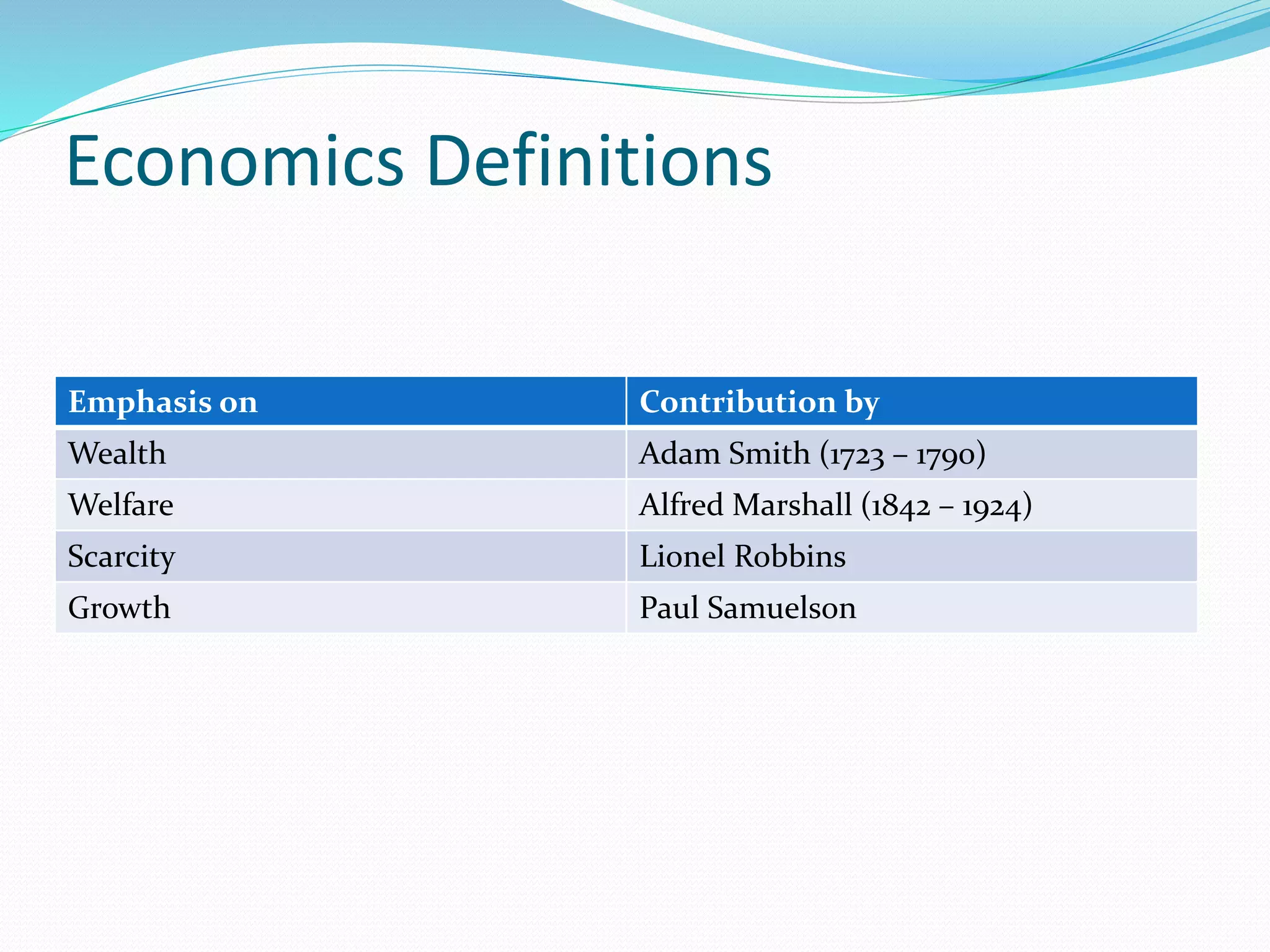

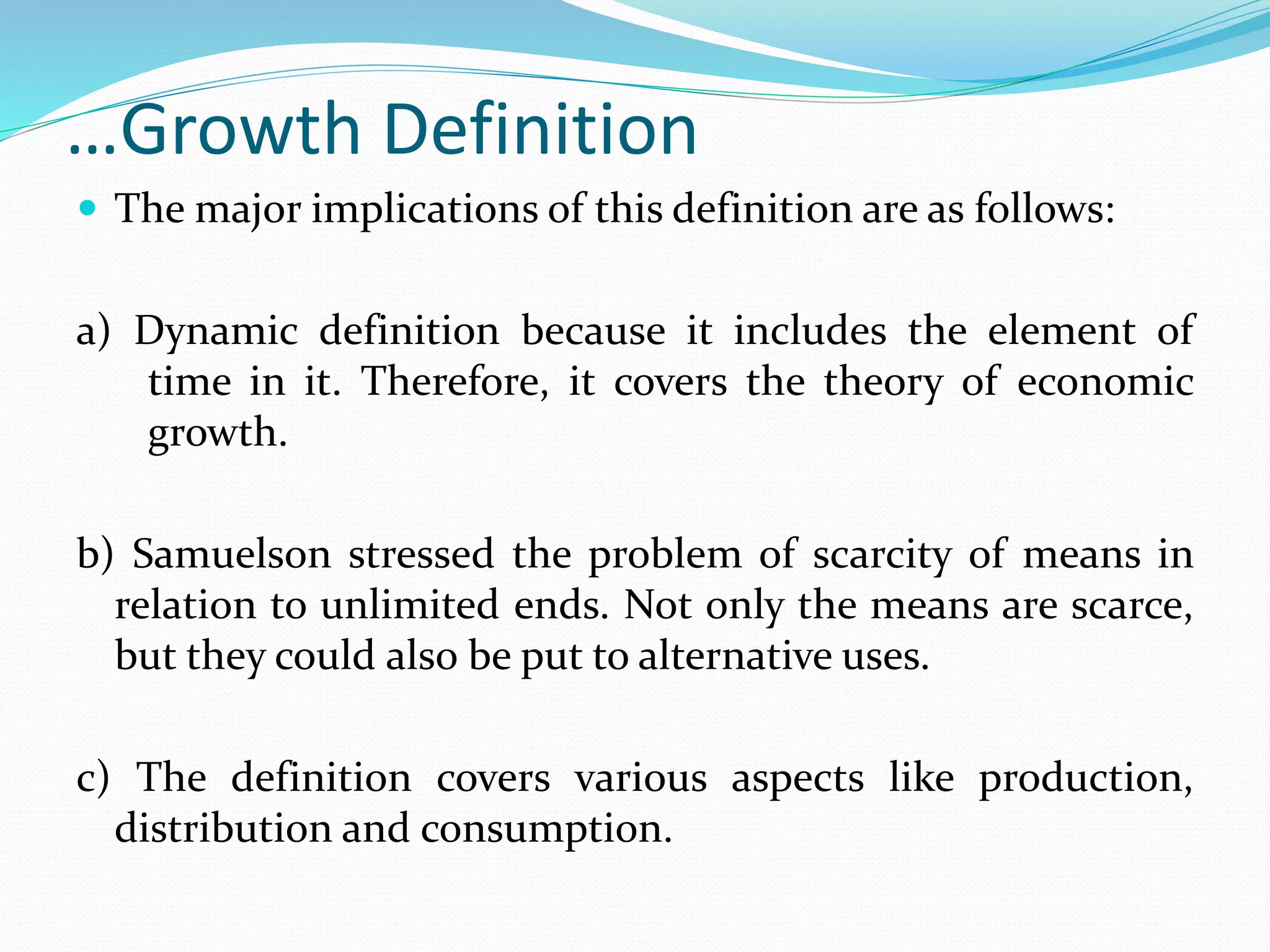

The document provides an overview of microeconomics and macroeconomics. It discusses key definitions and concepts in economics, including definitions of economics proposed by Adam Smith, Alfred Marshall, Lionel Robbins, and Paul Samuelson. It also summarizes the differences between microeconomics and macroeconomics. Microeconomics examines individual markets, firms, and consumer behavior, while macroeconomics analyzes aggregate economic indicators such as national income and output, inflation, and unemployment.