This document discusses VAT principles related to exports. Some key points:

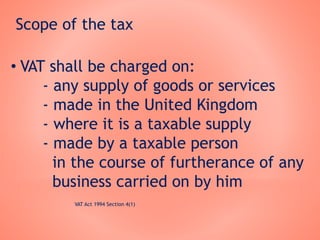

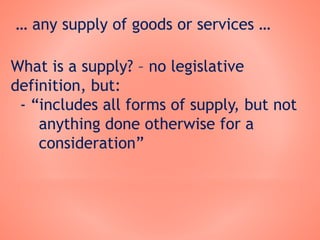

- VAT is charged on the supply of goods and services in the UK, with exceptions for exports.

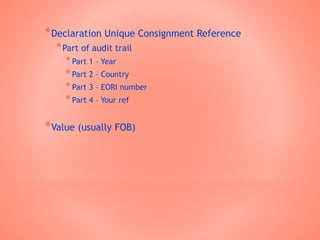

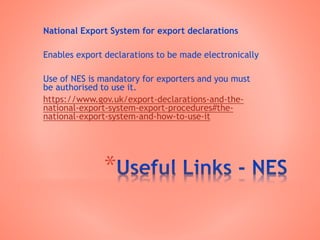

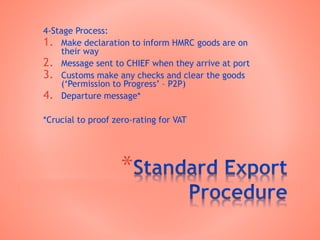

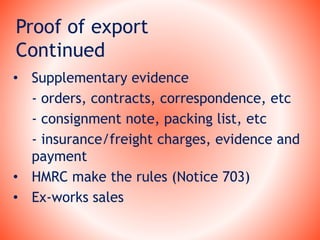

- For exports of goods to be zero-rated, the exporter must obtain proof of export within 3 months such as commercial documents or an official Goods Departed Message.

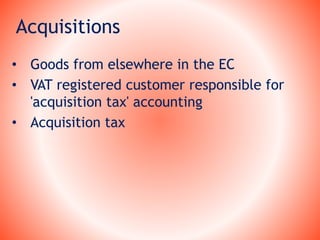

- Intra-EU trade is zero-rated for the supplier but the customer accounts for an acquisition tax in their domestic VAT return.

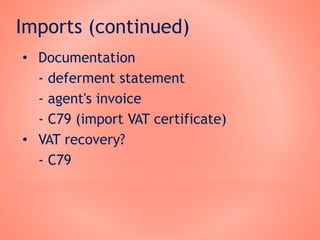

- Imports into the UK from outside the EU incur import VAT, while imports from within the EU are acquisitions subject to domestic VAT by the customer. Proper documentation is needed for imports and exports.