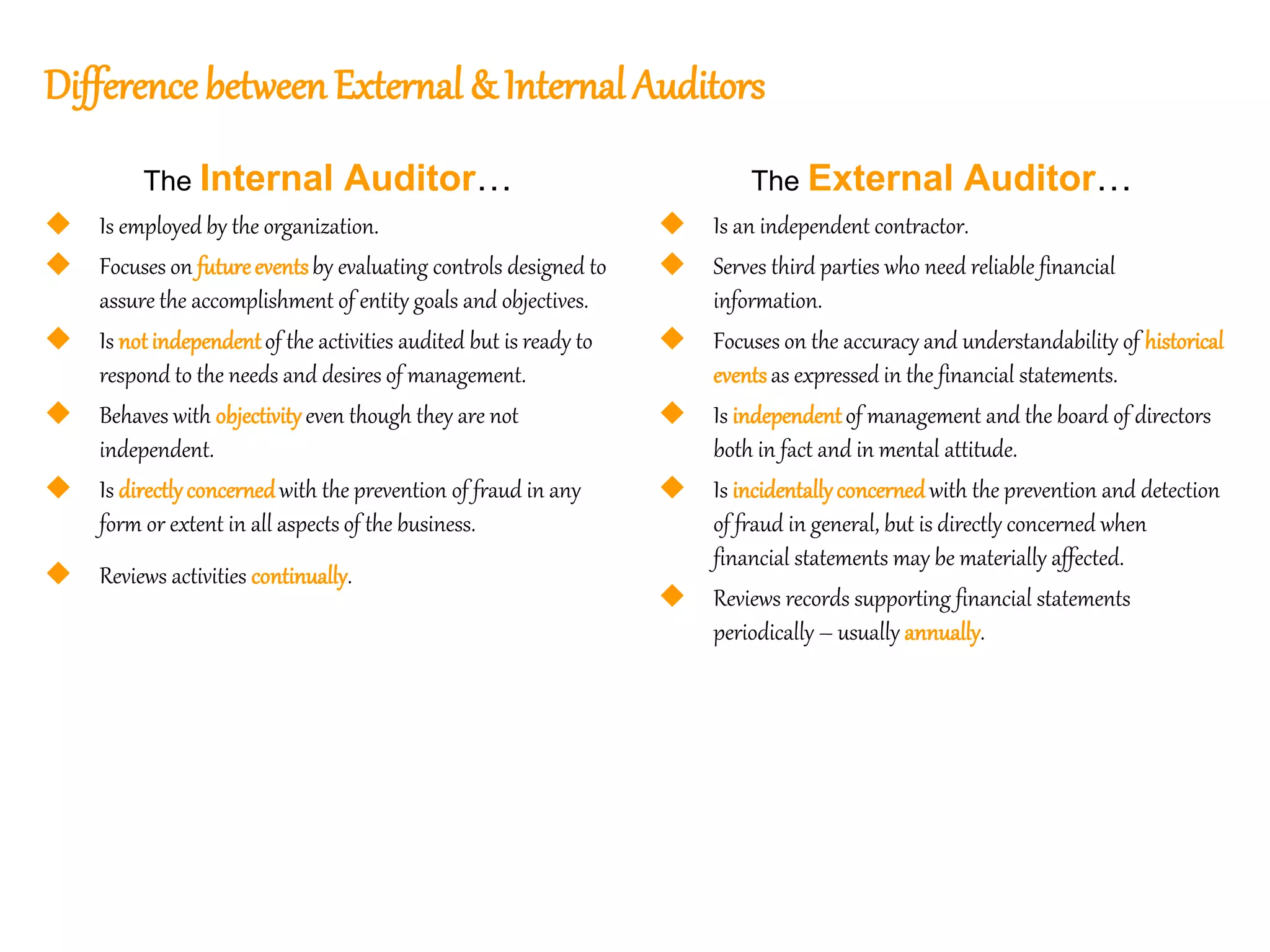

- Internal auditors differ from external auditors in that they are employed by the organization and focus on evaluating controls to assure goals, while external auditors are independent contractors focused on financial statements.

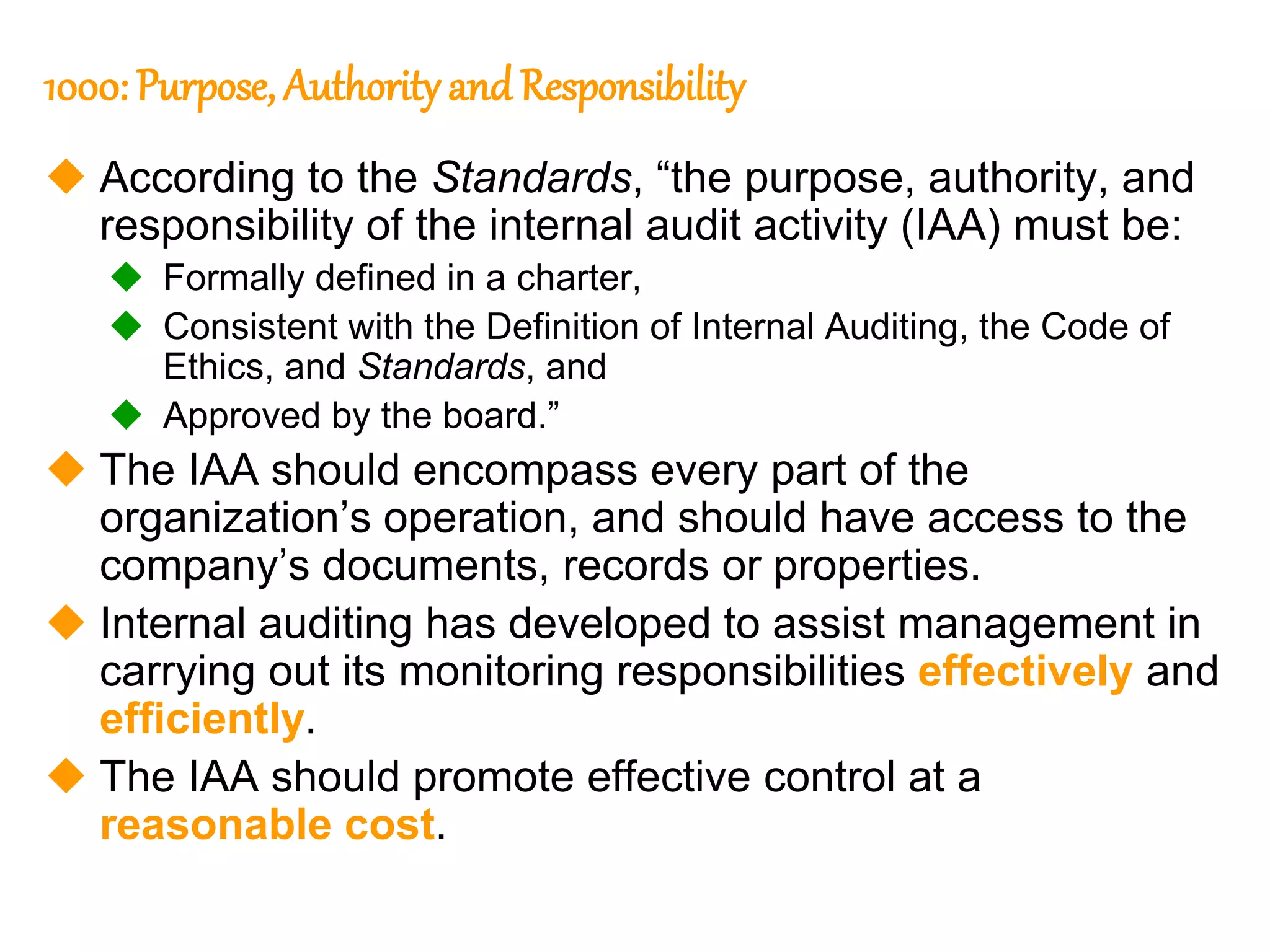

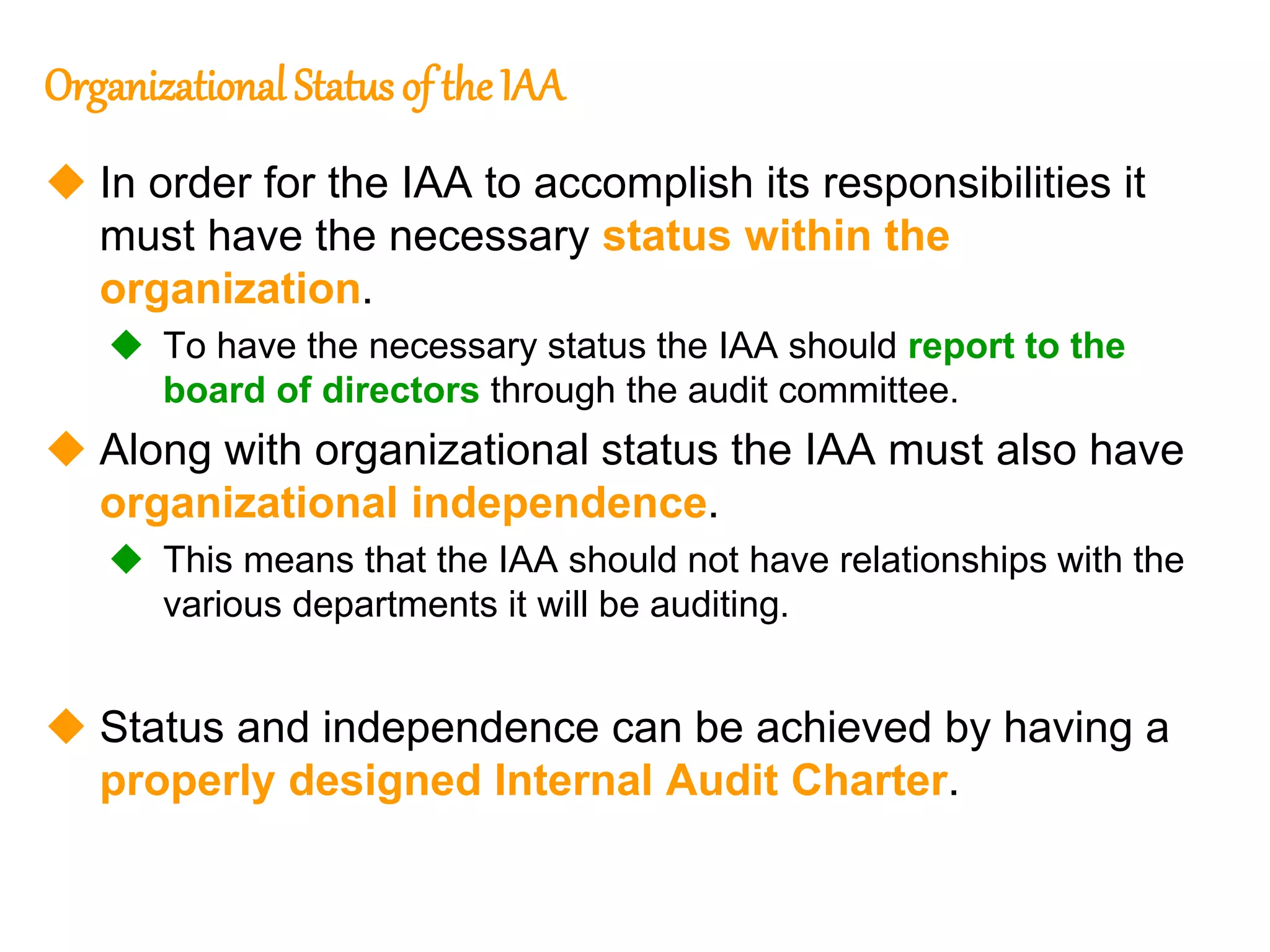

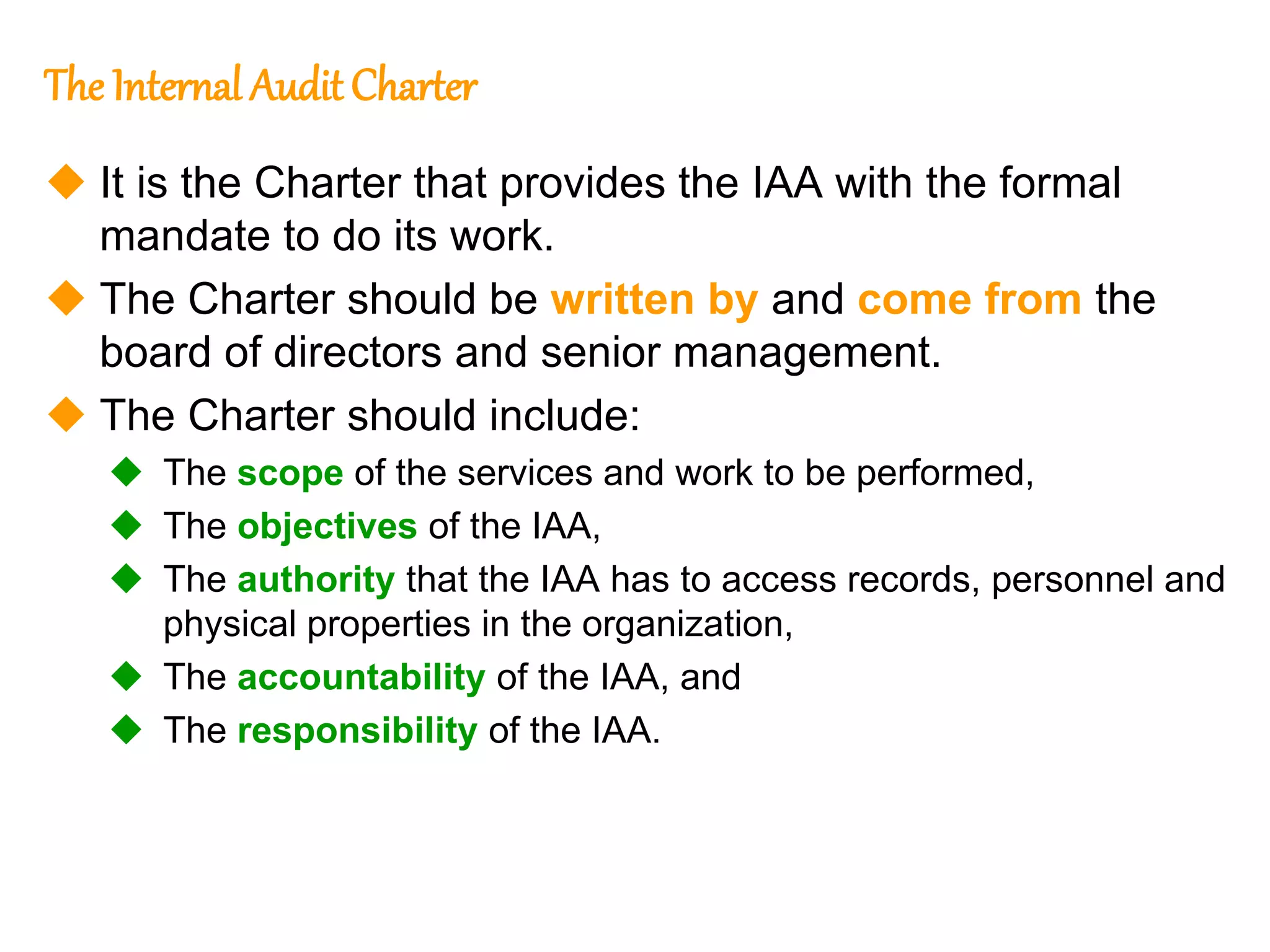

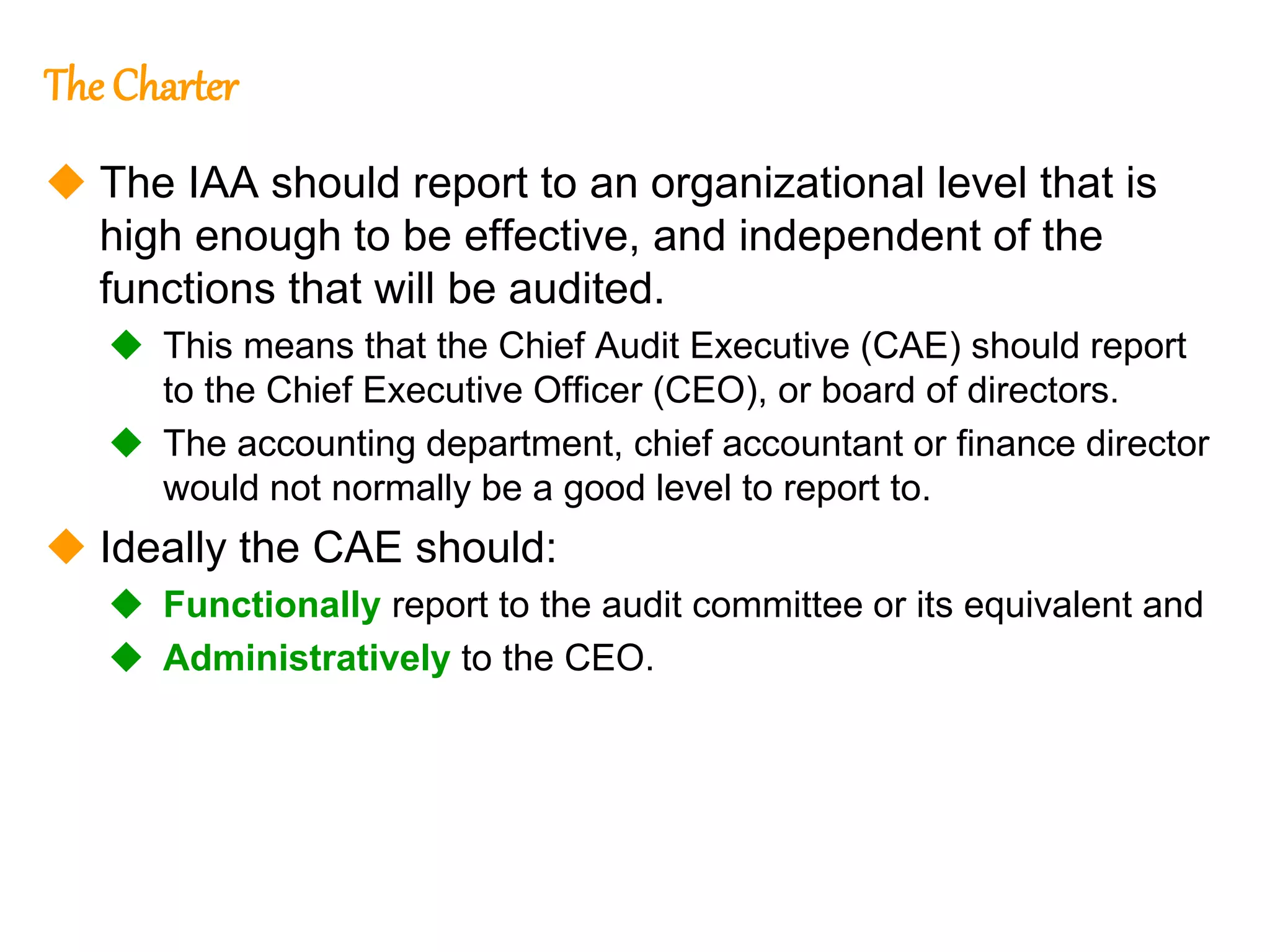

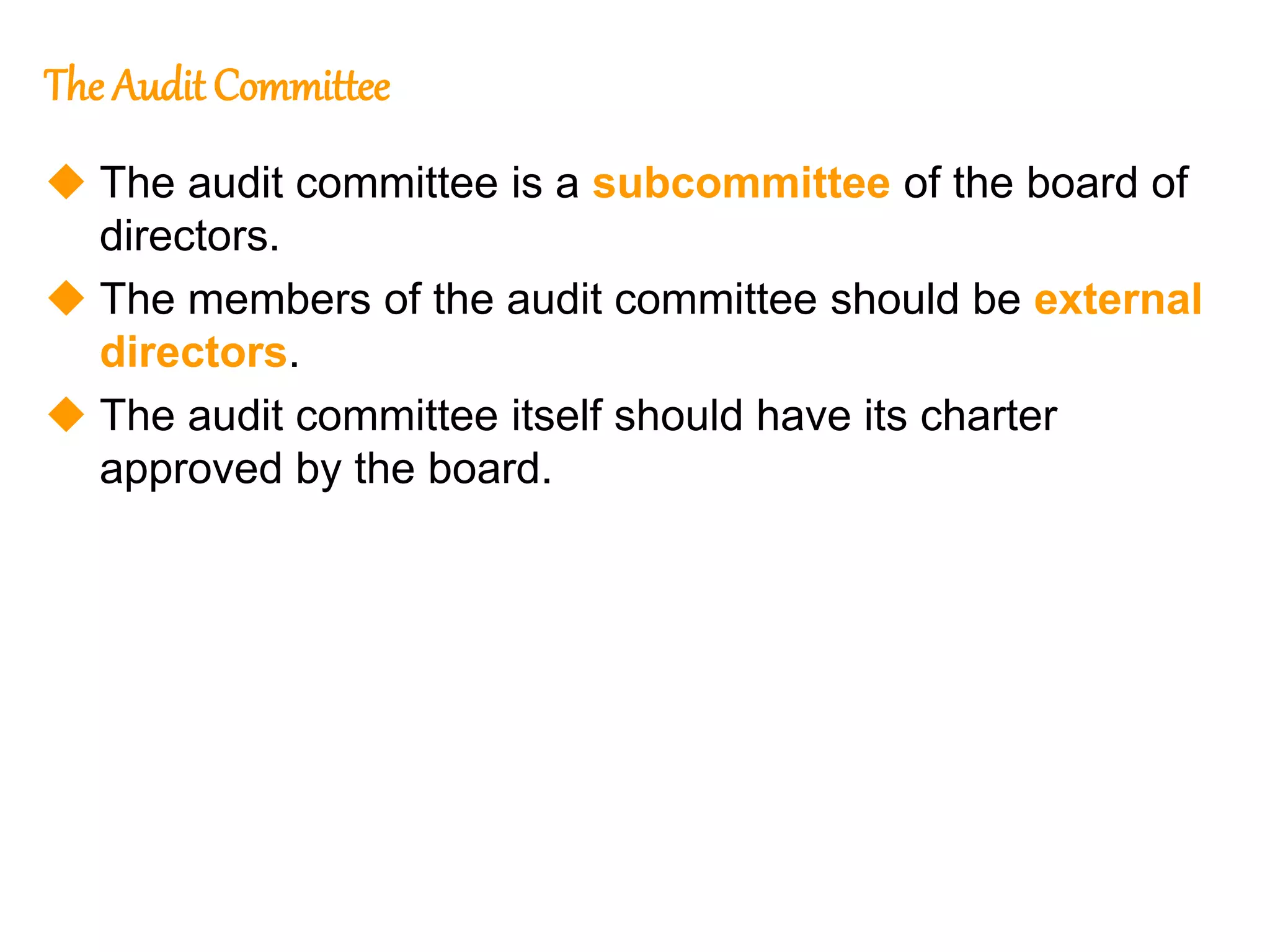

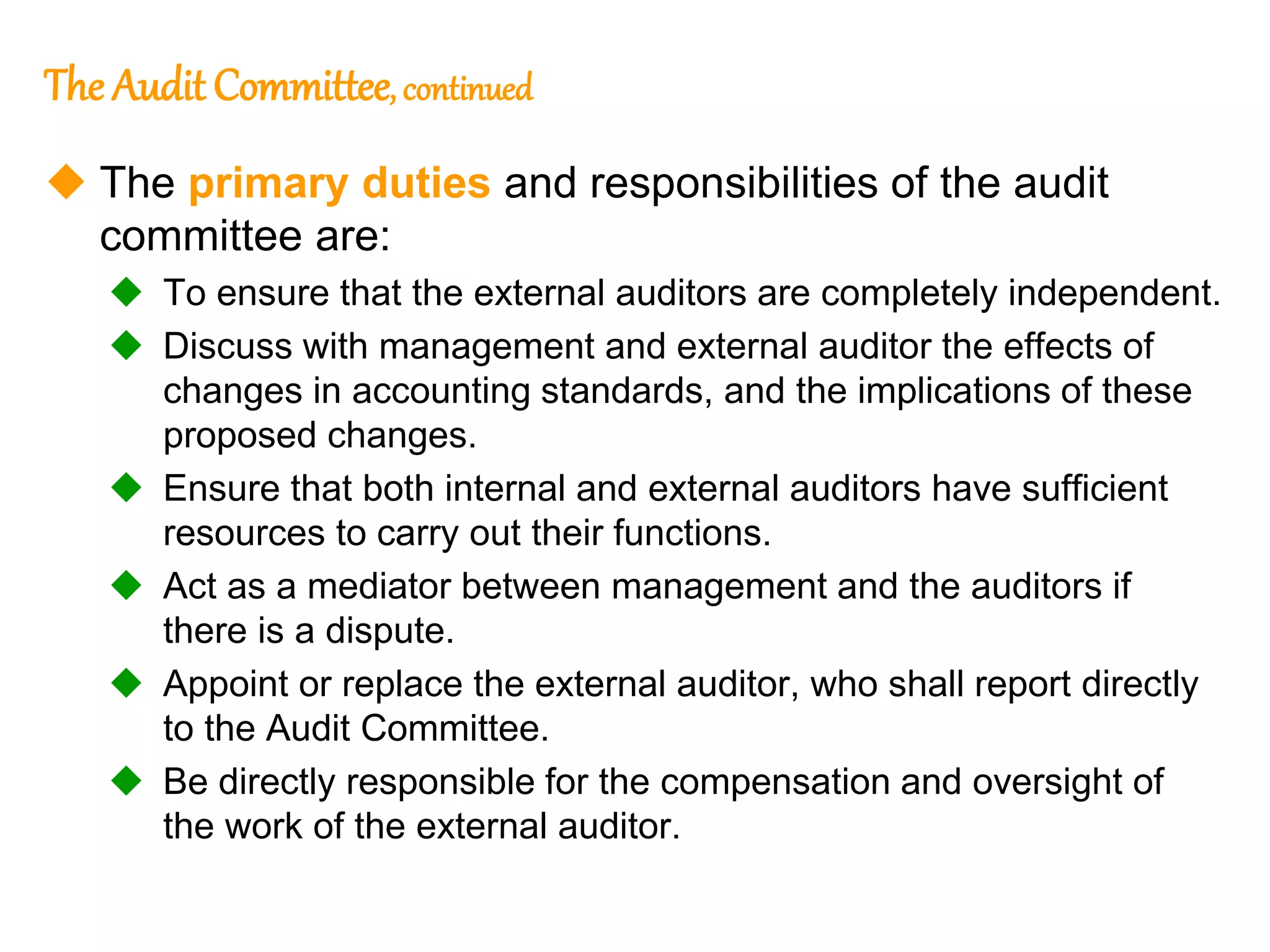

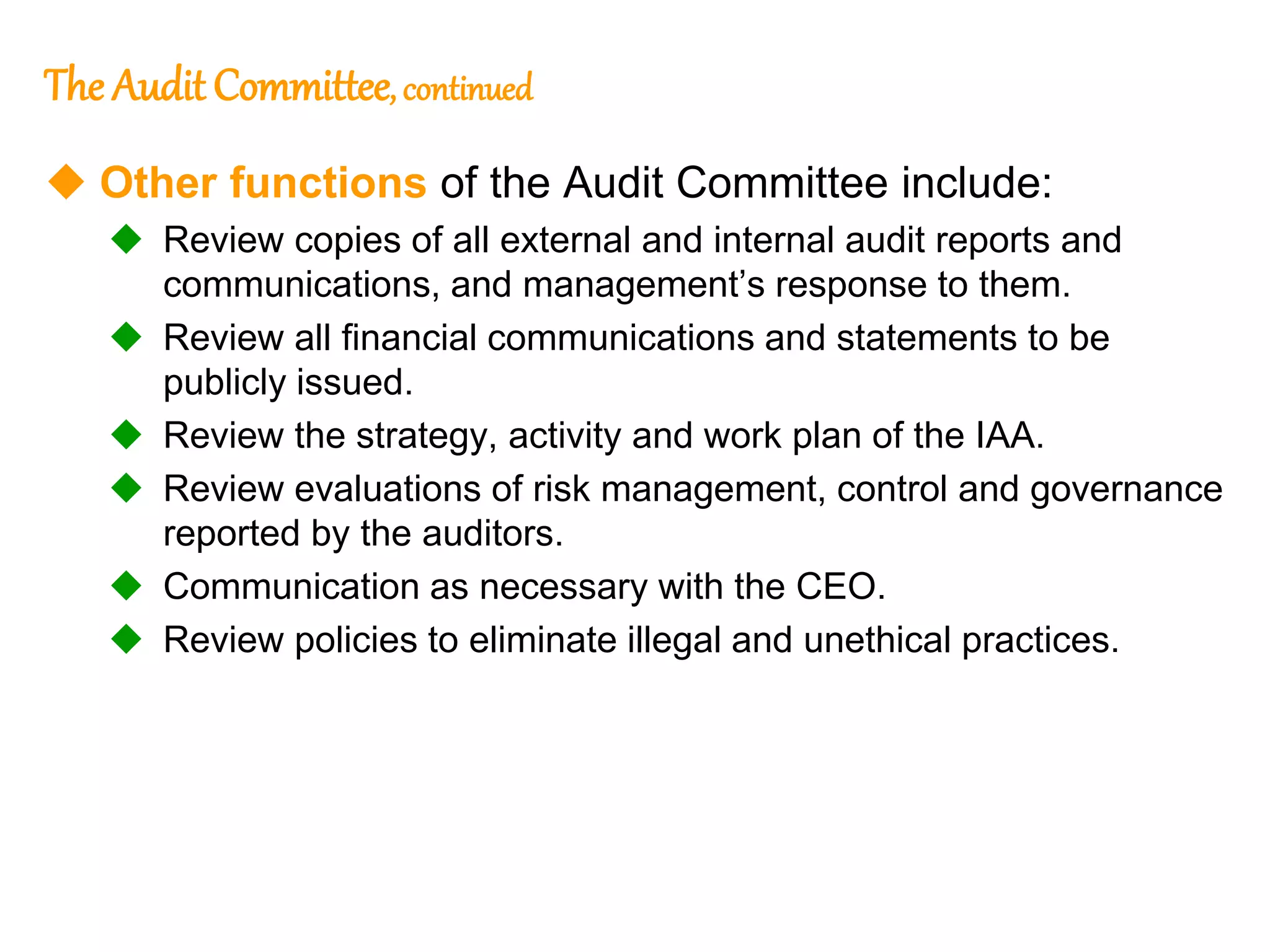

- An internal audit charter formally defines the internal audit activity's purpose, authority, and responsibilities as approved by the board. The charter establishes the activity's independence,

![53

53

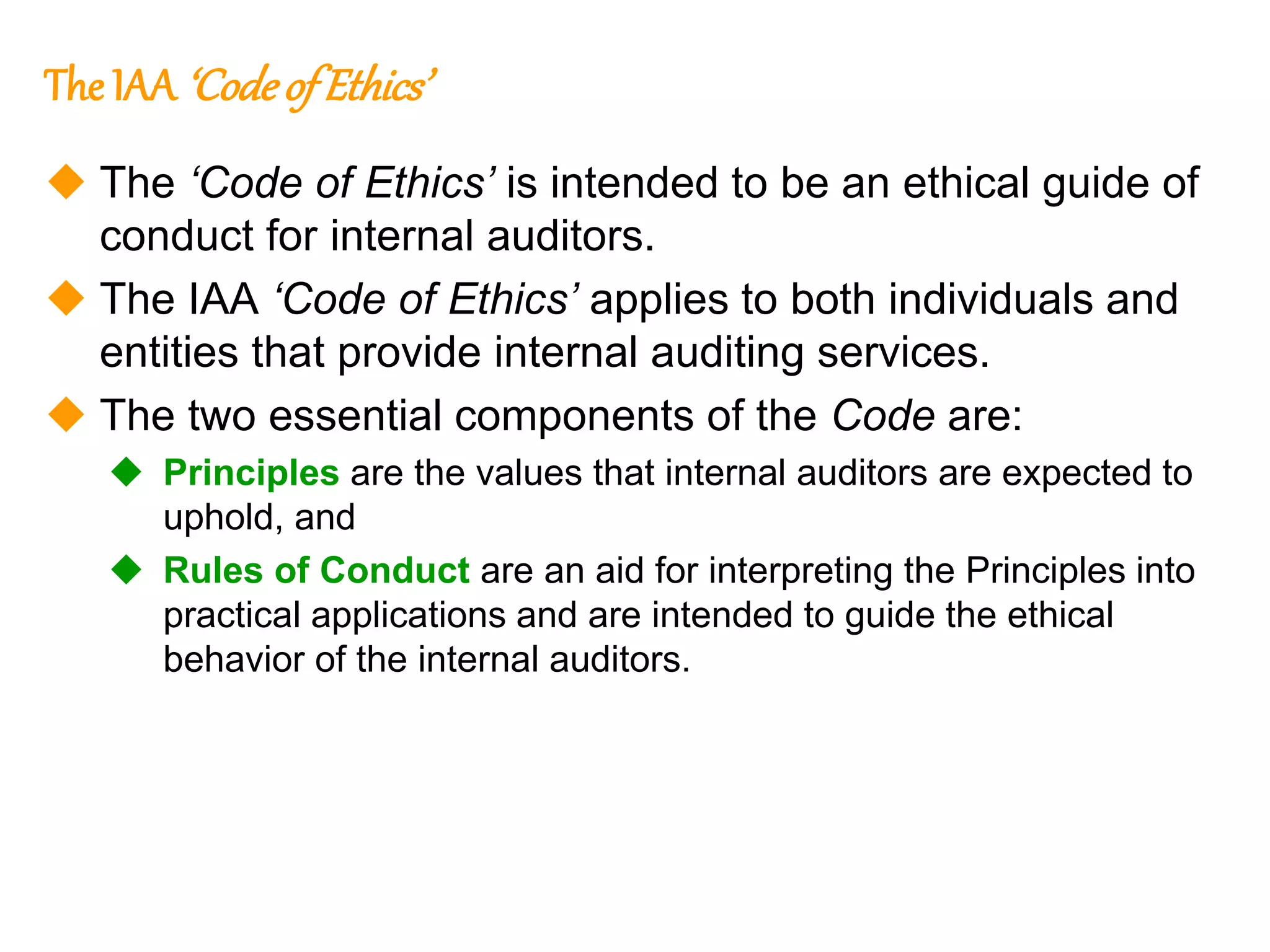

Rulesof Conduct

1. Integrity - Internal auditors:

1.1. Shall perform their work with honesty, diligence, and responsibility. [In other words,

the auditor does the right thing.]

1.2. Shall observe the law and make disclosures expected by

the law and the profession.

1.3. Shall not knowingly by a party to any illegal activity, or

engage in acts that are discreditable to the profession of internal

auditing or to the organization.

1.4. Shall respect and contribute to the legitimate and ethical

objectives of the organization.](https://image.slidesharecdn.com/vdocuments-230130044447-e1891447/75/vdocuments-mx_cia-part-1-slides-ppt-53-2048.jpg)

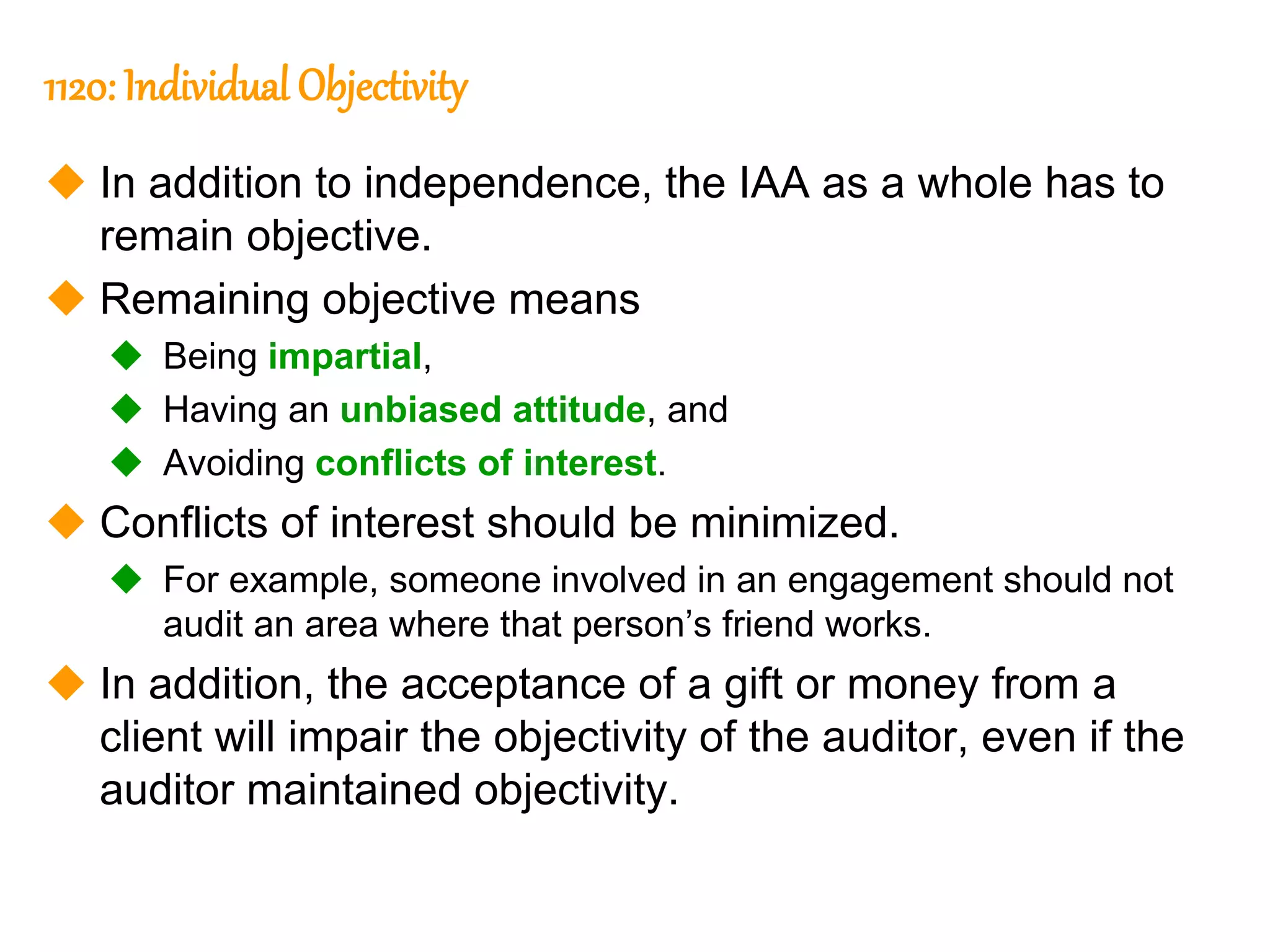

![54

54

Rulesof Conduct

2. Objectivity – Internal auditors:

2.1. Shall not participate in any activity or relationship that may impair or be presumed to

impair their unbiased assessment. This participation includes those activities or relationships

that may be in conflict with the interests of the organization.

2.2. Shall not accept anything that may impair or be presumed to impair their professional

judgment. [For example, a material gift (use of beach house) is considered to impair

objectivity.]

2.3. Shall disclose all material facts known to them that, if not disclosed, may distort the

reporting of activities under review. [For example, there may be some items that were

capitalized instead of expensed. This fact needs to be disclosed to management and the Audit

Committee.]](https://image.slidesharecdn.com/vdocuments-230130044447-e1891447/75/vdocuments-mx_cia-part-1-slides-ppt-54-2048.jpg)