Downloaded 43 times

![Important Definitions

1. Person [Sec 2(31)] :

The income tax is charged in respect of total income of the previous year of every

person. Here ‘person’ means,

a. Individual

b. Hindu Undivided Family [ HUF ]

c. Association of Persons [ AoP ] or Body of Individuals [BoI] whether incorporated or not

d. Company

e. Firm

f. Local Authority

g. Every Artificial Judicial Person [ AJP ] not falling in any of the preceeding categories](https://image.slidesharecdn.com/unit-1-tk-ppt-160726085511/85/Unit-1-tk-ppt-11-320.jpg)

![2. Assessee [ Sec 2(7) ] :

Income Tax Act,1961 defines ‘assesse’ as a person by whom any tax or any other sum of money is

payable under this Act, and includes,

* Every person in respect of whom any proceeding under this Act has been taken for the

assessment of his income or income of any other person in respect of which he is assessable,

or of the loss sustained by him or such other person, or the amount of refund due to him or to

such other person.

* Any Person who is deemed to be an assessee under any provisions of this Act.

* Any Person who is deemed to be an assessee in default under any provisions of the Act.](https://image.slidesharecdn.com/unit-1-tk-ppt-160726085511/85/Unit-1-tk-ppt-12-320.jpg)

![3. Assessment Year [Sec 2 (9)] :

• `Assessment Year’ means the period starting from April 1 and ending on March 31,

next year.

• Assessment year is the year immediately following the financial year wherein the

income of the Financial Year is assessed at the rates prescribed by relevant Finance

Act.

• In simple words, it is the year in which tax is payable on the income earned in

previous year. Ex: Current Assessment Year – 2016-17](https://image.slidesharecdn.com/unit-1-tk-ppt-160726085511/85/Unit-1-tk-ppt-13-320.jpg)

![4. Previous Year [Sec 3] :

“The year in which income is earned is known as Previous Year. Previous

Year is the Financial Year immediately preceding the Assessment Year.”

Ex: Previous Year - 2015-16

Notes : * All assessees are required to follow financial year ( i.e. Apr To Mar ) as

previous year.

* This previous year has to be followed for all sources of income

uniformly .](https://image.slidesharecdn.com/unit-1-tk-ppt-160726085511/85/Unit-1-tk-ppt-14-320.jpg)

![5. Income [Sec 2 (24)] :

Under Sec.2(24), the term “income” specifically include the following :

1. Profit & Gains

2. Dividend

3. Voluntary Contributions received by Trust

4. Perquisites in the hands of employees.

5. Any Special Allowance or benefit

6. City Compensatory Allowance/Dearness Allowance

7. Any benefit or perquisites to a director

8. Any benefit or perquisites to a representative assessee.

9. Any sum chargeable under section 28, 41 & 59.

10. Capital Gains

11. Insurance Profit

12.Banking income of a Co-operative Society

13.Winning from Lottery.

14. Employees Contributions towards provident fund

15. Amount received under Keyman Insurance Policy.

16.Amount exceeding Rs.50000/- by way of Gift received by an individual or HUF.](https://image.slidesharecdn.com/unit-1-tk-ppt-160726085511/85/Unit-1-tk-ppt-15-320.jpg)

![6. Gross Total Income [Sec. 14] :

As per Section 14, income of a person is computed under the following heads,

1. Salaries

2. Income from House Properties

3. Profits & Gains of Business or Profession

4. Capital Gains

5. Income from other Sources.

The aggregate income under these heads is termed as “ Gross Total Income”.](https://image.slidesharecdn.com/unit-1-tk-ppt-160726085511/85/Unit-1-tk-ppt-17-320.jpg)

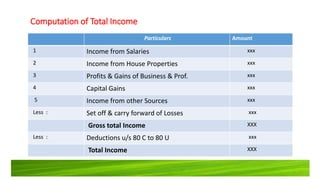

![7. Total Income [ Sec 2 (45) ] :

“` Total Income ’ means the total amount of income referred to in Section 5,

computed in the manner laid down in the Act.”

In other words, it is the income after allowing the deductions u/s 80 C to 80 U.](https://image.slidesharecdn.com/unit-1-tk-ppt-160726085511/85/Unit-1-tk-ppt-18-320.jpg)

The document discusses the history and evolution of income tax, tracing its origins from ancient civilization practices to modern-day India, where income tax was first introduced in 1860. It outlines important concepts such as direct and indirect taxes, definitions of key terms like 'assessees' and 'income', and the calculation of gross total and total income. The text emphasizes a structured approach to taxation that includes considerations of equity and justice, referencing historical texts like Manu Smriti and Kautilya's Arthashastra.