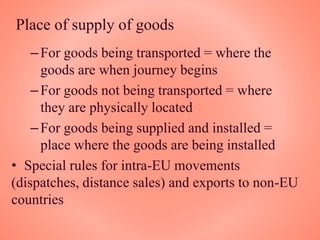

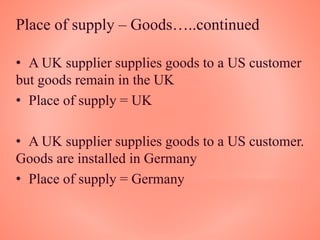

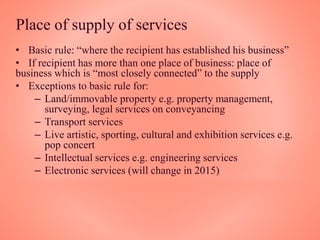

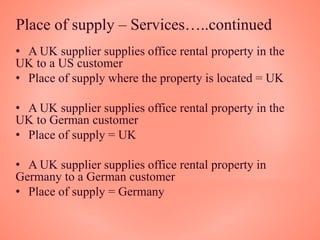

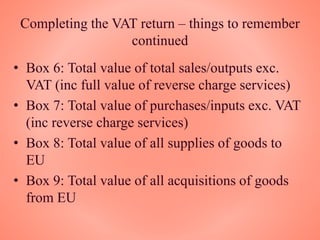

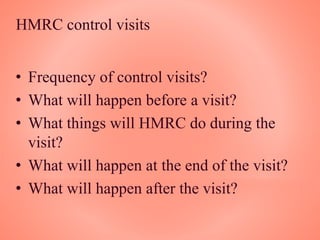

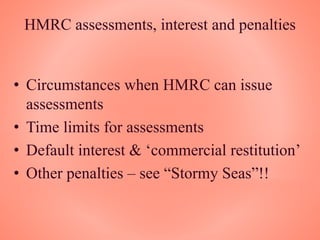

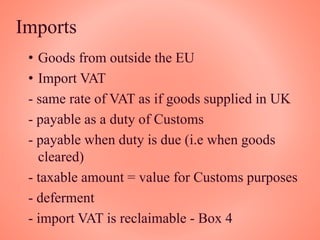

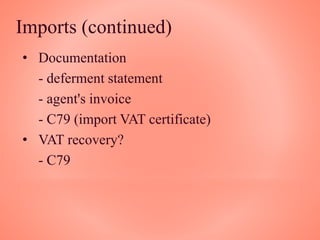

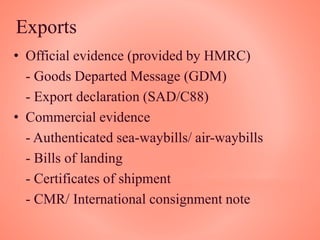

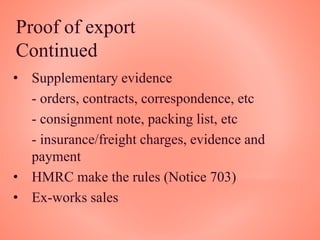

This document provides an overview of VAT (Value Added Tax) in the UK. It begins with basic principles, including that VAT is charged on business transactions and collected throughout the supply chain. It then covers various aspects of VAT law and how VAT works using an example. Key topics discussed in more detail include input tax, output tax, time and place of supply rules, international VAT issues, and VAT compliance obligations. Risk areas like penalties, disputes, and common pitfalls are also addressed. Throughout, the document aims to explain complex VAT concepts and highlight important considerations for businesses.