WFM - Initiating Coverage - Report

•

0 likes•188 views

- The document analyzes Whole Foods Market (WFM) and rates its stock as UNDERWEIGHT. While sales and EPS are forecasted to grow, concerns include WFM trading at a high P/E compared to its industry and risks to its growth strategy based on new store openings. - The intrinsic value of WFM according to the analysis is lower than its current stock price, and the stock is expected to fall to around $40 by the end of the fiscal year as its valuation realigns with industry levels.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to WFM - Initiating Coverage - Report

Similar to WFM - Initiating Coverage - Report (20)

More from Alessandro Masi

More from Alessandro Masi (16)

Recently uploaded

Recently uploaded (20)

WFM - Initiating Coverage - Report

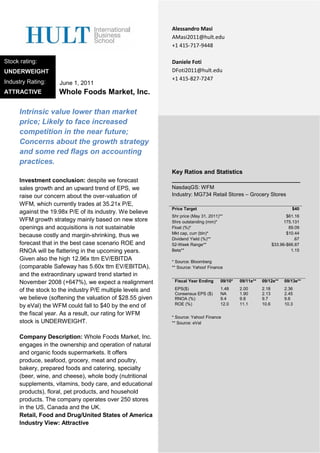

- 1. June 1, 2011 Whole Foods Market, Inc. Intrinsic value lower than market price; Likely to face increased competition in the near future; Concerns about the growth strategy and some red flags on accounting practices. Investment conclusion: despite we forecast sales growth and an upward trend of EPS, we raise our concern about the over-valuation of WFM, which currently trades at 35.21x P/E, against the 19.98x P/E of its industry. We believe WFM growth strategy mainly based on new store openings and acquisitions is not sustainable because costly and margin-shrinking, thus we forecast that in the best case scenario ROE and RNOA will be flattering in the upcoming years. Given also the high 12.96x ttm EV/EBITDA (comparable Safeway has 5.60x ttm EV/EBITDA), and the extraordinary upward trend started in November 2008 (+647%), we expect a realignment of the stock to the industry P/E multiple levels and we believe (softening the valuation of $28.55 given by eVal) the WFM could fall to $40 by the end of the fiscal year. As a result, our rating for WFM stock is UNDERWEIGHT. Company Description: Whole Foods Market, Inc. engages in the ownership and operation of natural and organic foods supermarkets. It offers produce, seafood, grocery, meat and poultry, bakery, prepared foods and catering, specialty (beer, wine, and cheese), whole body (nutritional supplements, vitamins, body care, and educational products), floral, pet products, and household products. The company operates over 250 stores in the US, Canada and the UK. Retail, Food and Drug/United States of America Industry View: Attractive Stock rating: UNDERWEIGHT Industry Rating: ATTRACTIVE Alessandro Masi AMasi2011@hult.edu +1 415-717-9448 Daniele Foti DFoti2011@hult.edu +1 415-827-7247 Key Ratios and Statistics _______________________________________ NasdaqGS: WFM Industry: MG734 Retail Stores – Grocery Stores Price Target $40 Shr price (May 31, 2011)** Shrs outstanding (mm)* Float (%)* $61.16 175.131 89.09 Mkt cap, curr (bln)* Dividend Yield (%)** $10.44 .67 52-Week Range** Beta** $33.96-$66.87 1.15 * Source: Bloomberg ** Source: Yahoo! Finance Fiscal Year Ending 09/10* 09/11e** 09/12e** 09/13e** EPS($) 1.48 2.00 2.18 2.36 Consensus EPS ($) NA 1.90 2.13 2.45 RNOA (%) 9.4 9.8 9.7 9.6 ROE (%) 12.0 11.1 10.6 10.3 * Source: Yahoo! Finance ** Source: eVal

- 2. 2 Industry analysis: overall, the industry follows an upward trend; therefore a general growth in sales can be forecasted for the Company in the next quarter, especially given the movement towards the specialty food sector, which grows faster than its comparables. Source: www.bea.gov Moreover, the trend followed by the personal consumption expenditures for food and beverages purchased for off-premises is increasing steadily since 2006 (despite the temporary bad performance in 2008) and is forecasted to keep growing. Source: www.bea.gov All in all, this makes the industry attractive, even though particularly sensible to disposable income and GDP fluctuations. Firm-specific analysis: among the various factors that can affect the profitability of the Company, we strongly believe that the following are going to determine Whole Foods’ future earnings: • the ability to open new stores, both in existing trade areas and in new areas, including international locations; • customer satisfaction and the creation of value for all its major stakeholders; • the ability to involve all employees and create a “Company-wide consciousness of shared fate by uniting the interests of team members as closely as possible with those of our shareholders”; • the capability to maintain profitable win-win business relations with its suppliers in order to keep the cost of the goods supplied low and to maximize the margin; • the global attitude towards organic and higher- quality products. Stores activities 2010 2009 2008 2007 2006 Stores at beginning of FY 284 275 276 186 175 Stores opened 16 15 20 21 13 Acquired stores 2 - - 109 1 Divested stores (2) - - (35) - Relocated stores - (5) (7) (5) (2) Closed Stores (1) (1) (14) - (1) Stores at end of fiscal year 299 284 275 276 186 Year-over-year growth 6% 7% 6% 46% 10% Sales identical stores 93.2% 91.4% 80.9% 88.8% 90.4% Sales new/relocated stores 6% 7.8% 9.9% 8.4% 8.8% Sales acquired stores 0.1% 0.0% 8.7% 1.3% 0.1% Other sales 0.7% 0.8% 0.5% 1.5% 0.7% Source: company filings Red flags on accounting practices: some concerns can be raised about high operating leases and relatively low capital leases, no impairment provided for goodwill in the Balance Sheet, and the expended employment stock options. Further, pre-opening expenses should be considered as a non-recurring item. Financial highlights: both ROE and RNOA are higher than 14% in 2006, then drop dramatically by, respectively, 7 and 5 points within 2 years, then recover steadily particularly from 2009 to 2010, reaching acceptable figures; the sales from the new stores are counterbalancing the decrease in sales of the existing ones principally given by the bad macroeconomic conditions. The total asset turnover shows a downward trend, therefore the business is moving from a cost leadership towards a product differentiation strategy. 2006 2007 2008 2009 2010 Net Profit Margin 3.60% 2.80% 1.40% 1.50% 2.70% x Total Asset Turnover 2.745 2.508 2.413 2.242 2.318 x Total Leverage 1.455 1.836 2.224 2.286 1.942 = ROE 14.38% 12.80% 7.70% 7.60% 12.00% n. of stores 186 276 275 284 299 ROE (per store) 0.077% 0.046% 0.028% 0.027% 0.040% Net Operating Margin 3.64% 2.81% 1.69% 2.10% 2.95% x Net Operating Asset Turnover 3.969 3.629 3.417 3.080 3.181 = RNOA 14.43% 10.20% 5.79% 6.46% 9.38% n. of stores 186 276 275 284 299 RNOA (per store) 0.08% 0.04% 0.02% 0.02% 0.03% Net Borrowing Cost (NBC) 0.22% 0.66% 2.39% 4.77% 3.04% Spread (RNOA - NBC) 14.21% 9.54% 3.40% 1.69% 6.35% Financial Leverage (LEV) 0.62% 26.88% 57.00% 66.42% 41.51% ROE = RNOA + LEV*Spread 14.52% 12.77% 7.73% 7.58% 12.01% Source: company filings and calculations The net borrowing cost is increasing within the 5 years period and so is the financial leverage, thus the risk of the returns to equity holders is increasing; the spread between RNOA and NBC is

- 3. 3 decreasing towards 2009 but recovers in 2010, thus the ROE exceeds the RNOA in each of the years to a larger extent since also the leverage is increasing. Source: company filings and calculations Whole Foods needs to push its operating margin up (therefore move towards product differentiation and quality) in order to obtain a high RNOA and generate value for its shareholders without exposing the business to risk from high leverage. Sales and PP&E forecasting: we believe a 5 year time horizon is appropriate, given the characteristics of the retail industry, where firms are not involved in any long R&D process. On top of the planned growth policy, we assume: • 3 stores openings per year starting from 2015; • 1% weighted average square footage growth rate 1% starting from 2015; • sales growth driven by footage expansion (with a 50% estimated expansion productivity adjustment) and comparable-store sales growth, whose sum gives back the total growth rate. We believe a good estimate of the gross PP&E to sales ratio for 2011 is the average of the ratios for the previous three years. For the subsequent years we estimated it as the moving average of the three previous years. With the same process we estimated the depreciation to PP&E ratio. Finally, we also assumed that, given the forecasted growth and the availability of earnings, the Company may bring the dividend payout ratio up by 0.5% yearly to 4% in 2016. Source: eVal The ratio analysis for the forecasted period shows that both ROE and RONA are acceptable, being close to 10%, the Profit Margin should be improved, while the business should strategically move from relying on assets towards product differentiation. The advanced DuPont model reveals the necessity to increase RNOA through improving margins: leverage has been decreased in the forecasted period, and this makes the business less risky and hence more attractive for investors. Margins have to be improved through a more careful cost policy: however, we assumed that due to the change of strategy, it would not

- 4. 4 have been possible for the Company to cut costs in the 5-year period. The turnover ratios look good, even though the net working capital turnover is decreasing, but this is due to the change of strategy. The firm is decreasing its leverage, hence lowering its debt to equity ratio. Interest coverage is improving steadily, and this makes the Company more attractive for investors. The credit risk is lowering. Valuation parameters: we estimated a required rate of return on equity of 8.92% calculated with the CAPM, given a risk-free rate of return of 3.17%, a beta of 1.15, and a market risk premium of 5%. Given the market capitalization, we did not apply any size premium to the CAPM. Given the market value of equity and debt, the Company has the following capital structure: (millions of $) Equity 11,052.35 98.15% Long-term debt 207.74 1.84% Short-term debt 0.44 0.01% Pref. equity 0.00 0.00% Total 11,260.52 100% Source: Bloomberg Looking at the Company bonds, we estimated a cost of debt of 3.36%. Equity Debt Weight 98.15% 1.84% Cost 8.92% 4.36%* W x C 8.75% 0.08% *Source: we increased the actual cost of debt given by Bloomberg by 1% since eVal estimated it as internally-inconsistent. Therefore, WFM has a 8.83% WACC. Differently, eVal considers the firm’s common equity, debt and preferred stock and then searches the WACC that discounts the forecasted future free cash flows to all investors back to this predetermined amount: both approaches are valid and particularly in this case since the WACC is very close to the cost of equity, given the capital structure of the Company. The cost of preferred stock is 6.85%, estimated from the dividend paid in 2009 and 2010 for the 425,000 outstanding shares of the Series A Preferred Stock (approximate value $413.1 million). There is no dilution factor for splits or stock dividends, but an adjustment is needed for 18,946 options outstanding as of 2010 exercisable at a weighted average price of $46.00, with weighted average remaining contractual life of 2.99 years, for a value of contingent claim per share of $25.53, resulting in $483.70 million total value of contingent claim. Absolute valuation: the DCF valuation model gives negative FCFE and FCFF for the first three and two forecasted periods respectively because of CapEx expenditures and the Wild Oats acquisition in 2008 that penalize the valuation of the firm. This pitfall is avoided by the Residual Income model, where the value is recognized earlier. The two valuation models suggest that the intrinsic value of the firm ($28.55/share) is lower than the current market price ($61.16/share). Therefore, we believe the stock is over-priced, even though the market probably absorbs such premium given the growth potential of the Company and the attractiveness of the industry, and seen the extraordinary continuous upward trend started in November 2008 (+647%). We agree that the Company is shareholders value and generating abnormal returns, but not to the extent recognized by the market. Overall, our recommendation is to sell the stock, since the income generated might be due mainly by accruals. We recognize cyclicality in the path followed by the stock price that will bring it down soon, and we also raise concerns about the growth strategy and the risks of the business. Sensitivity Analysis: given the price determined by eVal, which uses a linear smoothing algorithm, we consider $33.80 as the Base Case. Bull Case: with an increase in sales growth up to 11%, an increase in terminal year’s sales growth up to 5% and an increase of terminal year’s ROE by 1%. Under these assumptions, we obtain a stock price of $43.42. Bear Case: with a decrease in sales growth down to 7%, a decrease in terminal year’s sales growth down to 3% and a decrease of terminal year’s ROE by 1%. Under these assumptions, we obtain a stock price of $27.86. Such values say that the stock is particularly sensible to slight increase/decrease of sales and profitability. Forecasting EPS: forecast EPS and consensus analyst forecast of EPS both show an upward trend and do not show significant differences, even

- 5. 5 though the latter has a wider range of variation than the former within the period 2011-2013. 2011e 2012e 2013e Forecast EPS $2.00 $2.18 $2.36 Consensus Analyst Forecast of EPS* $1.90 $2.13 $2.45 *Source: MSN Money Market-based valuation: we believe that Safeway, Inc. (NYSE: SWY) represents an appropriate comparable for Whole Foods Market, Inc. The two companies have comparable risks and growth models. These characteristics make the use of the P/E Multiple method acceptable. Nevertheless, the capital structure and the way the two companies depreciate their fixed assets are different and have to be taken into consideration. WFM vs. SWY Item WFM SWY Interest rate Swaps Swaps Foreign Currencies Adjustments Adjustments Commodity Prices Price contracts Price contracts Current Economic Condition Sensitive Sensitive Total Debt/Equity (mrq) Most Equity Most Debt Merchandise Inventories Valued LIFO, remaining FIFO Valued LIFO, remaining FIFO Property and Depreciation At cost, building 20-30 years, equipment 3- 15 years At cost, building 7-40 years, equipment 3- 15 years Growth Model New stores New stores, CAPEX Source: company filings The following table represents Whole Foods’ stock value calculated as a multiple of Safeway’s P/E, currently trading at a discount to the market. The figure shows that even with this method the intrinsic value of the stock is by far lower than its current price. To be noticed that this valuation would be even more evident choosing other comparables, such as Kroger (NYSE: KR) or even Wal-Mart (NYSE: WMT), whose P/E ratios are, respectively, 14.26x and 12.06x. WFM Market-based Valuation (SWY) Year P/E SWY 2010 EPS WFM 2011e Price WFM 2011e 17.87 2.00 35.74 Source: Yahoo! Finance The calculation of Whole Foods’ relative P/E ratio, compared with S&P500 P/E reveals that in 2010 the stock was still trading at a premium, but was converging to the market in 2010. Looking at consensus EPS forecasts, relative P/E is expected to rise again, confirming that the stock is still trading at a premium to the market. Nevertheless, we believe that this premium will shrink soon. WFM Relative P/E Ratio Year P/E (ttm) WFM P/E (ttm) S&P 500 Relative P/E 2006 42.15 27.20 1.55 2007 37.95 24.01 1.58 2008 24.42 15.17 1.61 2009 35.87 20.52 1.75 2010 2011e 25.95 35.21 22.97 23.66 1.13 1.49 Source: Yahoo! Finance

- 6. 6 Appendix: Whole Foods Market, Inc. financial statements from the 10-k 2010

- 7. 7

- 8. 8

- 9. 9