Download to read offline

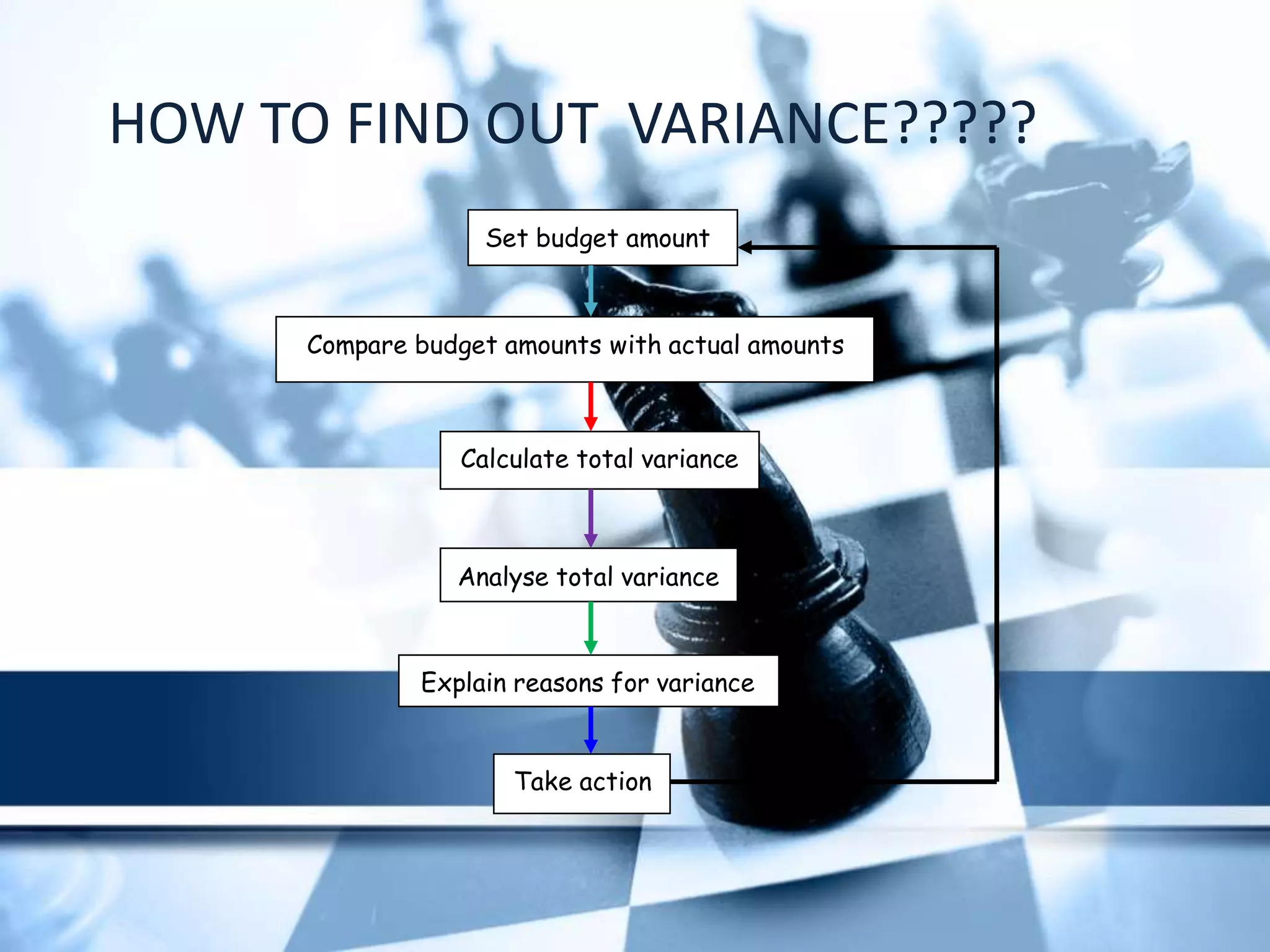

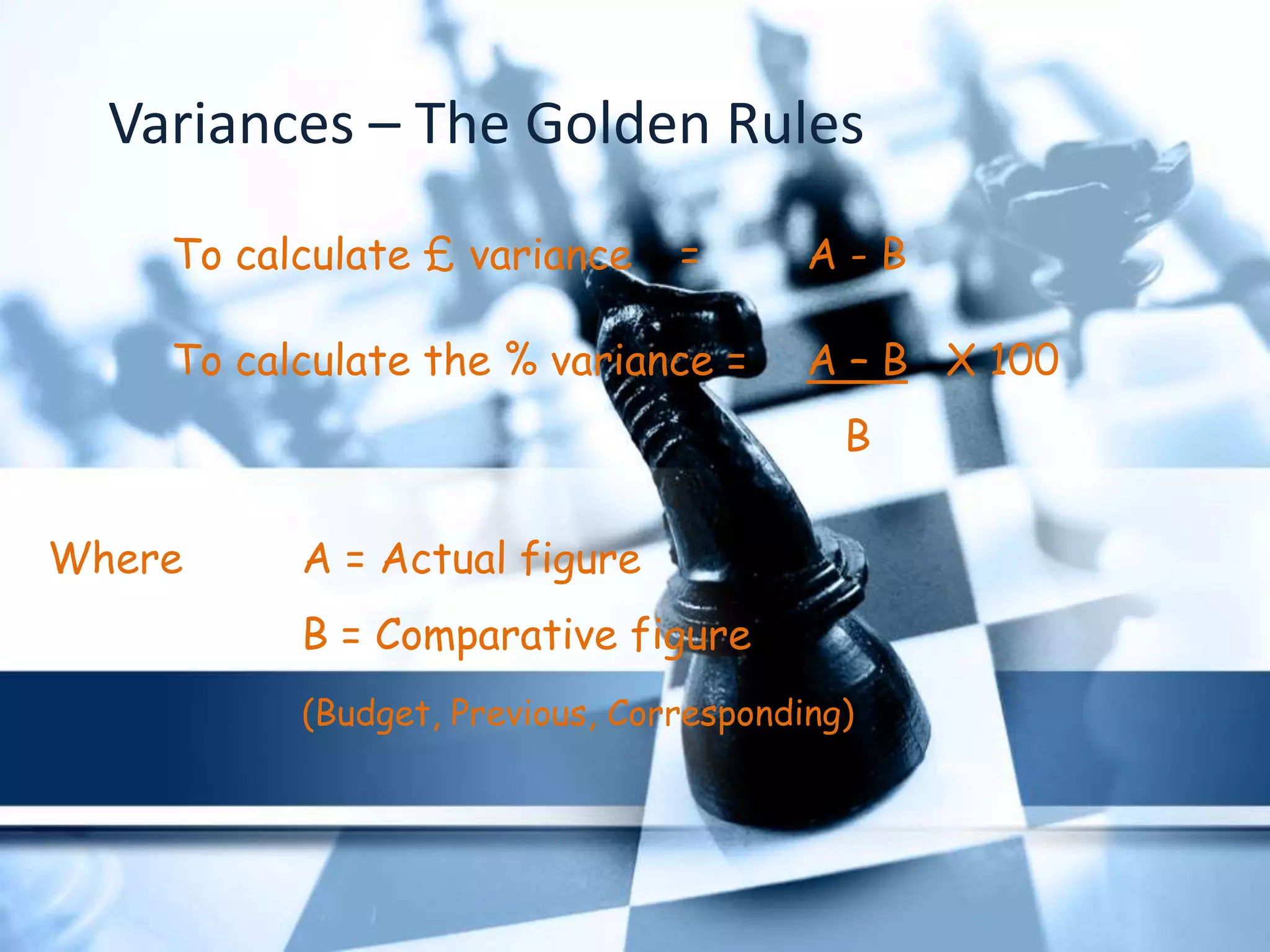

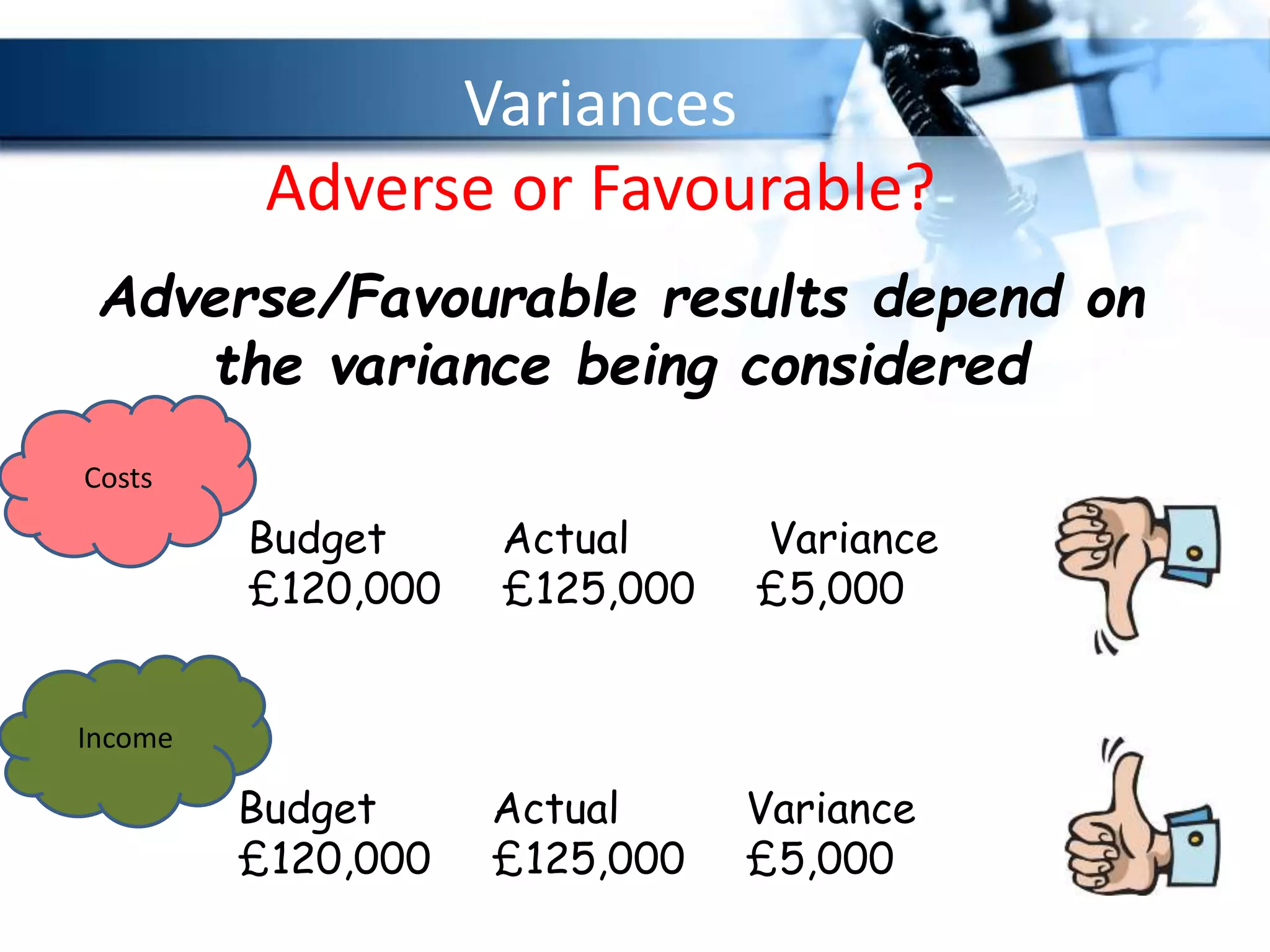

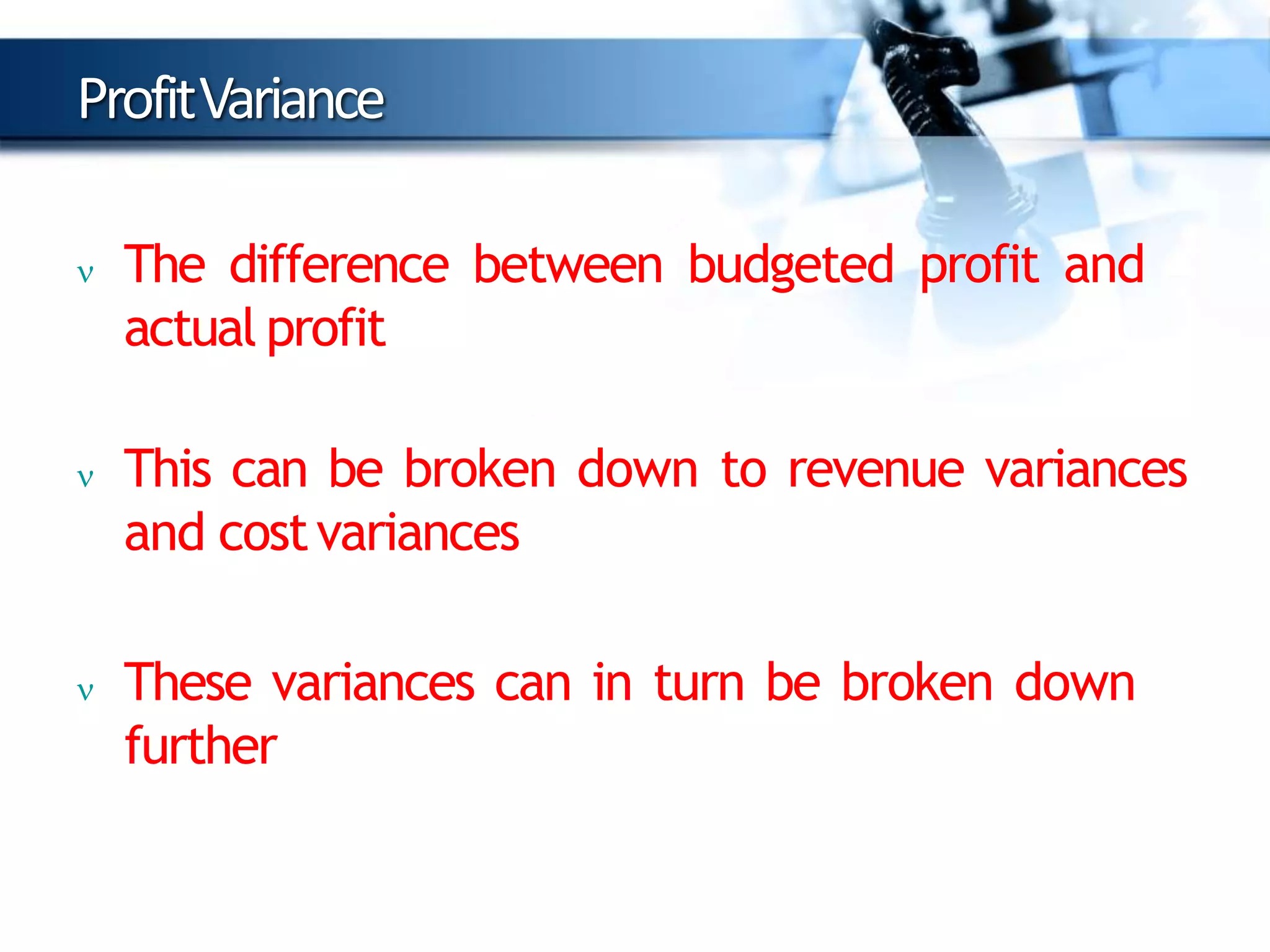

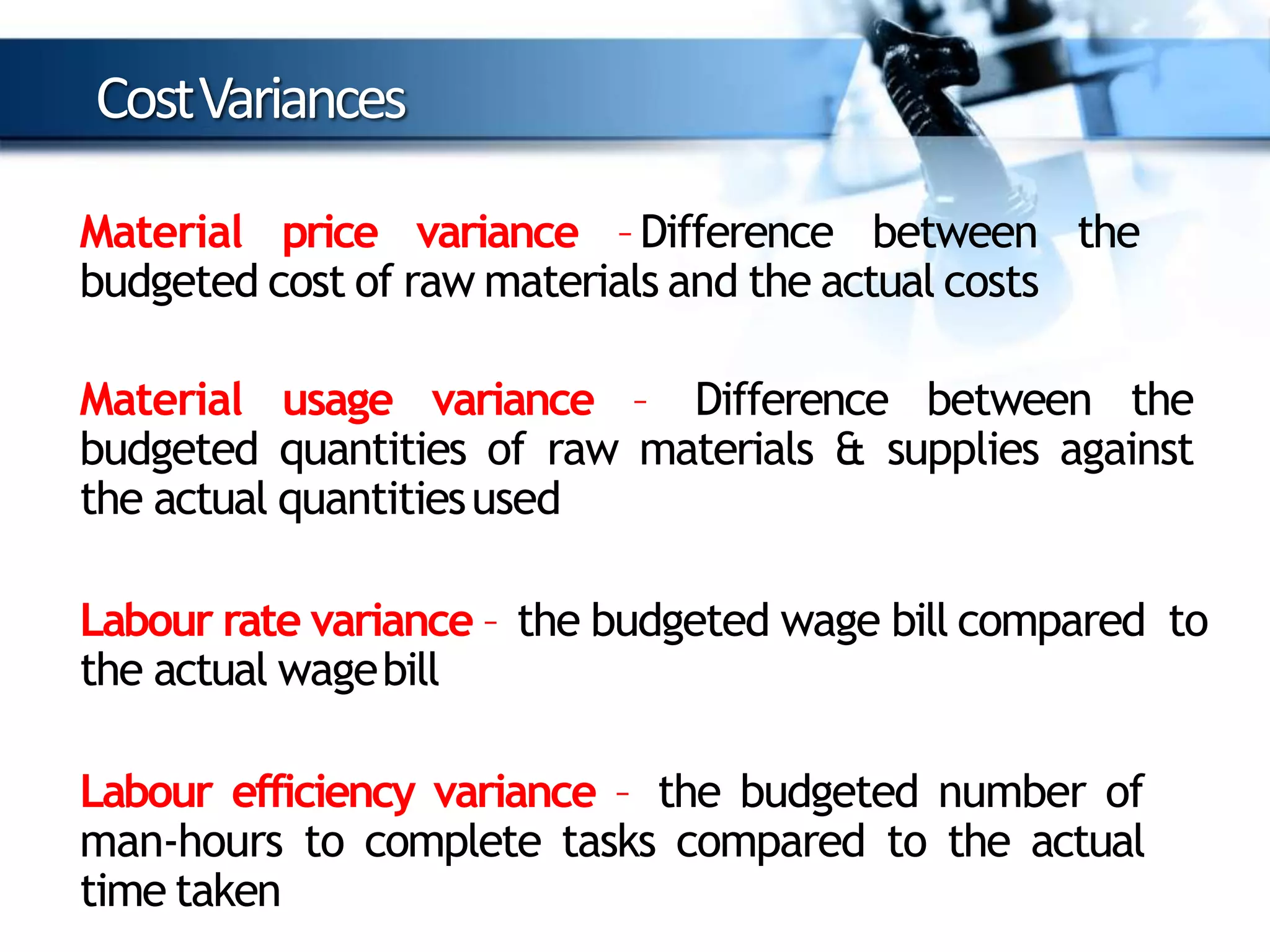

Variance refers to the difference between expected results, like a budget, and actual outcomes, such as expenditures. Variance analysis is a budgeting tool that evaluates performance by comparing budgeted and actual figures, identifying favorable or adverse variances that impact profits. It breaks down variances into categories like profit, sales, and cost variances, helping businesses make informed decisions and forecast future performance.