Downloaded 16 times

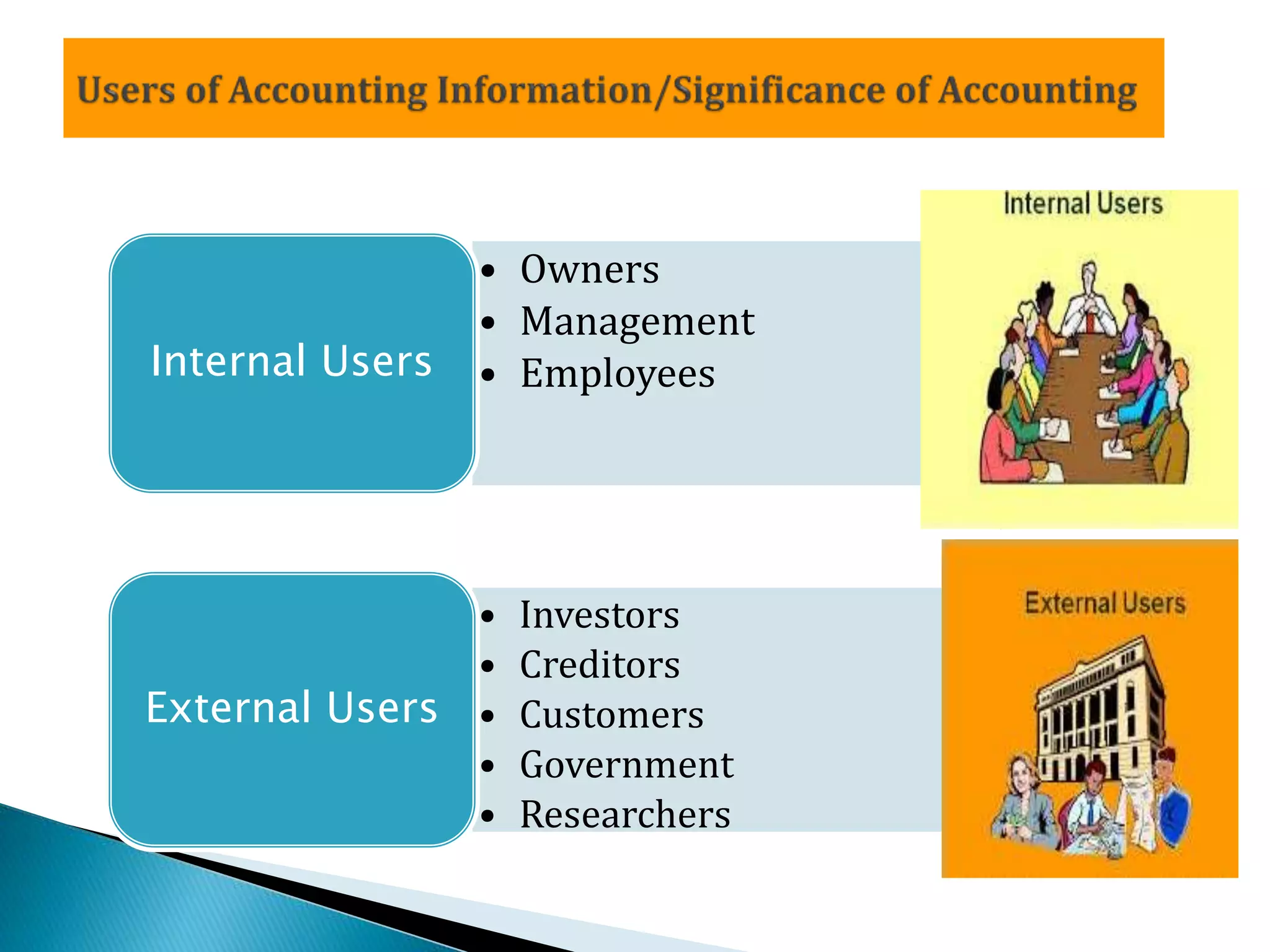

This document discusses the history and purpose of accounting. It notes that accounting originated in India thousands of years ago as described in the book "Arthashastra," and the modern double-entry system was first published by Luca Pacioli in 1494. The document defines accounting as recording, classifying, and summarizing financial information and transactions to facilitate decision making about a business. It outlines the objectives of accounting as maintaining records, meeting legal requirements, protecting assets, facilitating decisions, and communicating results to stakeholders.

![[000003]](https://cdn.slidesharecdn.com/ss_thumbnails/000003-120520101616-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)