This document summarizes changes to EU VAT rules taking effect in 2021, including:

- Abolishing the VAT exemption for goods under €22, with VAT now due on the first €0.01 of value.

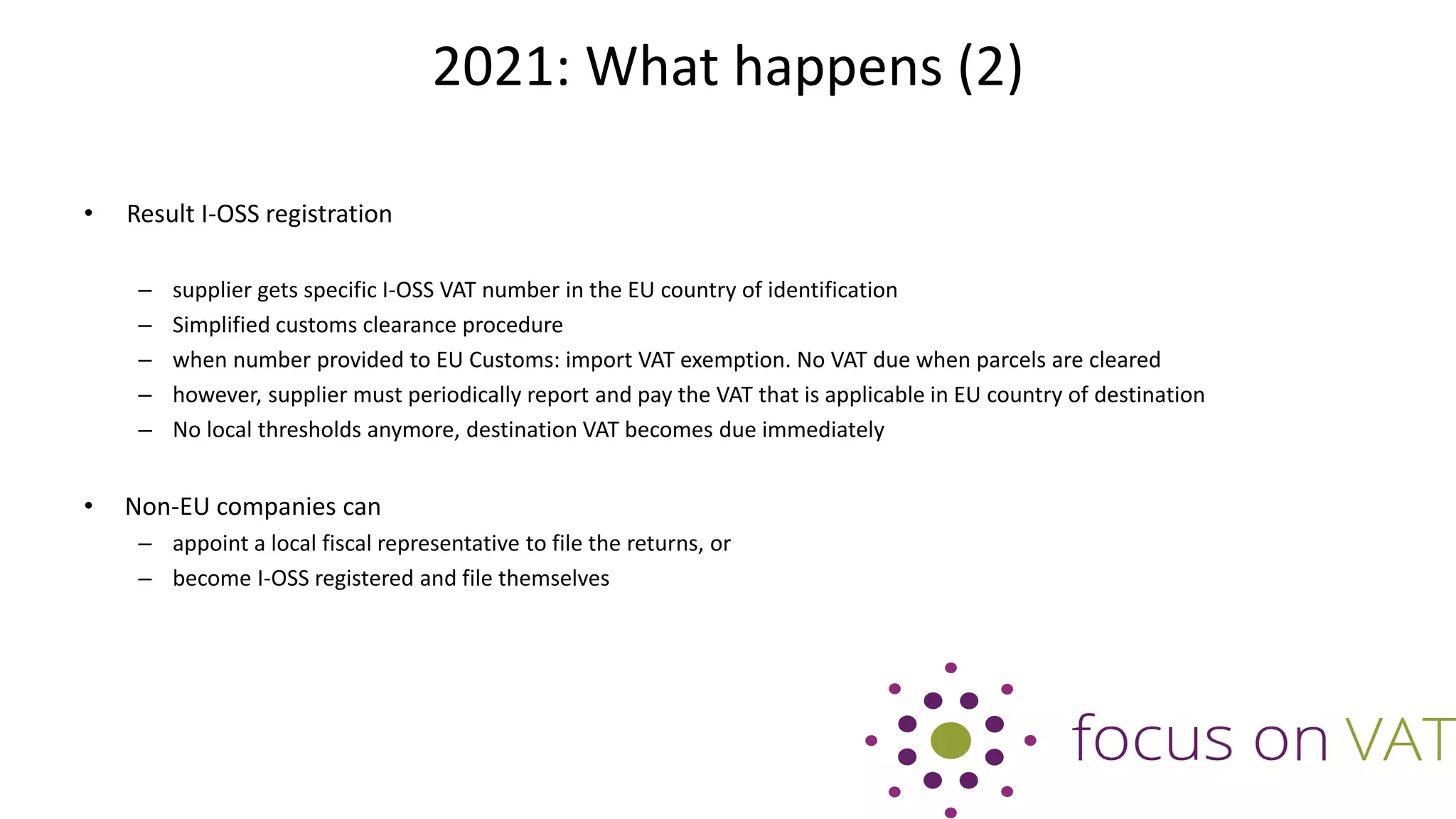

- Introducing the Import One Stop Shop (I-OSS) for goods valued up to €150, allowing simplified customs and VAT payment in the country of registration.

- If I-OSS is not used, transport companies must report imports and pay VAT under the "Fall Back" method, applying the standard VAT rate even if a reduced rate normally applies.

- Non-EU suppliers will face destination VAT on all imports as of €0.01, while EU suppliers can charge