Download as PDF, PPTX

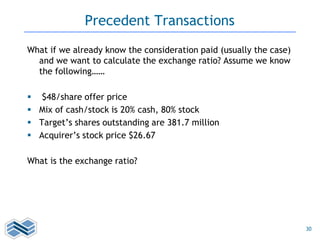

Okay, let's break this down step-by-step: * Offer price per share is $48 * Mix is 20% cash, 80% stock * To calculate the exchange ratio, we take the stock portion as a percentage of the total consideration * Stock portion is 80% of $48, which is 0.8 * $48 = $38.40 * Cash portion is 20% of $48, which is 0.2 * $48 = $9.60 * Total consideration is $38.40 stock + $9.60 cash = $48 * To get the exchange ratio, we take the stock portion ($38.40) and divide it by the acquirer's stock price.