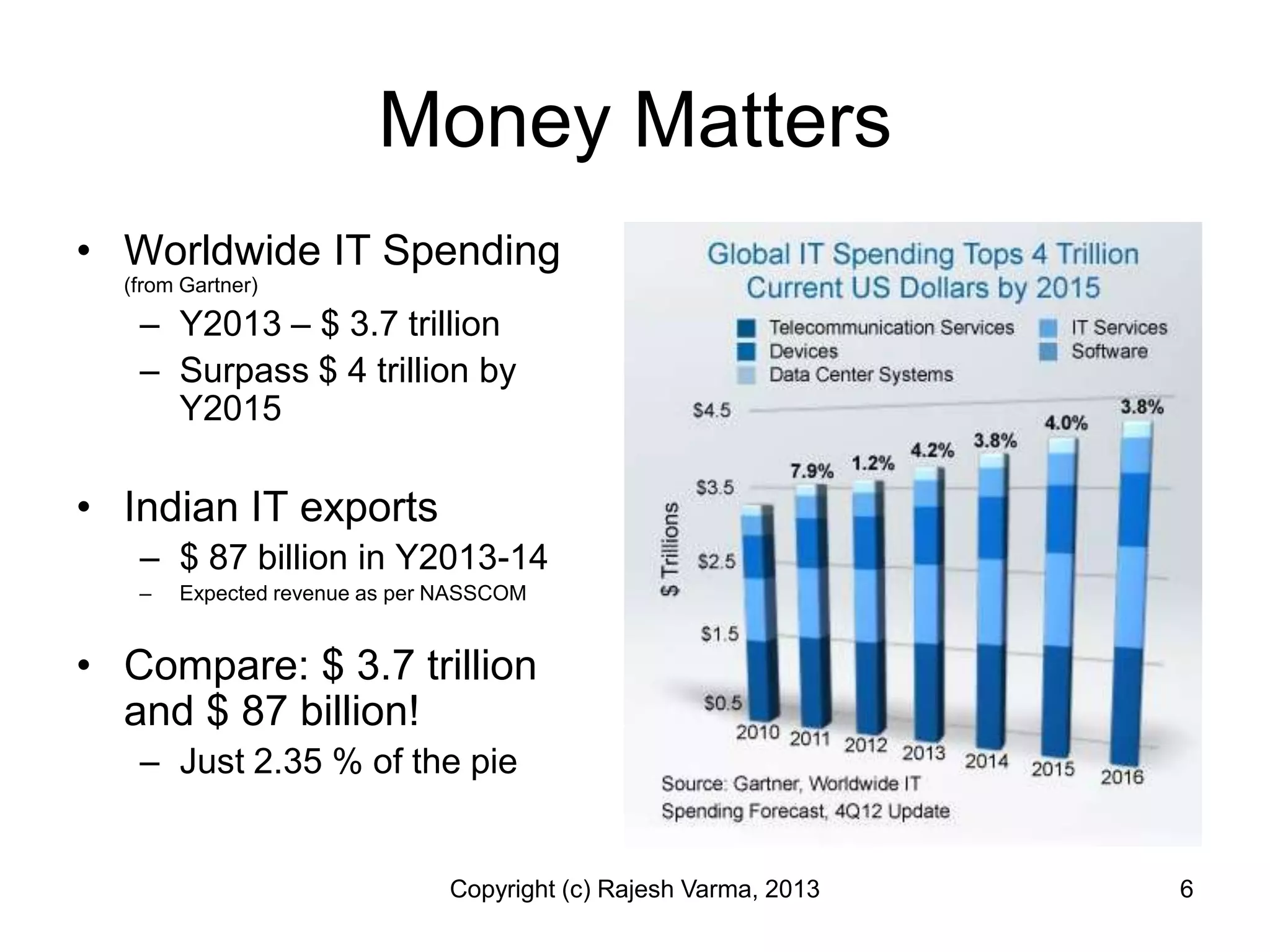

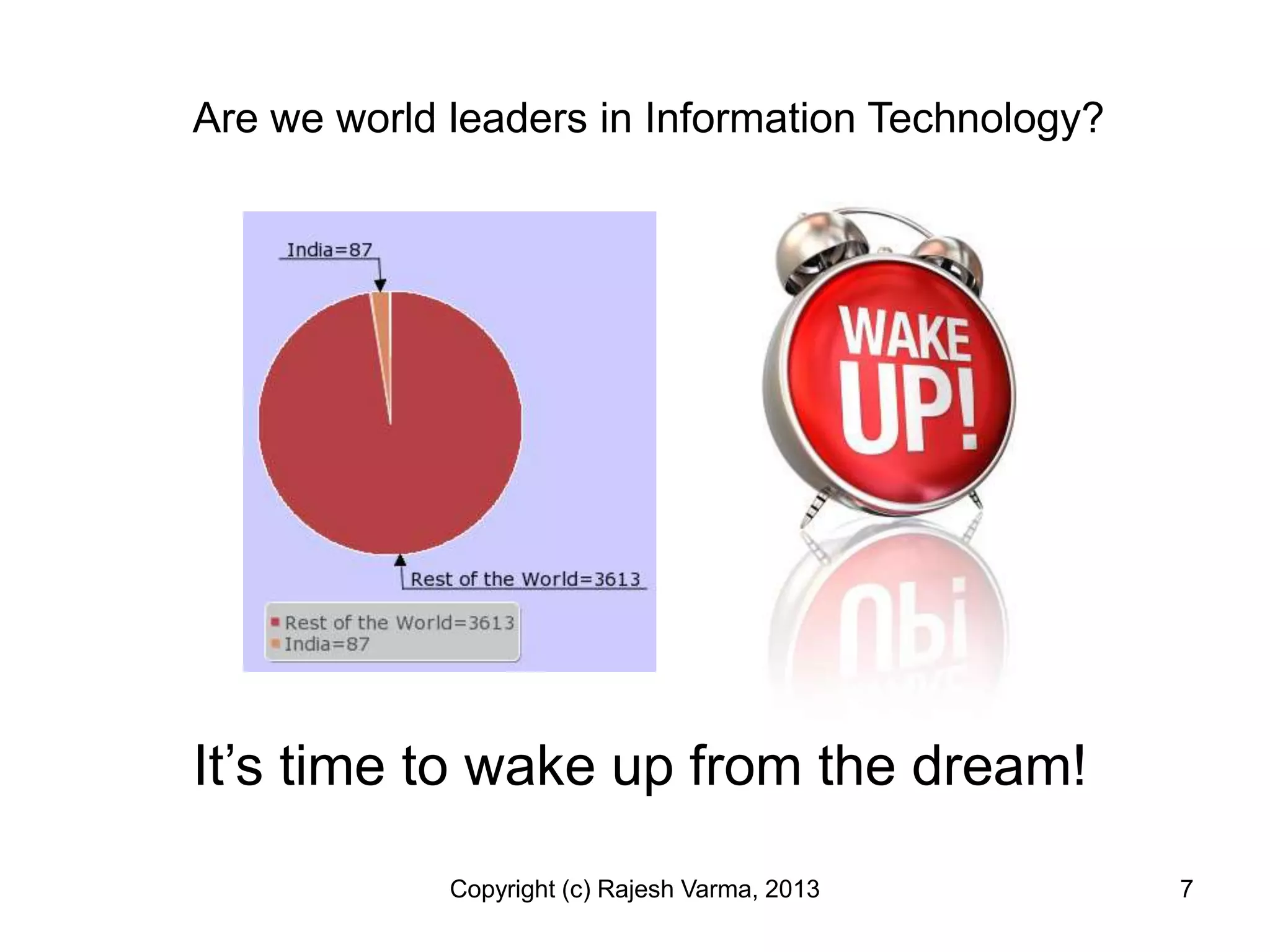

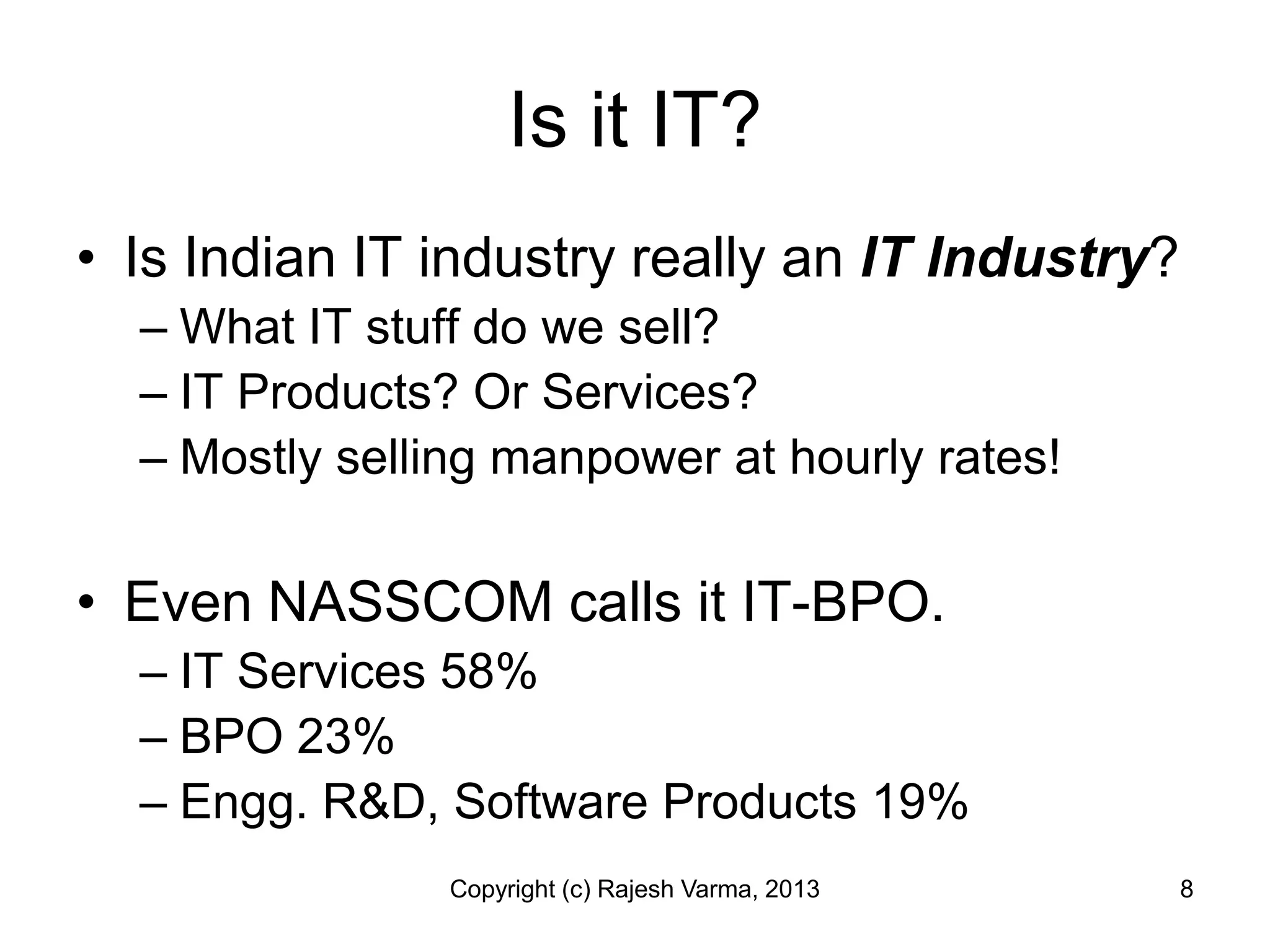

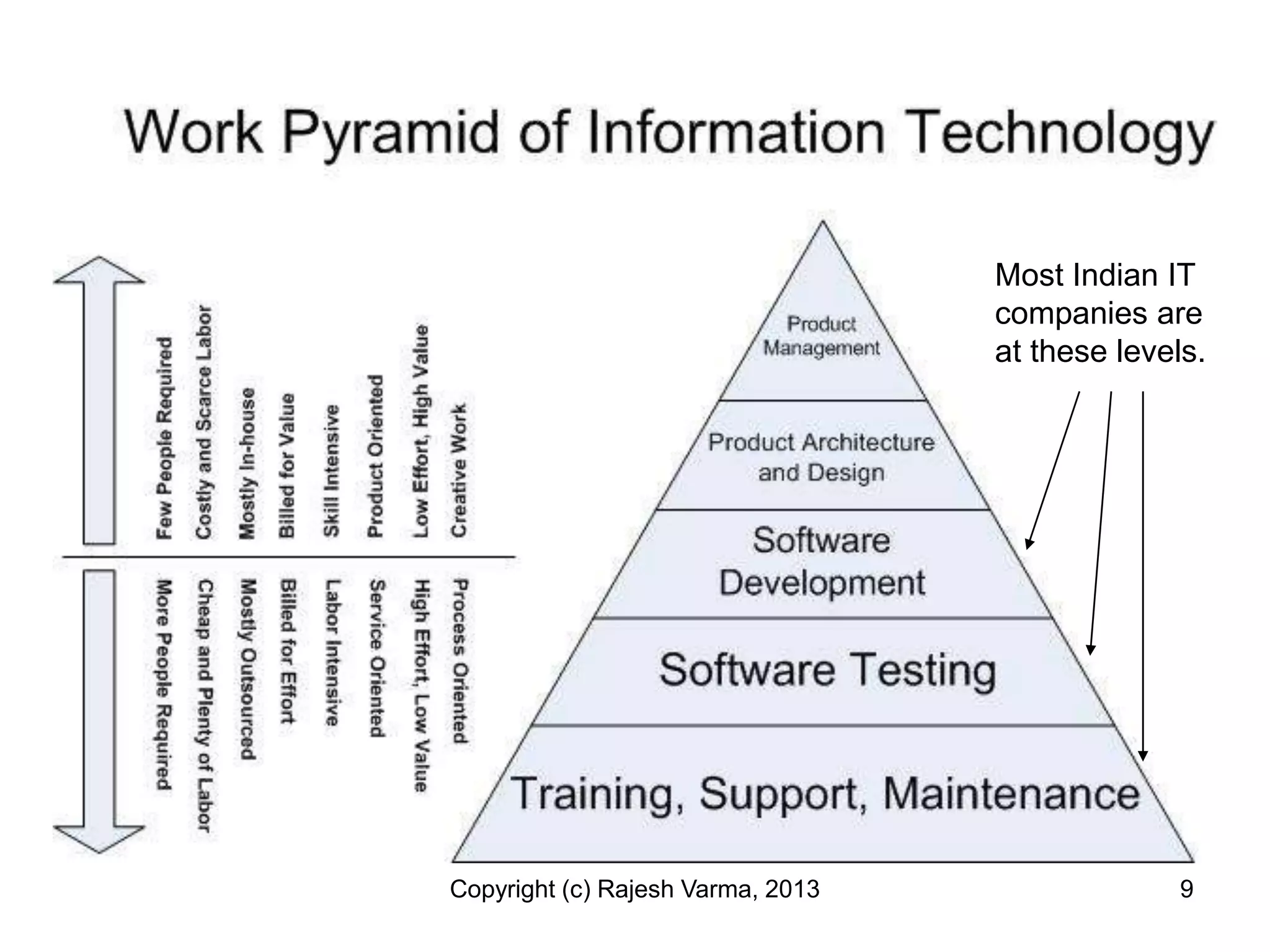

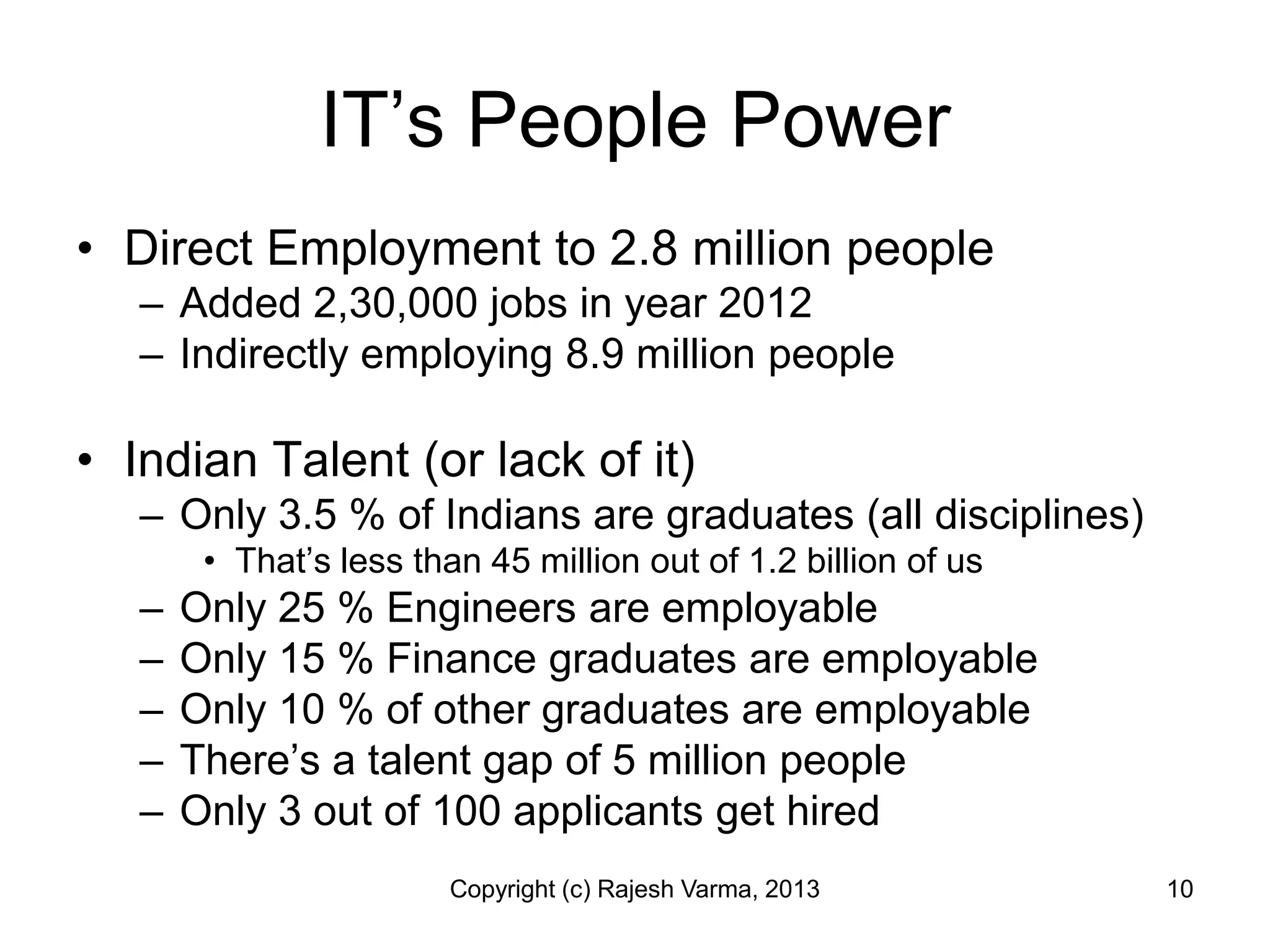

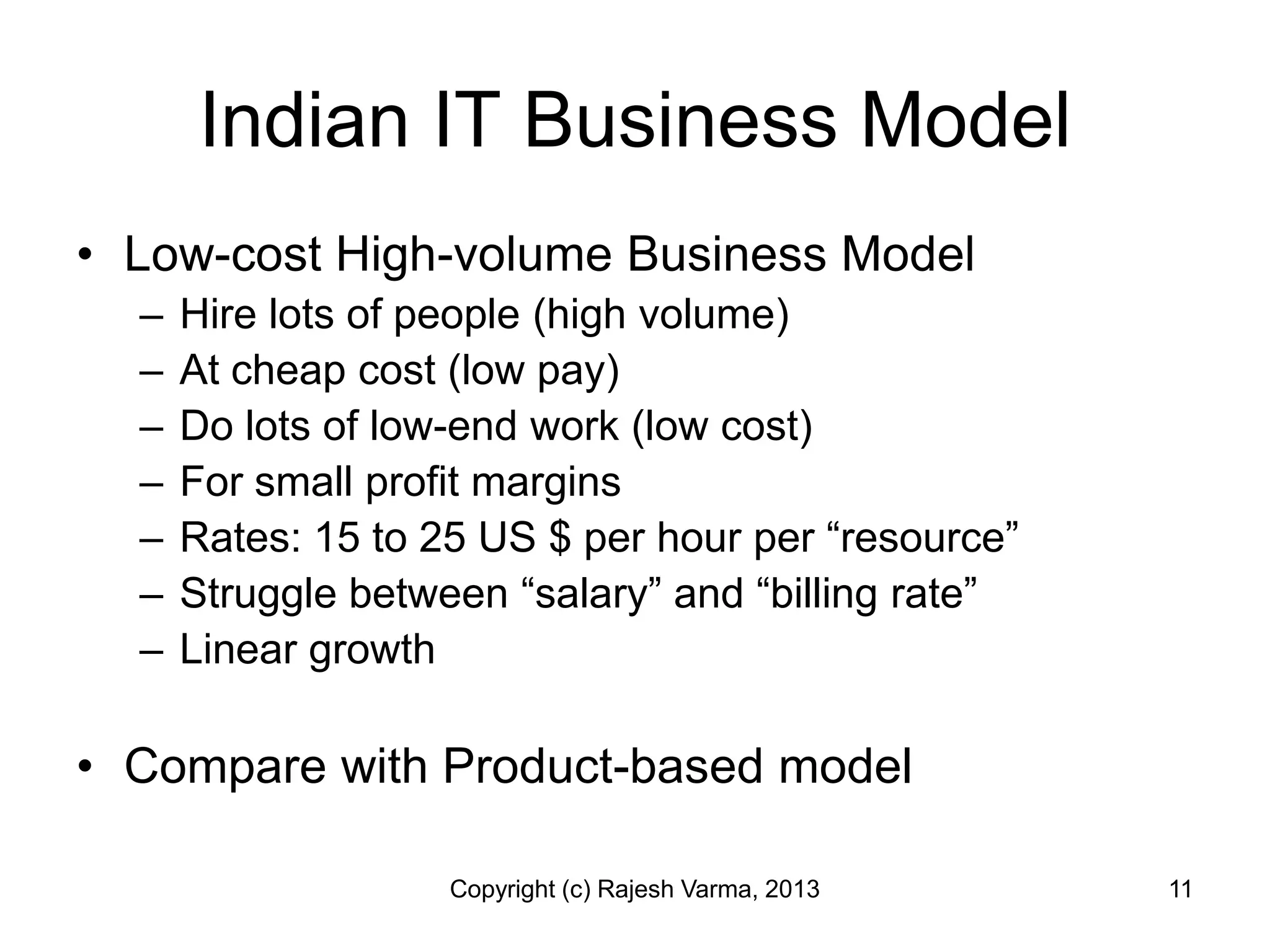

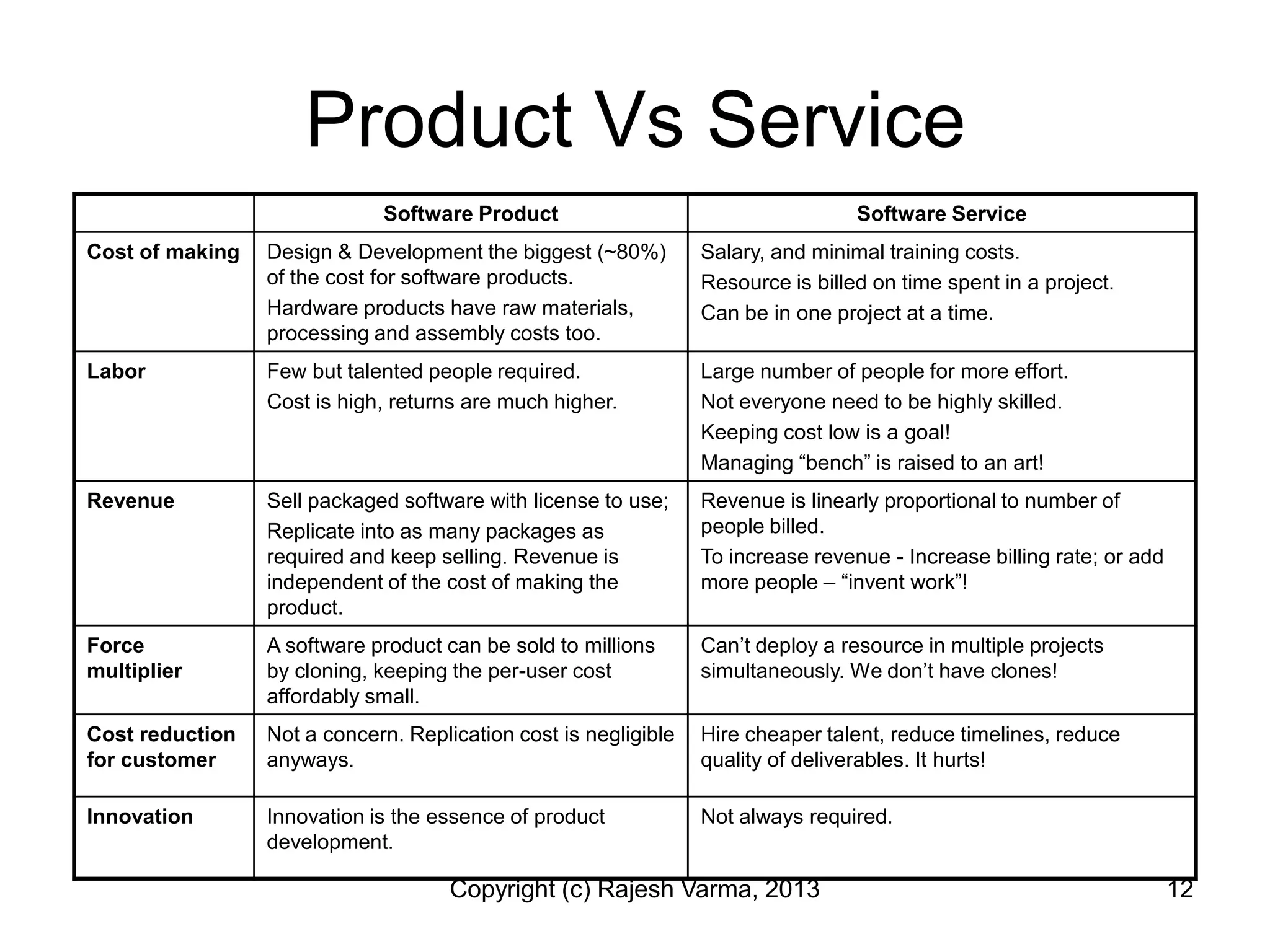

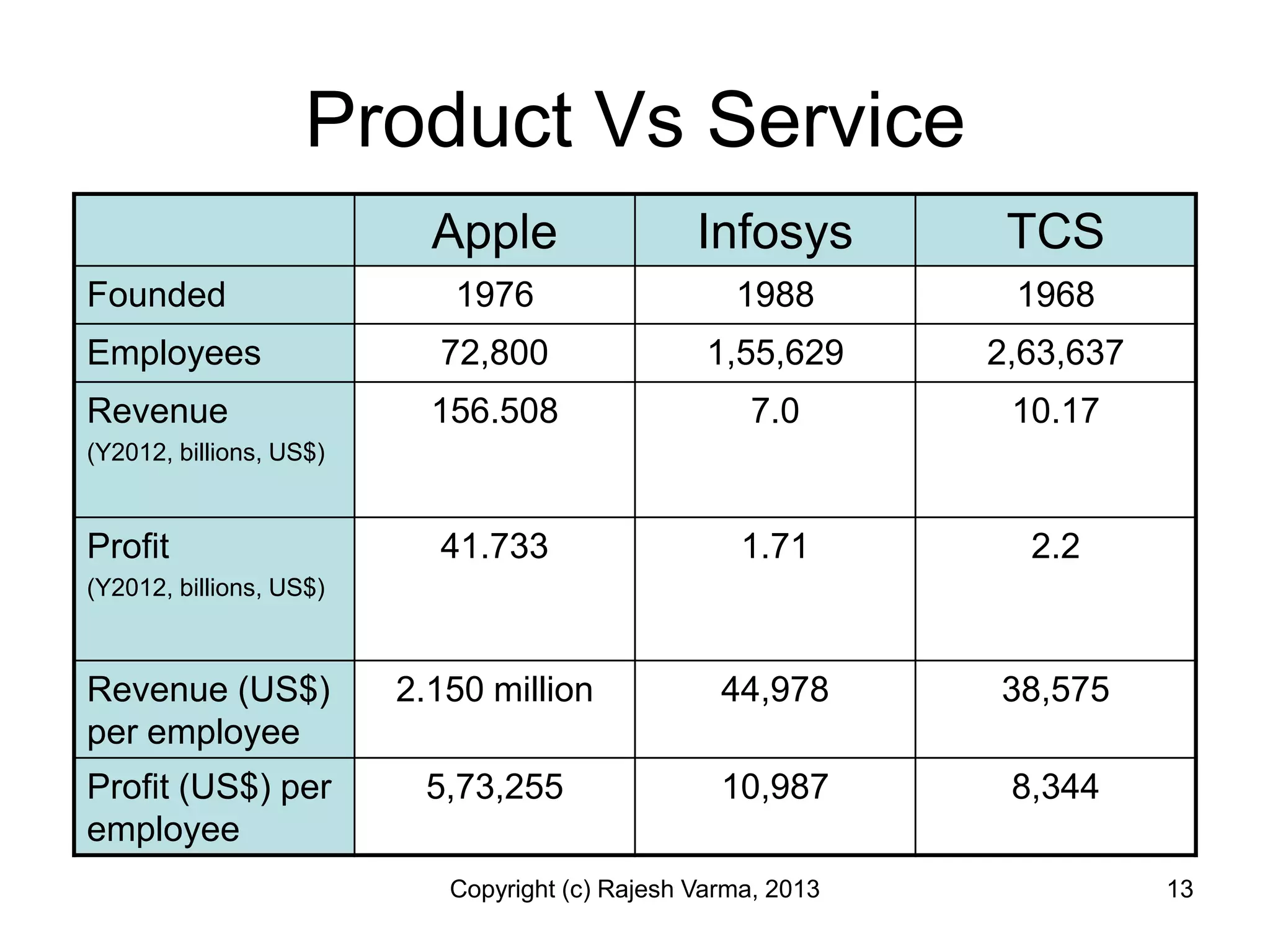

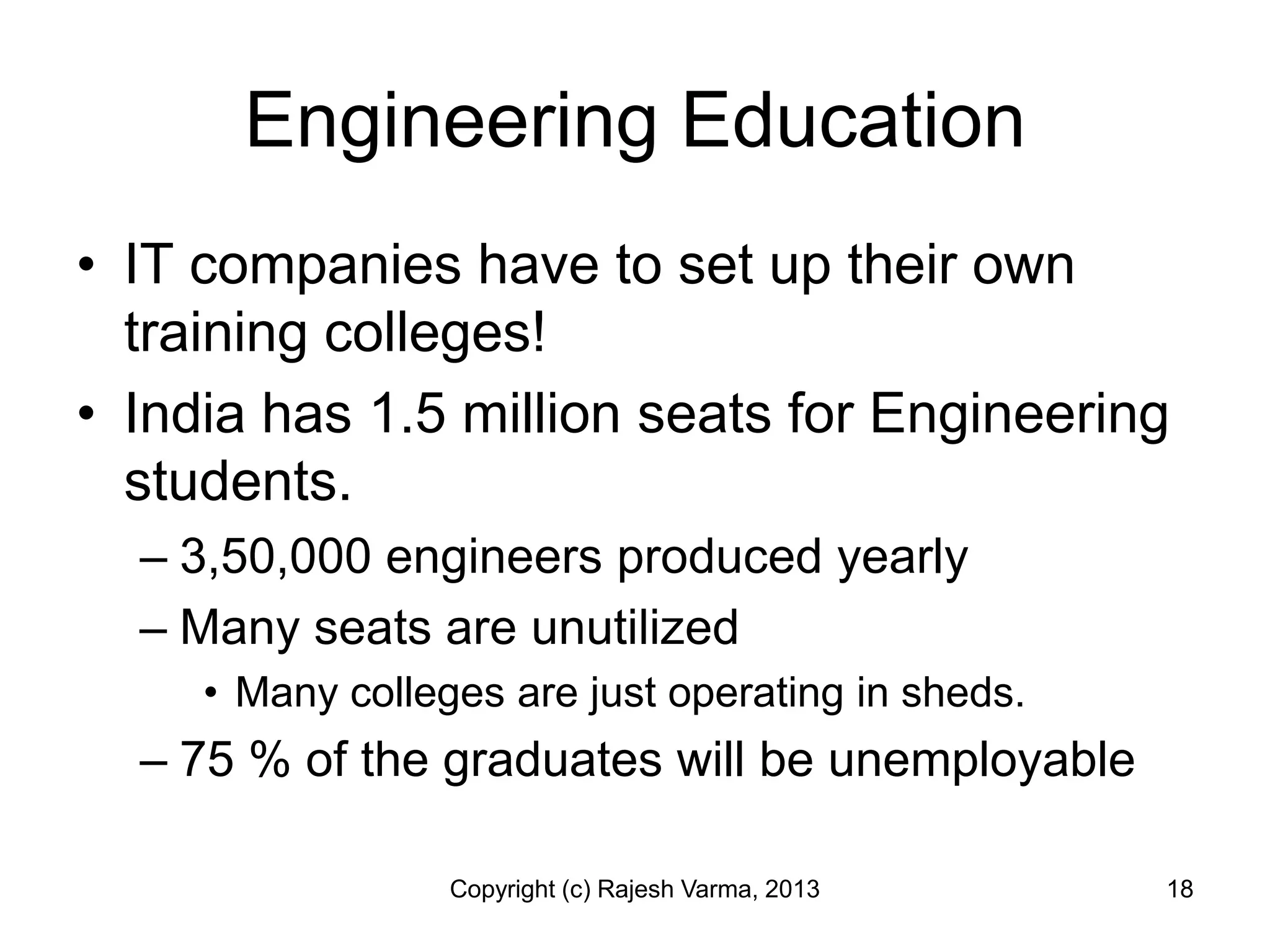

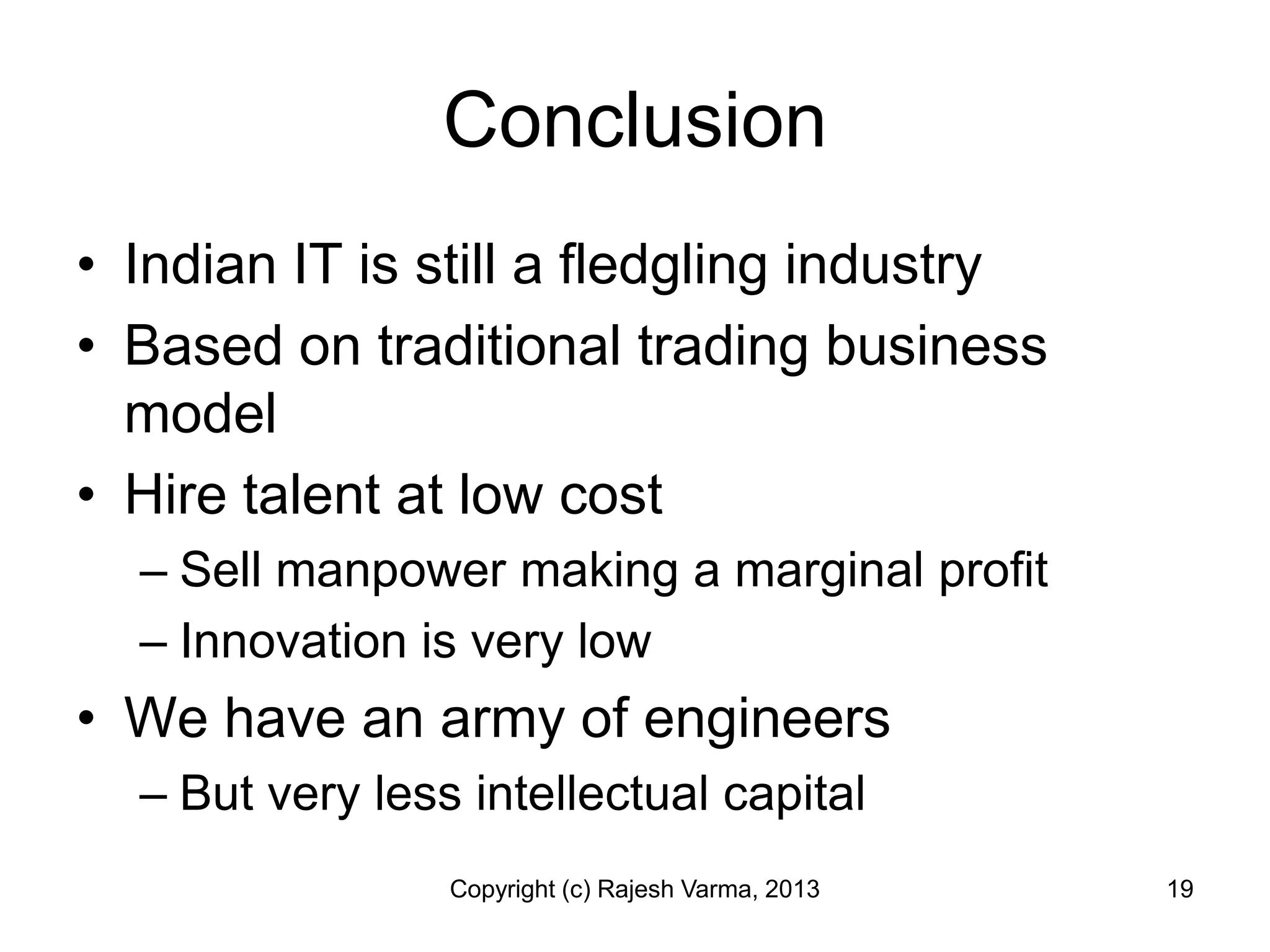

The document critiques the Indian IT industry, highlighting its reliance on low-cost manpower rather than innovation or substantial product development, resulting in only 2.35% of global IT spending. It discusses the industry's historical context, employment statistics, and the challenges of education and talent employability, leading to a conclusion that the industry is still underdeveloped. The author emphasizes the need for a shift towards innovation and improved intellectual property within the sector.

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)