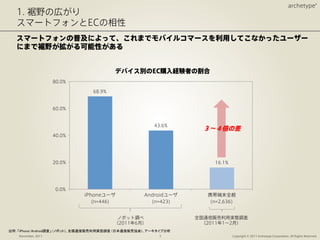

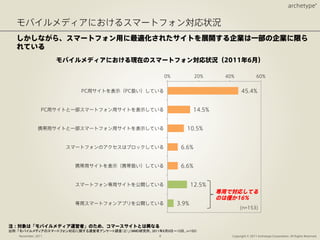

今後、モバイルコマース市場はスマートフォンの普及によってますます高いペースで拡大する可能性があります。スマートフォンの対応を急ぐ企業も増えてきました。 では、スマートフォン時代にはモバイルコマースをどのように考えれば良いのでしょうか?これまでと異なる点はどのようなところにあるのでしょうか? 今回はスマートフォンの登場によって、EC市場や人々の行動がどのように変化し、今後のスマートフォン・コマースに求められる要素を考えてみたいと思います。