Genmo Corporation*

On the night of February 27, 2012, certain records of the Genmo Corporation were accidentally

destroyed by fire. Two days after that the principal owner had an appointment with an investor to

discuss the possible sale of the company. The owner needed as much information as could be

gathered for this purpose, recognizing that over a longer period of time a more complete

reconstruction would be possible.

On the morning of February 28, the following were available: (1) A balance sheet as of

December 31, 2010, and an income statement for 2010 (Exhibit 1) and (2) certain fragmentary

data and ratios that had been calculated from the current financial statements (Exhibit 2). The

statements themselves had been destroyed in the fire. (In ratios involving balance sheet amounts,

Genmo used yearend amounts rather than an average.) And (3) the following data (in thousands):

2011 revenues.............................................................. $10,281

Current liabilities, December 31, 2011 ......................... 2,285

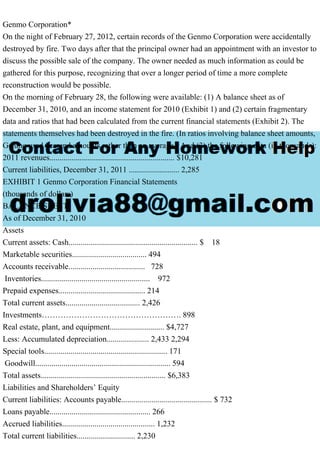

EXHIBIT 1 Genmo Corporation Financial Statements

(thousands of dollars)

BALANCE SHEET

As of December 31, 2010

Assets

Current assets: Cash................................................................ $ 18

Marketable securities..................................... 494

Accounts receivable...................................... 728

Inventories...................................................... 972

Prepaid expenses........................................... 214

Total current assets..................................... 2,426

Investments……………………………………………. 898

Real estate, plant, and equipment........................... $4,727

Less: Accumulated depreciation..................... 2,433 2,294

Special tools............................................................. 171

Goodwill................................................................... 594

Total assets.............................................................. $6,383

Liabilities and Shareholders’ Equity

Current liabilities: Accounts payable............................................. $ 732

Loans payable.................................................. 266

Accrued liabilities.............................................. 1,232

Total current liabilities............................. 2,230

Long-term debt.......................................................... 250

Other noncurrent liabilities......................................... 951

Total liabilities............................................................ 3,431

Shareholders’ equity: Preferred stock................................................. 25

Common stock................................................. 54

Additional paid-in capital.................................. 667

Retained earnings............................................ 2,206

Total shareholders’ equity....................... 2,952

Total liabilities and shareholders’ equity.................... $6,383

Income Statement, 2010

Total revenu.

Genmo CorporationOn the night of February 27, 2012, certain recor.pdf

1. Genmo Corporation*

On the night of February 27, 2012, certain records of the Genmo Corporation were accidentally

destroyed by fire. Two days after that the principal owner had an appointment with an investor to

discuss the possible sale of the company. The owner needed as much information as could be

gathered for this purpose, recognizing that over a longer period of time a more complete

reconstruction would be possible.

On the morning of February 28, the following were available: (1) A balance sheet as of

December 31, 2010, and an income statement for 2010 (Exhibit 1) and (2) certain fragmentary

data and ratios that had been calculated from the current financial statements (Exhibit 2). The

statements themselves had been destroyed in the fire. (In ratios involving balance sheet amounts,

Genmo used yearend amounts rather than an average.) And (3) the following data (in thousands):

2011 revenues.............................................................. $10,281

Current liabilities, December 31, 2011 ......................... 2,285

EXHIBIT 1 Genmo Corporation Financial Statements

(thousands of dollars)

BALANCE SHEET

As of December 31, 2010

Assets

Current assets: Cash................................................................ $ 18

Marketable securities..................................... 494

Accounts receivable...................................... 728

Inventories...................................................... 972

Prepaid expenses........................................... 214

Total current assets..................................... 2,426

Investments……………………………………………. 898

Real estate, plant, and equipment........................... $4,727

Less: Accumulated depreciation..................... 2,433 2,294

Special tools............................................................. 171

Goodwill................................................................... 594

Total assets.............................................................. $6,383

Liabilities and Shareholders’ Equity

Current liabilities: Accounts payable............................................. $ 732

Loans payable.................................................. 266

Accrued liabilities.............................................. 1,232

Total current liabilities............................. 2,230

2. Long-term debt.......................................................... 250

Other noncurrent liabilities......................................... 951

Total liabilities............................................................ 3,431

Shareholders’ equity: Preferred stock................................................. 25

Common stock................................................. 54

Additional paid-in capital.................................. 667

Retained earnings............................................ 2,206

Total shareholders’ equity....................... 2,952

Total liabilities and shareholders’ equity.................... $6,383

Income Statement, 2010

Total revenues.......................................................... $9,779

Cost of sales (excluding depreciation and amortization)… $8,165

Depreciation........................................................................ 278

Amortization of goodwill and special tools.......................... 343 8,786

Selling, general, and administrative expenses................... 430

Provision for income taxes.................................................. 163

Total costs and expenses................................................... 9,379

Net income.......................................................................... $ 400

EXHIBIT 2 Selected Ratios

2011 2010

Acid-test ratio.......................................................................... 0.671 0.556

Current ratio ........................................................................... 1.172 1.088

Inventory turnover (times) .......................................................10.005 8.400

Days’ receivables.................................................................... 39.66 27.17

Gross margin percentage........................................................ 15.12 16.50

Profit margin percentage.......................................................... 2.831 4.090

Invested capital turnover (times) ............................................. 2.091 2.355

Debt/equity ratio (percentage) ................................................. 62.15 40.68

Return on shareholders’ equity.................................................. ? 13.55

Questions 1. Prepare a balance sheet as of December 31, 2011, and the 2011 income statement.

2. What was the return on shareholders’ equity for 2011?

Solution

1) Acid test ratio= cash+A/R+marketable security/Current liabilities

0.671 = cash+A/R+marketable security/2285

3. cash+A/R+marketable security=0.671*2285

cash+A/R+marketable security=1533.24

2) Current ratio= CA/CL

1.172=CA/2285

CA= 1.172*2285

CA= 2678.02

3) Days receivable ratio=closing A/R*365 divided by revenue

39.66=closing A/R*365/10281

closing A/R= 39.66*10281/365

closing A/R= 1117.11

4) Inventory turnover=COS/Average stock

10.005= 8726.51 (from point 5)/average stock

Average stock= 872.21

5) Gross margin=GP/revenue*100

15.12=Gross profit/10281*100

Gross profit=1554.49

COS= revenue-GP

10281-1554.49

=8726.51

6) Average stock =872.21

opening+closing stock/2 = 872.21

972+closing=872.21*2

closing stock= 772.42

7) CA= cash+marketable securit+A/R+inventory+Prepaid expense

2678.02=1533.24+772.42+prepaid expense

prepaid expense= 372.36

8) Net margin ration= net income/revenue*100

2.831= net income/10281*100

Net income=291.06

9) Invested capital ratio= Annual sales/average stockholder equity

2.091= 10281/average equity

average equity=4916.79

opening +closing equity/2=4916.79

2952+closing/2=4916.79

closing equity=6881.58

10) debt equity=long term debt/equity*100

4. 62.15=long term debt/6881.58*100

long term debt=4276.90

11) Return on equity= net income/equity

=291.06/6881.58*100

=4.23

Return on equity for 2011= 4.23 (see point no. 11)Balance SheetAs of december

31,2011AssetsCurrent Assets: Cash and marketable

securities416.13A/R1117.11Inventory772.42Prepaid expenses372.36Total current

assets2678.02Total non current assets10765.46Total assets 13443.48Liabilitie and shareholder

equity:Current liability2285non current liability4276.9Total liability6561.9Shareholder

equity6881.58Total Liabilitie and shareholder equity:13443.48