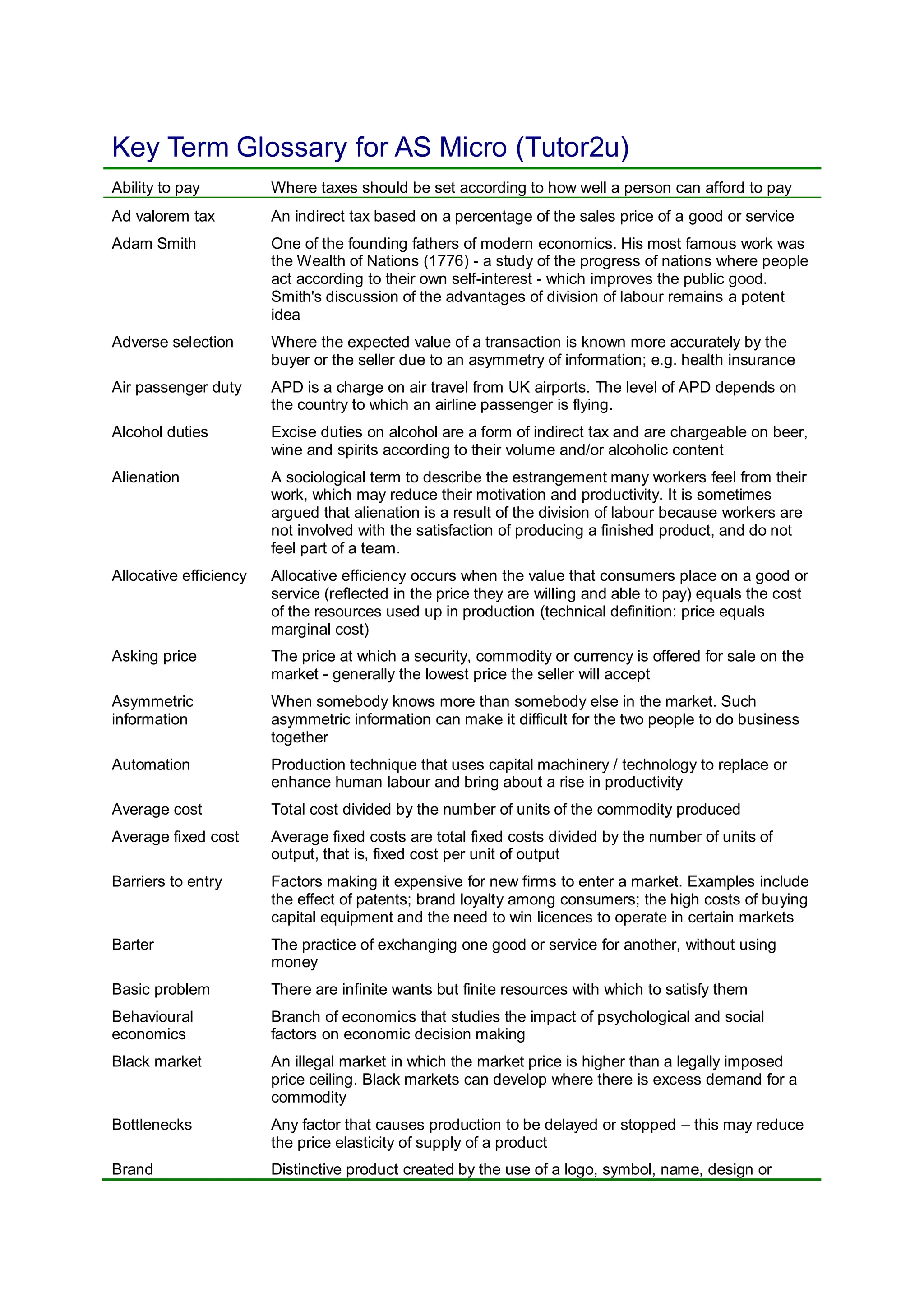

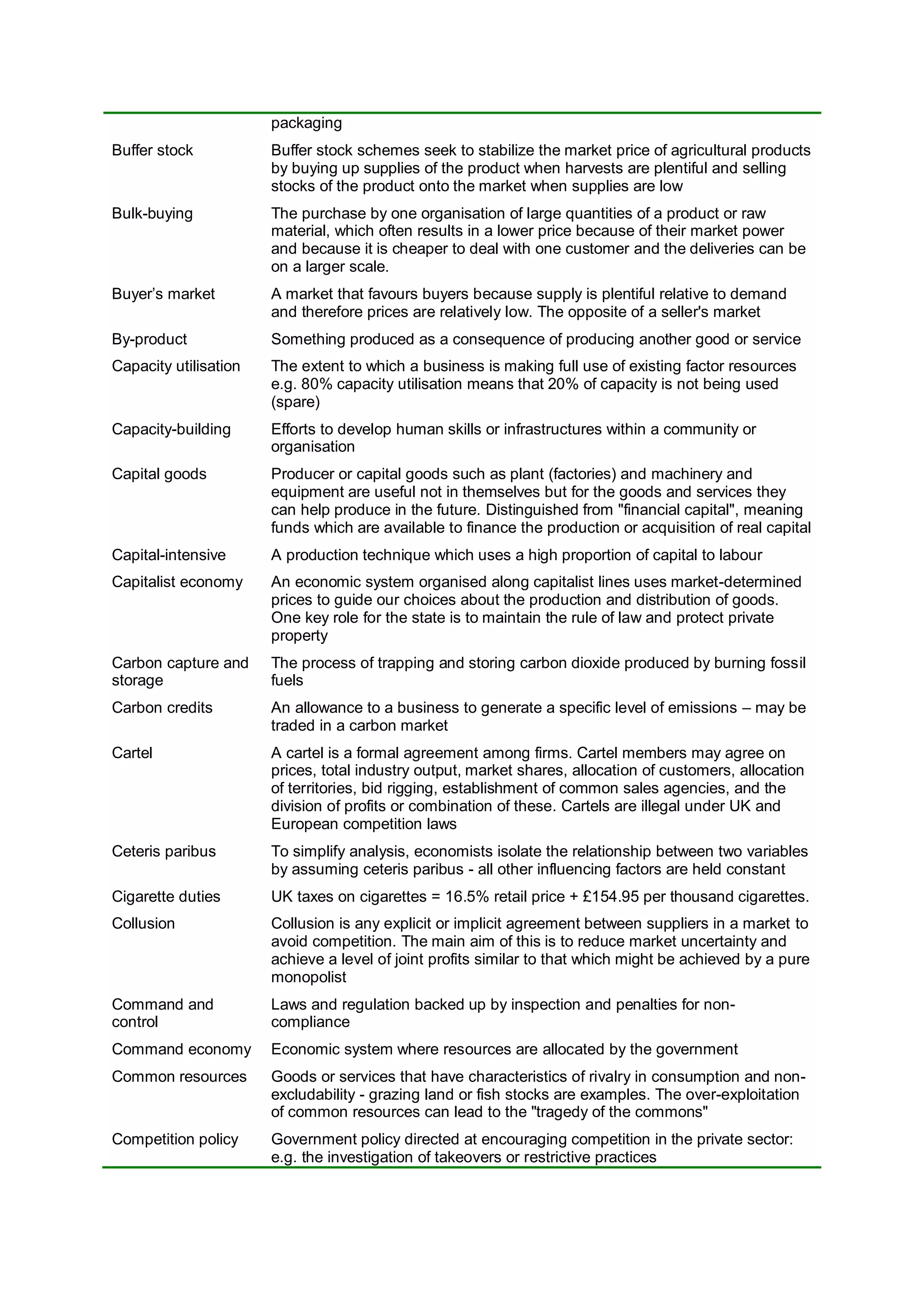

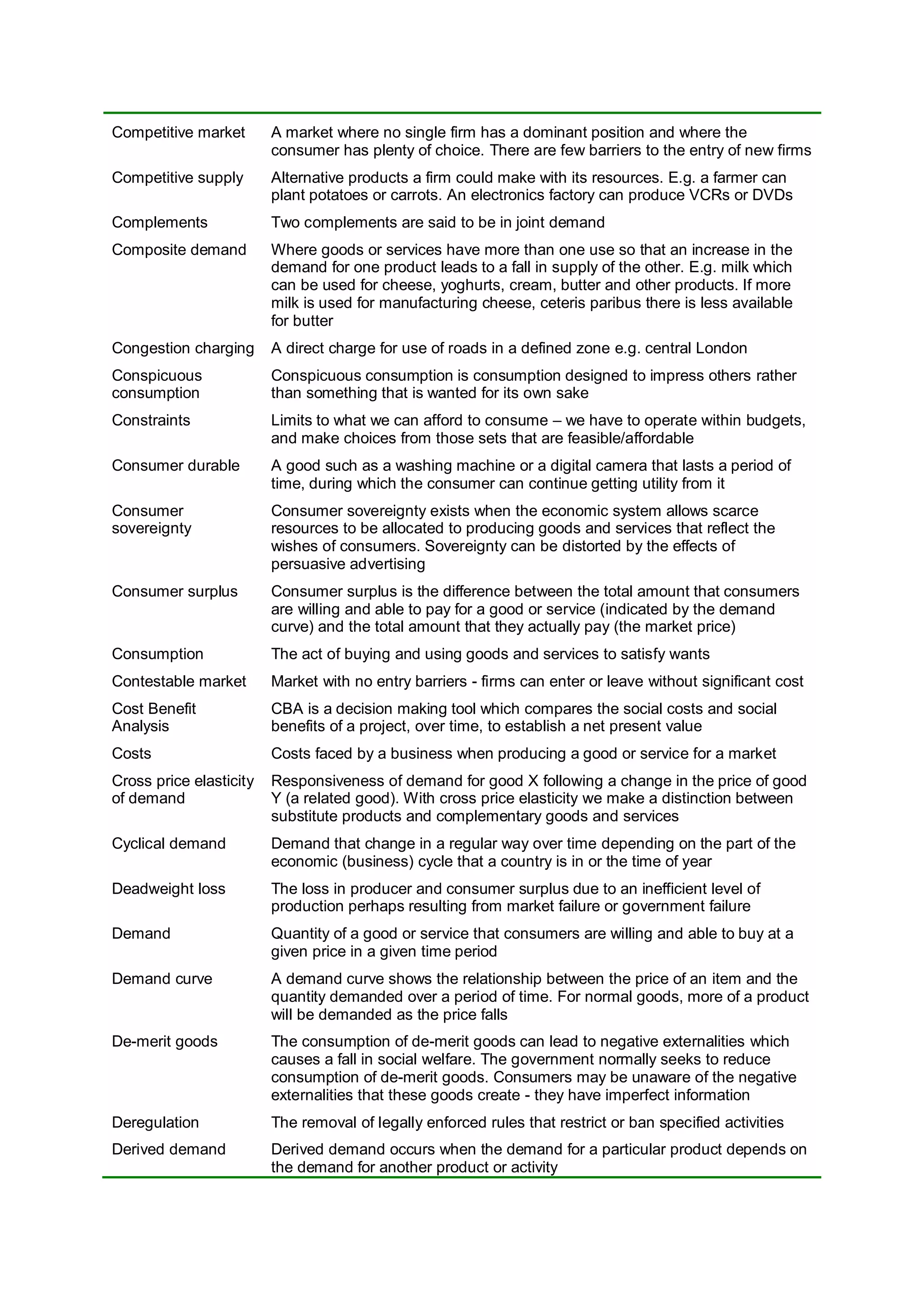

This document provides definitions for key economic terms used in AS Microeconomics. It defines terms such as ability to pay, Adam Smith, adverse selection, allocative efficiency, asymmetric information, barriers to entry, bottlenecks, command and control, consumer surplus, costs, deadweight loss, demand, division of labour, equilibrium, externalities, factors of income, firm, government failure, incentives, income, indirect tax, and information failure. In total, over 100 economic terms are defined in brief but clear explanations.