Downloaded 41 times

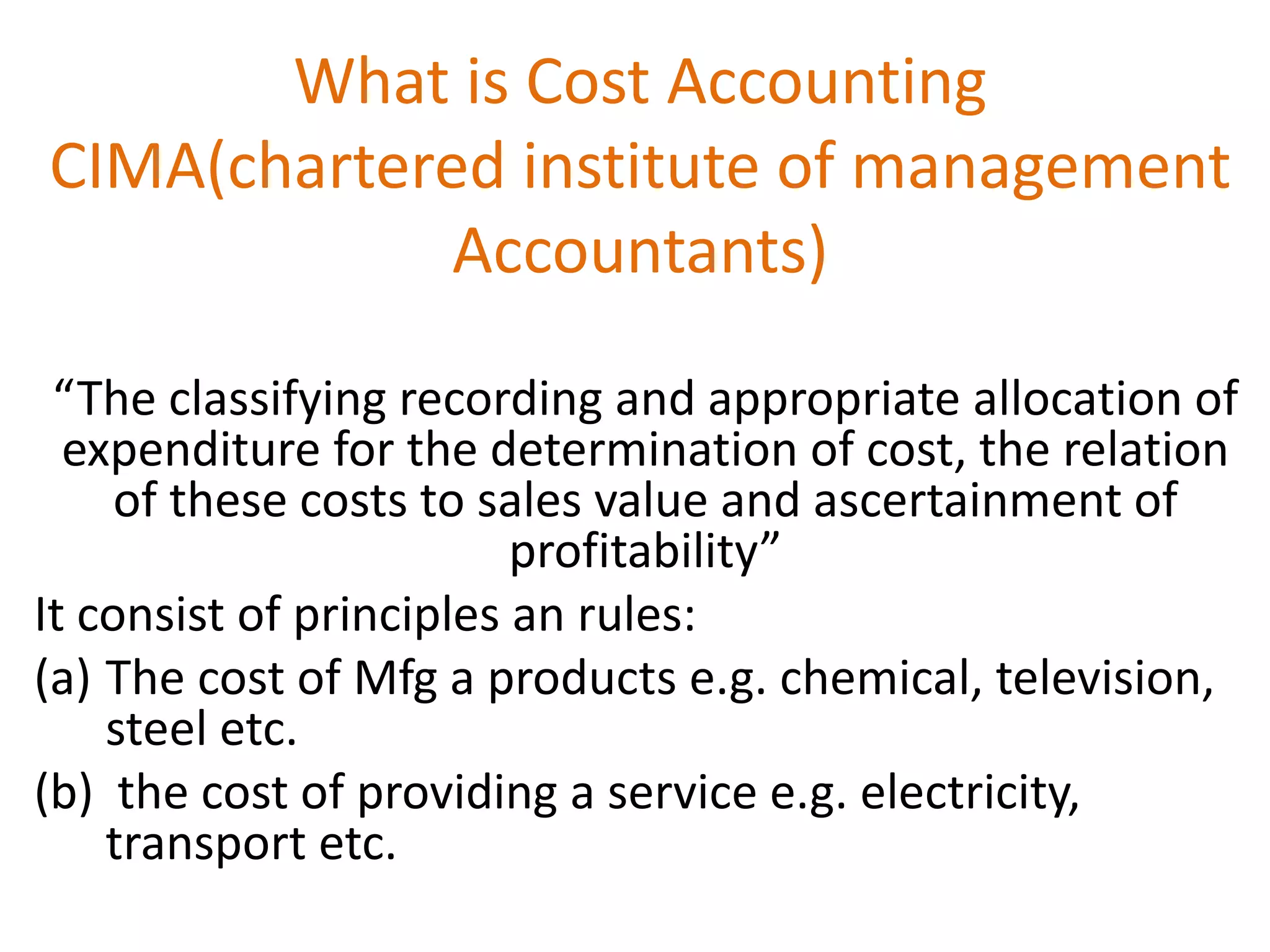

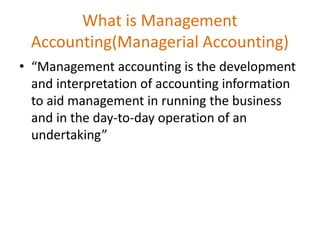

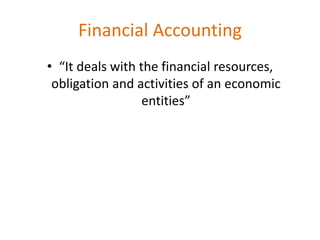

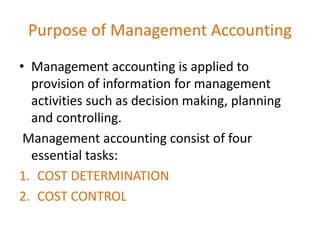

This document defines and compares cost accounting, management accounting, and financial accounting. It also discusses the objectives, nature, and scope of cost accounting and how cost accounting aids management. Cost accounting is defined as classifying, recording, and allocating costs to determine cost and profitability. Management accounting provides accounting information to aid management decision making. Financial accounting deals with financial resources and obligations to external parties. The document outlines key differences between cost accounting, management accounting, and financial accounting.