Download to read offline

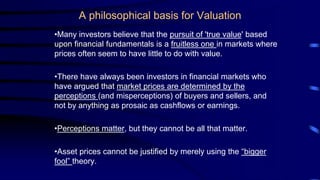

![The Building Blocks of Valuation

Choose a

Cash Flow Dividends

Expected Dividends to

Stockholders

Cashflows to Equity

Net Income

- (1- d) (Capital Exp. - Deprec’n)

- (1- d) Changein Work. Capital

= FreeCash flowto Equity (FCFE)

[d = Debt Ratio]

Cashflows to Firm

EBIT(1- tax rate)

- (Capital Exp. - Deprec’n)

- Changein Work. Capital

= FreeCash flow to Firm(FCFF)

&ADiscount Rate Cost of Equity

· Basis: Theriskier theinvestment, thegreater is thecost of equity.

· Models:

CAPM: RiskfreeRate+ Beta(Risk Premium)

APM: RiskfreeRate+ SBetaj (Risk Premiumj): n factors

Cost of Capital

WACC= ke( E/ (D+E))

+ kd ( D/(D+E))

kd = Current Borrowing Rate(1-t)

E,D: Mkt Val of Equity and Debt

&agrowth pattern

t

g

Stable Growth

g

Two-Stage Growth

|

High Growth Stable

g

Three-Stage Growth

|

High Growth Stable

Transition](https://image.slidesharecdn.com/value-1-231006180057-fef1086c/85/value-1-ppt-87-320.jpg)

This document discusses different approaches to valuation, including their philosophical basis and advantages/disadvantages. It covers discounted cash flow valuation, relative valuation, and the efficient market hypothesis. Discounted cash flow valuation estimates intrinsic value by discounting expected future cash flows. Relative valuation compares asset prices to similar assets based on common variables. The efficient market hypothesis states markets are efficient with respect to available information and economic profits cannot be earned. Both valuation methods have advantages like forcing assumptions to be made explicit, but also disadvantages like sensitivity to input estimates.