Downloaded 75 times

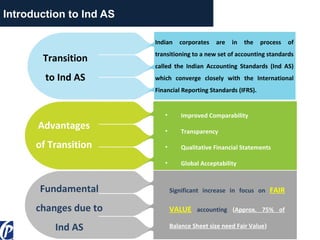

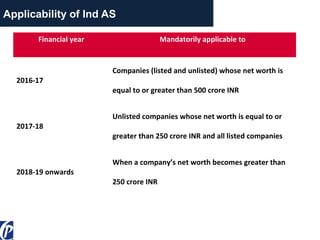

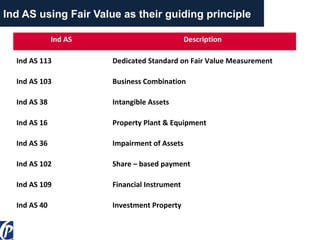

The document provides an overview of the Indian Accounting Standards (Ind AS) focusing on valuation principles and techniques, particularly related to fair value measurement. It discusses the transition to Ind AS, applications under various standards, and details methods such as the relative valuation method and discounted cash flow method. The document outlines the principles of assessing fair value including factors affecting measurements, valuation techniques, and the fair value hierarchy.