Downloaded 181 times

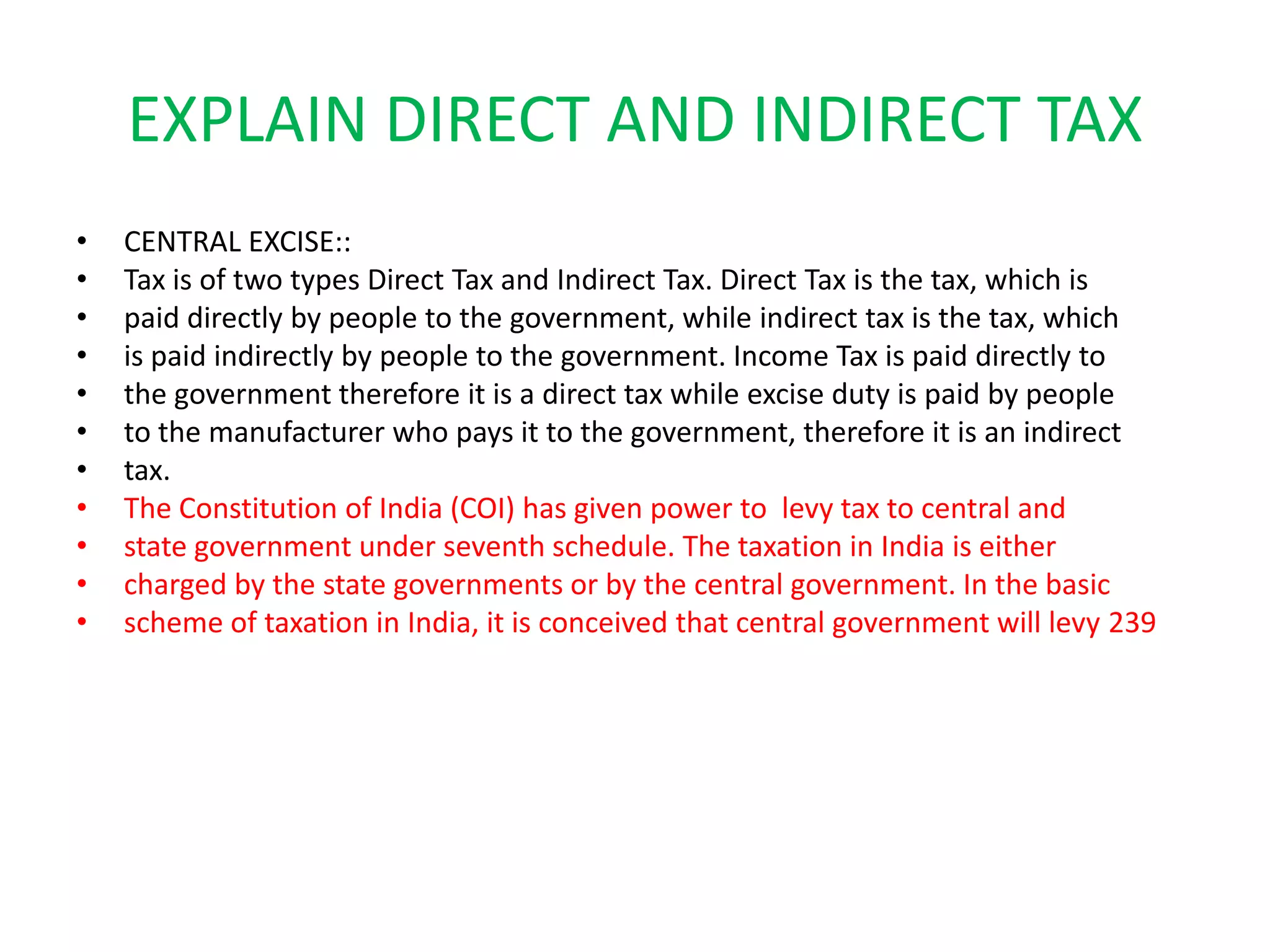

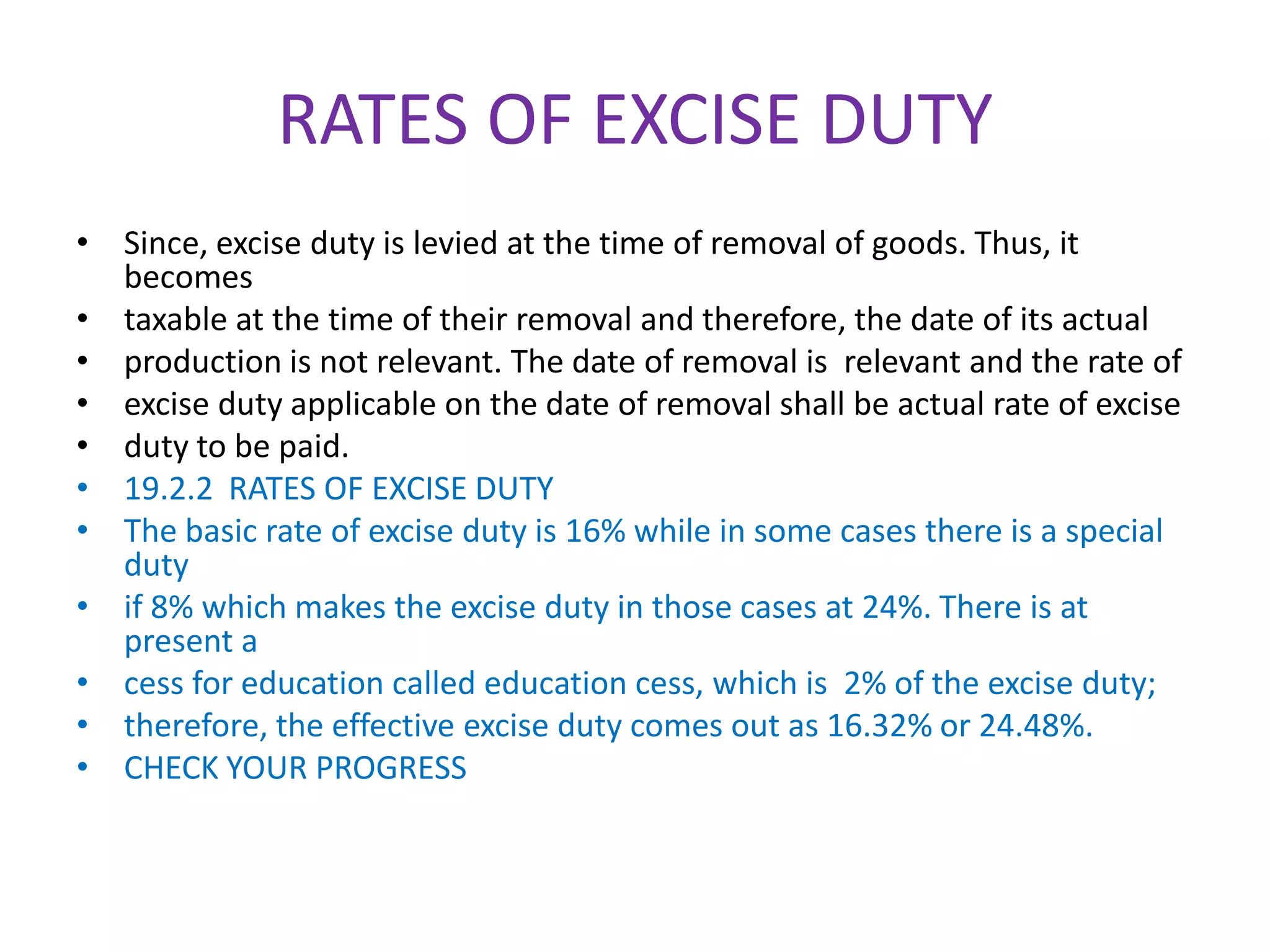

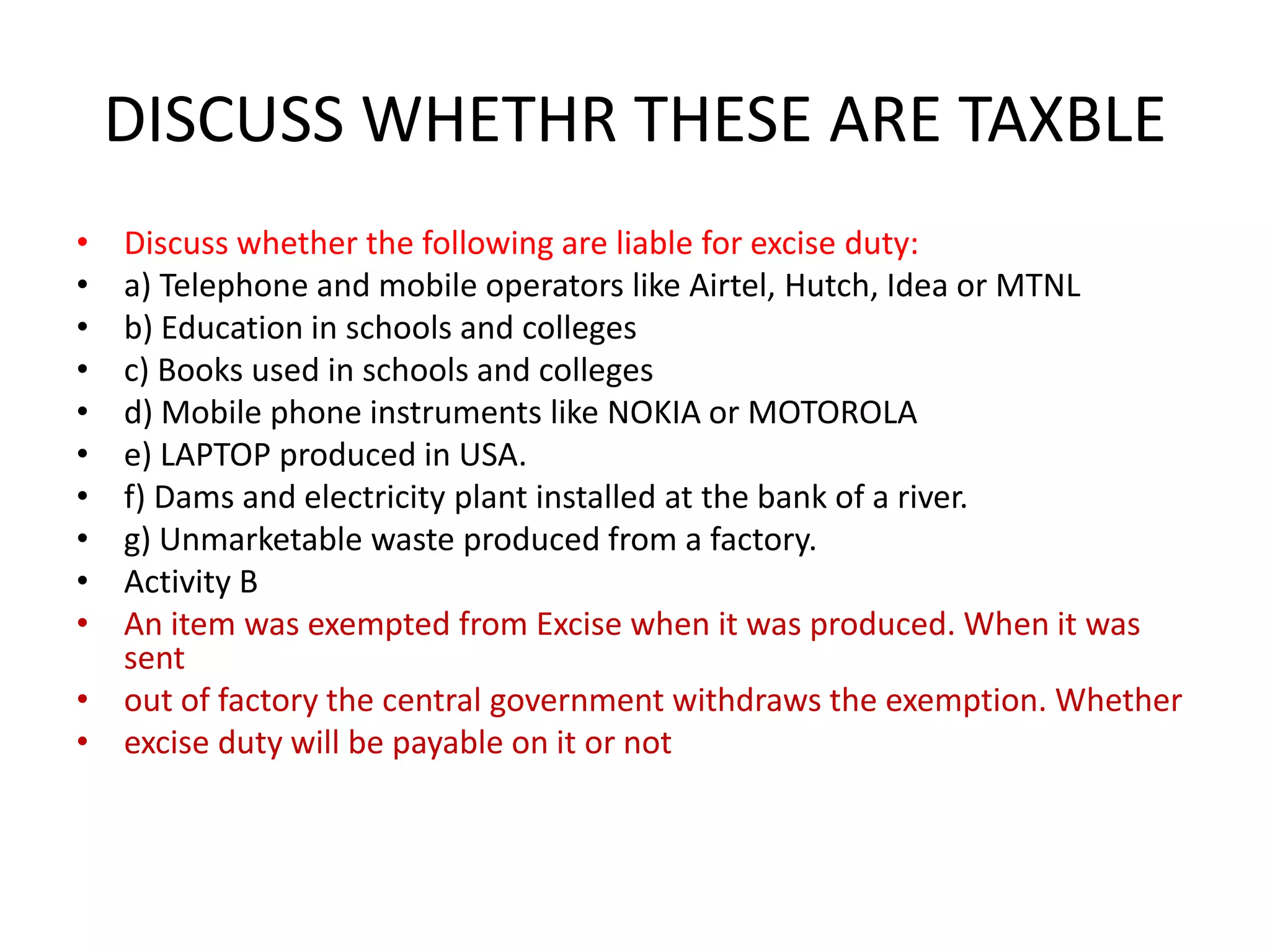

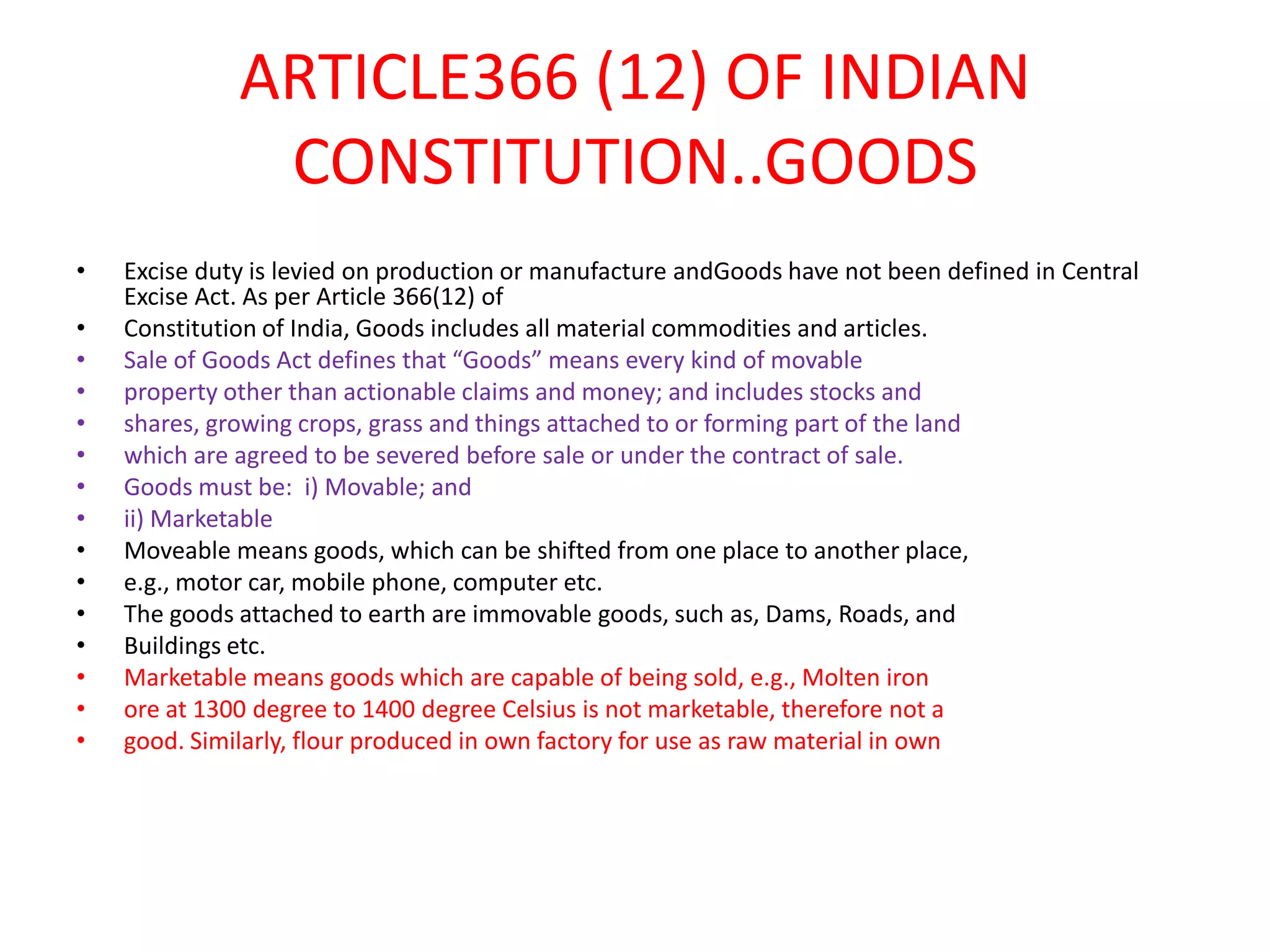

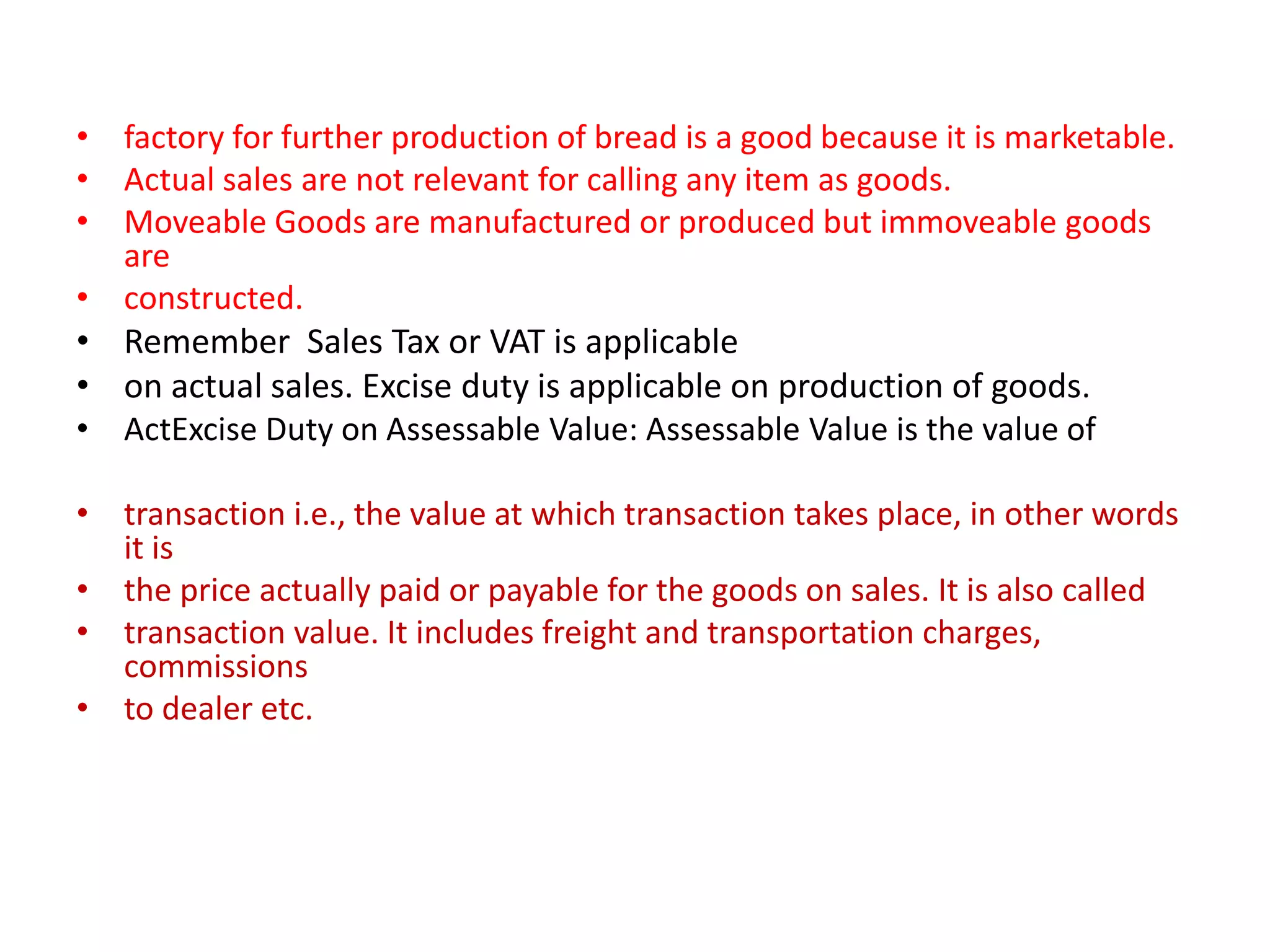

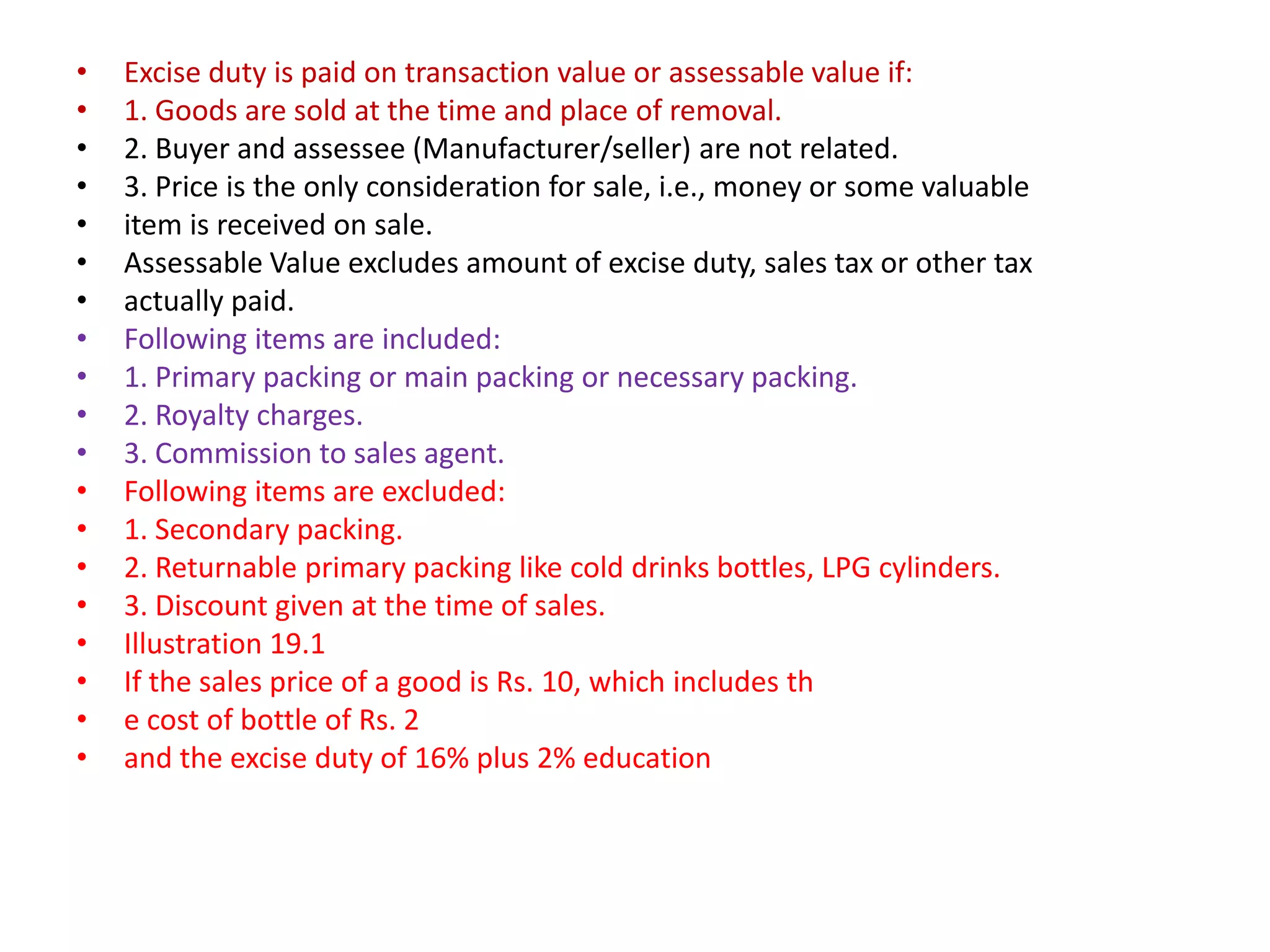

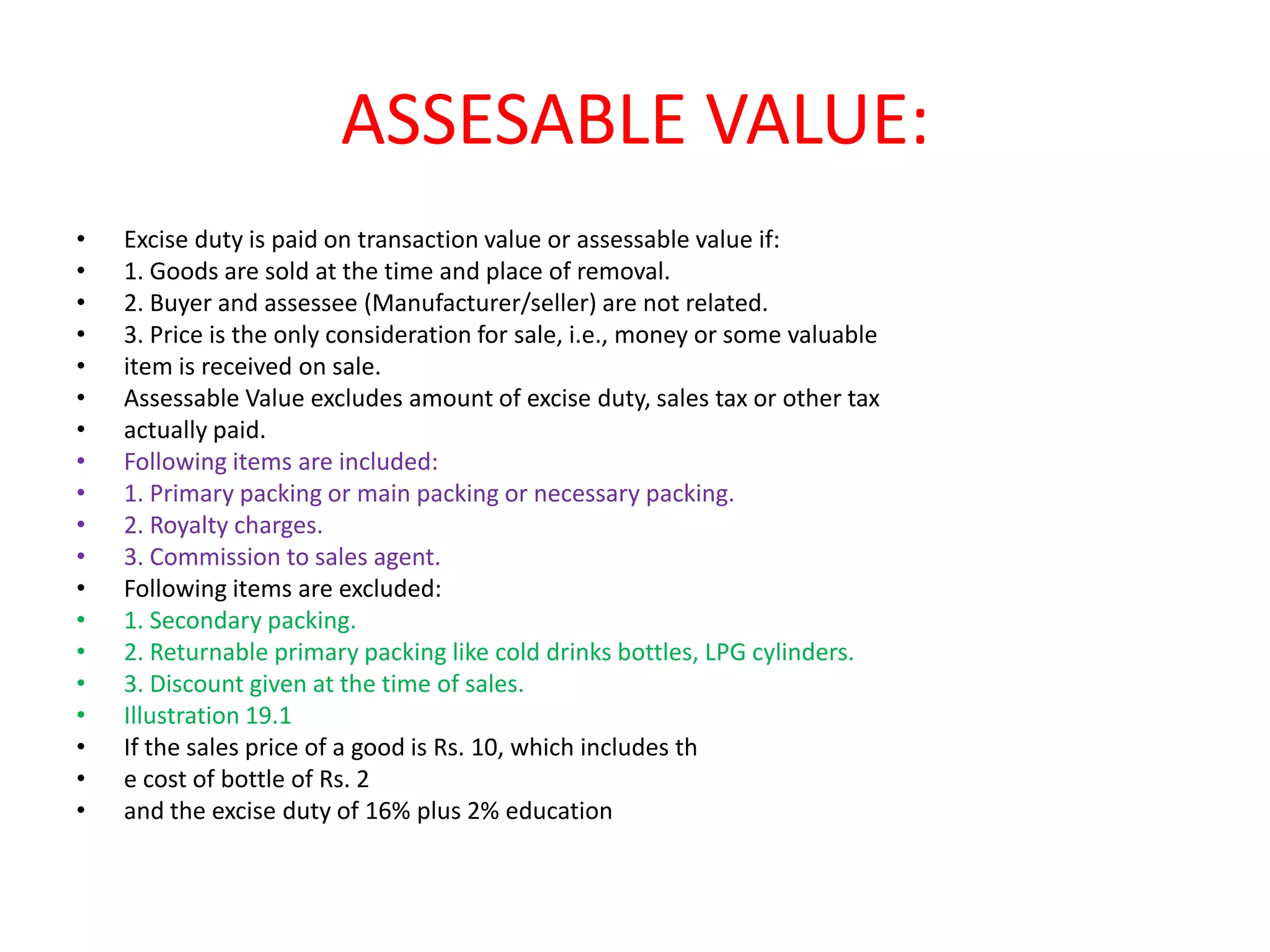

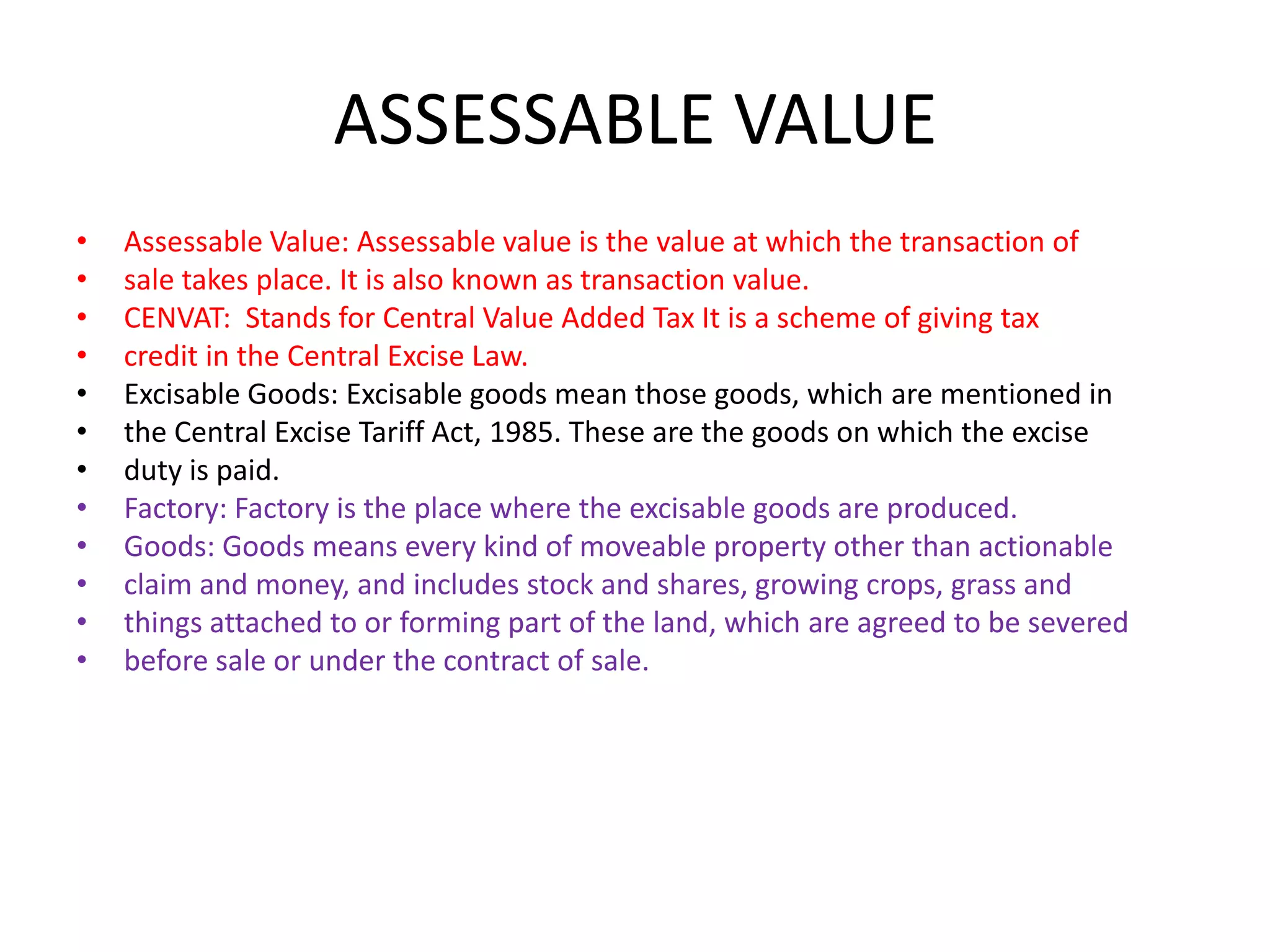

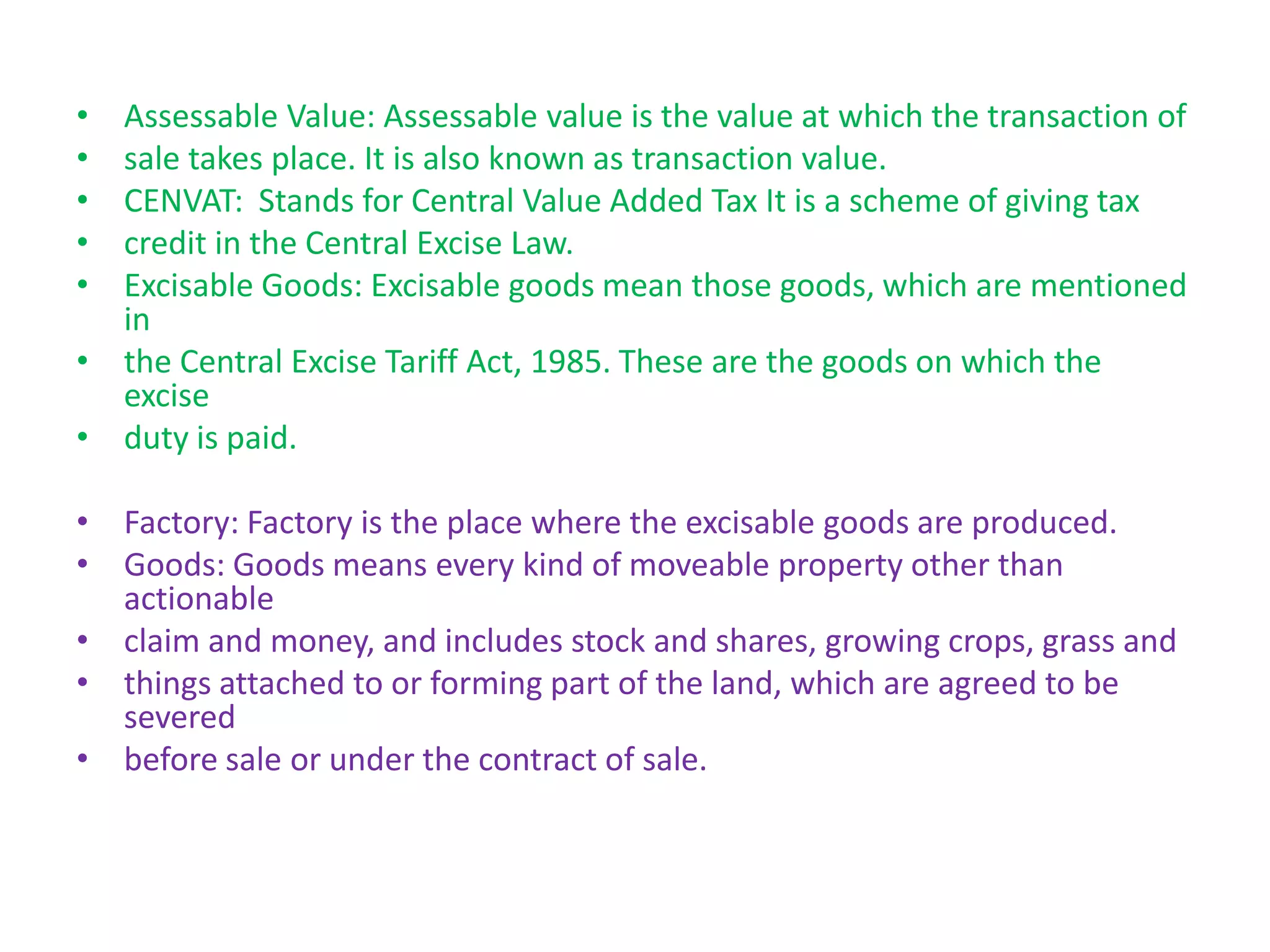

Direct and indirect taxes are discussed. Direct tax is paid directly to the government, like income tax, while indirect tax is paid indirectly, like excise duty which manufacturers pay to the government. Central excise duty is levied under the Central Excise Act on goods that are movable, marketable, and included in the tariff list if manufactured in India. The document outlines what is included in excise acts, the taxable event of manufacture, applicable rates, and assessable value which is the transaction value on which duty is paid. Key terms like CENVAT credit and excisable goods are also defined.