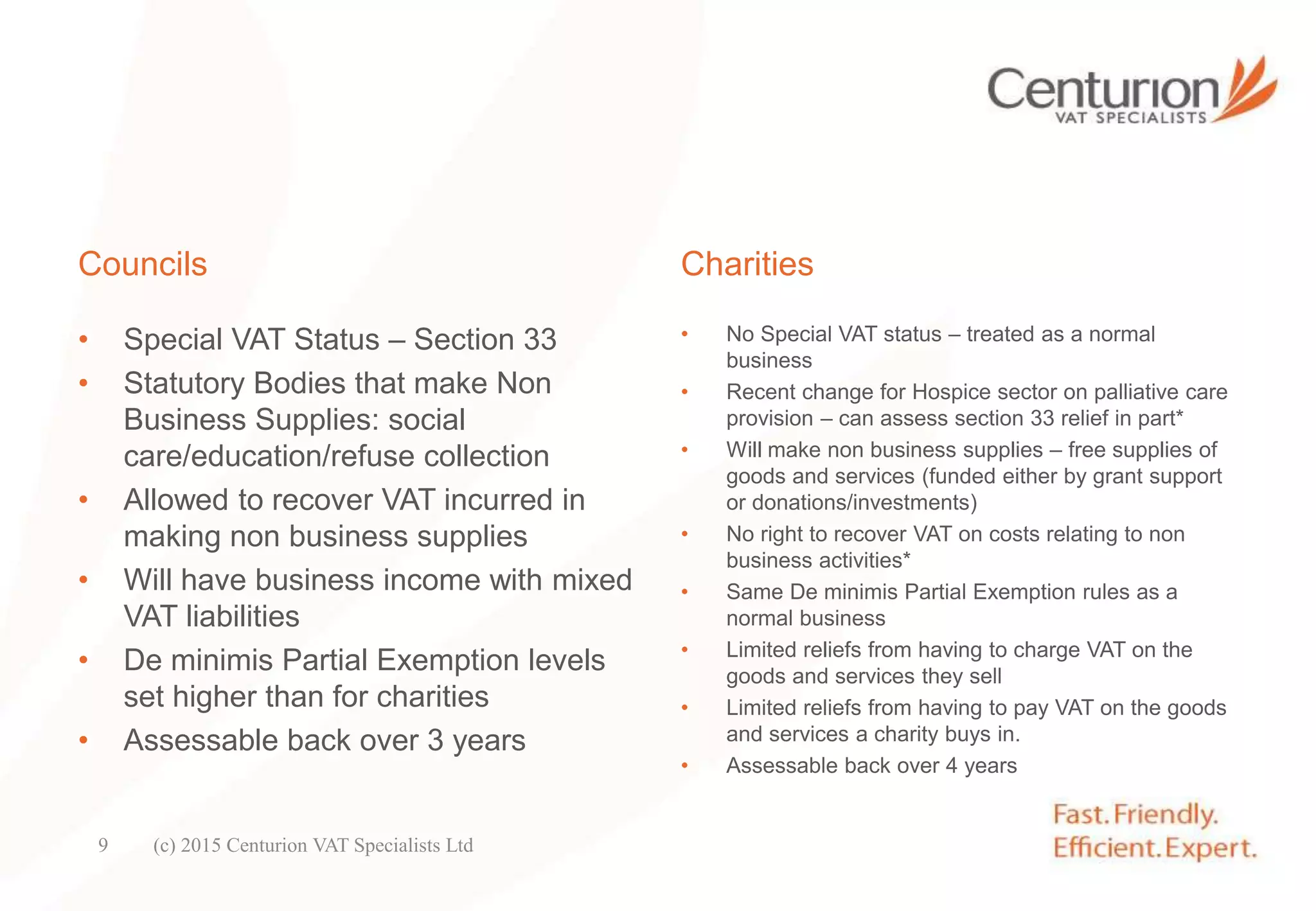

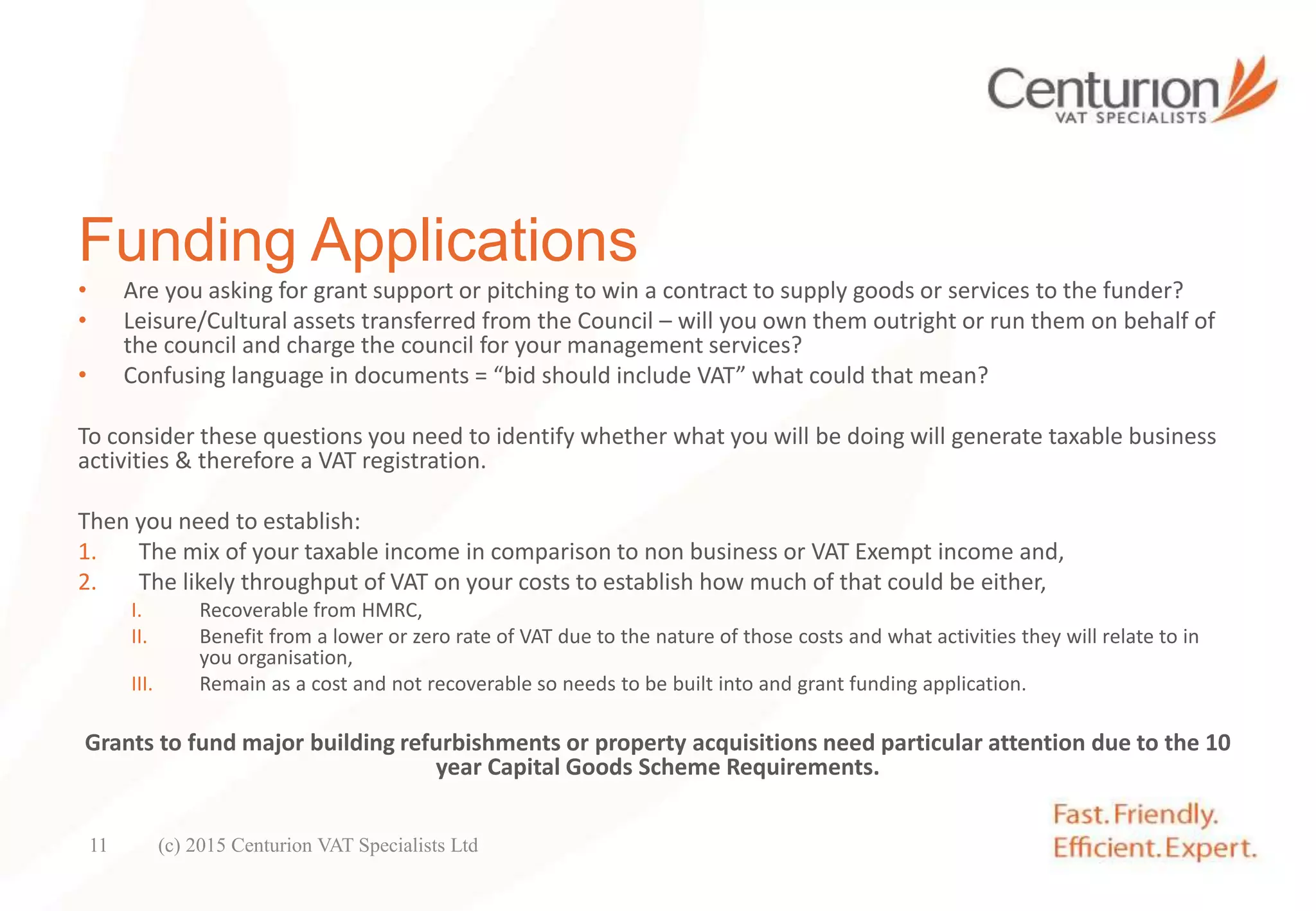

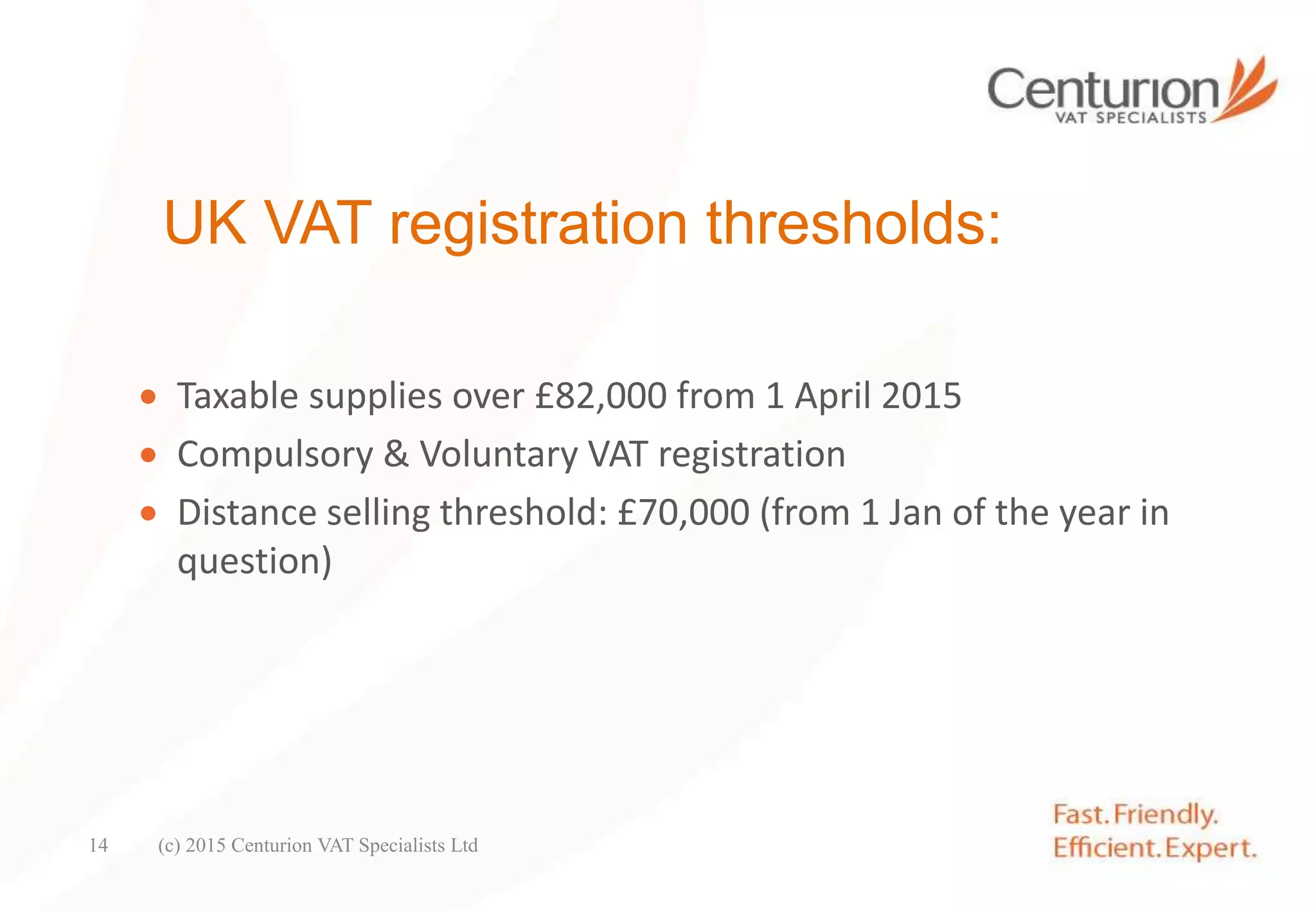

The document provides an overview of UK VAT rules as they relate to community asset transfers from councils to charities. It discusses the different VAT treatment of councils and charities, how VAT applies to funding applications, VAT registration requirements, and managing property assets and the associated VAT implications. Key points include the special VAT status councils have allowing recovery of VAT on non-business supplies, compared to charities which have no such relief; factors to consider regarding VAT implications when applying for grants or contracts; and triggers for VAT registration like surpassing turnover thresholds.